TW - Baron FinTech Fund Q2 2023 Quarterly Letter

2023-08-16 13:00:00 ET

Summary

- Baron is an asset management firm focused on delivering growth equity investment solutions known for a long-term, fundamental, active approach to growth investing.

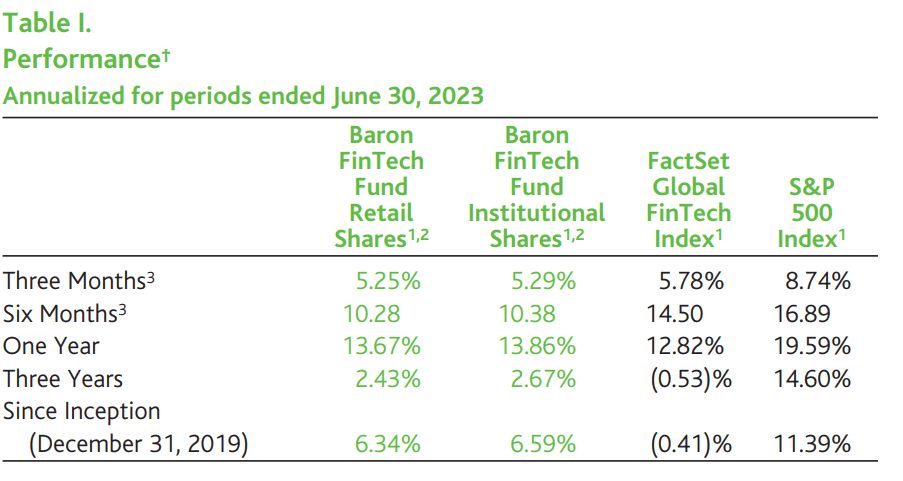

- In the quarter ended June 30, 2023, Baron FinTech Fund rose 5.29% compared with a 5.78% gain for the FactSet Global FinTech Index.

- During the second quarter, Fund performance was solid but just shy of the Benchmark.

- Stock selection in Enterprise Software, Capital Markets, and Tech-Enabled Financials coupled with unique exposure to Digital IT Services were detractors during the quarter.

Performance

In the quarter ended June 30, 2023, Baron FinTech Fund® (the Fund) rose 5.29% (Institutional Shares) compared with a 5.78% gain for the FactSet Global FinTech Index (the Benchmark). Since inception (December 31, 2019), the Fund has risen 6.59% on an annualized basis compared with a 0.41% decline for the Benchmark.

{kind=link}

Performance listed in the above table is net of annual operating expenses. The gross annual expense ratio for the Retail Shares and Institutional Shares as of December 31, 2022, was 1.63% and 1.20%, respectively, but the net annual estimated expense ratio was 1.20% and 0.95% (net of the Adviser's fee waivers), respectively. The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate; an investor's shares, when redeemed, may be worth more or less than their original cost. The Adviser reimburses certain Fund expenses pursuant to a contract expiring on August 29, 2033, unless renewed for another 11-year term and the Fund's transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month end, visit www.BaronFunds.com or call 1-800-99BARON.

U.S. equities rallied for a third consecutive quarter, supported by easing inflation, a pause in the Federal Reserve's rate hiking cycle, Congress' successful avoidance of the debt ceiling cliff, waning concerns of a banking crisis, earnings optimism, and economic reports substantiating the "soft landing" narrative. Market leadership remained narrow with a few large technology companies accounting for most of the recent gains in the major market indexes, driven by excitement over their potential ability to gain from widespread adoption of artificial intelligence ((AI)). This was most evident in the performance of the NASDAQ Composite Index, where the seven largest companies by market cap (Apple, Microsoft, NVIDIA, Amazon, Alphabet, Meta, and Tesla) were mostly responsible for the Composite's strong performance.

During the second quarter, Fund performance was solid but just shy of the Benchmark. Two-thirds of holdings generated positive returns. Three of the Fund's seven investment themes outperformed the Benchmark: Payments, Information Services, and E-Commerce. The investment themes that underperformed were Enterprise Software, Capital Markets, Tech-Enabled Financials, and Digital IT Services. Leaders outperformed Challengers (up 6.9% vs. up 2.6%, respectively). Growth outperformed value by a wide margin to extend its advantage for the year. Small- and mid-cap stocks remained out of favor, trailing their large-cap counterparts for a fourth consecutive month.

