GOLD - Barrick Gold: Easy Comps In Q3 Makes It A Buy Near Trough Multiples

2023-08-08 12:15:02 ET

Summary

- Barrick Gold Corporation reported lower production year-over-year, but we should see it steady going forward.

- Meanwhile, headline costs and margins disappointed, but I dig into why there's reason to be optimistic here from a forward-looking standpoint.

- At a valuation of ~5.6x FY2024 cash flow per share estimates, I'll look at whether Barrick finally offers enough margin of safety to start buying the dip.

The Q2 Earnings Season has been a mixed one for the Gold Miners Index ( GDX ), with rising operating costs mostly offsetting the record average realized gold price despite a pullback in diesel prices vs. peak levels last year. Plus, production levels at some sites have been affected by one-time headwinds, such as severe weather and wildfires in some jurisdictions, and massive strike at one of the world's largest polymetallic mines (Penasquito), affecting sales for not only Newmont ( NEM ) but also companies like Wheaton Precious Metals ( WPM ) with a stream on the asset.

Unfortunately, Barrick Gold Corporation ( GOLD ) Q2 results weren't able to buck this trend, with declines in margins, free cash flow, and gold output on a year-over-year basis.

{kind=link}

However, as I'll explain below, Barrick has a much stronger H2 ahead, benefits from easy comps in the current Q3 2023, and will look like a completely different company in 2024 whether gold sits at $1,800/oz or $1,950/oz. And given this setup, I see this pullback as a buying opportunity, with the potential for a 50% total return over the next 18 months.

Let's take a closer look at the company's Q2 results below and why a rearview mirror approach is the wrong one to take, with several factors working in Barrick's favor from now on.

Q2 Production & Sales

Barrick Gold released its Q2 results this week, reporting quarterly production of ~1.01 million ounces of gold, a 3% decline from the year-ago period. The slide in gold production was related to a softer quarter at Pueblo Viejo, with tie-in work on the nearly completed Expansion Project (14.0 million tonnes per annum) throttling output, lower production at Cortez related to mine sequencing and Turquoise Ridge, where planned autoclave maintenance was completed and autoclave processing was much lower at ~424,000 tonnes. This was partially offset by higher recoveries and throughput at Kibali and a slightly better quarter at its 61.5% owned Carlin Complex due to significantly higher average grades (4.55 grams per tonne of gold) that benefited from higher open-pit grades.

Unfortunately, the higher production at these two key assets was unable to pick up the slack. Despite a better quarter, costs at the NGM joint-venture came in at elevated levels of $1,388/oz.

