ABX:CC - Barrick Gold: Continue To Prefer Royalty Companies Over Miners

2023-10-09 11:39:56 ET

Summary

- Barrick Gold Corporation is one of the largest gold miners in the world.

- Barrick may show improved earnings in Q3, as inflation may be easing and production is expected to be higher. However, this is already consensus.

- Barrick, being a relatively high cost producer, is very sensitive to the price of gold. As gold prices have declined in recent months, Barrick's stock price has plummeted.

- For long-term investors, I continue to recommend gold royalty companies as the better investment vehicle due to their structurally better costs.

In my last update on Barrick Gold Corporation ( GOLD ), I was worried that a booming M&A market may spur Barrick to overpay for growth. Fortunately, Barrick's CEO has shown much more restraint than his predecessors and has not pulled the trigger. However, this quote in the company's Q1 earnings must have given investors some pause:

While we continue to build our peerless asset base, we are also casting our net wider and stepping up the hunt for fresh opportunities.

So the fact that Barrick has not announced a major transaction to keep pace with Newmont Corporation's ( NEM ) $16.7 billion acquisition of Newcrest Mining and Agnico Eagle Mine Limited's ( AEM ) $11 billion takeover of Kirkland Lake Gold is probably not from a lack of trying.

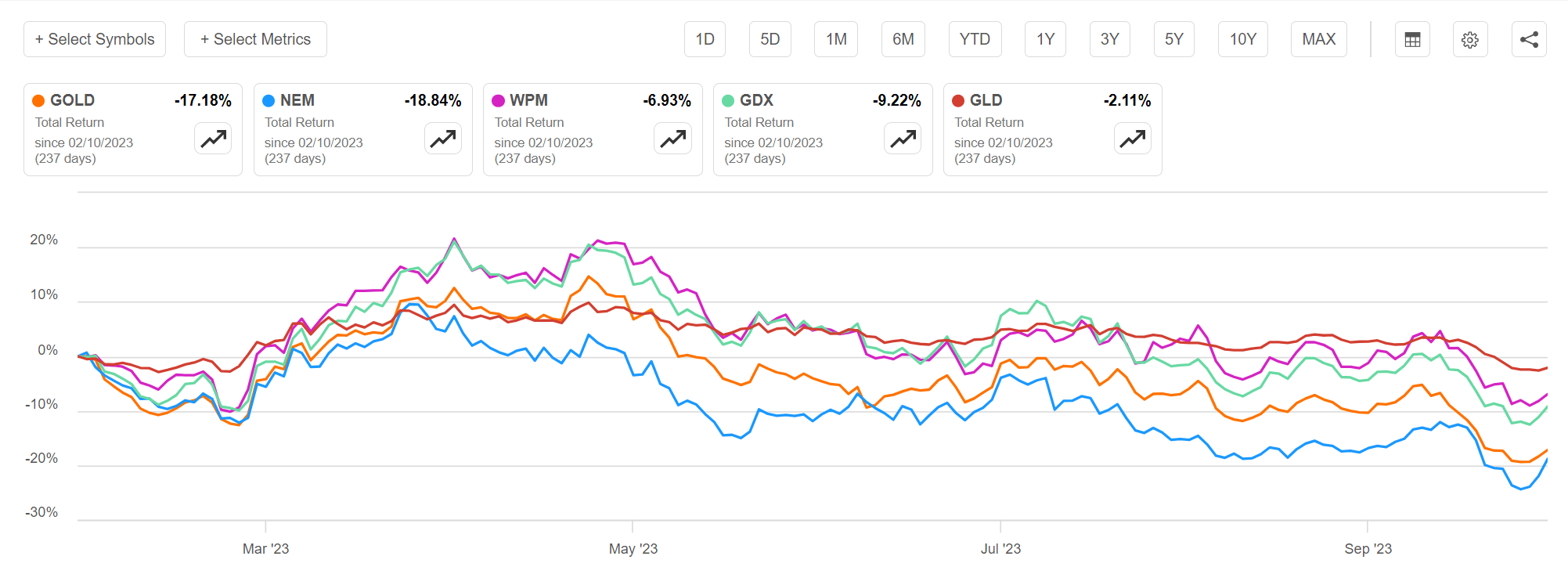

However, despite showing M&A restraint, Barrick Gold continued to underperform, as its share price has declined by 17% since my February update, underperforming peers as represented by the VanEck Gold Miners ETF ( GDX ) and the commodity as represented by the SPDR Gold Shares ETF ( GLD ) (Figure 1). Barrick also underperformed my preferred precious metals investment, Wheaton Precious Metals Corp. ( WPM ) by a mile, but at least the company can be proud of the fact that Barrick outperformed Newmont during this stretch.

Figure 1 - Barrick has underperformed the sector since February (Seeking Alpha)

{kind=link}

Many analysts have poured over Barrick's Q1 and Q2 results, so instead of just looking at the past, I will also take a look at the upcoming Q3 earnings to see if Barrick is now a good 'buy the dip' candidate.

