MA - Baron Opportunity Fund Q1 2023 Shareholder Letter

2023-05-02 17:00:00 ET

Summary

- Baron is an asset management firm focused on delivering growth equity investment solutions known for a long-term, fundamental, active approach to growth investing.

- During the first quarter, Baron Opportunity Fund® climbed 17.96% (Institutional Shares), outperforming the broader market.

- To conclude, despite the current uncertain macroeconomic environment, I remain confident in and committed to the strategy of the Fund.

Dear Baron Opportunity Fund Shareholder:

Performance

During the first quarter, Baron Opportunity Fund® ( BIOPX , BIOIX , BIOUX ) (the Fund) climbed 17.96% (Institutional Shares), outperforming the broader market, including the Russell 3000 Growth Index, which rose 13.85%, and the S&P 500 Index, which gained 7.50%.

Table I.

Performance†

Annualized for periods ended March 31, 2023

| Baron |

| Baron |

| Russell |

| S&P |

| Three Months 4 |

| 17.85% |

| 17.96% |

| 13.85% |

| 7.50% |

| One Year |

| (19.91)% |

| (19.70)% |

| (10.88)% |

| (7.73)% |

| Three Years |

| 15.07% |

| 15.37% |

| 18.23% |

| 18.60% |

| Five Years |

| 14.56% |

| 14.87% |

| 13.02% |

| 11.19% |

| Ten Years |

| 13.74% |

| 14.03% |

| 14.16% |

| 12.24% |

| Fifteen Years |

| 11.99% |

| 12.26% |

| 11.88% |

| 10.06% |

| Since Inception |

| 8.15% |

| 8.32% |

| 5.99% |

| 6.90% |

| Performance listed in the above table is net of annual operating expenses. Annual expense ratio for the Retail Shares and Institutional Shares as of September 30, 2022 was 1.31% and 1.05%, respectively. The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate; an investor's shares, when redeemed, may be worth more or less than their original The Adviser may reimburse certain Fund expenses pursuant to a contract expiring on August 29, 2033, unless renewed for another 11-year term and the Fund's transfer agency expenses may be reduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month-end, visit www.BaronFunds.com or call 1-800-99BARON. † The Fund's 3-, 5-, and 10-year historical performance was impacted by gains from IPOs and there is no guarantee that these results can be repeated or that the Fund's level of participation in IPOs will be the same in the future. 1 The Russell 3000® Index measures the performance of the broad segment of the U.S. equity universe comprised of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market. The Russell 3000® Growth Index measures the performance of those companies classified as growth among the largest 3,000 U.S. companies and the S&P 500 Index of 500 widely held large cap U.S. companies. All rights in the FTSE Russell Index (the "Index") vest in the relevant LSE Group company which owns the Index. Russell® is a trademark of the relevant LSE Group company and is used by any other LSE Group company under license. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. The indexes and the Fund include reinvestment of dividends, net of withholding taxes, which positively impact the performance results. The indexes are unmanaged. Index performance is not Fund performance; one cannot invest directly into an index. 2 The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. 3 Performance for the Institutional Shares prior to May 29, 2009 is based on the performance of the Retail Shares, which have a distribution fee. The Institutional Shares do not have a distribution fee. If the annual returns for the Institutional Shares prior to May 29, 2009 did not reflect this fee, the returns would be higher. 4 Not annualized. |

Review & Outlook

As I addressed in my quarterly letters last year, we did not make portfolio decisions based on macro or market projections. Instead, we remained focused on our long-term investment mandate (my tag line: faster for longer ); our in-house research differentiation; powerful and undeniable secular growth trends disrupting industries and driving long-term growth; and identifying exceptional businesses with, among other things, durable competitive advantages, cash-generative business models, and double-digit multi-year projected annual returns. I did emphasize last quarter that, based on our research and analysis, we believed the setting was favorable for our Fund and secular growth stocks. In particular, I highlighted that valuations had compressed to attractive levels and that projected financial metrics (revenues, earnings, and cash flow) had come down significantly to reasonable and even conservative levels. In addition, the inevitable principle of reversion to the mean augured well for growth stocks and the technology-related industry groups, which significantly underperformed since late 2021. While I could not and did not attempt to predict precise timing, reflecting on the first quarter, I believe these factors played a major role in our outperformance for the period. The Fund's exposure to the secular trends of artificial intelligence ((AI)), semiconductors, software, cloud computing, and electric vehicles (EVs) generated the lion's share of our outperformance. Leading the way (in contribution order) were individual investments in NVIDIA Corporation ( NVDA ) (up 90%), Tesla, Inc. ( TSLA ) (up 68%), Microsoft Corporation ( MSFT ) (up 21%), Amazon.com, Inc. ( AMZN ) (up 23%), indie Semiconductor, Inc. ( INDI ) (up 81%), Alphabet Inc. ( GOOG ) ( GOOGL ) (up 16%), Advanced Micro Devices, Inc. ( AMD ) (up 51%), and Meta Platforms, Inc. ( META ) (up 76%).

