FUPEF - BASF: Still A Good Long-Term Investment

Summary

- Despite huge challenges, BASF SE is still reporting solid results.

- The new Verbund site in China and the shift towards electric vehicles should contribute to growth for BASF.

- While there are risks for the dividend - due to potential government support and low free cash flow - BASF will probably keep the dividend stable.

- BASF is still undervalued - the stock is trading for extremely low valuation multiples.

In early 2022, I bought BASF SE ( BASFY ), the largest chemical producer in the world and one of the major corporations in Germany. In March, I published an article explaining my reasoning why I bought BASF. As I write this, the position is trading about 7% below the price I bought the stocks. When including the dividend payments, I am at plus/minus zero.

While this is not a great performance, the investment actually outperformed the S&P 500 Index (SP500) so far. And I will keep on holding BASF in my portfolio. In this article, I provide an update on the business and explain why I still think BASF is a good investment - despite the challenging market environment.

Quarterly Results

Considering the difficulties BASF is facing, the company actually reported solid results in the last quarter ( Q3 2022 ) as well as the first nine months of fiscal 2022. In the first quarter of fiscal 2022, sales increased from €19,669 million in the same quarter last year to €21,946 million this quarter - resulting in 11.6% year-over-year growth. But income from operations (EBIT) declined 29.0% YoY from €1,822 million in Q3/21 to €1,294 million in Q3/22, and earnings per share also declined 25.7% YoY from €1.36 in the same quarter last year to €1.01 this quarter. Free cash flow ("FCF"), on the other hand, increased from €1,077 million in Q3/21 to €1,295 million in Q3/22 - an increase of 20.2% YoY.

BASF Capital Market Story Presentation

{kind=link}

When looking at the results for the first nine months of fiscal 2022, we see a similar picture. Sales increased from €58,822 million in the first nine months of 2021 to €68,003 million in the first nine months of 2022 - resulting in 15.6% year-over-year growth. EBIT declined slightly (0.3% YoY) from €6,449 million to €6,429 million. And earnings per share also declined from €5.03 in the first nine months of 2021 to €4.67 in the first nine months of 2022 - a decline of 7.2% YoY. On the other hand, adjusted earnings per share increased 22.5% from €5.59 in the first nine months of 2021 to €6.85 this year. Free cash flow, however, declined from €1,866 million to only €783 million.

BASF Capital Market Story Presentation

{kind=link}

And for the full year fiscal 2022, BASF is expecting sales to be between €86 billion and €89 billion - compared to €78.6 billion in sales in 2021, resulting in about 9.5% to about 13% topline growth. EBIT before special items is expected to be in a range between €6.8 billion to €7.2 billion, and compared to €7.8 billion in 2021 this is reflecting a decline of 7.5% to about 13%.

Problem

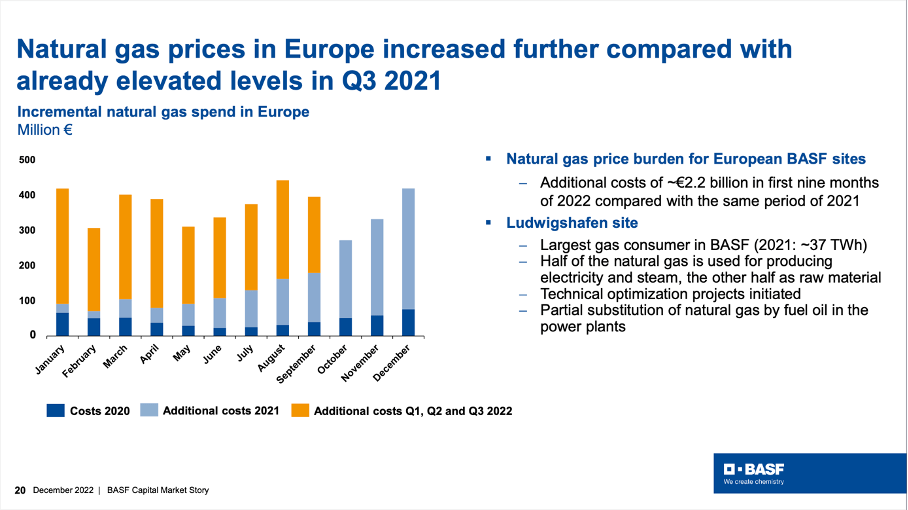

But considering the huge problems BASF is facing, the company has performed quite well in 2022. Especially the high natural gas prices in Europe are a huge burden for the business and led to additional costs of €2.2 billion in the first nine months of 2022 (compared with the same period of 2021). And costs in 2021 already were much higher than in 2020.

