BSET - Bassett Furniture: Cheap New Tech Innovations And Opening In Dallas

2023-04-08 01:32:40 ET

Summary

- Bassett Furniture is a leading home furniture retailer, manufacturer, and marketer in the United States.

- I believe that it is a great moment to review the business model because demand appears to be normalizing, and shortage of raw materials continues to improve.

- In my view, the implementation of new technologies, such as the virtual appointment program, may allow management to increase the reach of its business.

Bassett Furniture Industries, Incorporated ( BSET ) is adapting its long term expertise in the furniture industry to a new online sales model. Considering the state of the financial situation, I believe that Bassett is well positioned to invest in online marketing as well as to hire new experts in the field. I am optimistic about the current stock repurchase program. Even considering risks from failed technology implementation, I think that BSET stock is undervalued, and I am not the only one of this view.

Product Analysis

Bassett Furniture is a leading home furniture retailer, manufacturer, and marketer in the United States. It was founded in 1902.

The company sells its products primarily through a network of company-owned and licensee-owned brand-name stores under the name Bassett Home Furnishings, with additional distribution through other wholesale channels. They also sell products through the website of the company.

With 92 BHF stores as of February 25, 2023, the company's store program is designed to provide a single-source home furnishings retailer offering a unique blend of stylish, quality furniture and accessories at a high level of customer service.

In addition, the company has factories in Newton, North Carolina, Martinsville, and Bassett, Virginia, where it manufactures and assembles high-quality, custom home furnishings. Bassett Furniture also has an outdoor furniture brand, Lane Venture, which it distributes through other wholesale channels, and a Bassett outdoor furniture brand that is marketed through its BHF store network. I believe that it is a great moment to review the business model because demand appears to be normalizing , and shortage of raw materials continues to improve. Management also believes that inflationary pressures are not that problematic as there seems to exist moderation in input costs. In my view, these effects, among others, will likely bring back free cash flow in the coming years.

The Company Targets Very Specific Customers With Family Earnings Above $150K, Which Will Likely Make FCF Margins A Bit More Solid Than Peers

In my view, Bassett is extremely talented while selecting its long-term customers. The company targets families making close to $150k per year, which, in my view, would bring significant operating margins. In my view, these are customers who may not pay attention to the price of furniture.

I also appreciate that the company reports a strong domestic manufacturing footprint, which means that management may not have to deal with freight costs as well as unreliable supply-chains in Asia. In my view, the FCF margins will be a bit more solid than the competitors buying furniture in China or overseas.

Balance Sheet: No Debt, Financing Received From Customers, And Beneficial Terms From Lease Agreements

Since November 2022, Bassett has not reported significant changes in the balance sheet. Management continues to report significant liquidity, including cash and cash equivalents of $54 million, short-term investments of close to $17 million, and accounts receivable of $18 million. Besides, with inventories close to $79 million, total current assets stand at close to $183 million. With these figures in mind, I would be concerned about the current liquidity.

Non-current assets include property and equipment of $78 million, goodwill and other intangible assets worth close to $21 million, right of use assets under operating leases of around $96 million, and total long-term assets of $129 million. The asset/liability ratio is equal to 3.5x-4x, so in sum, the financial situation appears quite beneficial.

Source: 10-Q

I would not be worried about the list of liabilities because the company does not really report a lot of financial obligations. The most relevant liabilities are accounts payable worth $17 million, accrued compensation and benefits of $9 million, customer deposits worth close to $31 million, post-employment benefit obligations worth close to $10 million, and long-term portion of operating lease obligations of $93 million. Total long-term liabilities are equal to $107 million. In my view, Bassett receives financing from customers' deposits, and the leases signed by management appear quite beneficial. The fact that management does not really have to receive financing from banks is appealing.

Source: 10-Q

Expectations For The Future And My Assumptions

I am quite optimistic about the company's business strategies focused on adapting to constantly evolving market demands and taking advantage of the opportunities presented right after the pandemic. In my view, the implementation of new technologies, such as the virtual appointment program, may allow management to increase the reach of its business as well as to improve the customer experience. The company is also investing in digital advertising and outreach to attract more customers to its website as well as to increase online sales. In my opinion, sooner or later these efforts will likely bring revenue generation and FCF growth.

Besides, management is carefully evaluating its range of personalized products to offer a better online and in-store shopping experience. Additionally, I am optimistic about the analysis of its physical store model that the company noted in the last quarterly report. For instance, management appears to be emphasizing its commitment to local manufacturing and the use of organic materials. In my opinion, if customers appreciate the new changes and new offerings, or the target market expands, the company would experience business growth. In line with these remarks, I would recommend having a look at the following explanations given by management.