The market and economic backdrops have not materially changed, but they have continued to march along the paths we have been discussing and most experts have been predicting. The market dialogue and gyrations continued to revolve around interest rates, inflation, the Federal Reserve, and the (now expected) recession. Stocks rose sharply to start the year on investor hopes that moderating inflation data and weakening economic indicators would convince the Fed to stop raising rates, perhaps enabling them to orchestrate a soft landing. But lagging inflation data proved stubborn, rates and Fed Funds futures rose, and the market retreated in February. In early March, the emergence of a banking crisis, following the sudden failures of Silicon Valley Bank and Signature Bank, amplified market and economic risks. As a result, the Fed raised rates by just 25 bps (when 50 bps had been feared), U.S. Treasury yields collapsed, the yield curve inverted further, and the market sold off. Federal regulators quickly intervened to backstop bank depositors and to prevent contagion from spreading, helping the market end the quarter on a rebound.

As we sit here today - not trying to call the macro but observing the data and consensus expert opinions - it appears that peak rates for U.S. Treasuries (not Fed Funds, where another 25 bps increase is widely anticipated) and peak inflation are now in the rearview mirror. Looking at the road ahead, expectations are consolidating around a likely recession, with the bank failures and rescues and tighter credit conditions bolstering this view. 1 The range of projections is too wide to call if it will be short and shallow or long and deep. Bull and bear debates abound regarding market timing (did we bottom in October or are we in a bear market rally?), whether the negative of a weakening economy or the positive of lower rates on valuations influences stocks more, and which sectors or styles will lead the market's next phase. Yes, again, we stay informed on these issues, but eschew making portfolio decisions based on market or macro projections and continue to run our play as highlighted here and detailed in recent quarterly letters. We continue to run a more concentrated portfolio with an emphasis on the secular trends cited above. Among others, during the first quarter, we initiated or added to the following positions:

Software: GitLab Inc. ( GTLB ), HubSpot, Inc. ( HUBS ), and Workday, Inc. ( WDAY )

Semiconductors: Marvell Technology, Inc. ( MRVL ) and Advanced Micro Devices, Inc.

Digital Media: Meta Platforms, Inc.

Electric Vehicles/Autonomous Driving: Tesla, Inc. and Mobileye Global Inc. ( MBLY )

Health Care Equipment: DexCom, Inc. ( DXCM )

Biotechnology/Pharmaceuticals: Rocket Pharmaceuticals, Inc. ( RCKT )

One of our secular themes I would like to emphasize is AI, building on the discussion we started last quarter. AI is transformative technology, just now hitting its inflection point. We believe AI will be the next major secular tectonic shift, like mobile and cloud, and the most compelling force to power technology innovation and impact human life over the next decade. We have been investing in AI for years but appreciate that the current inflection brought about by the launch and adoption of generative AI and large-language transformer models, such as ChatGPT, is a new phase in the AI evolution that will disrupt many industries, strengthening some businesses and weakening others. We are engaged in deep research to gauge who will be disrupted and who will be empowered and to determine where the most significant value and differentiation lies: (1) the semiconductor chip and hardware infrastructure; (2) the generalized, foundational, or domain-specific models; (3) the prompt, chatbox, user interface, or intelligent APIs; 2 or (4) the data, whether public, proprietary, or customer-stored. At this stage of our research, we believe the greatest risk of disruption is in consumer-driven use cases, such as search. Conversational services, like ChatGPT - which exploded onto the scene at an unprecedented pace and now reportedly has over 300 million unique visitors - may become the starting point for people seeking information, entertainment, and products/services. We believe enterprise applications are more defensible for companies that continue to invest, innovate, and launch AI-based products and services, where incumbents may be able to build on their advantages in terms of scale, distribution across large customer sets and embedded workflows, and proprietary and/or customer data. We believe significant value exists across the semiconductor landscape and that most future AI workloads will be built on the infrastructure of cloud service providers. Lastly, at this juncture, we believe a key differentiator for companies will be the ability to capitalize on their unique data assets. The following recent quotes from two technology industry leaders explain the extraordinary potential of AI and its far-reaching implications for business and society:

- Jensen Huang, NVIDIA CEO, GTC Developers Conference, March 21, 2023: "The impressive capabilities of generative AI created a sense of urgency for companies to reimagine their products and business models.... Accelerated computing and AI have arrived.... We are at the iPhone moment of AI. Start-ups are racing to build disruptive products and business models, while incumbents are looking to respond. Generative AI has triggered a sense of urgency in enterprises worldwide to develop AI strategies. Customers need to access NVIDIA AI easier and faster.... ChatGPT is the fastest-growing application in history.... ChatGPT can compose memos and poems, paraphrase a research paper, solve math problems, highlight key points of a contract, and even code software programs.... Generative AI is a new kind of computer, one that we program in human language. This ability has profound implications. Everyone can direct a computer to solve problems. This was a domain only for computer programmers. Now, everyone is a programmer. Generative AI is a new computing platform like PC, internet, mobile, and cloud. And like in previous computing eras, first movers are creating new applications and founding new companies to capitalize on generative AI's ability to automate and co-create.... Generative AI will reinvent nearly every industry."

