BFFAF - BASF May Have To Write Down Some Or All EU Assets This Decade

2023-03-23 09:00:00 ET

Summary

- For now, BASF's European operations are mostly producing at reduced capacity or are temporarily idled.

- Many of its EU assets risk being written down, due to a lack of affordable and ample natural gas supplies to the EU market for the foreseeable future.

- For now, EU subsidies are keeping the chemical industry afloat. When it will stop helping companies cope with the high price of natural gas, BASF will most likely start divesting.

Investment thesis: As the economic divorce between the EU & Russia takes on the shape of being the new status quo for both sides, for the foreseeable future, BASF (BASFY) decided to write down its Russian assets . It is a costly decision mandated by political and geopolitical realities. BASF may have to do the same going forward at many of its European operations, not due to politics, but rather because of economics. Europe is probably always going to be just an unfavorable weather pattern event away from an energy disaster event, with no end in sight to the current situation. In between such disaster events, things will be less than ideal. It is hardly the optimal location for a company like BASF to operate, given that it uses natural gas as a feedstock for its petrochemicals, in addition to consuming large volumes of energy for its operations. At some point, most likely once EU governments cease to provide aid to industries affected by the energy crisis, it will probably have to start writing down at least some of its EU plants, taking significant financial losses in the process.

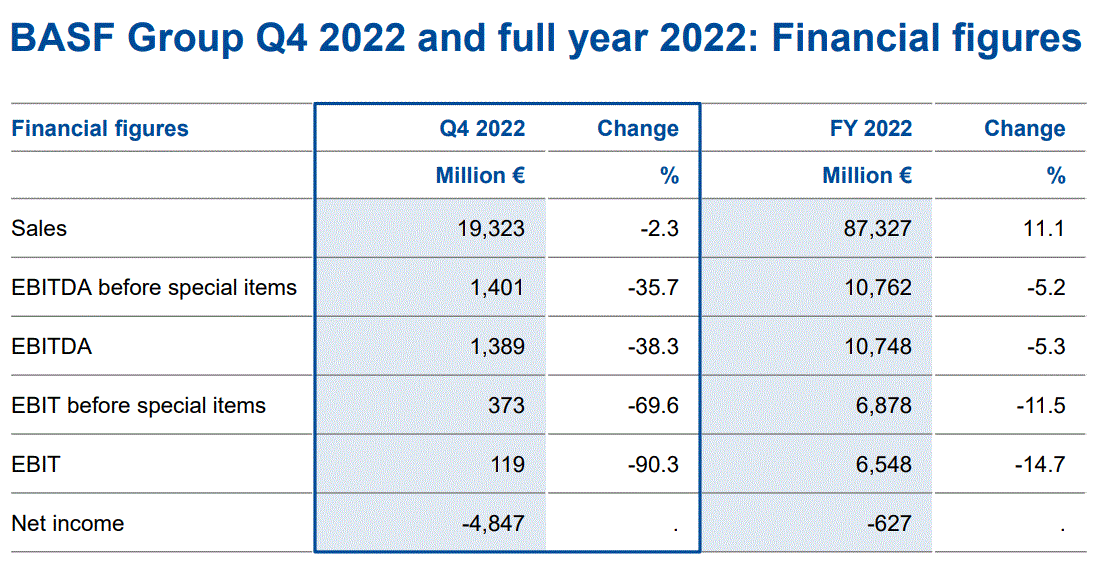

BASF's financial numbers held up alright until the last quarter of last year.

{kind=link}

BASF's net income for 2022 came in at a loss of 627 million euros. It is not a very significant margin of loss, given 83.3 billion euros in revenues, coming in at less than 1%. It is also arguably, not at all bad given that BASF's operations are based in Europe to a greater degree than they are in the rest of the world. As we know, 2022 has been a year of great turmoil in Europe in terms of energy supply issues, due to the Ukraine war.

The massive quarterly loss in Q4 is what turned a year that for the first nine months looked surprisingly strong for BASF, into a less-than-stellar year. The main factor that caused the massive loss in the fourth quarter was a writedown of its Russian assets that had an impact of 4.7 billion euros in the fourth quarter.

It may be tempting to declare the Russia-related writedown to be a one-time hit, which will allow BASF to just move on from here. Unfortunately, it may be just the beginning of what may turn out to be years of asset writedowns in Europe. These write-downs may feature as non-cash losses, but the loss of revenue-generating capacity, the loss of company asset value, and other negative aspects are very real.

Europe's energy crisis is not over, and it could potentially linger and even get worse this decade.

