BBDC - Barings BDC: A Suboptimal Way To Play The BDC Exposure

2023-12-03 23:16:53 ET

Summary

- Barings BDC focuses on issuing private credit for middle-market businesses with a disciplined approach to asset selection.

- The portfolio is well-diversified, with a bias toward finance, insurance, tech, and service-oriented businesses.

- BBDC primarily relies on sponsor-backed investments but also allocates a portion to speculative deals with relaxed financial conditions. About 33% of the portfolio is exposed to riskier segments than second lien.

- In the past 5 quarters, the Company has increased its debt by ~20%, while experiencing a slight decline in its NAV and further pressures on the write-downs.

- While BBDC provides an attractive yield of 11.5% and is placed in a favourable segment, the underlying risk profile renders the investment case suboptimal.

Barings BDC ( BBDC ) is an externally managed business development company ("BDC") that mostly issues private credit for middle-market businesses. BBDC's investment objective is to capture high current income streams via a disciplined and fundamental approach to asset selection.

There are a couple of key investment criteria that BBDC follows when signing investments:

- EBITDA of $10 million to $75 million (on a TTM basis).

- Preferably private equity sponsor-backed.

- History of growth and profitability on the bottom line level.

- Strong market position and competitive differentiation.

- Covenants and structural protections.

Portfolio and key exposures

If we take a look at the portfolio and key exposure points, we will recognize that there is nothing exotic when it comes to BBDC's asset allocation. In other words, there are no specific areas of differentiation that would place BBDC out of the usual norm in the context of private credit peers.

BBDC 3Q23 Earnings Presentation

The portfolio itself is well diversified with a bit of a skew towards finance & insurance, tech, and service-oriented businesses. Again, this is very common for BDC companies to bias their exposures into finance and tech industries as typically these kinds of businesses struggle to access financing via conventional means (e.g., bank loans).

BBDC 3Q23 Earnings Presentation

What we could consider a slight deviation from the norm is that the concentration in the first lien is not that dominant compared to the typical practice of peers. Roughly 33% of the investments embody more unfavourable and inherently more risky positions than the first lien.

For instance, equity, JV, and structured products which in BBDC's case account for ~23% of the AuM generate, per definition, significantly more volatile income than fixed income securities such as those falling under first lien and second lien categories.

Typically, BDCs and investors want to avoid any positions that could render the overall portfolio and cash generation less predictable because the underlying business itself already entails a high degree of irrespective whether it is put under first lien or not.

What is else that is rather BBDC specific is the mechanics of how the Company sources new deals. There are three ways how deal origination takes place at BBDC:

- Sponsor backed , where the financing is made for companies that are owned and backed by private equity firms (and also originated by BBDC).

- Non-sponsored investments , where the financing is made irrespective of the ownership.

- Platform investments , where BBDC invests in two originators of uncorrelated middle market first-lien loans.

For the first and second categories, the key covenants are the same and entail a relatively high degree of protection (e.g., LTV below 50%). The third category, however, is quite speculative with LTV up to 80%.

BBDC 3Q23 Earnings Presentation

Looking back at the proportions of how investments have been made across the three aforementioned categories, we can notice that BBDC tries to mostly rely on sponsor-backed cases to avoid the assumption of potentially dangerous risk.

With that being said, BBDC still invests roughly 10% of the total quarterly volumes into the third category (i.e., the speculative one), where the requirements for solid financial conditions of businesses are more relaxed.

Thesis

All in all, BDCs have become increasingly attractive vehicles for investors, where to place part of their money. During tight monetary conditions and increased uncertainty in the economy, access to credit is by definition more constrained. This, in turn, imposes favourable tailwinds for BDCs to act by providing well-needed credit.

Plus, now when the SOFR is so high, the private credit flows have become rather attractive for yield-seeking investors. To put it differently, most of the first-lien and second-lien private credit investments by BDCs are made on variable debt terms (e.g., fixed margin + SOFR). In the context of 5.3% SOFR and generally high fixed margins (due to elevated credit risk), BDC loans can indeed get very appealing.