- Bill Gates, Microsoft Co-Founder, "The Age of AI Has Begun," GatesNotes blog, March 21, 2023: "In my lifetime, I've seen two demonstrations of technology that struck me as revolutionary. The first time was in 1980 when I was introduced to the graphical user interface - the forerunner of every modern operating system, including Windows.... The second big surprise came just last year.... In September...I watched in awe as [the team from OpenAI] asked GPT, their AI model, 60 multiple-choice questions from the AP Bio exam - and it got 59 of them right.... GPT got a 5 - the highest possible score, and the equivalent to getting an A or A+ in a college-level biology course.... I knew I had just seen the most important advance in technology since the graphical user interface.... The development of AI is as fundamental as the creation of the microprocessor, the personal computer, the Internet, and the mobile phone. It will change the way people work, learn, travel, get health care, and communicate with each other. Entire industries will reorient around it. Businesses will distinguish themselves by how well they use it."

Below is a partial list of the secular megatrends we focus on:

- Cloud computing

- Software-as-a-service (SaaS)

- Artificial Intelligence

- Mobile

- Semiconductors

- Digital media/entertainment

- Targeted, people-based digital advertising

- E-commerce

- Genomics

- Genetic medicine

- Minimally invasive surgical procedures

- Cybersecurity

- Electric vehicles/autonomous driving

- Electronic payments

Table II.

Top contributors to performance for the quarter ended March 31, 2023

| Percent |

| NVIDIA Corporation |

| 3.80% |

| Tesla, Inc. |

| 2.82 |

| Microsoft Corporation |

| 2.69 |

| Amazon.com, Inc. |

| 1.41 |

| indie Semiconductor, Inc. |

| 1.14 |

NVIDIA Corporation is a semiconductor mega-cap company and global leader in gaming cards and accelerated computing hardware and software. Shares of NVIDIA rose over 90% during the first quarter because of material developments in generative AI evidenced by the release of ChatGPT and other competitive models. On its fourth quarter fiscal 2023 earnings call on February 22, Colette Kress, NVIDIA's CFO said, "AI adoption is at an inflection point.... The opportunity is significant and driving strong growth in data center that will accelerate through the year." On the same call, Jensen Huang, NVIDIA's CEO emphasized: "The accumulation of technology breakthroughs has brought AI to an inflection point. Generative AI's versatility and capability has triggered a sense of urgency at enterprises around the world to develop and deploy AI strategies.... NVIDIA AI is essentially the operating system of AI systems today.... The activity around AI infrastructures...has just gone through the roof in the last 60 days. And so there's no question that whatever our views [were] of this year as we enter[ed] this year has fairly dramatically changed as a result over the last 60, 90 days." Indeed, our research indicates that shortages of NVIDIA GPUs 3 are the biggest gating factor for AI adoption and that about 90% of AI-model training runs are performed on their GPUs. During its annual GTC conference 4 in March, NVIDIA announced new products and services that expand its addressable market and together form a full AI computing platform. These included: (1) new AI training systems (where it is dominant) and inferencing systems (where the field is more wide open), such as specialized chips in the areas of large language models and recommender systems, simulation and graphics rendering, and video use cases; (2) new fully managed AI services in partnership with the major cloud service providers, called NVIDIA DGX Cloud and NVIDIA Omniverse Cloud; (3) new domain-specific generative AI foundational models, branded NVIDIA AI Foundations, which NVIDIA customers can harness to build and train custom language models with their own proprietary data to develop differentiated offerings; and (4) industry-specific accelerator libraries, spanning such diverse verticals as genomics analysis and computational lithography. We continue to believe NVIDIA's end-to-end AI platform and leading market share in gaming, data centers, and robotics (including automotive), along with the size of these markets, will enable the company to drive durable growth for years to come.