Brief Company Overview

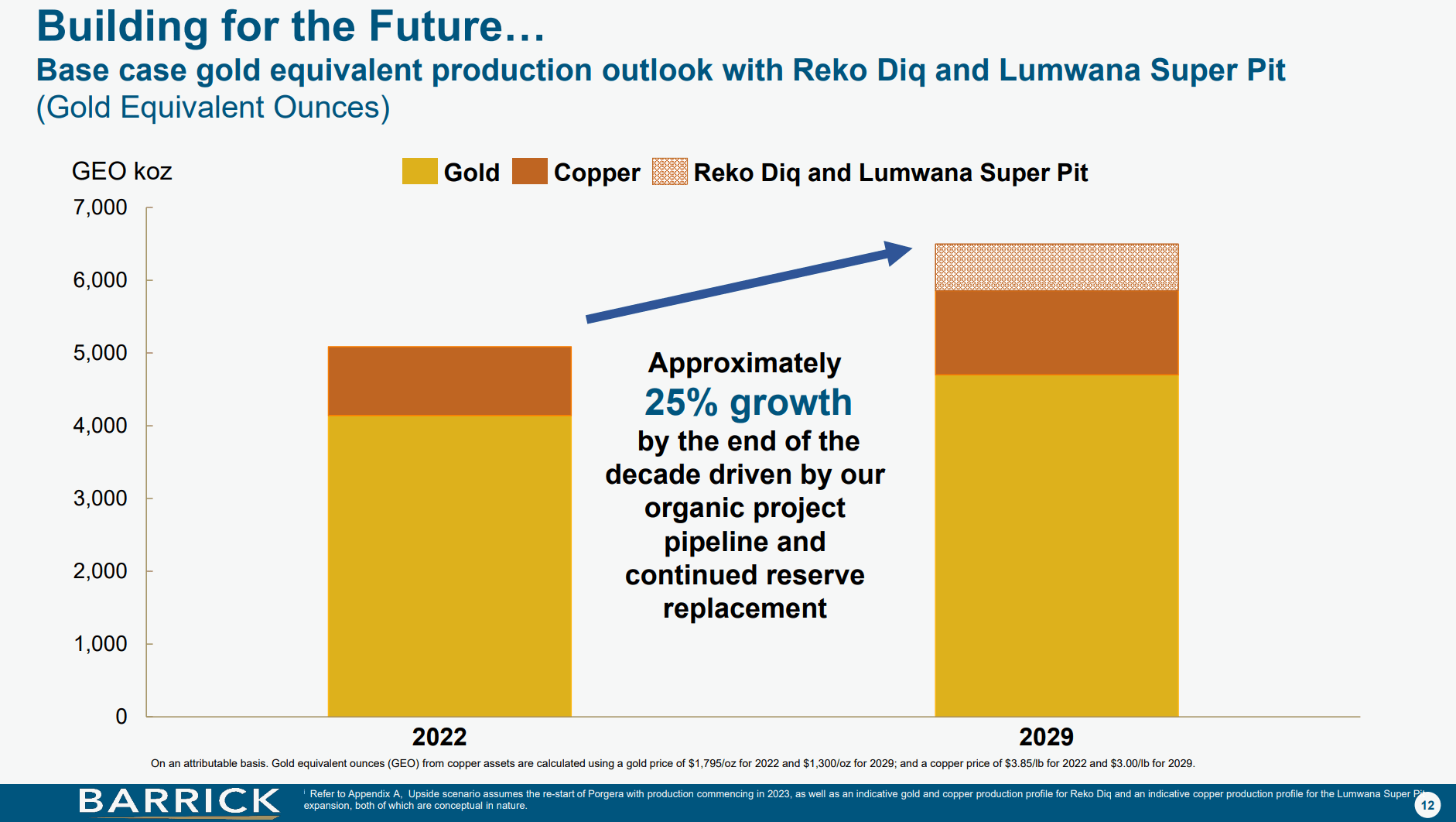

First, for those unfamiliar with the company, Barrick is one of the largest gold producers in the world with assets that can produce ~5 million ounces of gold and gold equivalents ("AuEq") annually (Figure 2). Barrick also has plans to grow to > 6 million oz AuEq by the end of the decade from its organic pipeline.

Figure 2 - GOLD produces 5 million oz and has plans to grow to > 6 million oz (GOLD investor presentation)

{kind=link}

Inflation Finally Peaking

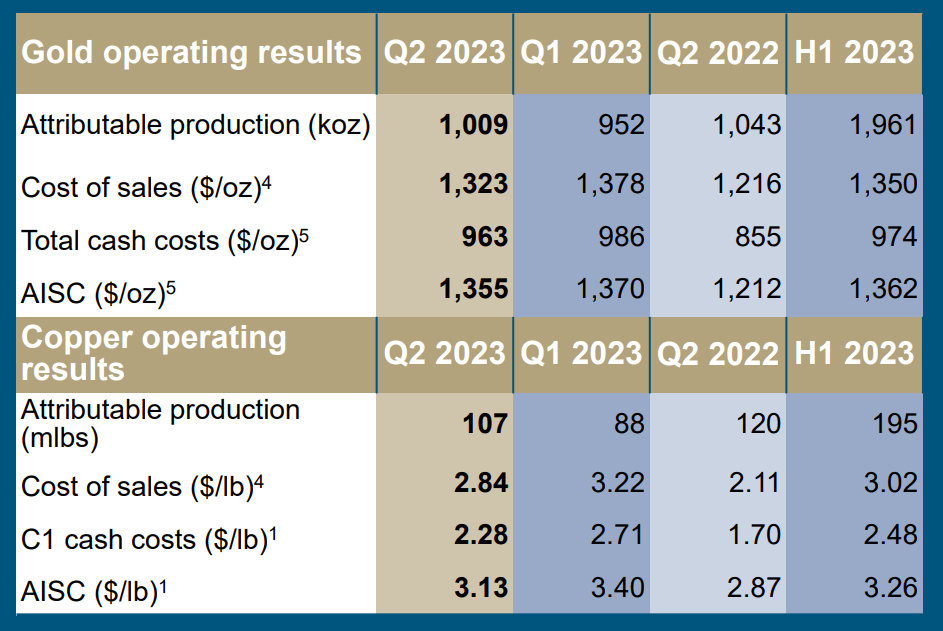

My primary concern with Barrick for the past year has been soaring inflation crimping the company's margins. Fortunately, that trend seems to be finally easing. In the most recently reported Q2 earnings, Barrick saw a QoQ decline in cash costs in the gold business from $986/oz to $963/oz, and in the copper business from $2.71/lb to $2.28/lb (note, copper costs are heavily dependent on volume, so Q1's copper costs were abnormally elevated due to low production volumes) (Figure 3).

Figure 3 - GOLD cost inflation finally abating (GOLD investor presentation)

{kind=link}

This is a welcome improvement since costs directly feed into a miner's margins. However, before investors celebrate, we should take a look at the evolution of Barrick's production and costs.

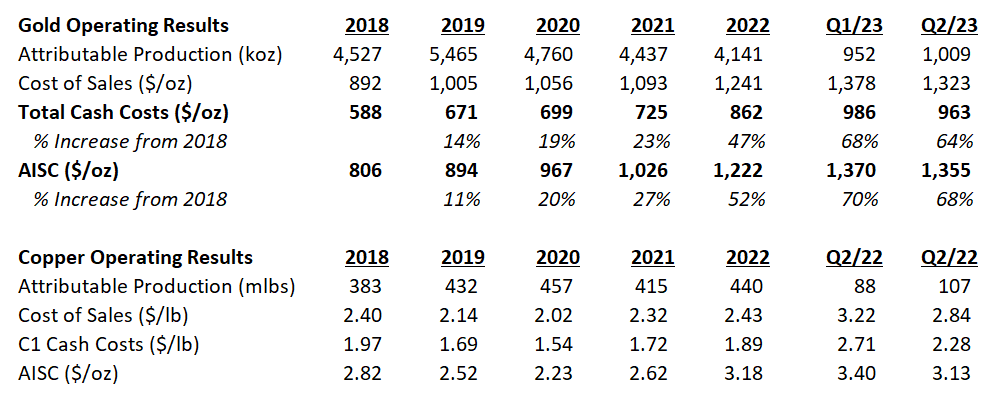

Since 2018 (the time of the Randgold merger), Barrick's gold production has declined from 4.5 million oz to 4.1 million oz in fiscal 2022 while cash costs have leapt ~65% from $588/oz in 2018 to $963/oz as of Q2/23 (Figure 4).