Within Payments, lower exposure to this underperforming category coupled with strong performance from Network International Holdings plc ( NWITY ) aided performance. Shares of Network, a leading payment processing company operating in the Middle East and Africa, were up sharply after the company agreed to be acquired by a private equity firm. Strength in Information Services was broad-based, led by double-digit gains from rating agency and data provider S&P Global Inc. and real estate data and marketing platform CoStar Group, Inc. ( CSGP ) S&P Global was the largest contributor due to rebounding debt issuance and stronger equity markets. CoStar performed well after reporting robust financial performance, with new sales growing 18% in the first quarter. Multifamily bookings strength offset weaker results in the company's commercial real estate business, and the nascent residential offering is showing early signs of traction. Shopify Inc. ( SHOP ) drove most of the relative gains in E-Commerce as the company's shares continued their upward trajectory from the prior quarter. The company's quarterly results were solid, with 15% growth in gross merchandise value and 25% growth in revenue driven by growing adoption of its merchant solutions. In addition, the sale of its capital-intensive logistics business to Flexport was well received by investors. We believe the sale should improve margins and allow Shopify to focus on its core strengths: its best-in-class software and leading commerce ecosystem. The Fund also benefited from its lack of exposure to Hardware, which was the worst performing category in the Benchmark.

Stock selection in Enterprise Software, Capital Markets, and Tech-Enabled Financials coupled with unique exposure to Digital IT Services were detractors during the quarter. Within Enterprise Software, lower exposure to this well performing theme combined with share price declines from investment management analytics provider FactSet Research Systems Inc. ( FDS ) and property and casualty insurance software vendor Guidewire Software, Inc. ( GWRE ) weighed on performance. Despite reporting solid quarterly results, FactSet's stock fell as economic uncertainty led to slower growth in subscription revenue. We believe this is a temporary phenomenon that shouldn't impact FactSet's long-term growth prospects. Guidewire detracted from performance after announcing mixed quarterly results related to the timing of near-term revenue and cash flow. We remain optimistic about Guidewire because it is far along on its cloud migration journey and is demonstrating more consistent recurring revenue growth and gross margin expansion. Electronic trading platforms MarketAxess Holdings Inc. ( MKTX ) and Tradeweb Markets Inc. ( TW ) were mostly responsible for stock-specific weakness in Capital Markets after their shares were impacted by a slowdown in trading activity. Performance in Tech-Enabled Financials was adversely impacted by insurer The Progressive Corporation ( PGR ), as higher claims costs weighed on profitability. We believe margins will improve as premium rates climb and inflation moderates. The Fund's active exposure to Digital IT Services was a drag on performance due to underperformance from outsourced software development provider Endava plc ( DAVA ). After many years of strong growth, revenue is slowing as economic uncertainty causes customers to cut back on IT spending. We believe this is a temporary headwind and expect growth to improve next year as businesses continue to modernize and digitize to better serve their customers.

{kind=link}

Shares of rating agency and data provider S&P Global Inc. rose due to rebounding debt issuance and stronger equity markets. Following steep declines last year, non-financial corporate bond issuance was up double digits during the quarter as issuers got more comfortable with higher interest rates and some macro concerns abated. Solid equity market performance benefited asset-based fees, while continued strength in derivatives trading further bolstered Indices revenue. The integration of the IHS Markit acquisition is progressing well, with the company having already achieved over 90% of targeted cost synergies. We continue to own the stock due to the company's long runway for growth and significant competitive advantages.

Network International Holdings Plc is a leading payment processing company operating in the Middle East and Africa. Shares spiked in April after the company received two takeover offers from private equity firms. Following a period of due diligence and negotiation, Network's Board agreed in June to be acquired by Brookfield Asset Management for £4.00 per share, representing a 64% premium to the share price before takeover speculation began. Brookfield plans to combine Network's operations with another Middle Eastern payment processor, Magnati, that it acquired last year to create a regional powerhouse. We exited our position after the share price rose close to the acquisition price.