Tesla, Inc. designs, manufactures, and sells EVs, related software and components, and solar and energy storage products. Following a sharp decline at the end of 2022, Tesla's stock rebounded in the first quarter of 2023 on investor expectations that Tesla will continue to grow vehicle deliveries and maintain solid gross and operating margins despite a potential recession, competition in China, and vehicle price reductions. We wrote a long piece on Tesla last quarter and refer readers back to it, because for long-term investors not much has changed over the last three months. Tesla did hold its first Investor Day in March, and several Baron analysts and portfolio managers attended. We toured the Austin Gigafactory, drove in a Cybertruck, boarded a Semi truck, and spoke with a wide swath of Tesla senior managers. During the formal presentation, Tesla highlighted, among other things: (1) its broad and deep bench of executive talent supporting CEO Elon Musk; (2) its "Master Plan 3-Sustainable Energy for All of Earth," which featured EVs, renewable power from solar and wind, and stationary electric storage; (3) its vehicle assembly innovations, including massive casted parts (building Model Y bodies with single front and rear castings, replacing a substantial number of parts and fastening steps), a stainless steel exoskeleton (for Cybertruck), and its next-generation highly efficient "unboxed process" for its next-gen $25,000 vehicle; (4) a future permanent-magnet electric motor that will not require any rare earths; and (5) the massive untapped market opportunity for commercial stationary electric storage, branded Megapack, as the world steadily shifts to renewable energy. As long-term shareholders, we have witnessed Tesla exploit its innovative Model 3/Y now-global mass-market platform to increase vehicle deliveries from barely a standing start to over 1.3 million units, while achieving industry-leading margins and reinforcing its iron-clad balance sheet to almost $23 billion in cash (and effectively no recourse debt). We expect Tesla's next-generation EV and Megapack products to have a similar impact on company results.