Figure 4 - GOLD's cash costs have increased 65% from 2018 (Author created with data from company reports)

{kind=link}

Rising Costs Are An Industry Phenomenon

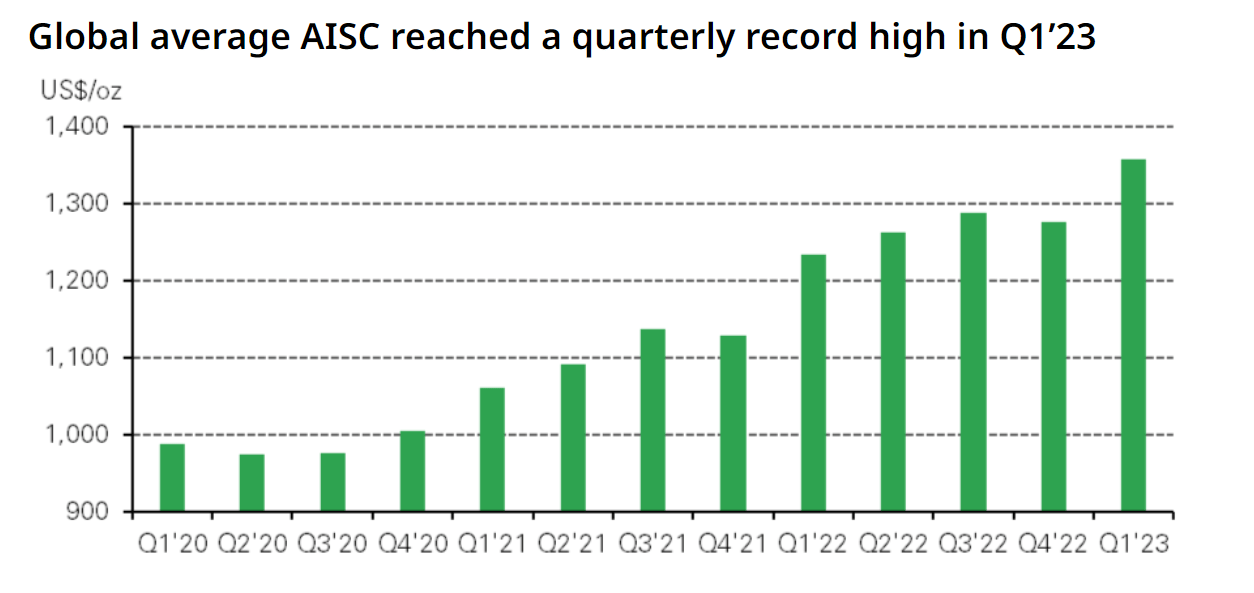

Rising costs are an industry phenomenon that is not unique to Barrick, as the World Gold Council 's data shows average All-in-sustaining-costs ("AISC") have climbed to $1,358/oz as of Q1/23 (Figure 5).

Figure 5 - Industry AISCs have climbed significantly (World Gold Council)

{kind=link}

So the increase in Barrick's AISC from $967/oz in 2020 to $1,370/oz in Q1 and $1,355/oz in Q2/23 is actually just 'par for the course'.

But Don't Expect A Return To Historical Costs

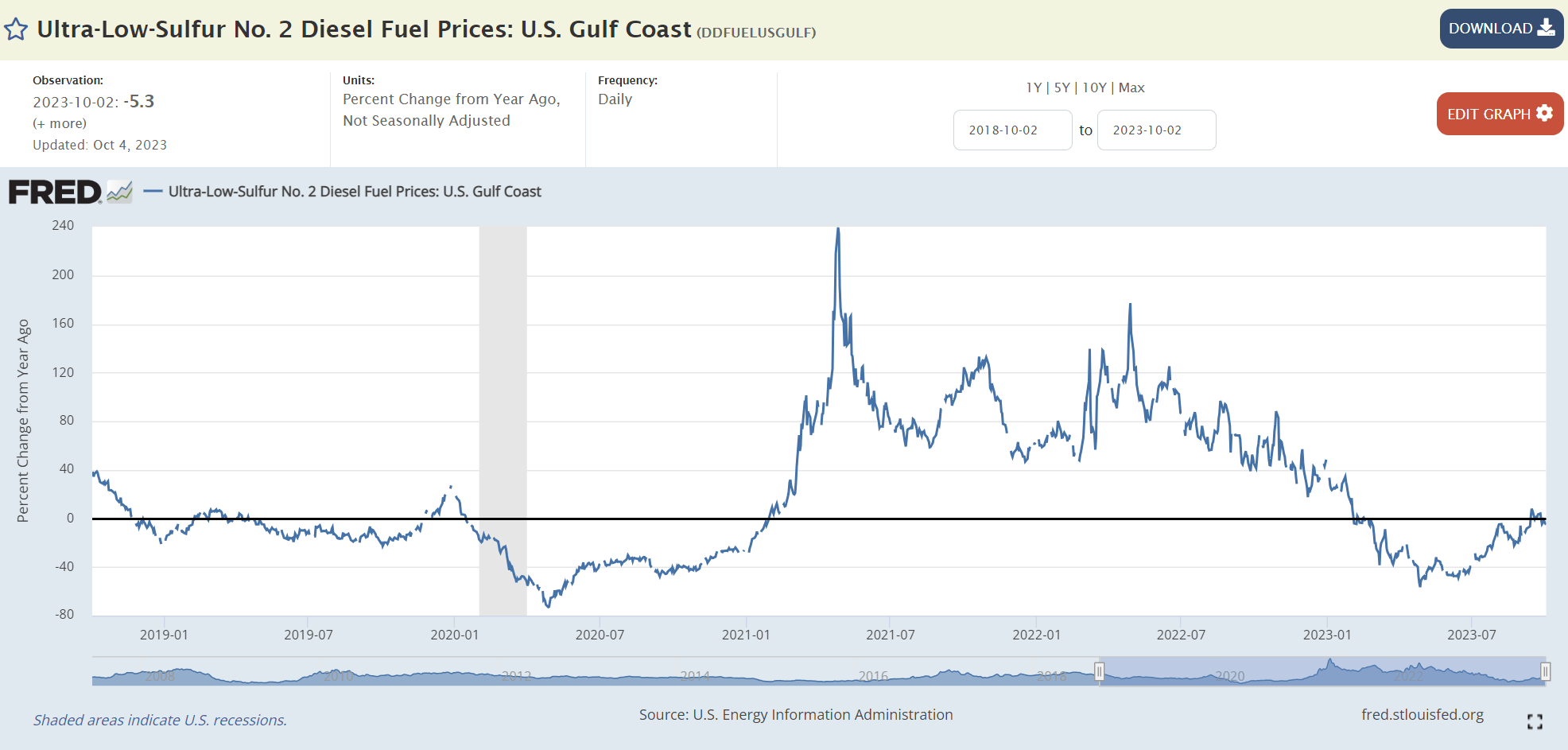

Diesel fuel, which is used to power most of the industry's machinery, is a big component of Barrick's cash costs (15% according to a recent presentation). Diesel prices finally saw YoY declines in Q2/2023, and is likely to be a tailwind in the upcoming Q3/2023 report as well (Figure 6).