Shares of Fair Isaac Corporation (FICO), a data and analytics company that helps predict consumer behavior, contributed to performance. The company reported solid quarterly financial results and modestly raised its full-year outlook while taking a more conservative approach to guidance due to macroeconomic uncertainty. CEO Will Lansing sounded confident that the business can hold up well across various macro backdrops and sounded particularly excited about the momentum in the software business. We retain conviction and believe that FICO will be a steady earnings compounder, which should drive solid returns for the stock over the long term.

{kind=link}

Shares of MSCI Inc. ( MSCI ), a leading provider of investment decision support tools, detracted from performance. The company reported steady first quarter earnings results and reiterated its outlook for 2023. The stock's decline was driven by: (1) weaker new sales activity in ESG due to the political environment in the U.S. and some regulatory updates in the EU around classifying ESG funds; and (2) broader macro uncertainty starting in late March, leading to a tightening of client budgets, lengthening of sales cycles, and higher cancelations from smaller clients. Despite some near-term uncertainty, we believe that business fundamentals remain sound, and we retain conviction that MSCI owns durable, "all weather" franchises that should enable the company to compound earnings at a double-digit rate for many years.

Endava plc provides outsourced software development for business customers. Shares fell due to a pullback in customer demand in March following multiple bank failures. Management reduced financial guidance for the June quarter to reflect greater macroeconomic uncertainty and lower revenues from private equity-backed companies, which represent about 20% of its business. Sales activity has since rebounded, which supports management's view that the current slowdown is temporary and demand for digital transformation should persist. Management believes generative AI will be a tailwind for its business by stimulating more demand to build AI tools for customers and increasing internal efficiency to free up resources for additional projects. We continue to own the stock because we believe Endava will continue gaining share in a large global market for IT services.

MarketAxess Holdings Inc. operates the leading electronic platform for trading corporate bonds. Weak performance during the quarter was driven by a decline in trading activity. Following a strong start to the year, trading volumes slowed in March due to short-term dislocations in the regional banking sector and remained subdued due to lower credit spread volatility. Interest rate movements and product mix shifts have also pressured its variable fee rate, leading to lower-than-expected revenue. We continue to own the stock because we believe MarketAxess will benefit from the secular shift to electronic trading in the corporate bond market.

Portfolio Structure

We seek to invest in competitively advantaged, growing fintech companies that we can own for years. We conduct independent, fundamental research and take a long-term perspective. We invest in companies across all market capitalizations and geographies. The quality of the ideas and level of conviction determine the position size of each investment. We do not try to mimic an index, and we expect the Fund will look very different from the Benchmark.

As of June 30, 2023, the Fund held 46 positions. The Fund's 10 largest holdings represented 39.8% of net assets, and the 20 largest holdings represented 66.0% of net assets. International stocks represented 14.7% of net assets. The market capitalization range of the investments in the Fund was $661 million to $499 billion with a median of $23.0 billion and a weighted average of $93.1 billion. The Fund's active share versus the Benchmark was 87.2%.