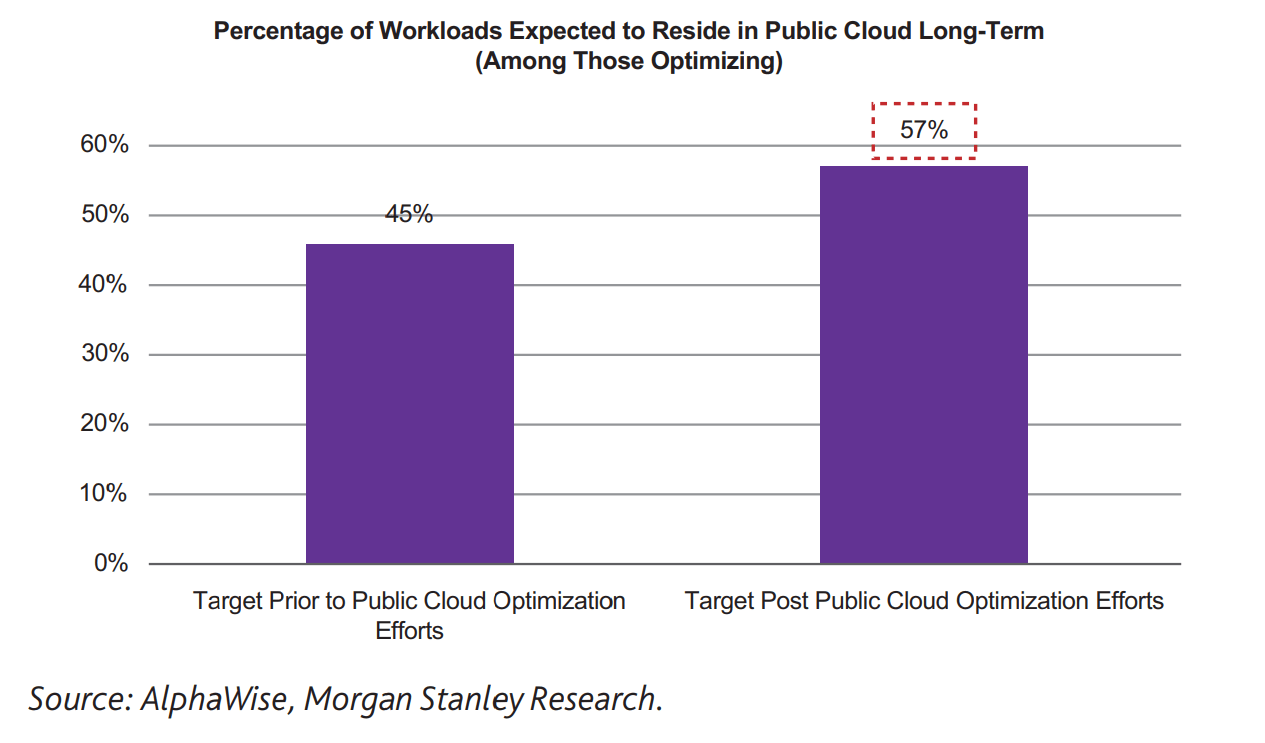

Shares of mega-cap software and cloud vendor Microsoft Corporation performed well during the quarter despite mixed fiscal second quarter results. Microsoft's largest consumer business, Windows licensed to computer vendors, decreased sharply year-over-year as last year's results were bolstered by pandemic-related purchases. Its key commercial business, reported as Microsoft Cloud, grew 29% on a constant-currency basis, beating Wall Street expectations. Drilling down, its Azure cloud computing business also beat expectations, growing 38% on a constant-currency basis, but growth slowed in December, and management's forward guidance was for further deceleration to a low 30% level. Since tougher macro trends emerged last year, cloud businesses, like Azure, have faced headwinds from enterprise customers optimizing their cloud workloads and spending, after a brisk pace of expansion over the last two years. Microsoft CEO Satya Nadella addressed this during the last earnings call: "Just as we saw customers accelerate their digital spend during the pandemic, we are now seeing them optimize that spend.... This is an important time for Microsoft to work with our customers, helping them realize more value from their tech spend and building long-term loyalty.... Moving to the cloud is the best way for any customer in today's economy to mitigate demand uncertainty…while gaining efficiencies of cloud-native development.... I fundamentally believe tech as a percentage of GDP is going to be much higher...on a secular basis.... [W]hat [customers] accelerated during the pandemic, they're making sure they're getting most value out of it or optimizing it.... [A]t some point the optimizations will end...[and] the money that they save in any optimization of any workload is what they'll plow into new workloads and those workloads will start ramping up." Our research continues to indicate that the long-term secular trend of cloud computing remains healthy and intact and will only be boosted by the AI inflection. Morgan Stanley recently issued a report titled "Cloud Optimization: Short Term Pain for Long Term Gains." It echoed Nadella's commentary and our own internal research, concluding that today's cloud optimization would ultimately yield "higher cloud adoption, upsizing [the] opportunity by 30% longer term." The key finding of this report, supported by a survey of 80 chief information officers across the U.S. and Europe, was optimization is increasing the expected penetration of the cloud longer term, with 57% of workloads expected to reside in the cloud post-optimization vs. 45% of workloads pre-optimization.

{kind=link}

Moreover, we believe Microsoft is positioned to be a prime beneficiary of AI because of its ownership of and partnership with OpenAI, the inventor of ChatGPT; its Azure AI supercomputing cloud infrastructure, which is the exclusive cloud provider to OpenAI and a leading AI development platform for other enterprises; and Microsoft's own AI innovations across Bing search (a chatbox virtual assistant), GitHub CoPilot software development (automated code suggestions and completion), and its Office suite of worker-productivity software (virtual assistants, branded CoPilot, to draft or summarize an email, enter data into a spreadsheet, prepare slides, etc.). We remain confident Microsoft is well positioned to continue taking share through any economic downturn and emerge stronger on the other side.

Amazon.com, Inc. is the world's largest retailer and cloud infrastructure services provider. Shares were up in the quarter, driven by positive commentary and actions around cost discipline as well as the broader technology rally. We believe Amazon is well positioned in the short to medium term to meaningfully improve core North American retail profit margins to pre-pandemic levels, mainly by rationalizing fulfillment center costs. The focus on cost discipline has expanded to the whole company, with a second major round of layoffs and CEO Andy Jassy declaring, "Over the last several months, we took a deep look across the company, business by business, invention by invention, and asked ourselves whether we had conviction about each initiative's long-term potential to drive enough revenue, operating income, free cash flow, and return on invested capital." From a top-line growth perspective, Amazon has substantially more room to grow in e-commerce, where it has roughly 15% penetration of its total addressable market, and in retail advertising, which is now a $45 billion annualized business with attractive margins, still growing at a 20% constant-currency rate despite the challenging economic backdrop. In addition, Amazon also remains a leader in the vast and growing cloud infrastructure market with Amazon Web Services (AWS). While AWS is facing the same optimization headwinds as Azure, we believe its long-term opportunity is the same and that AWS can grow over 20% in a normalized macro environment. In his recent shareholder letter, Jassy stated: "While these short-term [macroeconomic and optimization] headwinds soften our growth rate, we like a lot of the fundamentals that we're seeing in AWS. Our new customer pipeline is robust, as are our active migrations.... AWS is still in the early stages of its evolution and has a chance for unusual growth in the next decade." Finally, though it has not been as splashy as its peers so far, Amazon is also well positioned to provide computing infrastructure for the forthcoming generative AI wave, announcing services like Amazon Bedrock, which allow customers to use the supported large language model of their choice, and CodeWhisperer, a tool for software developers to autocomplete code using generative AI.

Indie Semiconductor, Inc. is a designer, developer, and marketer of automotive semiconductors for advanced driver assistance systems (ADAS) as well as connected car, user experience, and electrification applications. Shares rose during the quarter after the company announced the acquisition of GEO Semiconductor and met or exceeded revenue and gross margin guidance for the seventh straight quarter since coming public. After raising capital in late 2022 to fund acquisition activity - we increased our position size when the stock traded down on this convertible bond deal - early this year indie announced its buyout of GEO Semiconductor for up to $270 million (including potential earnouts), to round out its ADAS sensor portfolio with a leader in camera processing technology. We find GEO Semiconductor to be a synergistic acquisition that accelerates indie's growth and margin trajectory. The automotive semiconductor vertical remains attractive. We believe indie will continue to deliver on its targeted model of profitability in the second half of 2023, achieving 60% gross margins and 30% operating margins by 2025. We also project indie continues to rapidly increase revenue, as it fulfills its $4.2 billion, and growing, strategic backlog.