{kind=link}

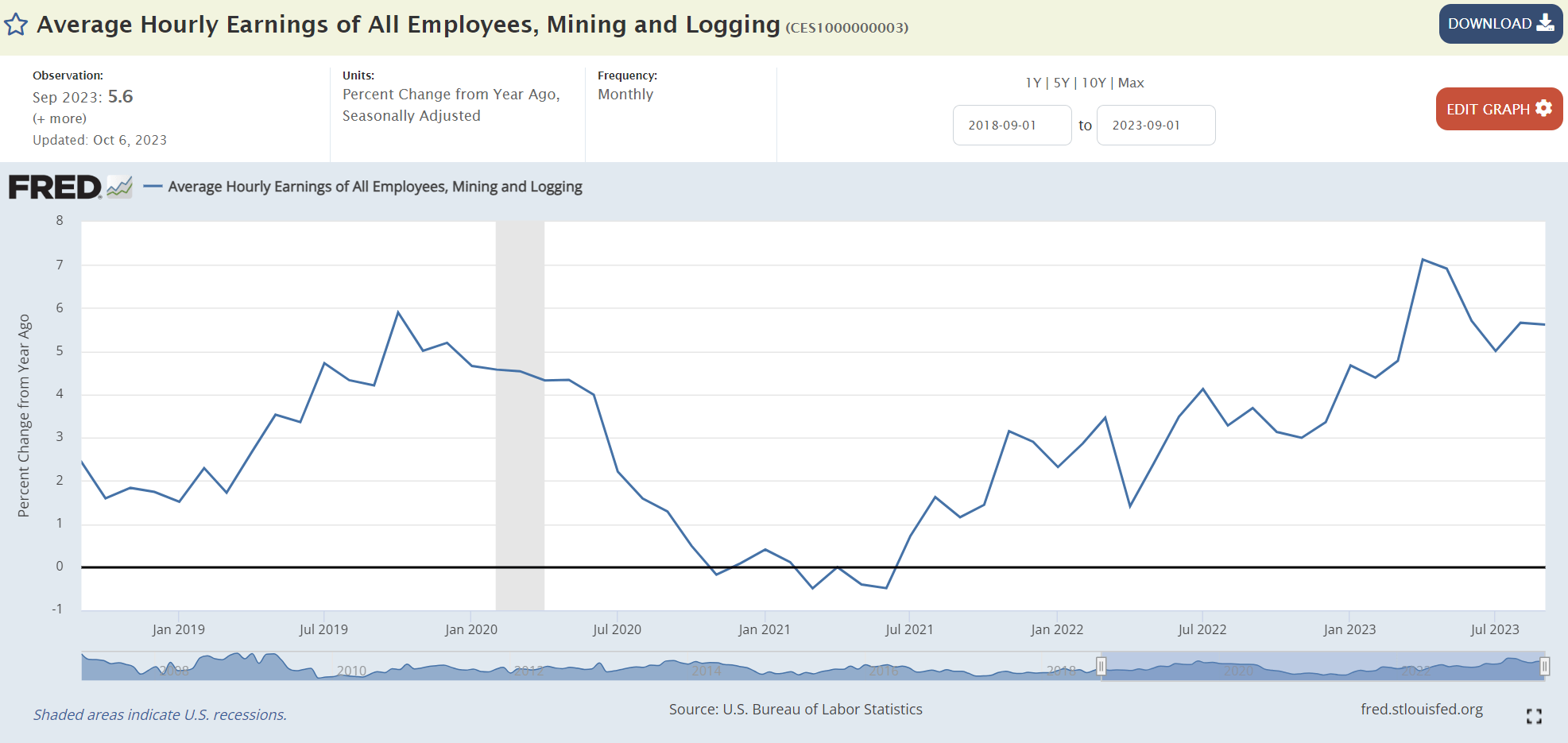

However, other large components of Barrick's cash costs may not see the same level of disinflation. For example, labor, which is the 2nd largest component of cash costs, continues to see elevated levels of inflation (Figure 7).