This is also the case for BBDC as almost the entire first and second lien exposure is based on floating debt. For example, as of Q3, 2023, the weighted-average portfolio yield stood at 11.2%.

{kind=link}

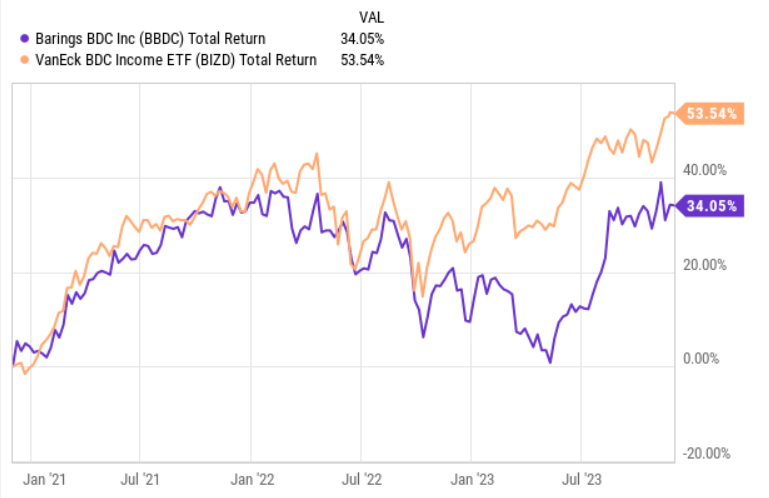

As we can see in the chart above, over the past 3-year period BBDC has performed well (on a total return basis). This is in line with the current structural dynamics that clearly favour BDC space, as I mentioned above.

With that being said, now we come to a point, where I have to elaborate a bit on why, in my view, BBDC is suboptimal investment despite the positive (for BDCs) macroeconomic backdrop. I also think that this is the main reason why BBDC has lagged behind the overall U.S. BDC universe.

There are three issues:

- Unfavourable leverage. Just over the past 5 quarters, BBDC has increased its indebtedness by ~20% (from net debt to equity of 0.99x to 1.18x). In the meantime, the NAV per share has declined by $0.03 and the dividend has remained more or less stable.

- Poor quality portfolio. As indicated above, approximately one-third of BBDC's exposure is placed outside the first or second lien universe, into securities that per definition do not provide (and do not have to) stable streams of incoming cash. We can also notice this by looking at the recent accruals, which have quite consistently ticked higher going from 0.7% in Q3, 2022 to 1.6% in Q3, 2023. Putting on top of this the fact that BBDC has in the same period become considerably more levered, the picture does not seem that good.

- Consequences from debt rollover. BBDC just as any other BDC has attracted external leverage to fund new investments. In BBDC's case, the overall debt structure is very solid with almost no maturities until 2026 and most of the loans being priced against fixed rates (~4.5%). The issue here is that even with the favourable external financing, BBDC has not been able to increase its NAV in a notable manner. The bigger issue is, however, that BBDC will have to refinance these proceeds in 2026 at potentially higher interest rates which would introduce a direct downward pressure on the current cash generation. Granted, nobody knows where the interest rates will be so far in the future, but under a situation of these high interest rates, BBDC's dividend would be clearly underwater after a refinancing event.

The bottom line

While, in my opinion, there is a material merit of allocating part of portfolio into BDC structures to capture the opportunities in the private credit markets and enjoy relatively high yields, BBDC is not an optimal choice.

The fact that BBDC puts so high reliance on riskier segments than first or second lien and by looking at the recent dynamics within the operating KPIs (e.g., increased write-downs, higher leverage with a drop in NAV), at least to me, renders the investment case too risky. Plus, there is a meaningful risk of suffering negative consequences from rollover of the external debt position in 2026 in case the interest rates remain this high.

At the same time, I would not short BBDC just because of the structural tailwinds that the entire BDC segment is currently exposed to.

For further details see:

Barings BDC: A Suboptimal Way To Play The BDC Exposure