Table III.

Top detractors from performance for the quarter ended March 31, 2023

| Percent |

| ZoomInfo Technologies Inc. |

| -0.50% |

| CoStar Group, Inc. |

| -0.36 |

| Arrowhead Pharmaceuticals, Inc. |

| -0.27 |

| Rivian Automotive, Inc. |

| -0.27 |

| Endava plc |

| -0.25 |

ZoomInfo Technologies Inc. ( ZI ) provides go-to-market business intelligence software. Shares detracted from performance after the company shared a weaker top-line outlook driven by continued macro uncertainty. We have spoken with company management and conducted additional research to validate our longer-term thesis. ZoomInfo is a profitable and cash-generative business with the most comprehensive platform of software and data to improve the go-to-market efforts of its customers, not to mention new products in the marketing and talent-acquisition verticals. When the macro headwinds abate, we believe ZoomInfo will accelerate growth as it continues to penetrate its $70 billion-plus total addressable market.

CoStar Group, Inc. ( CSGP ) is the leading provider of information and marketing services to the commercial real estate industry. After two straight quarters of robust performance, shares detracted during the quarter, likely due to profit taking. Despite the macro backdrop, CoStar's fundamentals remain solid, with net new sales growing 15% in the quarter and margins expanding by 200 bps, excluding growth investments. We expect the company's core businesses to continue to benefit from the migration of real estate market spending to online channels. CoStar has begun to invest aggressively in expanding its residential marketing platform and attacking the substantial residential market opportunity. We estimate CoStar invested around $230 million in this initiative in 2022 and its initial 2023 guidance implies a total investment approaching $500 million. This is a significant upfront commitment, but we believe the residential market represents a transformative opportunity. The company's proprietary data, broker-oriented approach, and best-in-class management all position it to succeed in this endeavor.

Arrowhead Pharmaceuticals, Inc. ( ARWR ), a biotechnology company specializing in RNA interference (RNAi) medications to treat a variety of diseases, detracted from performance. The company has lacked major wins in recent years, while also tallying some losses. Management's late-stage drug licensing efforts to drive upfront and running royalties to bolster its balance sheet and ensure a longer cash runway have also pressured shares. Reinvigorating the company's strategic story remains a key consideration for Arrowhead going forward. Last year, we reduced our portfolio weighting in Arrowhead but decided to maintain a foothold position. We believe Arrowhead's efforts to target RNAi to the lungs will open a new therapeutic area of exploration. In our view, this initiative may lead to RNAi economies of scale, allow for an expansion of pipeline and collaboration opportunities, and generate a long runway for growth.

Shares of Rivian Automotive, Inc. ( RIVN ), a U.S.-based EV manufacturer, fell during the quarter. Despite seven-fold growth in its monthly production rate between late 2021 and the end of 2022, production guidance for 2023 missed analyst forecasts because of supply-chain constraints, principally semiconductors. Moreover, notwithstanding an attractive long-term opportunity and favorable product reviews by customers and industry experts, investors remain concerned about liquidity risks as the company burns cash during its early production stage while unit economics remain challenged. Vehicle sales through the end of 2023 will be at Rivian's legacy vehicle pricing, which was set before inflationary and supply-chain pressures emerged last year across the entire automotive space. New pricing and improved unit economics should be realized in 2024, and Rivian is slated to launch its R2 vehicle line in 2026. We have adjusted Rivian to a smaller position in our portfolio. Despite near-term macro and execution risks, we do believe that Rivian's current valuation offers attractive long-term returns. During the year, we will remain focused on Rivian's production ramp, vehicle demand, unit-level economics, and cost controls as well as progress on its R2 vehicle platform, its next-gen Enduro electric motor, and its battery system advancements.

Endava plc ( DAVA ) provides outsourced software development for business customers. Shares fell after the company reduced financial guidance to reflect slower bookings as macroeconomic uncertainty weighed on client decision-making in December. The company reported solid quarterly results, with 30% revenue growth and 26% earnings growth. Management noted that bookings have improved in the first couple of months of 2023, and they expect annualized revenue growth to quickly return to more than 20%. We remain investors because we believe Endava will continue gaining share in a large global market for IT services.

Portfolio Structure

We invest in secular growth and innovative businesses across all market capitalizations, with the bulk of the portfolio landing in the large-cap zone. Morningstar categorizes the Fund as U.S. Large Growth. As of the end of the first quarter, the largest market cap holding in the Fund was $2.1 trillion and the smallest was $1.4 billion. The median market cap of the Fund was $33.9 billion and the weighted average market cap was $566.1 billion.

As of March 31, 2023, the Fund had $871.1 million of assets under management. We had investments in 46 unique companies. The Fund's top 10 positions accounted for 50.7% of net assets.

Given the market backdrop, fund flows continued to be slightly negative to start the year.