Barrick Gold - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

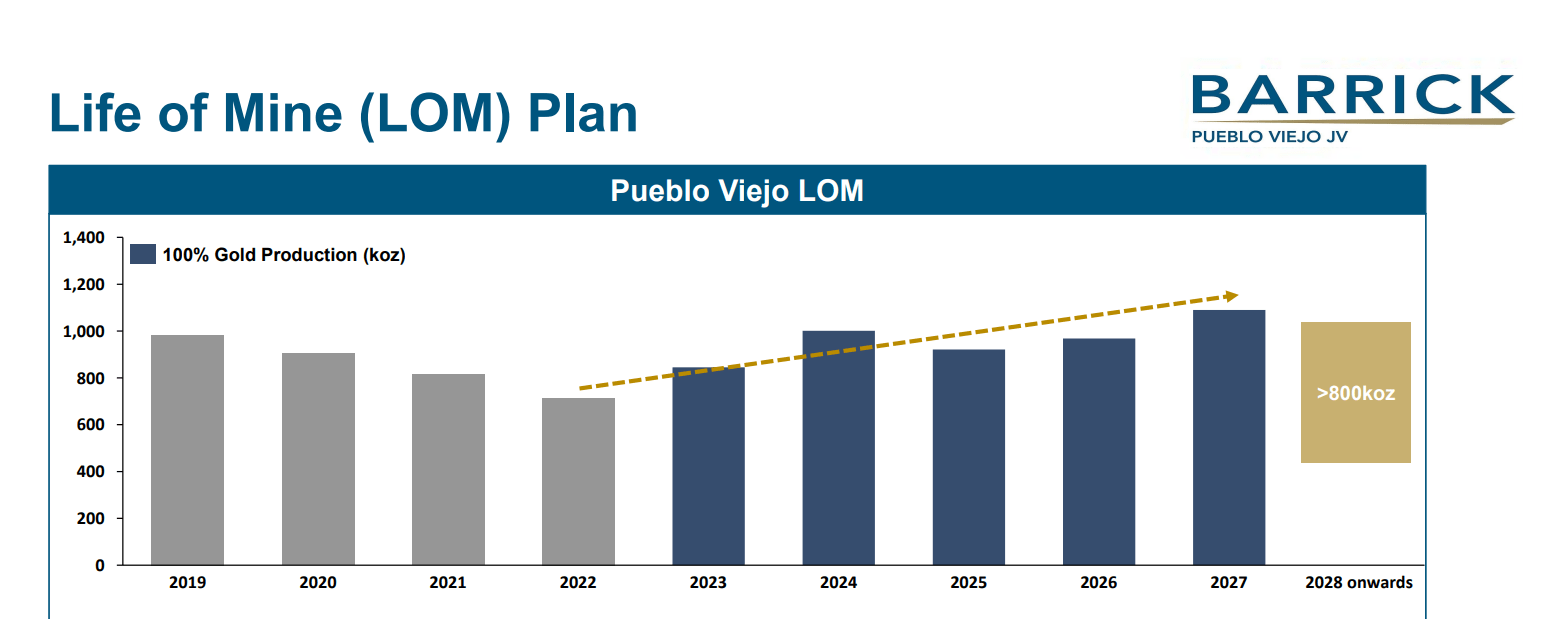

Although this is disappointing, it's important to remember that Barrick guided for back-end weighted production so the fact that it's tracking at ~46.6% of its annual guidance midpoint should not be alarming. And while the above chart clearly shows a steady decline in quarterly gold production, investors must not lose sight of the fact that Barrick will see a significant step-up in production at Pueblo Viejo (60%) going forward, with the plant expansion expected to result in production north of 600,000 ounces attributable to Barrick next year (~150,000 ounce quarterly average) and ~135,000 attributable ounces form 2024-2027, translating to a 75% and 95% growth increase from the depressed levels in Q2 2023 (~77,000 ounces produced at $1,219/oz). The result should be lower costs and significantly higher free cash flow from this asset, one key pillar to Barrick's turnaround that's already set in motion.

Pueblo Viejo Expansion - Increasing Production Profile (Company Website)

{kind=link}

Plus, elsewhere in the portfolio, H1 2023 should have been a better period if the Record of Decision at Goldrush was not delayed (allowing for it to start ramping up) and Porgera had been restarted in line with more optimistic expectations. However, the ROD at Goldrush is expected by year-end and this is an incredible asset, expected to produce over 400,000 ounces per annum once it reaches commercial production by 2026. Meanwhile, Porgera finally looks to be closing in on the finish line in terms of a restart, and both of these assets will help increase production, and both are lower-cost assets. So, with H2 being stronger for Barrick and 2024 expected to be a better year, I would expect consistent sequential and year-over-year growth in production for Barrick going forward, with a more material step up in output in 2025 to 4.5+ million ounces of gold (4.2 million ounce guidance midpoint in 2022).

As highlighted in Barrick's MD&A, the Goldrush ROD is now expected in Q4 2023, but underground and development has continued under the Horse Canyon/Cortez Unified Exploration Project POA in the meantime, with a minor modification by the Bureau of Land Management approved to allow for an additional ~635,000 tonnes of waste to be placed on the existing waste rock storage facility near CHOP (allowing underground development to continue into mid-2024).

Barrick Gold - Quarterly Revenue (Company Filings, Author's Chart)

{kind=link}

Unfortunately, the better forward outlook doesn't help Barrick's recently reported Q2 financial results, with revenue coming in at ~$2.83 billion (down 1% year-over-year), operating cash flow coming in at $832 million (down 10% year-over-year), and free cash flow plunging to just $63 million, with trailing-twelve-month free cash flow now barely positive. This is certainly not what one wants to see from a ~$20.0 billion company, but like production, there are nuances here that are important to consider.

For starters, the gold price has spent its 21st consecutive week above the $1,900/oz level (a new record), suggesting that higher gold prices might be here to stay. Second, capital expenditures are up sharply on a trailing-twelve-month basis vs. Q2 2022 (~$3.14 billion vs. $2.61 billion). Third, near peak inflationary pressures have impacted profitability but appear to be easing finally, which will all translate to improve margins and free cash flow in H2 2023 and 2024.

Costs & Margins

While the production results showed moderate declines, Barrick's cost performance wasn't much better from a headline standpoint. This is because all-in sustaining costs [AISC] came in at $1,355/oz (up 12% year-over-year), and while they pulled back from their peak hit in Q1 ($1,370/oz), they were a little higher than I anticipated. The good news was that Barrick's average realized gold price helped to offset the impact of higher costs, with AISC margins only down slightly at $617/oz vs. the $649/oz reported in Q2 2022.

Still, these margins were slightly below my estimates of $625/oz, and continue to remain well below the levels Barrick enjoyed in 2020 when the stock outperformed the market with a 23% return in 2020. However, the higher costs were related to lower production from its low-cost Pueblo Viejo Mine, fewer ounces sold than produced in the period, and another quarter of relatively high mine site sustaining capital ($524 million).

