GTES - Barnes Group: Attractive Upside Despite Some Bumps On The Road

- Barnes Group has not fared particularly well recently, as mixed fundamental performance has hindered investor enthusiasm.

- The company likely deserved a bit of pain, but shares are now looking quite cheap.

- Ultimately, upside for investors could be attractive down the road and investors would be wise to consider a stake in the firm.

One thing that I have found to be true about investing is that, sometimes, it can take a long while for a particular call to play out as expected. One great example of this can be seen by looking at Barnes Group ( B ), a company that focuses largely on the industrial and aerospace markets. Although I had previously rated the company a 'buy', reflecting my belief that it would generate returns that outperform the broader market, shares in recent months have disappointed. Some of this pain has been driven by the fact that some fundamental performance of the enterprise has not been particularly robust. But given how cheap shares are today, I do believe that upside potential is still on the table. The only thing I believe now is that it would take a little more patience than I previously anticipated. But with how shares are priced today, it is possible that now may make sense to buy in even more if you are still bullish on the firm.

Times have been tough

Back in November of 2021, I wrote an article that took a bullish take on Barnes Group. In that article, I acknowledged that the company had experienced some pain during the pandemic. At the same time, however, I said that the fundamental picture for the firm was improving. I lauded the company's significant customer base and said that the outlook for the long term was solid. I also concluded that shares were attractively priced at that time, leading me to rate the company a 'buy'. Unfortunately, things have not gone exactly as planned. Instead of outperforming the market, shares have underperformed. While the S&P 500 is down by 11.8% since the publication of that article, shares of Barnes Group have generated a loss for investors of 19.8%.