BASF Capital Market Story Presentation

{kind=link}

Although BASF is still able to handle these expenses and report a profit, the company is focusing on permanent cost reductions as well as structural adjustments. The implementation is starting right now and should be completed by the end of 2024, and the program is expected to generate about €500 million in annual cost savings. It is always difficult to make predictions - and I honestly don't know much about the energy market and natural gas prices - but I would not assume gas prices get even higher over the next few years. On the other hand, we also should not expect gas prices to fall back down to 2020 levels in the foreseeable future.

High Capital Expenditures

Another temporary problem we are seeing is the high capital expenditures, although this is not a structural problem. As I wrote in my last article, BASF is expecting rather high capital expenditures in the next few years. Between 2022 and 2026, the company is expecting €25.6 billion in capital expenditures - about €5.1 billion to €5.2 billion annually on average, with the peak coming in 2024. The capital expenditures are evenly distributed between investments in existing businesses and investments in growth projects (especially battery material and the Zhanjiang Verbund site). This has several implications. Let's start with the positive side - the growth potential that will arise from these massive investments.

Drivers of Long-term Growth

When looking at drivers for long-term growth, we must mention two projects - the new Verbund site in China as well as the shift to EV. These are also those two projects BASF is heavily investing in.

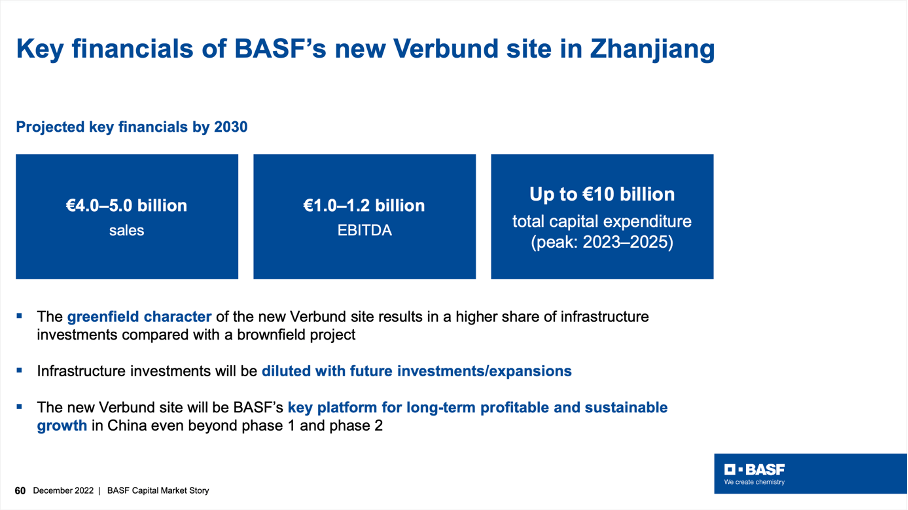

The biggest project for BASF right now is the new Verbund site in Zhanjiang, China - located in Guangdong province, which is seen as the economic growth engine of China and a powerhouse of BASF's key customer industries. And while worldwide chemical production is expected to grow with a CAGR of 3.0% till fiscal 2030 and reach a market of $5.6 trillion, demand in Greater China is expected to grow with a CAGR of 4.04%. By 2030, Greater China likely will account for more than half of the world's chemical production.

During the last earnings call , management also underlined again it does not want to delay the investments in the new Verbund site in any way to achieve returns from this investment as soon as possible. First, downstream plant started in August 2022 and is producing performance materials for automotive and consumer industries. And until 2030, BASF is expecting €4.0 billion to €5.0 billion in annual sales and about €1.0 to €1.2 billion in EBITDA. And while this will be a solid contributor to growth, the project will also eat up about €10 billion in total capital expenditures (peak will be between 2023 and 2025).