Barrick Gold - Quarterly AISC & Directional Estimates (Company Filings, Author's Chart) Barrick Gold - Quarterly AISC Margins (Company Filings, Author's Chart)

{kind=link}

{kind=link}

However, as I stated in my previous update on Barrick in July, it's important not to take a rearview mirror approach on costs and margins:

"AISC margins have the potential to improve to $700/oz in Q3 2023 assuming improved all-in sustaining costs of $1,250/oz and an average realized gold price of $1,950/oz. This would translate to a ~55% increase year-over-year vs. the $453/oz AISC margins in Q3 2022. So, while Barrick has struggled to hold the line on margins over the past two years as it's come up against near unprecedented inflationary pressures combined with increased investment and a declining production profile, this is expected to flip starting in Q3 with extremely easy comps on deck."

Meanwhile, if we look at the bigger picture, Barrick's all-in sustaining costs should improve to sub $1,150/oz in FY2024, benefiting from higher production overall, the benefit of increased production from lower-cost assets (Goldrush, Pueblo Viejo), and more normalized sustaining capital expenditures vs. another elevated year of sustaining capital in FY2023 (2023 guidance: attributable sustaining capital of $1.45 billion to $1.70 billion). Just as importantly, several producers have discussed easing of inflationary pressures, another potential tailwind if this trend continues.

So, even if we assume conservative AISC of $1,170/oz in FY2024 and a similar average realized gold price of $1,970/oz (2023 estimates: $1,960/oz), Barrick's AISC margins will improve from $573/oz in FY2022 to $800/oz in FY2024. This is a massive improvement and should help to shift sentiment surrounding the stock.

Barrick Gold - Annual Average Realized Gold Price, AISC & AISC Margins & 2023/2024 Estimates (Company Filings, Author's Chart & Estimates)

{kind=link}

In fact, if Barrick were to report AISC margins of $800/oz (2024), which I believe is achievable, its margins would only be 1% shy of its FY2020 AISC margins of $811/oz which briefly saw the stock soar to new multi-year highs at $31.20 per share. And while I think banking on a return to $31.00 per share is a stretch in the next 18 months, I think a target of $24.00 is quite achievable (50% total return), which would place Barrick at less than 9x FY2024 cash flow per share estimates ($2.85) and barely 16x free cash flow. I see these as very reasonable multiples for the world's second-largest producer, especially given that its margin and free cash flow figures should improve even further in 2025 with another massive year out of Pueblo Viejo, a full year of production from Goldrush, a full year of production from Porgera, and guidance for declining total capital expenditures for its gold business, as highlighted below.

Barrick Gold - Total Attributable Capex & Total Gold Operations Capex (Company Website)

{kind=link}

Finally, while Barrick Gold may be considered a producer in less favorable jurisdictions by some investors or a low-growth company, it's important to note that the company actually has over 45% of production from Tier-1 ranked jurisdictions (Nevada, Ontario). Meanwhile, while it has seen a decline in production over the past several years because of divestments (KCGM 50%), Lagunas Norte, Morila), assets winding down (Long Canyon, Golden Sunlight), and Porgera being placed in care & maintenance, Barrick set to return to growth. This is because Pueblo Viejo will enjoy a much larger production profile with the 14.0 million tonne per annum expansion, it has massive growth projects in Lumwana Super Pit and Reko Diq to grow gold-equivalent ounce production, Porgera will be restarted, and Cortez will also seeing growing production this decade (Robertson, Goldrush) even without factoring in growth from Hanson and Fourmile.

Barrick Gold - Quarterly Gold Production by Jurisdiction (Company Filings, Author's Chart)

{kind=link}

So, what are the main reasons that justify owning Barrick following its post Q3 earnings decline?

1. It's nearly as cheap as it was in September 2022 before staging a major reversal, trading at just ~5.6x FY2024 cash flow per share estimates at a share price of US$16.00.

2. It has easy comps on deck in Q3 2023 as it laps peak production and it has easy comps on deck on a full year basis as we head into 2024 with 2023 being weighed down by delayed production at Goldrush, elevated mine-site sustaining capital, and lower gold production.

3. The company is finally set to begin seeing growing production levels both from gold and copper, with major growth projects being investigated in its copper business and key projects nearing the finish line in its gold business (PV Expansion, Goldrush ramp-up, Porgera restart).

4. The company is opportunistically buying back shares, continues to grow resources and reserves, and is benefiting from a higher gold price, all pointing to per share growth with the hard work by previous Randgold CEO Mark Bristow finally starting to be realized and show up in its results.

Summary

Barrick Gold may be out of favor today, but with margins, free cash flow and production all set to rise materially, I would expect this to translate to improved sentiment for Barrick going forward.

So, while rearview mirror statistics (declining production, rising costs, paltry free cash flow generation) might prompt some to steer clear of Barrick, this makes little sense when easy comps are finally in place and the company is set to see a significant improvement in its financial results going forward, even if gold prices lose the $1,900/oz level. In summary, with the stock hovering below US$16.00 following a largely telegraphed weak Q2 report (pre-reported) and trading near its most attractive valuation levels in years outside of Q3 2022 and Q1 2020, I see the stock as a Buy.

For further details see:

Barrick Gold: Easy Comps In Q3 Makes It A Buy Near Trough Multiples