{kind=link}

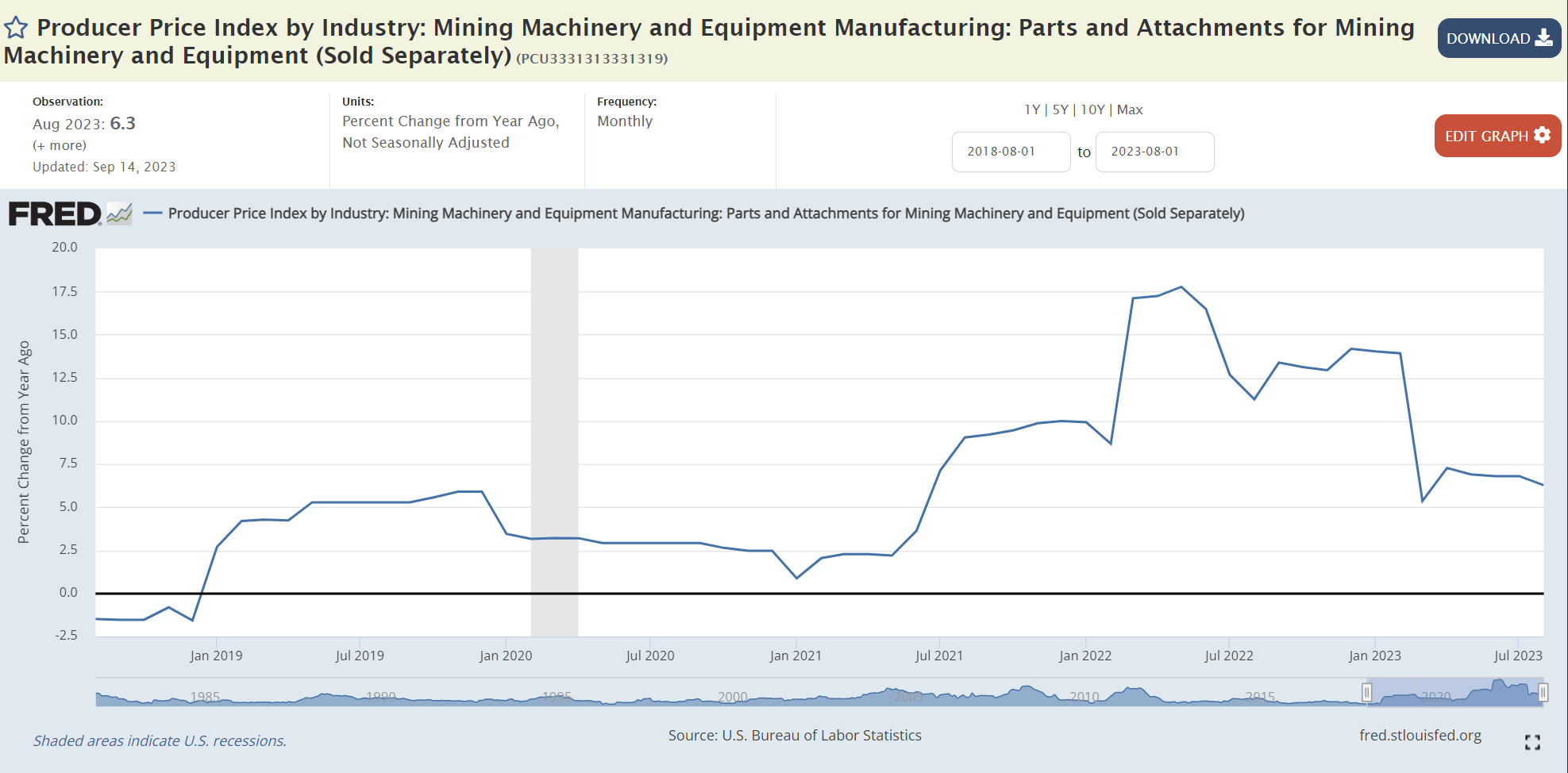

Likewise, consumables and spares, which can be modeled using the PPI for Mining Machinery and Equipment: Parts and Attachments, is still showing mid-single-digit inflation (Figure 8).

Figure 8 - PPI inflation for machinery parts is still elevated (St. Louis Fed)

{kind=link}

So investors should not expect cash costs to decline materially from current levels for Barrick.

Continue To Prefer Royalty & Streaming Business Model

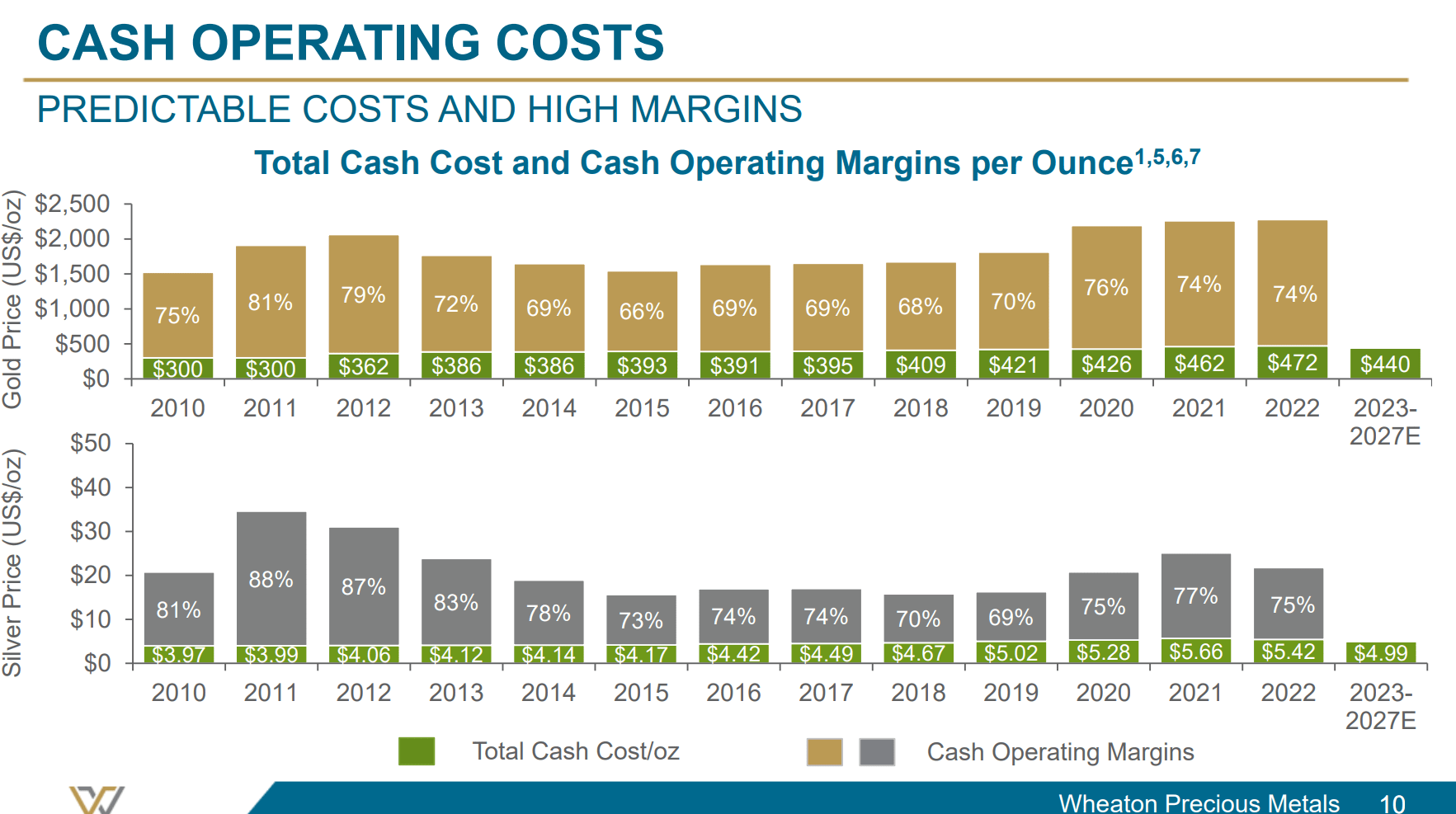

Elevated mining costs is the main reason I continue to prefer the royalty and streaming business model used by Wheaton Precious Metals and other royalty companies. In contrast to miners with soaring costs, WPM's has low and steady 'cash costs' that are negotiated at the time of the royalty and streaming agreements (Figure 9).

Figure 9 - WPM has low and steady cash costs (WPM investor presentation)

{kind=link}

Investors who want to learn more about WPM and the royalty business model can refer to this article.