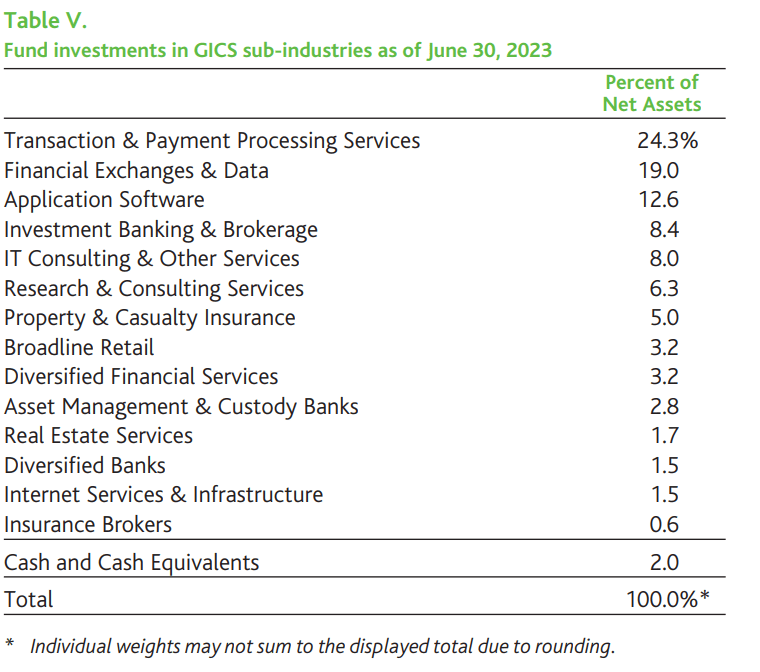

We segment the Fund's holdings into seven investment themes. As of June 30, 2023, Information Services represented 22.5% of net assets, Tech- Enabled Financials represented 19.8%, Payments represented 19.4%, Enterprise Software represented 12.7%, Capital Markets represented 8.8%, Digital IT Services represented 8.0%, and E-Commerce represented 6.6%, with the remainder in cash. Relative to the Benchmark, the Fund is most underweight in Enterprise Software and Payments, and has overweight positions in Capital Markets, Digital IT Services, Tech-Enabled Financials, Information Services, and E-Commerce.

We also segment the Fund's holdings between Leaders and Challengers. Leaders are generally larger, more established companies with stable growth rates, higher margins, and moderate valuation multiples. Challengers are generally smaller, earlier-stage companies with higher growth rates, lower margins, and higher valuation multiples. As of June 30, 2023, Leaders represented 73.4% of net assets and Challengers represented 24.6%, with the remainder in cash.

{kind=link}

{kind=link}

Recent Activity

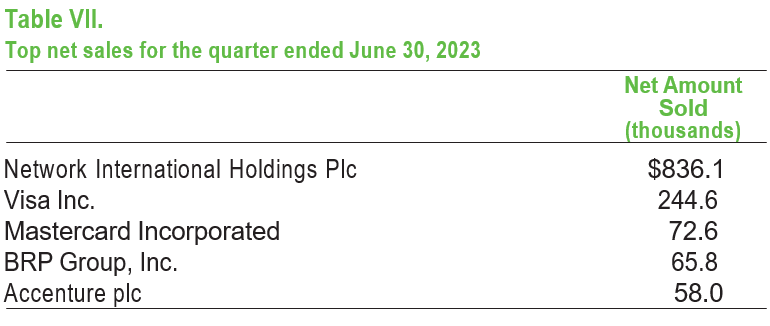

During the quarter, we initiated one new position and exited one position. Below we discuss some of our top net purchases and sales.

{kind=link}

We initiated a position in Nu Holdings Ltd. ( NU ) (dba Nubank), a Latin American digital bank with operations in Brazil, Mexico, and Colombia. Nubank was founded in 2014 with a mission to provide Brazilian consumers with better and more convenient access to financial products. The financial services industry in Brazil operates as an oligopoly, where the top five banks control a large majority of assets and deposits. This has historically led to high fees, poor customer service, and limited access to basic products such as credit cards and loans for the mass market. Nubank is disrupting this market via its digital distribution and intense focus on user experiences, which have enabled it to reach over 80 million registered users (almost half of the Brazilian adult population) in less than 10 years with very little marketing. We believe Nubank has four key competitive advantages driving its success: a user-friendly technology-driven platform, a track record of conservative credit underwriting, a low-cost funding base consisting mainly of retail deposits, and strong brand awareness. The company is led by co-founder and CEO David Vélez, who is also the company's largest shareholder.

We have followed Nubank through its late-stage private financing rounds and IPO in 2021. We saw the company navigate a difficult COVID period with superior asset quality while achieving scale and profitability much faster than investors anticipated. The company swung to profitability in the first quarter of this year with a 10% ROE driven by 87% revenue growth and strong operating leverage. Nubank has been rapidly scaling its business while launching new products and entering new markets such as Mexico and Colombia. In Brazil, the company has already reached 10% share of the credit card market. We believe Nubank will achieve similar penetration in newer products and geographies given the attractiveness and convenience of its platform, thereby driving significant asset growth. We believe the company's ROE will expand from 10% currently to 25% or 30% over the next few years driven by operating leverage and balance sheet optimization (better asset mix and higher leverage). We expect the combination of strong earnings growth and ROE expansion will drive meaningful share price appreciation over time.