BASF Capital Market Story Presentation

{kind=link}

A second driver of growth is the expected shift towards electric vehicles ("EVs"). The chemical content per car is about 2.5 times higher in an electric vehicle (compared to a car with an internal combustion engine ("ICE")). And especially the CAM (cathode active material) as a key component of any battery cell more than doubles the chemical content which can be found in today's average ICE vehicle. And the market for CAM will grow with a CAGR of 22% annually and reach a total size of 7,2000 thousand tons by 2030 (about 60% of demand will stem from Asia). BASF is targeting a market share above 10% and is expecting about €1.5 billion in sales in 2023 and about €7 billion in sales in 2030.

BASF Capital Market Story Presentation

{kind=link}

In my last article about Fuchs Petrolub ( FUPEF ), I also talked about the growth potential electronic vehicles will offer. However, management of Fuchs Petrolub is not expecting EV to grow at such a high pace as most are expecting and seems to be a little more cautious.

Free Cash Flow?

Aside from future growth potential, we are seeing a problem in the next few years. The extremely high spendings result in a rather low free cash flow. Over the long term, these capital expenditures probably make sense and will lead to higher revenue (and free cash flow), but over the next few years, they will lead to a rather low free cash flow for BASF.

BASF Capital Market Story Presentation

{kind=link}

In the last ten years, the average free cash flow from operations was €7,586 million. In the last five years, average free cash flow from operations was €7,407 million. And when assuming capital expenditures of €5.12 billion annually for the years till 2026 this is resulting in a free cash flow of €2.4 billion (which we take as a basis in our calculation - see below). And when assuming that BASF will have about €2.5 billion lower capital expenditures from fiscal 2027 going forward, free cash flow could be as high as €4.9 billion.

Dividend and Share Buyback

Another problem that seems to arise is the dividend safety for BASF. At this point, I don't really think the dividend will be cut. However, there are two potential risks for the dividend. First, the major capital expenditures are reducing the free cash flow to a level where we can't be sure if BASF is able to cover its dividend. When taking cash from operations from the last few years and capital expenditures, the average free cash flow could be around €2.5 billion which is not enough to pay €3,072 million in dividends (dividend payments for fiscal 2021). But during the last earnings call, management assured analysts that the dividend is covered:

So the short answer to your question is, we fully expect to cover the dividend with the free cash flow and the expectation is also that from a free cash flow perspective, Q4 will be a very strong quarter.

Another challenge for the dividend is the German "Gaspreisbremse" - a subsidy scheme in Germany paying consumers' gas bills beyond a certain threshold. And there is a major discussion if companies profiting from government support are allowed to pay dividends (see here and here - both sources in German!). Right now, it seems like BASF will forgo any government support as long as it is unclear if the company will be allowed to pay dividends. During the last earnings call, CEO Martin Brudermüller made BASF's position clear when asked about the dividend by an analyst:

Let me say, we are entrepreneurs. And that means we want to take the decisions what is right and wrong for the company. And I don't want to have any side strengths that we get something in that we are limited in deciding what we think is the right thing. The dividend policy is high ranking for us, you know that. And that's also what we communicated. So, I have a hard time if anyone tells me or tells us what the right dividend policy is. So, I think this gives you some indication that whatever is possible we try to do on our own feet. I think also very clearly, there is a responsibility for everyone. That's for a private person, but also for a company. We cannot - it cannot work that everything is paid by public. So, if everyone just opens their hand and say, give me the delta and the difference for the next 2 years or 3 years and then I continue when energy prices come down, we will be over-debted and it will be a disaster for the next generations to come.