Gold Prices Taking A Breather

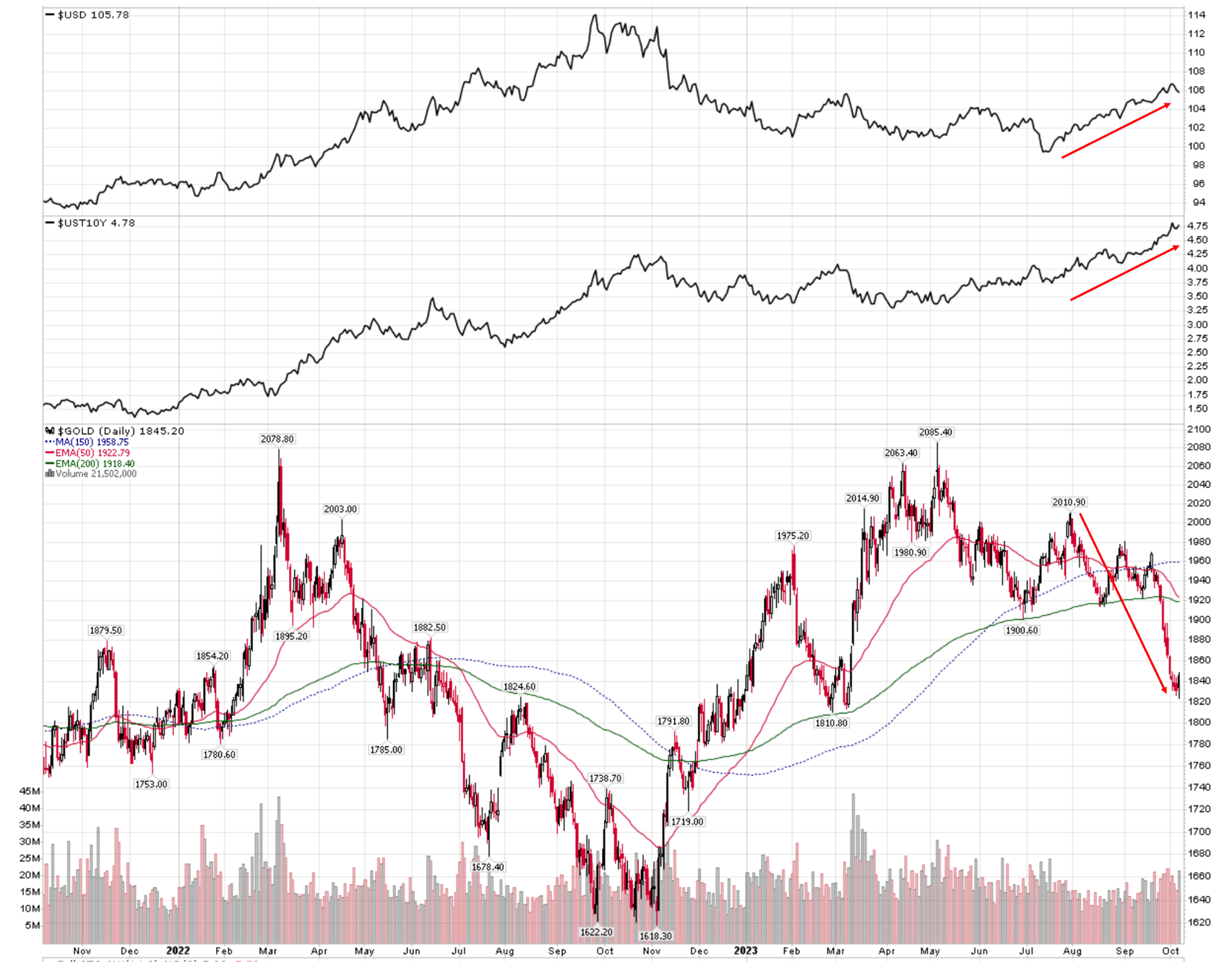

The other main headwind for Barrick and other gold and precious metal mining companies in the past few months has been the price of gold. The soaring US dollar and interest rates have placed heavy pressure on the price of gold and silver, with gold prices declining from a summer high of over $2,000/oz to a recent low of $1,825 (Figure 10).

Figure 10 - US dollar and interest rates have pressured gold prices (Author created with price chart from stockcharts.com)

{kind=link}

In fact, the average price of gold declined 2.6% QoQ in Q3, from $1,978/oz to $1,926/oz (calculated from Yahoo Finance data ), so Barrick's margins in the upcoming Q3 earnings report may be compressed due to lower gold prices. (Investors should note that Barrick reported a realized gold price of $1,972 in Q2/2023, so this average gold price estimate is directionally accurate).

Production Should Be Higher; But Improvements Already Baked-In

Offsetting a lower gold price, we know from the company's Q2 earnings report that production is going to be second-half weighted, as the company produced only 2.0 million oz of gold and 195 million lbs of copper in H1/2023 but maintained its 4.2-4.6 million oz of gold and 420-470 million lbs of copper guidance. Hence investors should be expecting higher production in the upcoming Q3 earnings report.

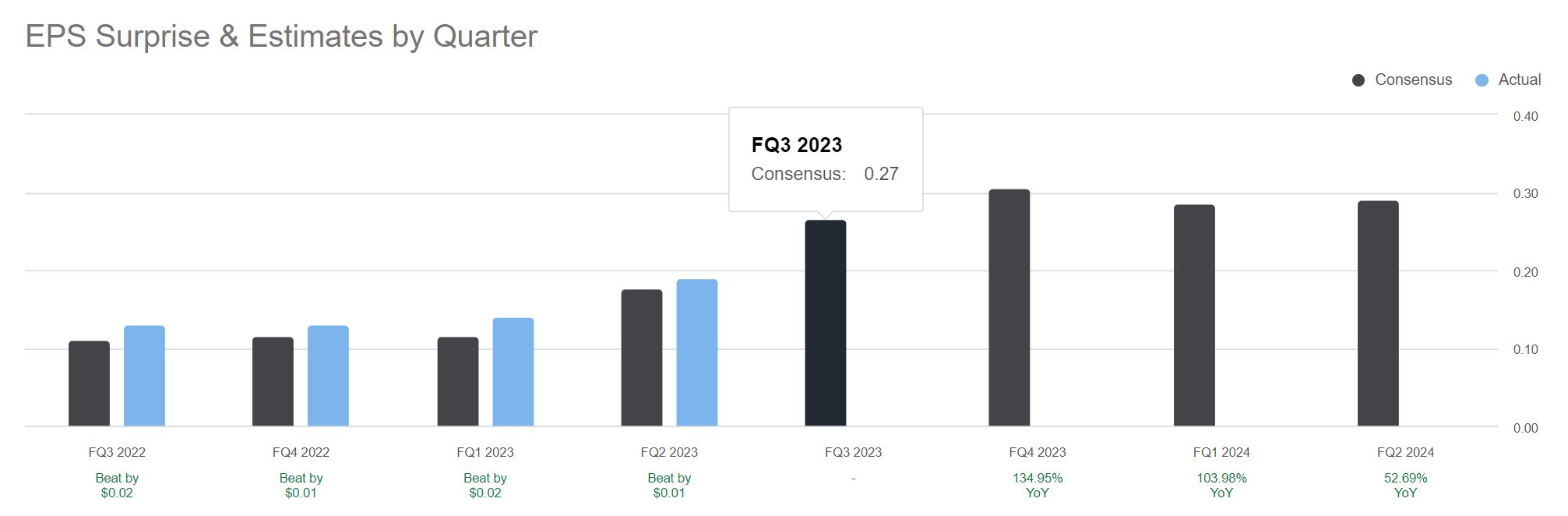

However, a stronger Q3 earnings is already factored-in by Wall Street analysts in my opinion, as consensus expects Barrick to earn $0.27 / share in Q3/2023 compared to $0.19 in Q2, and $0.13 / share in Q3/2022 (Figure 11).