Table IV.

Top 10 holdings as of March 31, 2023

| Quarter End |

| Quarter End |

| Percent of |

| Microsoft Corporation ( MSFT ) |

| $2,146.0 |

| $125.1 |

| 14.4% |

| NVIDIA Corporation ( NVDA ) |

| 686.1 |

| 56.9 |

| 6.5 |

| Tesla, Inc. ( TSLA ) |

| 656.4 |

| 54.0 |

| 6.2 |

| Amazon.com, Inc. ( AMZN ) |

| 1,058.4 |

| 50.1 |

| 5.8 |

| Visa Inc. ( V ) |

| 475.3 |

| 29.6 |

| 3.4 |

| Gartner, Inc. ( IT ) |

| 25.8 |

| 26.7 |

| 3.1 |

| Mastercard Incorporated ( MA ) |

| 346.4 |

| 25.4 |

| 2.9 |

| Alphabet Inc. ( GOOG ) |

| 1,330.2 |

| 25.3 |

| 2.9 |

| ServiceNow, Inc. ( NOW ) |

| 94.3 |

| 24.2 |

| 2.8 |

| CoStar Group, Inc. ( CSGP ) |

| 28.0 |

| 24.1 |

| 2.8 |

Recent Activity

Table V.

Top net purchases for the quarter ended March 31, 2023

| Quarter End |

| Amount |

| Meta Platforms, Inc. |

| $549.5 |

| $9.9 |

| Marvell Technology, Inc. |

| 37.1 |

| 6.8 |

| DexCom, Inc. |

| 44.9 |

| 6.6 |

| Tesla, Inc. |

| 656.4 |

| 6.1 |

| GitLab Inc. |

| 5.2 |

| 5.6 |

We continued rebuilding our position of Meta Platforms, Inc. , the world's largest social network, this quarter. We believe Meta is competitively well-positioned to utilize its leadership in mobile advertising and expand further with the generative AI shift, especially given its massive user base, substantial technological scale, and innovative culture. Core engagement has been strong at Meta, especially with the success of Instagram Reels, which is regaining share from TikTok. Across its platforms, Meta has 3.7 billion monthly active users. A U.S. TikTok ban would further materially benefit Meta. In terms of improving monetization, Meta has developed more effective ad targeting in the last few months with its Advantage+ product. Longer term, Meta has invested in generative AI for years and has among the world's best and largest datasets and distribution. We believe generative AI can materially help Meta improve existing products (e.g., instantly generate personalized creative ads) and expand into new areas (e.g., through WhatsApp and Messenger chats). On the profitability front, Meta's management is serious about cost discipline (laying off approximately 21,000 workers) and prioritizing a more efficient environment, led in earnest by CEO Mark Zuckerberg. Valuation remains relatively attractive, especially as we expect double-digit earnings per share growth, and additional growth options remain.

We took advantage of weakness to purchase shares of Marvell Technology, Inc. , a leading supplier of infrastructure semiconductor solutions that enable the rapid and efficient movement of data throughout the broader data economy, from the data center core to the network edge. Through both organic development and acquisitions led by CEO Matt Murphy since he took over in 2016, Marvell has built a portfolio of market-leading products and IP across computing, networking, security, electro-optics, and storage. Consequently, the company is a critical partner for hyperscale cloud service provider, data center, enterprise networking, carrier infrastructure, consumer, and automotive/industrial end-market customers. Marvell is targeting 15% to 20% average revenue growth through the semiconductor cycle in the coming years, largely driven by secular trends and company-specific product innovations within the cloud, 5G, and automotive end markets. We believe Marvell can deliver on or exceed this target because, among other growth opportunities, its market-leading optical products are critical to delivering increasing data transmission speeds required by hyperscale customers in AI training and inference. At the same time, the company is simultaneously ramping up a custom silicon business working directly with hyperscale partners. Given the dislocation in the stock on near-term cyclical concerns, we believe we paid an attractive price for the long-term growth of this industry-leading company.

We started a position in DexCom, Inc. , a medical device company that sells continuous glucose monitoring (CGM) devices for people with diabetes. DexCom is in the early stages of the launch of its seventh-generation device called the G7, which offers many new features, including 60% smaller size, a disposable transmitter, and 30-minute sensor warmup, among other features. We think the G7 will drive revenue growth acceleration through continued penetration in the core insulin-intensive diabetes population globally. In addition, Medicare recently decided to provide coverage of CGM for people with Type 2 diabetes who are basal insulin users, meaning people with diabetes who use insulin daily but don't need to use insulin intensively at every meal or multiple times daily. This expanded coverage adds millions of people to DexCom's addressable market. Over the long term, we believe DexCom will have an opportunity to expand into the even larger category of non-insulin users with Type 2 diabetes given the benefits of CGM in helping all people manage their diabetes.