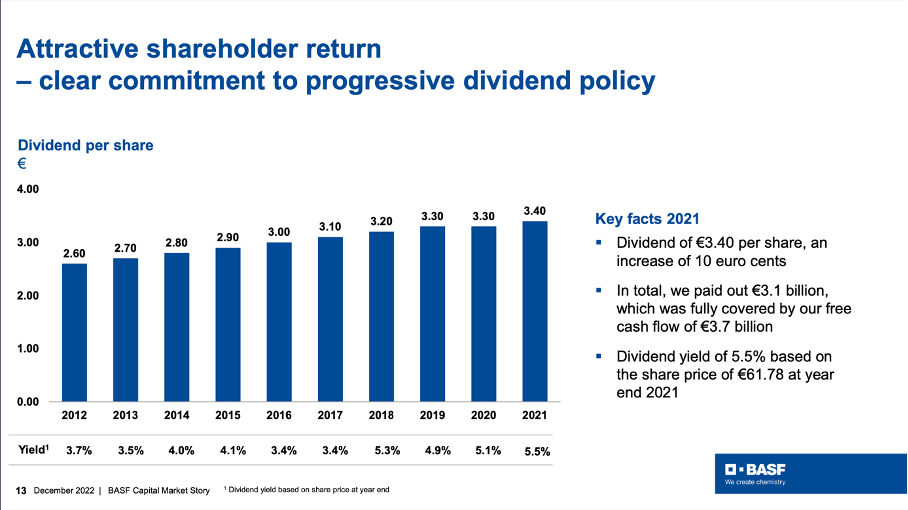

When looking at these statements, we can be rather confident that BASF will pay a dividend in 2023 (for fiscal 2022), and we can expect BASF to keep the dividend at least stable. And if BASF should pay an annual dividend of €3.40 once again, this is resulting in a dividend yield of almost 7.5%.

BASF Capital Market Story Presentation

{kind=link}

Aside from the dividend, BASF issued a share buyback program in January 2022 with a volume of up to €3 billion. At current share prices, BASF could repurchase about 7% of its outstanding shares ( here you can see the amounts spent and shares purchases so far). All in all, this is a smart move - despite the lower free cash flow due to high capital expenditures - as the stock is trading below its intrinsic value.

Intrinsic Value Calculation

When looking at simple valuation metrics, BASF seems to be extremely cheap. In the last four quarters, BASF generated €5.65 in earnings per share, which is resulting in a P/E ratio of only 8. And when using the adjusted earnings per share (€8.02 in the last four quarters), BASF is trading for a ridiculously cheap valuation multiple of 5.7. Aside from looking at earnings per share, we can also look at the free cash flow and in the last four quarters, the company generated an FCF of €2,585 million resulting in a P/FCF ratio of 15.7. And as I have written frequently in the past, I consider the P/FCF the most important one among the simple valuation metrics.

And aside from looking at simple valuation metrics, we can also use a discount cash flow calculation to determine an intrinsic value. And according to the statements from above, we calculate with the following assumptions.

Until 2030, BASF is expecting between €11 billion and €12 billion in additional revenue from its new Verbund site in China and the higher demand due to batteries for EV. This is resulting in about 1.5% topline growth. Additionally, we can expect about €2.5 billion to €3 billion in additional EBIT, resulting in about 4.0% to 4.5% growth for the bottom line. And this is only growth stemming from the new Verbund site as well as EV. As we can also assume growth from existing Verbund sites and maybe a further margin improvement, we can expect about 4% to 5% bottom line growth for BASF.

And for the next four years (fiscal 2023 till fiscal 2026), we are rather cautious and assume only €2,400 million in free cash flow for fiscal 2023 (according to calculations above) and 4% growth for the following years. As mentioned above, spendings will be rather high in the next four years, leading to a lower free cash flow. For fiscal 2027, we assume €4,000 million in free cash flow - due to much lower CapEx and because even higher assumptions seem too optimistic - and once again 4% growth for the following years. We also assume 4% growth till perpetuity. When calculating with these assumptions and a 10% discount rate as well as 918.5 million outstanding shares, we get an intrinsic value of €58.33 for BASF. And when being more optimistic and calculating with 5% instead of 4%, we get an intrinsic value of €68.36.

And when looking at past growth rates, 5% growth is not an unrealistic assumption. Over the last ten years, BASF was struggling a bit, but when looking at longer timeframes, growth rates in the mid-single digits are not unrealistic.

| CAGR | Since 1980 | Since 1990 | Since 2000 | Since 2010 |

|---|---|---|---|---|

| Revenue | ||||

| 4.27% | ||||

| 3.92% | ||||

| 3.80% | ||||

| 1.90% | ||||

| EPS | ||||

| 8.28% | ||||

| 8.35% | ||||

| 8.86% | ||||

| 1.76% |

Conclusion

Even when calculating with cautious assumptions, BASF seems to be undervalued at this point. And there is the possibility for BASF growing at a higher pace than 4% in the next few years. While higher growth rates are possible for BASF, I would not count on that scenario, but BASF must only grow in the low-to-mid single digits in the coming years to be fairly valued or even undervalued.

For further details see:

BASF: Still A Good Long-Term Investment