Figure 11 - Consensus already expects a big improvement in Q3 earnings (Seeking Alpha)

{kind=link}

Valuation Remains Cheap, But Maybe Cheap For A Reason

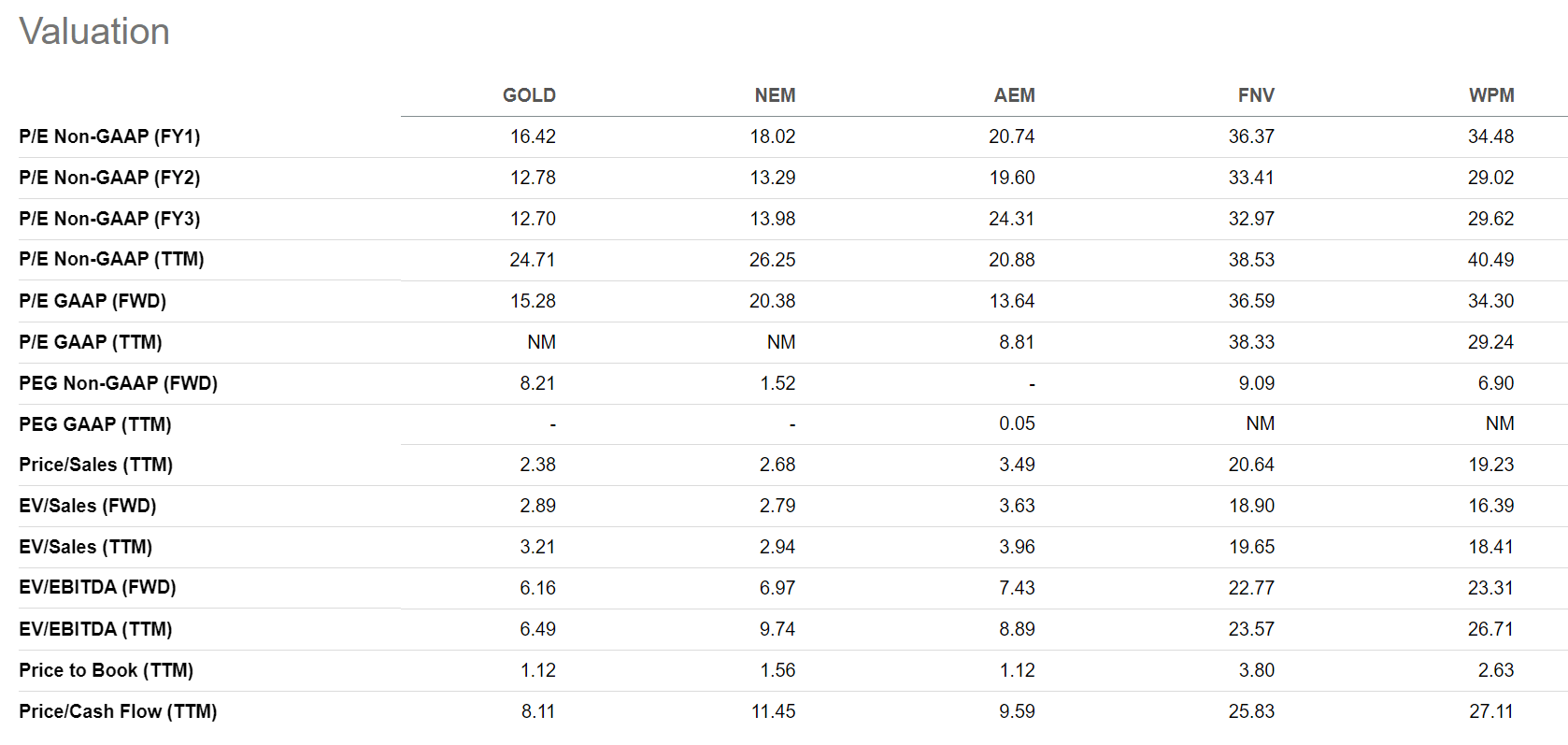

Valuation-wise, Barrick remains 'cheap' when compared to peers such as Newmont and Agnico Eagle Mines, trading at 16.4x Fwd P/E vs. 18.0x and 20.7x respectively (Figure 12).

Figure 12 - GOLD is 'cheap' relative to peers (Seeking Alpha)