{kind=link}

We sold Network International Holdings Plc after the company received multiple offers to be acquired by private equity firms. The winning bid represented a 64% premium to the share price before the takeover speculation began. Given limited upside after the shares spiked and traded near the takeover price, we exited the position.

We modestly trimmed Visa Inc. ( V ) , Mastercard Incorporated ( MA ), and Accenture plc ( ACN ) to manage the position sizes and raise capital to fund purchases elsewhere. These stocks remain full-sized positions and high-conviction ideas in the Fund.

Outlook

Concerns about a banking crisis appear to be fading after the failures and takeovers of SVB Financial, Signature Bank, and First Republic Bank. Quick action by regulators to guarantee deposits and expand liquidity reinforced confidence in the banking system and stemmed the deposit flight. Bank industry earnings in the second quarter have been solid against a low bar, led by more resilient deposits and better-than-feared deposit mixes. However, fundamental headwinds remain for many banks due to slowing loan growth, rising deposit costs, net interest margin pressure from an inverted yield curve, and potentially more onerous capital and liquidity requirements. The Fed's most recent Senior Loan Officer Survey from April showed tighter standards across business and consumer loan categories compared to the prior quarter, a continuation of trends that began last year. We are mindful of the potential for higher credit losses from commercial real estate and other potential headwinds from the rapid rise in interest rates over the last 15 months.

Nevertheless, the outlook for technology spending by financial institutions remains bright, which should benefit our fintech holdings. Jack Henry & Associates, Inc. ( JKHY ), a provider of core systems software for financial institutions, surveyed 118 small banks and credit unions from January through March who expect their technology spending this year to rise by 7% on average. 79% of respondents will spend more on technology, with the top priorities being growing loans, growing deposits, and increasing operational efficiency. Investment bank Baird conducted a more recent mid-year survey of 48 small banks and credit unions in the aftermath of the bank failures, and the results showed minimal change in IT spending expectations from the beginning of the year. Respondents expect about 5% spending growth with their core processor, a slight acceleration from last year and near the high end of the historical range observed over the 14 years that Baird has been doing this survey. 82% of respondents said spending expectations were stable or up since the beginning of the year, and most haven't seen any change in deposit activity. Community banks and credit unions have been more insulated from deposit pressures at mid-sized regional banks, likely due to smaller account sizes and more loyal customers.

Tighter lending standards by banks may create more opportunities for private credit providers, such as Apollo Global Management, Inc. ( APO ), Ares Management, Blackstone, and KKR. These lenders operate outside of the banking system to make loans to mostly privately held, middle-market companies. Instead of relying on bank deposits that can be withdrawn daily and are susceptible to runs and repricing, non-bank lenders fund loans using committed capital from investment vehicles, life insurance policies, and annuities that is more stable with a more predictable cost. This enables better asset-liability duration matching and reduces risk for multi-year loans against illiquid assets. Private credit is one of the fastest-growing segments in the lending landscape with close to $1.3 trillion in assets under management, having tripled in the last 10 years and expected to exceed $2 trillion in five years, according to Moody's Corporation ( MCO ). As banks tighten credit standards and potentially face more onerous regulations, non-bank lenders will likely capture additional market share with attractive risk-adjusted returns. Jamie Dimon noted on JPMorgan's recent earnings call that higher bank capital requirements is "great news" for private credit lenders who will be "dancing in the streets" as commercial lending moves out of the banking system. We expect Apollo Global will continue to benefit from growth in the private credit market. Additionally, elevated yields and the prospect of the Fed nearing the end of its rate hiking cycle makes fixed income an attractive asset class for investors, which should also benefit traditional asset managers with fixed income exposure such as BlackRock Inc. ( BLK ).

