BFFAF - BASF: Disappointing Results

Summary

- Competitiveness in Europe is declining, so BASF's plan is to increase CAPEX investment outside the old continent.

- There is a risk of a dividend policy change (based on an FCF generation projection).

- Low cycle, margin pressure, and an economic slowdown are facts. We might suffer short-term turbulences, but BASF is still BASF. They 'create chemistry'.

After a few days to digest all the information released, we are back to provide an update on the German chemical player BASF ( OTCQX:BASFY , OTCQX:BFFAF ). Today, we are not providing a buy case recap; however, it is important to report a few latest developments:

- In April 2022, we published an analysis to investigate BASF's direct/indirect exposure to Russia . Later on, given the Wintershall Dea uncertainty, we decided to remove from BASF's sum-of-the-parts valuation and deduce €4 per share;

- In October 2022, after the Q3 results, we derived BASF's outlook for the Q4 EBIT, which we forecasted at €500 million and, at that time, it was much below Wall Street estimates;

- In January 2023, we presented an analysis called: Lower EU Gas Prices, BASF Is Our Top Pick , where we emphasized how: 3/4 of BASF's total operating profit (EBIT) was coming from non-EU countries, the gas price was going down, and the company was still yielding more than 7%.

What's gone wrong?

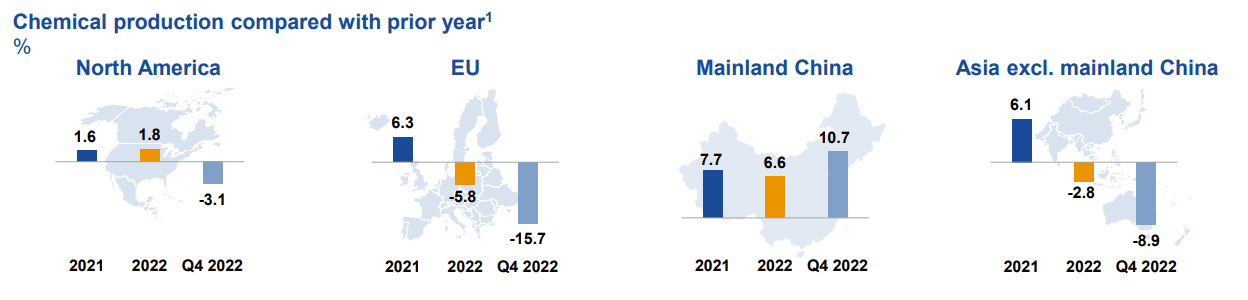

First of all, the European chemical market is significantly declining. Higher cost basis and capacity addition from comps in favorite geographies (Turkey, for instance) are eroding BASF's dominant position (Fig 1).