2023 is a big year from a technology standpoint as our long-awaited digital transformation becomes more obvious with the debut of our new web platform in the next ninety days. Adding a new level of omni-channel capabilities has been a major objective from the outset and we are close to bringing it to the marketplace. Source: Quarterly Report

We elected to increase marketing expenses as well to maintain consumer engagement on the web and in our stores. Source: Quarterly Report

Investors will also do good by having a look at the stores to be opened and remodeled in 2023. In particular, it is relevant to the new store in Dallas and the new tests that management will do in new stores, which may help enhance sales in other existing stores.

Our new Dallas store opened in the period and we also remodeled two other existing locations in the Dallas market to test a new fixturing package designed to further enhance accessory sales. Source: Quarterly Report

We will begin work on our new large store (25,000 square feet) in Tampa early in April. We are excited about the new face that our latest formats put on our brand presentation, and we will monitor the performance of these locations as we consider enhancements to certain stores in the rest of the fleet. Source: Quarterly Report

I also believe that noting that management expects to continue acquiring its own shares is very relevant. Management believes that the shares are undervalued by the market.

We retired $1.8 million of our stock in the quarter and plan to continue to actively acquire shares while we believe the stock is undervalued. Source: Quarterly Report

My Cash Flow Statement Model Indicated A Fair Price Close To $27 Per Share

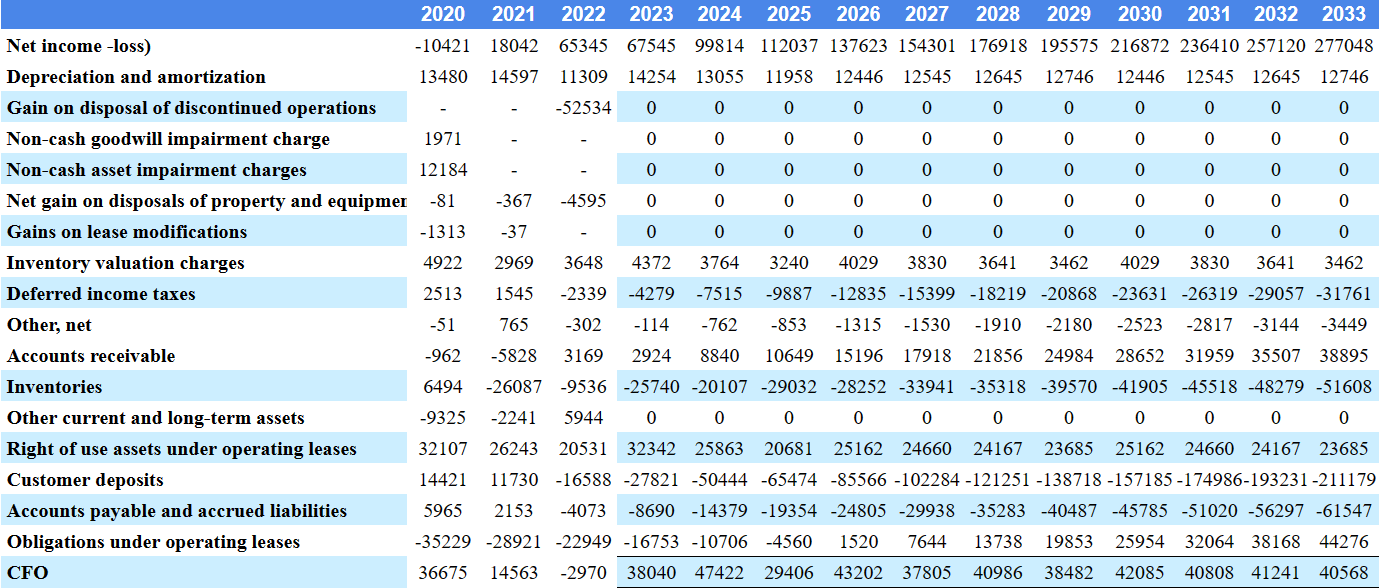

My cash flow statement includes net income growth from 2023 to 2033, D&A approximately constant, decreases in accounts payable, and decreases in customer deposits. Capital expenditures are as large as future D&A, implying growing free cash flow.