Another fintech industry trend we're seeing is a pickup in M&A activity, most notably in the payments sector. The year started with Nuvei's

$1.3 billion acquisition of Paya announced in January. In April, Network International received an initial takeover offer from a group of private equity firms, which was then topped by Brookfield Asset Management whose

$2.8 billion offer was accepted by the Board in June. Following reports earlier this year of a bidding war between Visa Inc. and Mastercard Incorporated to acquire cloud-based issuer processor and core banking software provider Pismo, Visa announced its intention to acquire the Brazilian company for $1 billion in late June. In early July, Fidelity National Information Services (FIS) agreed to sell a majority stake in its payment processing business Worldpay to private equity firm GTCR at an $18.5 billion valuation, effectively undoing FIS's $43 billion acquisition of Worldpay in 2019. Investment company Prosus is seeking to sell Dutch payment firm PayU for an estimated value exceeding $500 million. We believe this flurry of acquisitions suggests that valuations have fallen to attractive levels for many fintech companies, both public and private, and that well-capitalized strategic and financial buyers will continue to opportunistically invest in the sector. Meanwhile, funding for earlier-stage fintech startups fell to the lowest level since 2017. According to CB Insights, global fintech funding in the second quarter fell 64% from a year ago with deal count down 42%. Less capital going into the fintech sector should benefit our publicly traded incumbents by reducing competitive intensity, improving industry profitability, and providing opportunities for strategic acquisitions with attractive returns.

Thank you for investing in Baron FinTech Fund. We are optimistic about the Fund's prospects and remain significant shareholders alongside you.

Sincerely,

Josh Saltman, Portfolio Manager

Footnotes

† The Fund's 3-year historical performance was impacted by gains from IPOs and there is no guarantee that these results can be repeated or that the Fund's level of participation in IPOs will be the same in the future.

1 The FactSet Global FinTech Index ™ is an unmanaged and equal-weighted index that measures the equity market performance of companies engaged in Financial Technologies, primarily in the areas of software and consulting, data, and analytics, digital payment processing, money transfer, and payment transactional-related hardware across 30 developed and emerging markets. The S&P 500 Index measures the performance of 500 widely held large cap U.S. companies. The Fund includes reinvestment of dividends, net of foreign withholding taxes, while the FactSet Global Fintech Index ™ and S&P 500 Index include reinvestment of dividends before taxes. Reinvestment of dividends positively impacts the performance results. The indexes are unmanaged. Index performance is not Fund performance; one cannot invest directly into an index.

2 The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

3 Not annualized.

Investors should consider the investment objectives, risks, and charges and expenses of the investment carefully before investing. The prospectus and summary prospectus contains this and other information about the Funds. You may obtain them from the Funds' distributor, Baron Capital, Inc., by calling 1-800-99BARON or visiting www.BaronFunds.com. Please read them carefully before investing.

Risks: In addition to general market conditions, FinTech Companies may be adversely impacted by government regulations, economic conditions and deterioration in credit markets. Companies in the information technology sector are subject to rapid changes in technology product cycles; rapid product obsolescence; government regulation; and increased competition, both domestically and internationally, including competition from foreign competitors with lower production costs. The IT services industry can be significantly affected by competitive pressures, such as technological developments, fixed-rate pricing, and the ability to attract and retain skilled employees, and the success of companies in the industry is subject to continued demand for IT services. The Fund is non-diversified, which means it may have a greater percentage of its assets in a single issuer than a diversified fund. The Fund invests in companies of all sizes, including small and medium sized companies whose securities may be thinly traded and more difficult to sell during market downturns. Portfolio holdings are subject to change. Current and future portfolio holdings are subject to risk.

The discussions of the companies herein are not intended as advice to any person regarding the advisability of investing in any particular security. The views expressed in this report reflect those of the respective portfolio manager only through the end of the period stated in this report. The portfolio manager's views are not intended as recommendations or investment advice to any person reading this report and are subject to change at any time based on market and other conditions and Baron has no obligation to update them.

This report does not constitute an offer to sell or a solicitation of any offer to buy securities of Baron FinTech Fund by anyone in any jurisdiction where it would be unlawful under the laws of that jurisdiction to make such offer or solicitation.

Active Share a term used to describe the share of a portfolio's holdings that differ from that portfolio's benchmark index. It is calculated by comparing the weight of each holding in the Fund to that holding's weight in the benchmark. Positions with either a positive or negative weighting versus the benchmark have Active Share. An Active Share of 100% implies zero overlap with the benchmark.

BAMCO, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission (SEC). Baron Capital, Inc. is a broker-dealer registered with the SEC and member of the Financial Industry Regulatory Authority, Inc. (FINRA).

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Baron FinTech Fund Q2 2023 Quarterly Letter