{kind=link}

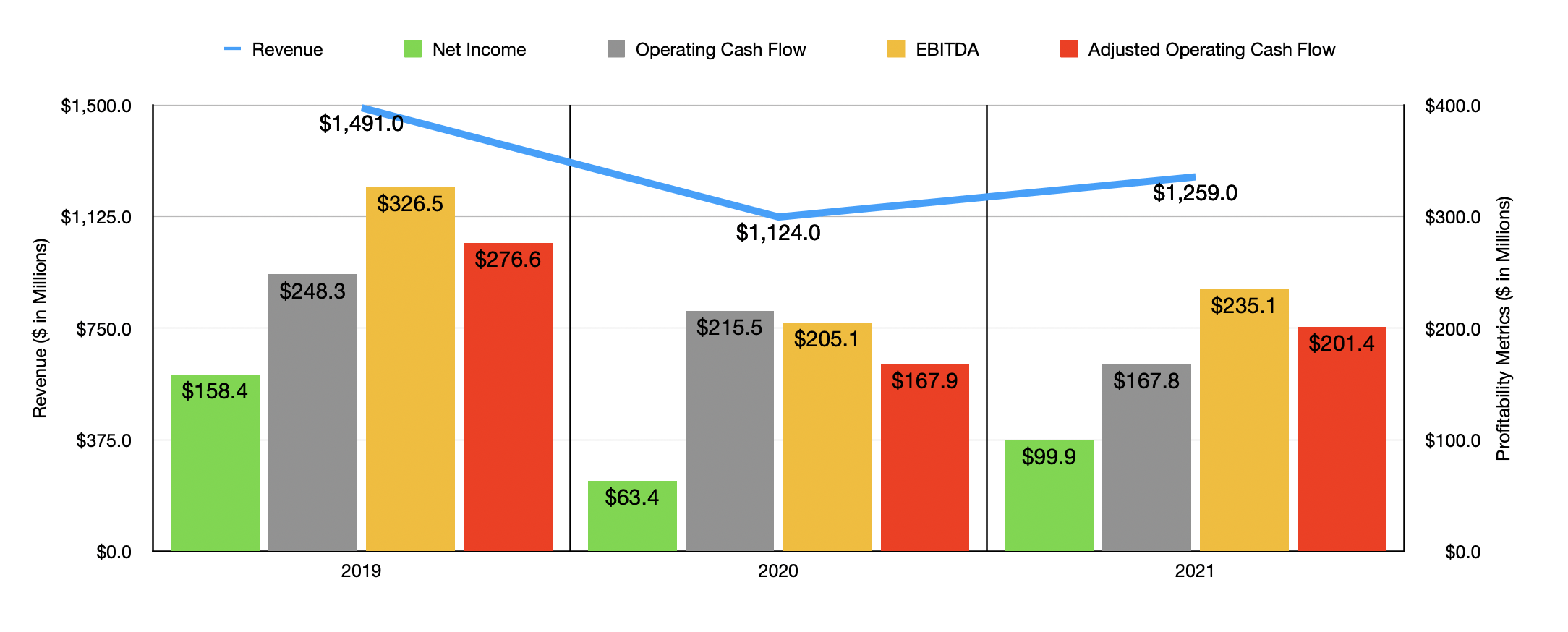

In the short term, I would say that some of this pain might have been warranted. After all, the company has ceased improving and seems to be hovering around where it was the same time last year. In some ways, the fundamental picture is even worse. Consider, for instance, how the company ended its 2021 fiscal year . Sales for that year came in at $1.26 billion. That was slightly higher than the $1.12 billion generated in 2020. At the same time, it still marked a sizable downturn from the $1.49 billion the company achieved in 2019. Net income of $99.9 million was better than the $63.4 million achieved in 2020. But it still was lower than the $158.4 million generated in 2019. Operating cash flow went from $215.5 million in 2020 down to $167.8 million last year. But if we adjust for changes in working capital, it would have risen from $167.9 million to $201.4 million. Meanwhile, EBITDA increased from $205.1 million to $235.1 million.