{kind=link}

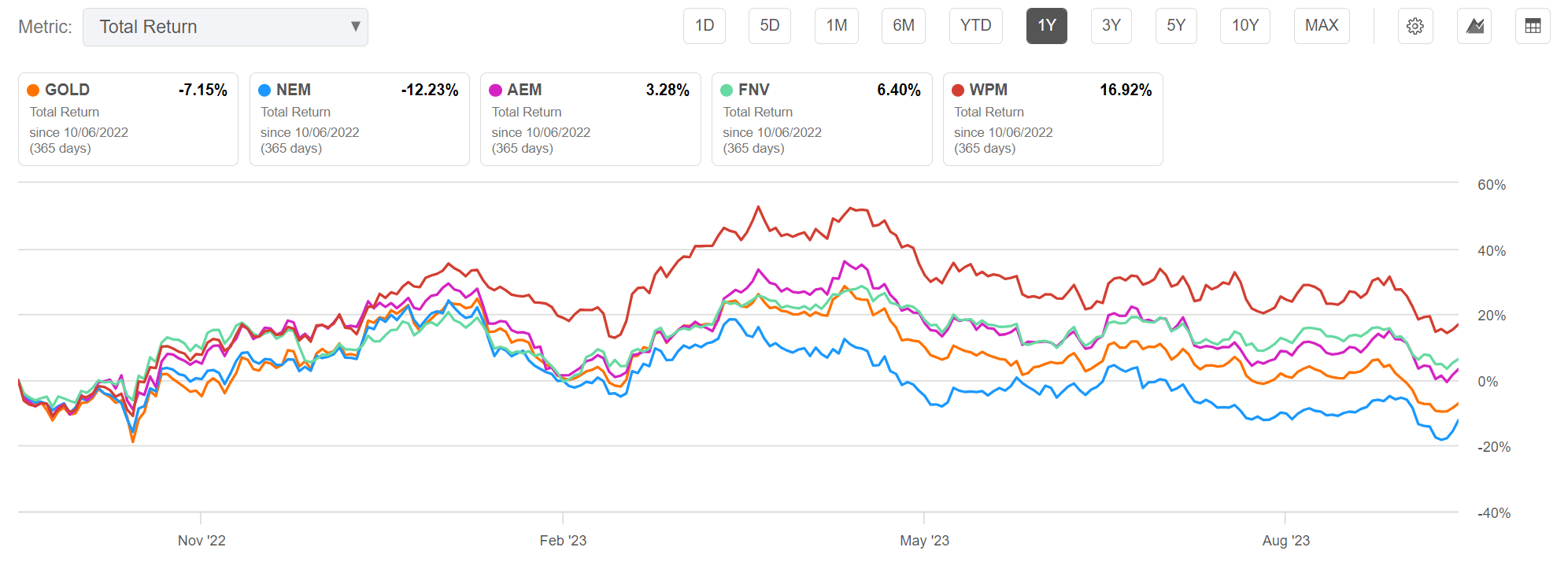

However, I would caution against using P/E multiples to predict forward returns for gold miners. For example, in my initiation article from October 2022, we can see GOLD was the 'cheapest' stock, trading at 15.6x Fwd P/E compared to NEM at 17.3x, AEM at 18.0x, FNV at 31.4x, and WPM at 26.3x (Figure 13).

Figure 13 - GOLD was 'cheapest' in October 2022 as well (Seeking Alpha)

But if we look at total returns in the past year, GOLD has significantly underperformed peers, with the exception of Newmont, which has done worse (Figure 14).

Figure 14 - But cheap stocks have underperformed (Seeking Alpha)

{kind=link}

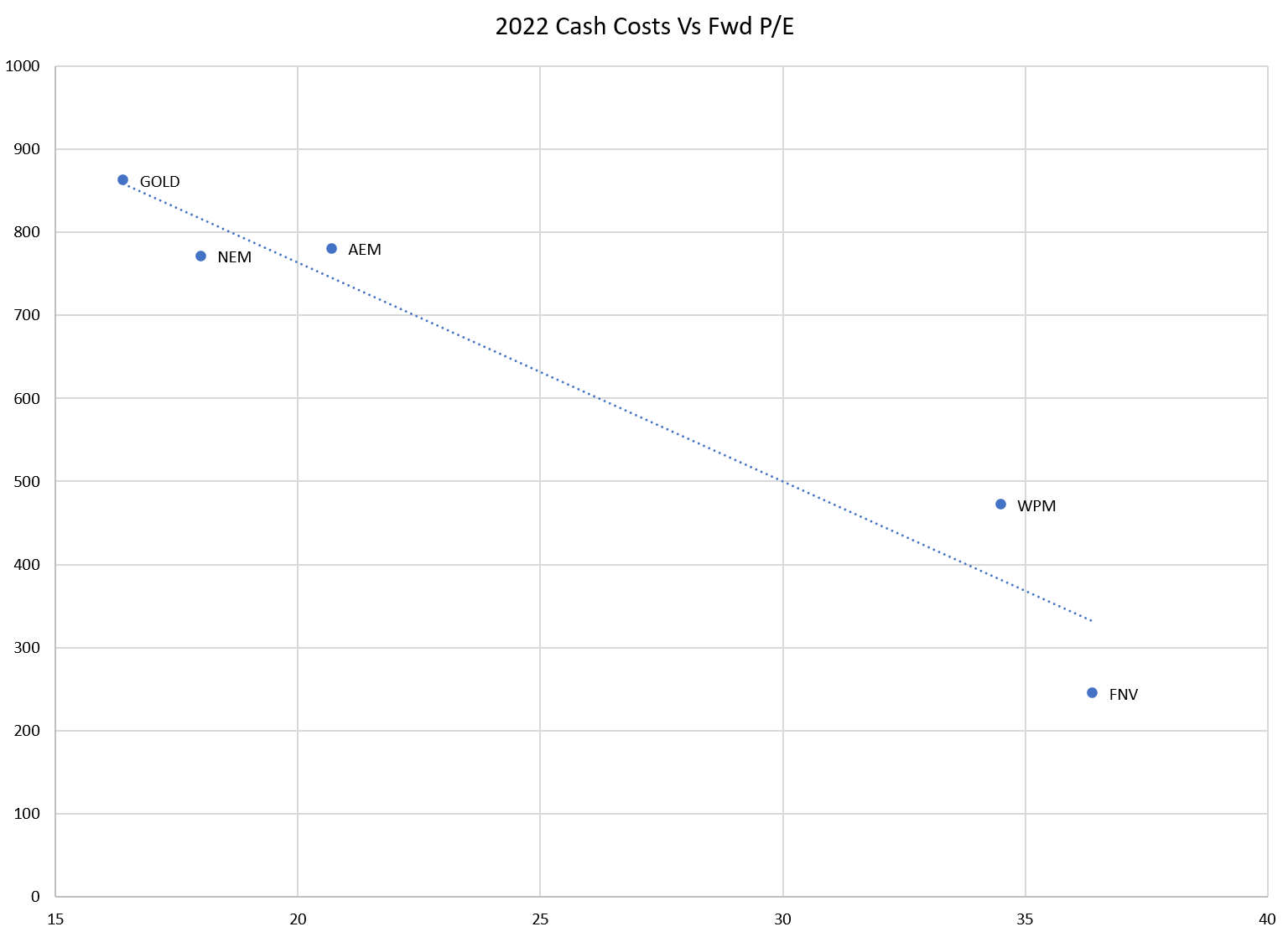

In fact, since all gold producers are price takers, I believe their 'valuation multiples' are simply a reflection of the profitability of their assets, i.e. those with a lower cash cost (and thus higher margins) have a higher P/E (Figure 15).

Figure 15 - 2022 Cash costs vs. Fwd P/E (Author created with data from company reports and Seeking Alpha)

{kind=link}

Risk To Cautious View

Of course, Barrick, being a relatively high cost producer, may have higher operational leverage to the price of gold. If gold prices rise quickly in a short period of time, the impact to Barrick's margins will be greater when compared to a company like Wheaton Precious Metals, with a low cash cost to begin with.

Conclusion

Looking forward, the upcoming Q3 earnings report should show good growth in earnings for Barrick, as production is expected to be materially higher and inflation may be moderating. However, elevated production costs may be here to stay as high consumables and labor inflation offset declines in fuel prices.

The biggest driver to gold miners' returns is gold prices, and that has turned into a headwind for Barrick and other gold miners on the back of a surging US dollar and rising interest rates.

Overall, I continue to prefer the royalty and streaming business model of Wheaton Precious Metals, as royalty companies have structurally lower costs allowing for better profit margins.

For further details see:

Barrick Gold: Continue To Prefer Royalty Companies Over Miners