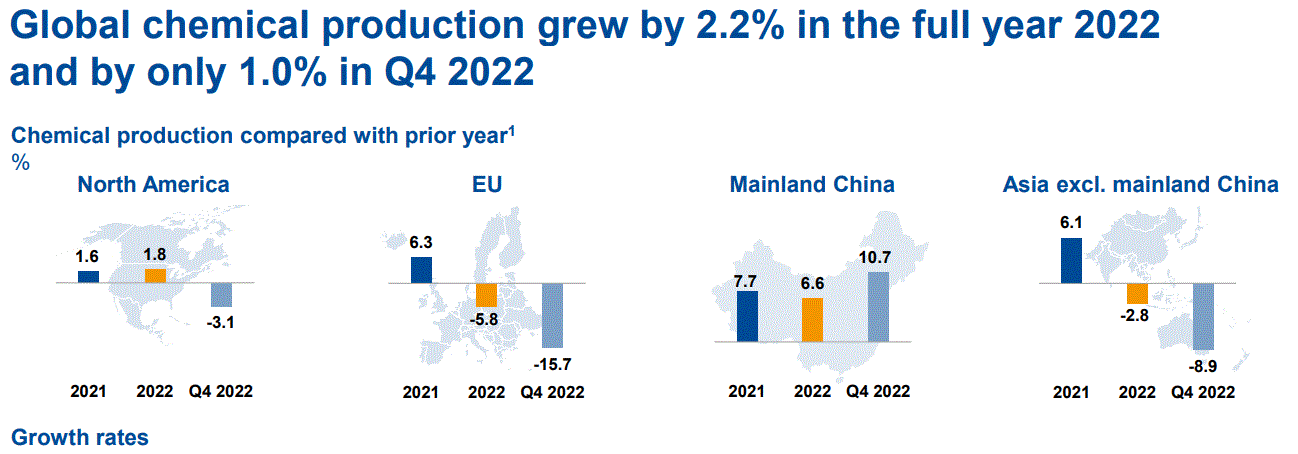

Global petrochemical production saw some regions grow last year, while Europe saw a significant decline of almost 6%.

{kind=link}

As we can see, the fourth quarter was particularly brutal for Europe's chemicals industry. It correlates with the start of the winter heating season, which requires the allocation of natural gas supplies to households, retail, services, and other businesses that tend to require heating for employees as well as for the comfort of customers. It is a reflection of the roughly one-fifth decline in natural gas demand that the EU experienced in the past fall & winter.

Overall EU natural gas demand declined by 13% or 55 Bcm in 2022, and the IEA believes that the EU should work towards cutting demand by another roughly 40 Bcm this year. Russian exports to the EU amounted to 155 Bcm in 2021, while this year, Russian supplies to the EU will be minimal. It, therefore, seems that the IEA expects the EU to rely mostly on demand cuts, which amount to about a quarter of the total average yearly EU demand we have seen in past years in order to make ends meet. The rest will be made up of mostly extra LNG imports, which are set to continue driving up the EU natural gas spot price since it is the only way for the EU to attract those extra volumes.

EU natural gas demand will probably have to remain depressed beyond this year, for potentially an indefinite period of time. Some of the demand destruction is already occurring through substitution, which should gradually help to normalize the new demand levels. Households, government facilities, and businesses helped a great deal in the past winter by preserving natural gas at the cost of some discomfort, as thermostats were turned down by a few degrees from ideal. The mild winter helped a great deal in this regard. We should not expect favorable weather to intervene every year. Furthermore, households and other entities should not be expected to accept personal discomfort forever. Eventually, people will demand to have reasonable living conditions, at a reasonable price that they can afford to pay in terms of utility costs.

What this means is that the burden of demand reduction will probably increasingly fall on energy-intensive businesses, as well as industrial sectors that use natural gas as a feedstock, like the chemicals sector. BASF, along with other chemical companies will have to consider abandoning, in other words, permanently shutting down at least some of their EU operations in response to a potential institutionalization of the European energy crisis.

It is becoming increasingly hard to see a path for the EU to regain enough affordable natural gas supply volumes to feed an industrial base that evolved along with decades of growing dependency on large-scale, affordable, and dependable volumes of Russian natural gas imports. There is no replacement for it, aside from mostly far more expensive LNG imports. In fact, things may get worse as Norway's oil & gas production is forecast to start declining within a year or two at the most. Norway has been the secondary pillar on which affordable & dependable natural gas supplies for Europe were resting.

Investment implications:

For a better illustration of how the current European natural gas crisis which is still ongoing and likely to be permanent has affected BASF's European operations, perhaps the best measure is its own analysis of EBIT evolutions across regions.

BASF

As we can see, the second half of 2022 was challenging in most regions, but nowhere did it get as severe as it did in Germany, its home base, and the country that has been arguably the most affected by the loss of Russian gas imports. LNG imports, which is what Germany has been increasingly relying on in the past months, clearly are not cutting it. The cost is too high, and its availability is not dependable enough for a chemicals company like BASF to operate profitably and with predictable outlooks that allow for future business planning.

Germany is probably where we will see the first BASF facilities put on the chopping block. It may try to sell them for nothing since some of those facilities are doomed to never recover their profitability prospects. It is possible that we would have seen an effort to divest already if it were not for robust German government financial support for the industrial sector in the past year. The measures amounting to 200 billion euros will last into next year, after which there will probably be very little left for the chemical industry, which is particularly vulnerable to justify continuing operations in Europe.

The energy crisis mitigation spending levels that we are seeing right now all across the EU, meant to blunt the impact of the energy crisis are not sustainable. Neither is it sustainable to ask households to live in less-than-ideal conditions in their homes in order to save energy indefinitely. People might accept some measures only as a temporary necessity, not as a new normal. What is left then is for industries that are natural gas intensive to re-adapt to what is now increasingly shaping up to be a new reality, with no prospects of improvement for the foreseeable future.

BASF will have to adjust if the global energy flows will realign in a way that will leave Europe out in the cold, by incurring repeated asset writedowns in Europe. The timing may not be certain, but odds are that it will coincide with the end of government support programs for the industry. If it closes European plants, it will also strive to open new ones in places like North America or China, with the latter set to sow up a large portion of Russia's pipeline gas exports, in addition to the resources available from Central Asia. The new capital spending needs will weigh heavily on its finances going forward, in addition to the costs of divestment. The dividend which is currently over 7%, may not be sustainable unless by some miracle the EU energy dissipates. Taking all the above-mentioned factors into account, I do not see a good reason to be invested in this stock at the current valuation level. The odds are far greater and more pronounced for the downside outcome than they are for any potential upside scenario, therefore the risk/reward considerations do not add up.

For further details see:

BASF May Have To Write Down Some Or All EU Assets This Decade