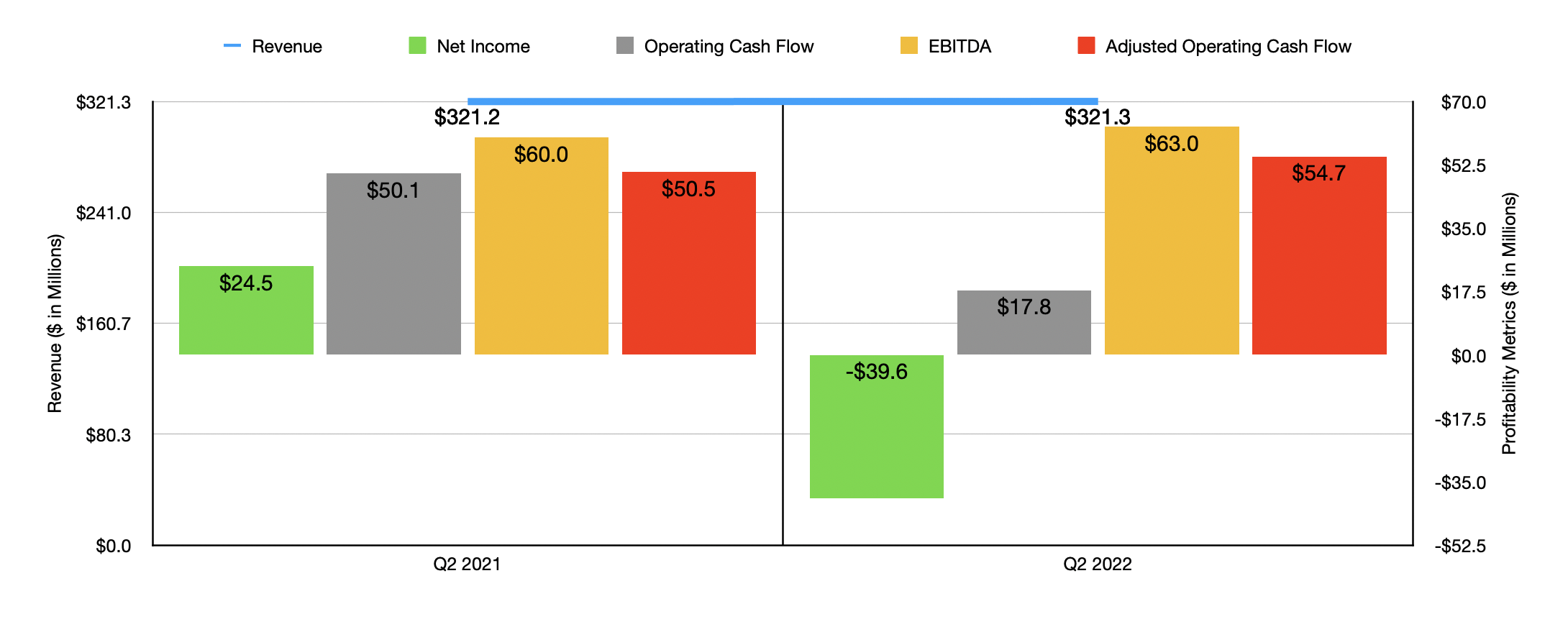

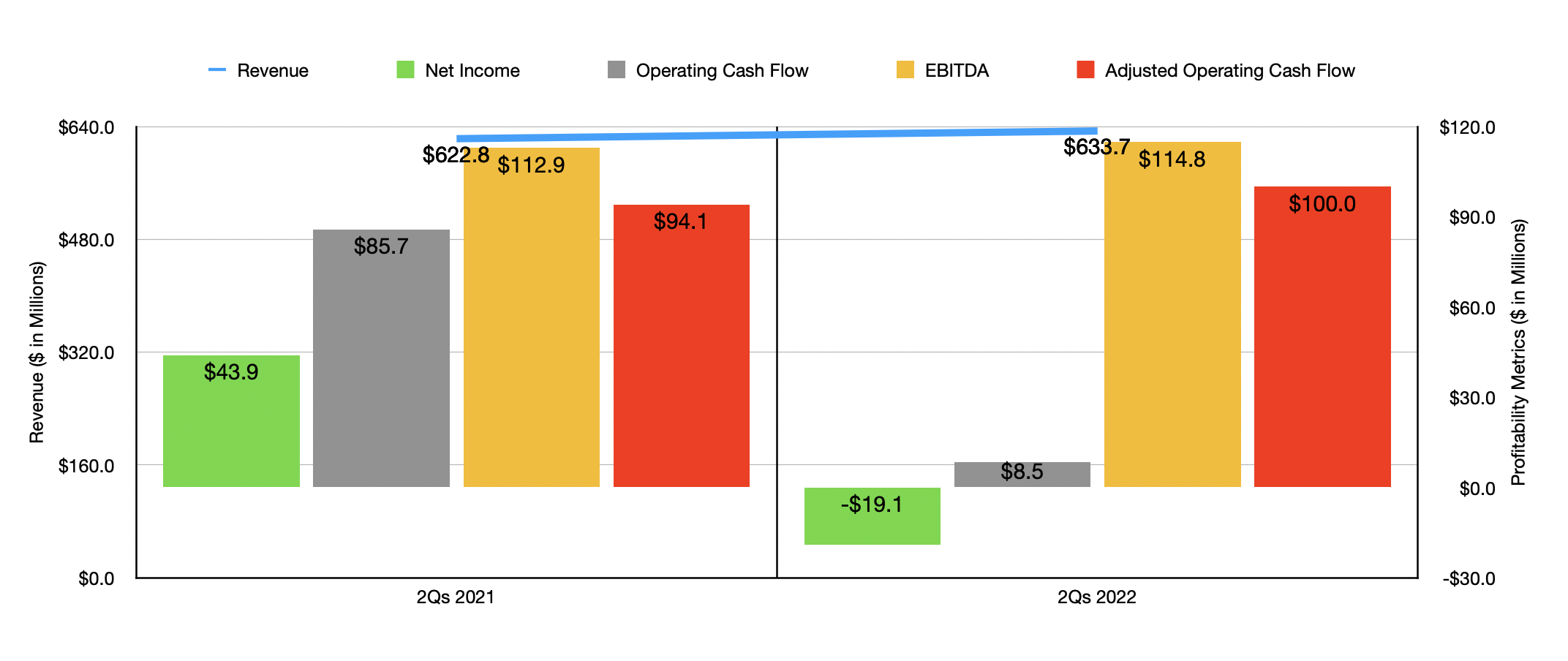

Although the general picture here was positive, the company has hit something of a roadblock this year. Due to difficult market conditions, revenue has virtually flatlined. In the latest quarter of the year , the second quarter of 2022, sales of $321.3 million were only $100,000 higher than what they were the same time last year. For the full year-to-date timeframe, sales of $633.7 million translated to a modest 1.8% rise over the $622.8 million generated the same time of the company's 2021 fiscal year.

{kind=link}

We also have the issue of profitability. In the latest quarter, the company generated a net loss of $39.6 million. That's down from the $24.5 million generated the same time one year earlier that has brought the total net profit for the company for the first half of the year down to a negative $19.1 million compared to the $43.9 million profit achieved in the first half of 2021. Operating cash flow also declined, dropping from $50.1 million to $17.8 million, taking the year-to-date figure down from $85.7 million to $8.5 million. If we adjust for changes in working capital, at least, the picture does look better. Using this approach, the metric rose from $50.5 million in the second quarter of last year to $54.7 million the same time this year, while for the first six months it rose from $94.1 million to $100 million. A very similar trend can be seen when looking at EBITDA, as the charts above and below both illustrate.

{kind=link}

When it comes to the 2022 fiscal year as a whole, management expects organic revenue to rise by between 5% and 6% year over year. However, much of this would be offset by a 3% hit caused by foreign currency fluctuations. Despite the sales increase, earnings per share should be between $1.90 and $2.05, implying anything from a 2% drop to a 6% increase year over year. This excludes a $0.27 per share hit caused by restructuring costs this year and a $1.33 per share impairment charge. The company has also been negatively impacted by increased raw material, utility, labor, and freight costs because of inflation and supply chain issues.