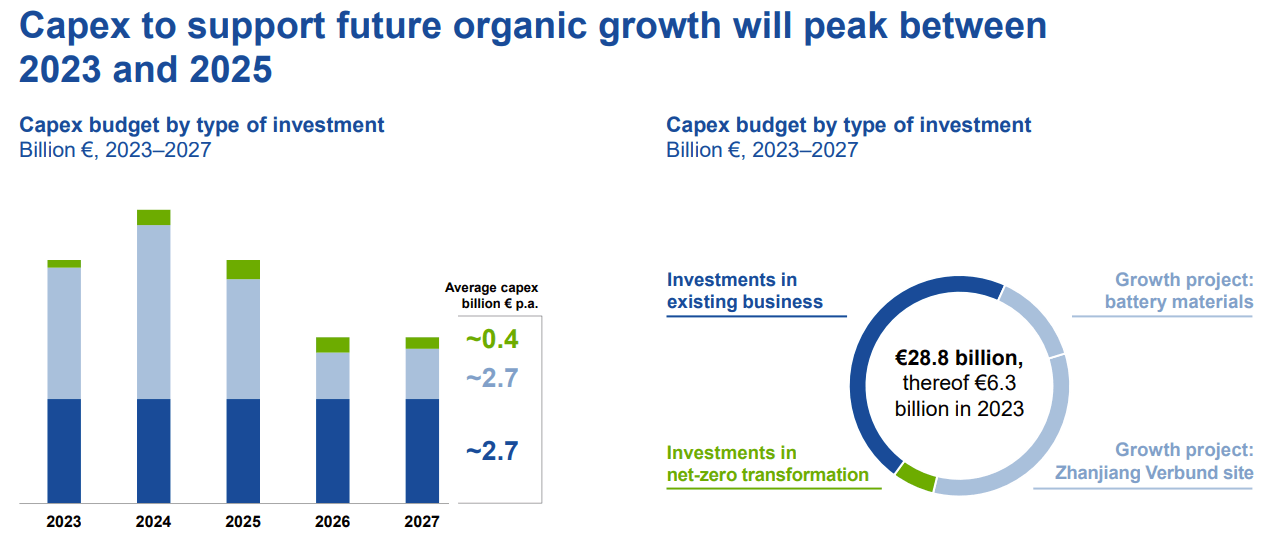

From a strategic point of view, the company announced an investment CAPEX plan of approximately €28.8 billion (€6.3 billion in 2023) to support future top-line sales growth. As you can see from Fig 2, CAPEX will peak between 2023 and 2025. In detail, to move its presence towards higher-growth & lower-cost areas, the German chemical leader decided to predominantly deploy the capital outside of Europe, and overall, this coincides with a low cycle demand.

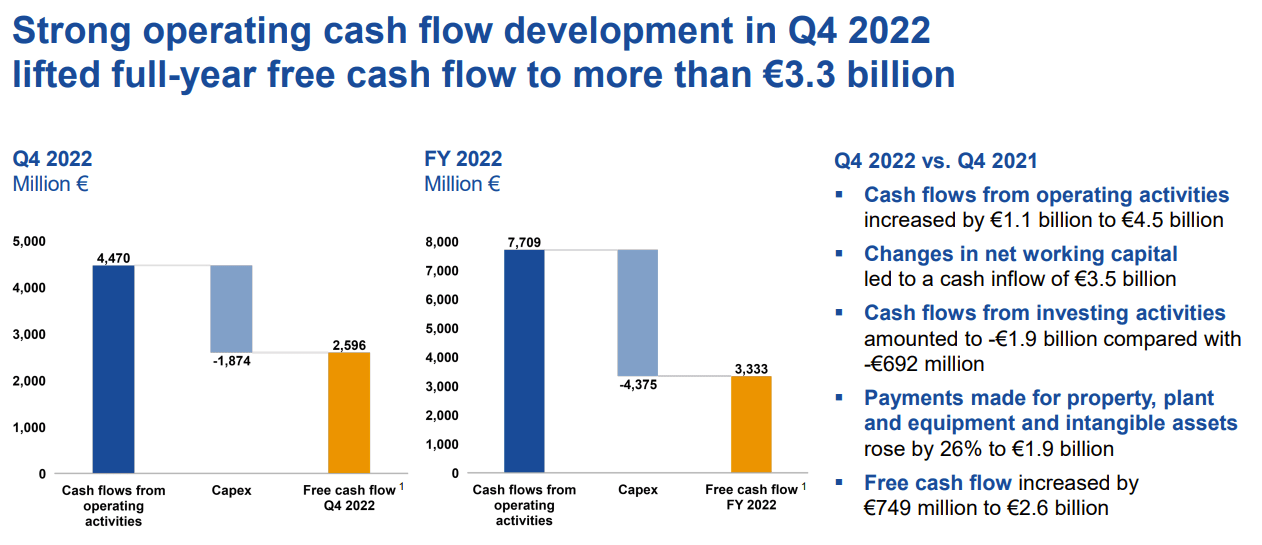

In 2022, BASF FCF was above the dividend payment requirements. In detail, the company's free cash flow reached €3.3 billion and signed a minus 10.2% on a yearly basis. However, if we add the €6.3 billion CAPEX investment schedule for 2023, BASF won't be able to cover its dividend with the FCF generation.

So, we are not surprised to see a flat dividend confirmation from the management team. This adds another concern, increasing interest rates might hit BASF's profitability. As a result, we are forecasting BASF's cash flow with a €3 billion (plus) deficit for this year. In addition, based on the forecasted period, we believe that BASF FCF will be negligible until 2025.