We discussed Tesla, Inc. above and at length in our prior quarterly letter. To reiterate, despite macro and company-specific short-term concerns, we remain confident in the company's competitive position, growth opportunities, margin profile, and management. Tesla was our top net purchase in the fourth quarter, and we used continued weakness early in the first quarter to add to our position.

We increased our position in GitLab Inc. after a sharp pullback in the stock price following its fourth quarter earnings report. GitLab is a software platform that developers, IT professionals, and security teams use to manage all stages of the software development life cycle. While GitLab's fourth quarter performance was solid, with 58% revenue growth, management issued disappointing 2023 revenue guidance. New customer growth was healthy, but GitLab saw lower expansion rates in its base product as some existing customers cut back on paid licenses to account for layoffs in their businesses, while others slowed purchasing in anticipation of lower developer hiring this year. Management is assuming this trend will continue through the remainder of 2023. Longer term, we believe GitLab can continue to gain share in the $40 billion software developer market because its ability to address all stages of the software life cycle in a single, unified application give it an advantage over point solutions. Shorter term, we see upside to the guidance as: (1) customers continue to upgrade to GitLab's higher-priced product tier to add security and compliance features; (2) net new customer growth remains healthy; and (3) GitLab is implementing a price increase that should yield an acceleration in revenues toward the end of 2023 and into 2024. The company also continues to demonstrate solid operating leverage. We believe the price increase will help GitLab achieve profitability sooner than initially projected.

Table VI.

Top net sales for the quarter ended March 31, 2023

| Quarter End |

| Amount |

| $1,330.2 |

| $30.8 |

| 20.7 |

| 12.1 |

| Gartner, Inc. ( IT ) |

| 25.8 |

| 11.7 |

| ZoomInfo Technologies Inc. ( ZI ) |

| 10.0 |

| 8.7 |

| Edwards Lifesciences Corporation ( EW ) |

| 46.0 |

| 7.9 |

As we did last quarter, we continued to decrease our weighting in Alphabet Inc. because, as stated earlier, we believe ChatGPT and/or similar AI-based services present a hard-to-measure risk to Google's virtual search monopoly.

Our sales of Gartner, Inc. and argenx SE were both trims because the stocks performed relatively better than the rest of the portfolio last year and increased in position size. As you can see in Table IV, Gartner remains a top six position in the portfolio; argenx remains just outside of the top 10 and our largest biotechnology investment.

Our sale of ZoomInfo Technologies Inc. was for tax-loss purposes, and we repurchased some of our position later in the quarter.

To conclude, despite the current uncertain macroeconomic environment, I remain confident in and committed to the strategy of the Fund: durable growth based on powerful, long-term, innovation-driven secular growth trends. We continue to believe that non-cyclical, durable, and resilient growth should be part of investors' portfolios and that our strategy will deliver solid long-term returns for our shareholders.

Sincerely,

Michael A. Lippert

Portfolio Manager

| Footnotes 1 Our portfolio has no direct exposure to regional banks. While the financial services sector is a relevant customer segment for many of our investments, particularly Endava plc, our companies predominantly serve larger financial institutions and payments businesses, Endava included, and have immaterial exposure to regional banks. 2 Application Programming Interface, or API, is a mechanism that enables two software components to communicate with each other using a set of definitions and protocols. 3 Accelerated computing chips, known as graphical processing units, or GPUs. 4 GPU Technology Conference (GTC). |

| Investors should consider the investment objectives, risks, and charges and expenses of the investment carefully before investing. The prospectus and summary prospectus contain this and other information about the Funds. You may obtain them from the Funds' distributor, Baron Capital, Inc., by calling 1-800-99BARON or visiting www.BaronFunds.com . Please read them carefully before investing. Risks: Securities issued by small and medium sized companies may be thinly traded and may be more difficult to sell during market downturns. Companies propelled by innovation, including technology advances and new business models, may present the risk of rapid change and product obsolescence, and their success may be difficult to predict for the long term. Even though the Fund is diversified, it may establish significant positions where the Adviser has the greatest conviction. This could increase volatility of the Fund's returns. The Fund may not achieve its objectives. Portfolio holdings are subject to change. Current and future portfolio holdings are subject to risk. The discussions of the companies herein are not intended as advice to any person regarding the advisability of investing in any particular security. The views expressed in this report reflect those of the respective portfolio managers only through the end of the period stated in this report. The portfolio manager's views are not intended as recommendations or investment advice to any person reading this report and are subject to change at any time based on market and other conditions and Baron has no obligation to update them. This report does not constitute an offer to sell or a solicitation of any offer to buy securities of Baron Opportunity Fund by anyone in any jurisdiction where it would be unlawful under the laws of that jurisdiction to make such offer or solicitation. BAMCO, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission (SEC). Baron Capital, Inc. is a broker-dealer registered with the SEC and member of the Financial Industry Regulatory Authority, Inc. (FINRA). |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Baron Opportunity Fund Q1 2023 Shareholder Letter