{kind=link}

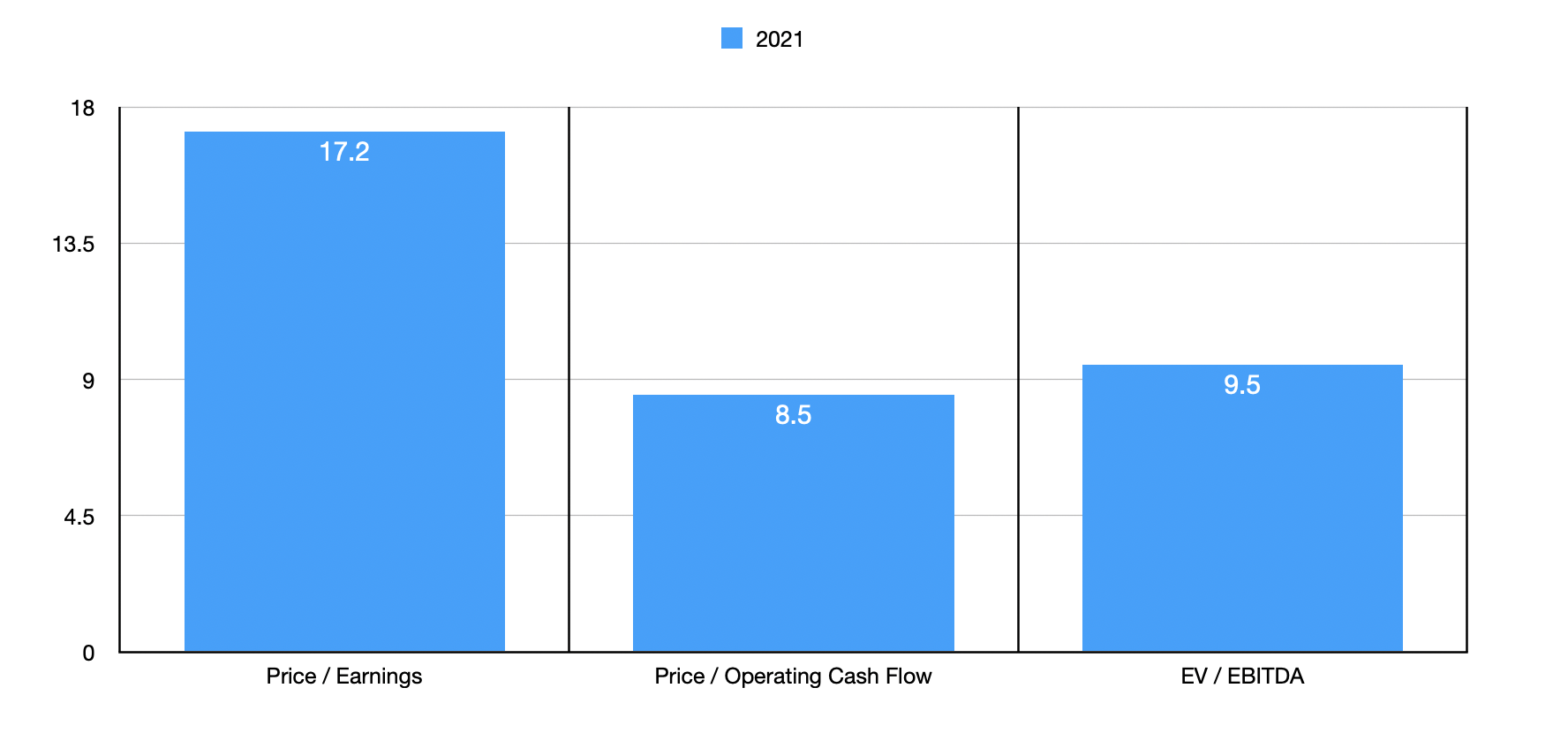

Regardless, if we take management guidance seriously, the adjusted earnings for the company should come out to $99.8 million. That's virtually identical to the $99.9 million generated in 2021. Because of how close this is, I have decided to just value the company based on 2021 results. Doing so, we end up with a price-to-earnings multiple of 17.2. The price to adjusted operating cash flow multiple should be 8.5, while the EV to EBITDA multiple should come in at 9.5. As part of my analysis, I also compared the company to the same five firms I compared it to in my last article. On a price-to-earnings basis, these companies ranged from a low of 5.8 to a high of 27.7. In this case, three of the five companies were cheaper than Barnes Group. Using the price to operating cash flow approach, the range was from 7.5 to 21.7, while using the EV to EBITDA approach, the range was from 4.2 to 11.3. In both cases, only one of the five companies was cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Barnes Group |

| 17.2 |

| 8.5 |

| 9.5 |

| Mueller Industries ( MLI ) |

| 5.8 |

| 7.5 |

| 4.2 |

| Mueller Water Products ( MWA ) |

| 27.7 |

| 21.7 |

| 11.3 |

| Crane Holdings Co ( CR ) |

| 10.8 |

| 17.9 |

| 10.4 |

| Standex International ( SXI ) |

| 18.9 |

| 14.6 |

| 9.8 |

| Gates Industrial Corporation ( GTES ) |

| 14.1 |

| 11.5 |

| 9.6 |

Takeaway

Although the fundamental picture for Barnes Group has stopped improving for the most part, shares of the enterprise do still look pretty cheap. I fully suspect that current market conditions will continue to weigh on the business for at least the rest of this year. And because of that, some downside was probably warranted. But on the whole, I feel like the market has overreacted to the troubles the company is facing. Shares are cheap and, at some point, the markets in which it operates will improve. And when that does come to pass, the upside for investors could be quite attractive. Because of that, I am keeping my 'buy' rating on the company for now.

For further details see:

Barnes Group: Attractive Upside Despite Some Bumps On The Road