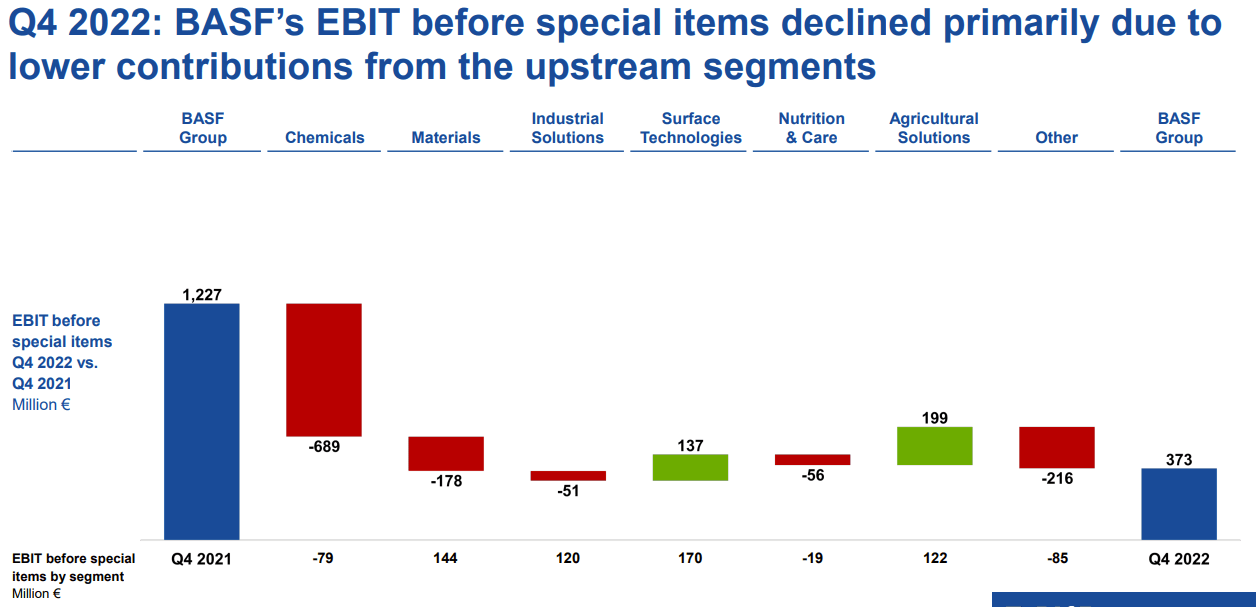

As already mentioned in point 3), we estimated a Q4 EBIT of €500 million; however, BASF reported a lower number at €373 million (Fig 4). Considering the fact that we are projecting higher debt evolution and this year, net debt reached €16.26 billion, we decided to make minor changes to the company EBIT projection, arriving at €4.8 billion for 2023.

Cross-checking sell-side analysts, another negative concern was due to BASF's €1 billion cost savings plan. From what we understood, Wall Street believes that there were no assumptions about higher fixed costs, and more important, there was no visibility on the to-do list. Looking at the press release , BASF emphasizes that it is in their interest to retain wide-ranging experience employees, especially since there are vacancies and many colleagues will retire in the next few years. The CEO also explained that these " measures will be implemented stepwise by the end of 2026 and are expected to reduce fixed costs by more than €200 million per year ".

Still related to BASF's outlook, the company implied a significant tailwind in China and an improving demand in Europe in the second part of the year; however, neither of these is evident at this point.

{kind=link}

Source: BASF Q4 and FY 2022 results presentation (Fig 1)

{kind=link}

(Fig 2)

{kind=link}

(Fig 3)

{kind=link}

(Fig 4)

Conclusion and Valuation

Here at the Lab, we are cautious about BASF's Fiscal Year 2023 earnings. Keeping the dividend at €3.40 per share means a total payout of €3 billion, and we acknowledge that management might push BASF leverage to high-end industry standard (2.35x 2024 Net debt on EBITDA), forecasting a flat DPS. According to our calculation, the dividend alone accounts for a plus 0.3x net debt /EBITDA per year. Lower gas costs should be a positive catalyst in the short term; however, they are still twice higher as the historic price. Higher interest rates, protectionist pressure, and a lower demand given a possible economic slowdown are negative points that cannot be unnoticed. Despite BASF's compelling valuation, and tasty dividend per share, we are not so confident in the short term. However, looking at the long-term horizon, BASF is trading at a higher discount on the EV/EBITDA (14% vs 7%), so we decided to value the German company with a Price Earning of 7x (in line with our past valuation), and we derive a price target of €55 per share ($11.8 in ADR).

For further details see:

BASF: Disappointing Results