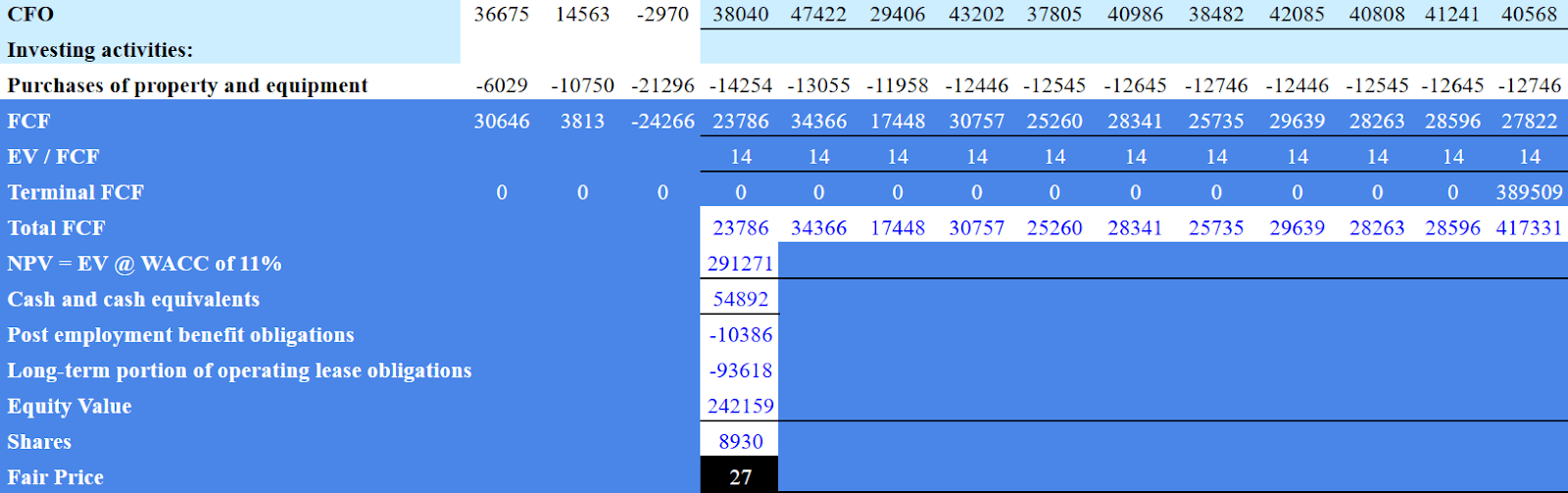

The numbers for 2033 include net income of $277 million, depreciation and amortization of $12 million, changes in deferred income taxes of close to -$32 million, changes in accounts receivable of $38 million, and changes in inventories of close to -$52 million. Besides, I also included 2033 changes in customer deposits of -$212 million, changes in accounts payable and accrued liabilities of close to -$62 million, and changes in obligations under operating leases of $44 million. Finally, the CFO would stand at $40 million with purchases of property and equipment worth close to -$13 million and 2033 free cash flow of $27 million.

{kind=link}

If we assume an exit multiple of EV/FCF of 14x and a WACC of 11%, the NPV would be close to $291 million. Now, with cash and cash equivalents of $54 million, post-employment benefit obligations worth close to -$11 million, and long-term portion of operating lease obligations of -$94 million, the equity value would stand at close to $242 million. Finally, the fair price would be close to $27 per share. My results are not far from the expectations of other analysts.

{kind=link}

Competitors

Competition in the home furnishings retail market is intense and diverse. The company faces competition from national, regional, and local retailers as well as online stores. In addition, the entry of new competitors in the market is easy due to the lack of barriers. Competitors may employ various strategies, such as aggressive advertising, pricing, and marketing, to attract customers. As a result, the company faces the risks of losing market share, revenue, and customers in addition to incurring increased expenses or price reductions, which may have a material adverse effect on its operating results.

Risks

I believe that Bassett faces a significant number of risks from competitors including home furnishings retailers and wholesalers through online sales. In my view, management appears to be successful in selling online, but there are other peers, which may have substantial expertise in creating online experiences. It is also a bit uncertain whether the company will be able to successfully sell online to its specific exclusive customer profile.

There is also the possibility of incurring losses as a result of the recent acquisition of Noa Home and the inability to anticipate or successfully respond to changes in consumer tastes and trends. Each of these risks could have a significant negative impact on the company's future business, cash flow, and results of operations. As soon as analysts lose their faith in the future revenue growth or FCF growth of Bassett, expectations may decline, and so may the stock price.

I would also expect risks from the total amount of accounts receivable and the concentration of customers. If some of these customers fail to pay, or pay later than expected, the company could face liquidity issues, or may have to receive financing from banks. In this regard, I believe that investors may want to have a look at the lines below.

On November 26, 2022, and November 27, 2021, approximately 31% and 24%, respectively, of the aggregate risk exposure, net of reserves, was attributable to five customers. In fiscal 2022, 2021 and 2020, no customer accounted for more than 10% of total consolidated net sales. Source: Annual Report

My Opinion

Bassett Furniture is a prominent company in the United States, but it was hit hard during the Covid-19 pandemic. The company is in the process of adapting to the online sales model, which, in my view, could bring significant revenue growth and FCF growth. Considering the state of the balance sheet, I believe that the company is well positioned to invest in online marketing, or hire experts in the field. Even considering potential risks from failed M&A operations, failed market campaigns, or competitors, I believe that the stock price could trade at higher marks.

For further details see:

Bassett Furniture: Cheap, New Tech Innovations, And Opening In Dallas