BSET - Bassett Furniture: Eyeing A Financial Recovery

2023-11-28 12:51:20 ET

Summary

- Bassett is facing weak demand and lower earnings due to a poor macroeconomic situation and the divestment of Zenith Freight Lines, completed in 2022.

- Bassett's future stock performance seems to largely depend on its financial recovery and ability to improve margins.

- I believe that the stock is currently priced with fair assumptions of future financials, constituting a hold rating.

Bassett ( BSET ) manufactures and retails furniture with a focus on the United States. The company is currently at an interesting point in time as Bassett is facing weak demand and the divesture of Zenith Freight Lines in FY2022 contribute to a lower earnings level. The financial recovery seems to largely determine Bassett's future stock performance.

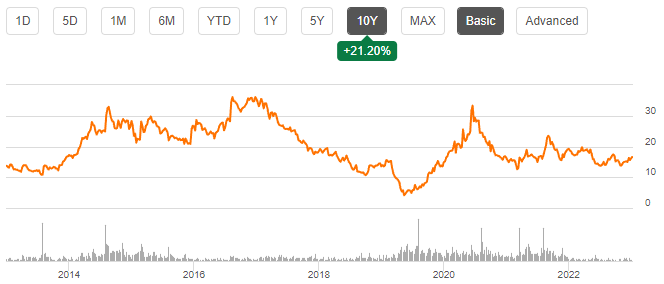

The company’s stock return has historically been quite modest – in the past ten years, the stock has appreciated by 21%. Bassett does pay out a good amount in dividends with a current yield of 4.33% .

{kind=link}

Ten Year Stock Chart (Seeking Alpha)

Sale of Zenith Freight Lines - A Contributor to Decreasing Earnings

In March of 2022, Bassett completed the sale of its logistics subsidiary, Zenith Freight Lines, to J.B. Hunt for a consideration of around $87 million. Although the transaction significantly improved Bassett’s balance sheet , the sale had its drawbacks - since the transaction was made, Bassett’s revenues and earnings have started to decline partly due to the discontinued operations. The company’s current trailing EBIT stands at $6.6 million compared to a FY2022 figure of $29.8 million.

The lost third-party sales from the transaction represented around $16.8 million in sales and $1.7 million in operating income in FY2022, in addition to Bassett’s self-use of the freight services. In the same year, Zenith’s charges for Bassett’s use of logistical services added up to around $9.1 million.

Bassett 2022 Annual Report

It is still a bit early to judge the transaction’s long-term applications – J.B. Hunt’s logistics network as a whole seems to have more coverage, and as Bassett has signed a long-term agreement with the company, the improved network could provide some benefits; the Zenith assets should be able to be utilized better under J.B. Hunt.

Contributing more significantly to the currently poor earnings is the macroeconomic situation, currently lowering Bassett's sales level – Bassett’s management sees the current demand for furniture as weak despite good business around holiday events. Due to high freight costs during the pandemic, some of Bassett’s inventory is still marked very high, contributing poorly to gross margins – as this effect subsides, Bassett’s margins should expand back into a more historical level. The sale of the Zenith assets attributes to lower earnings, but doesn't seem like the main contributor.

A Long-Term Financial View

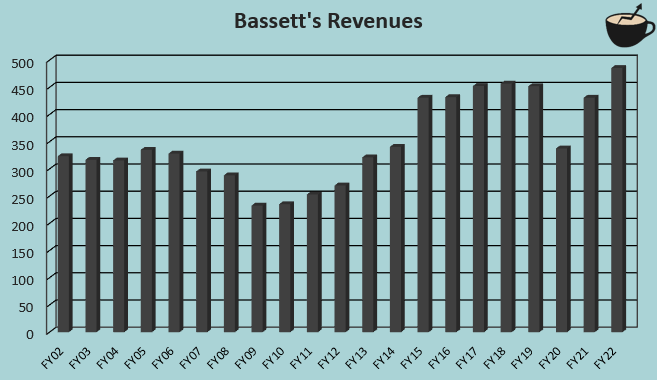

On a more long-term horizon, Bassett’s growth seems very modest with a revenue CAGR of 2.1% from FY2002 to FY2022. The furnishing industry is very mature and stable, and Bassett doesn’t seem to really have too much of a differentiation in the industry to drive market share growth – it would seem that a similar future in terms of revenues is likely.

{kind=link}

Author's Calculation Using TIKR Data

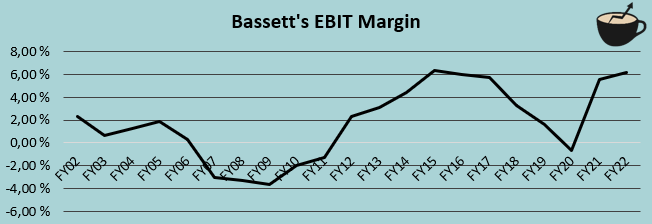

The more important question is how much of the sales is left to the bottom row; Bassett’s long-term history doesn’t seem to indicate a clear figure for the future. The company’s EBIT margin has fluctuated between -3.7% and 6.3% with an average of 1.8% between FY2002 and FY2022:

{kind=link}

Author's Calculation Using TIKR Data

Margins Seem To Determine Bassett’s Trajectory

For the investment case, I believe that investors should mostly keep a close eye on Bassett’s margin level. The company’s long-term margins have fluctuated significantly with revenues, and the sale of the Zenith assets adds further uncertainty to a sustainable future margin level.

I believe that most of the company’s current pressure in margins comes from lower gross margins than the company has achieved on a long-term basis. From FY2013 to FY2022, Bassett’s average gross margin has been 55.0% , compared to a current figure of 52.7%. In the case that Bassett’s gross margin rises back to the ten-year average, the EBIT margin would rise from the current trailing level of 1.6% into 3.9%. Due to the higher freight costs associated with the current inventory, and a weak demand, I would believe that the current gross margin is lower than it should be in the medium-term future – I believe that a recovery into near ten-year average is a reasonable expectation.

Also, the lower sales level does contribute negatively to the EBIT margin beyond a lower gross margin due to fixed costs – a higher sales level should provide some operating leverage as the sales level recovers. Bassett has been able to mitigate the effect of lower sales in the SG&A level through a good cost control – despite a good amount of inflation, Bassett’s SG&A has decreased by around $6 million in the current fiscal year compared to previous fiscal year’s figures. The leverage that higher sales should provide seems quite small, as the company has been able to vary costs, but could still provide some leverage to the EBIT margin.

Summing up, the currently low EBIT margin of 1.6% shouldn’t be considered as a base scenario for a long-term margin. After the macroeconomic situation improves, I believe that Bassett has the capability to improve the EBIT margin into a figure that’s close to 4% if gross margins recover. The margin estimate is still quite unsure – as an investor, I would suggest to keep a close eye on the margin trajectory.

Valuation

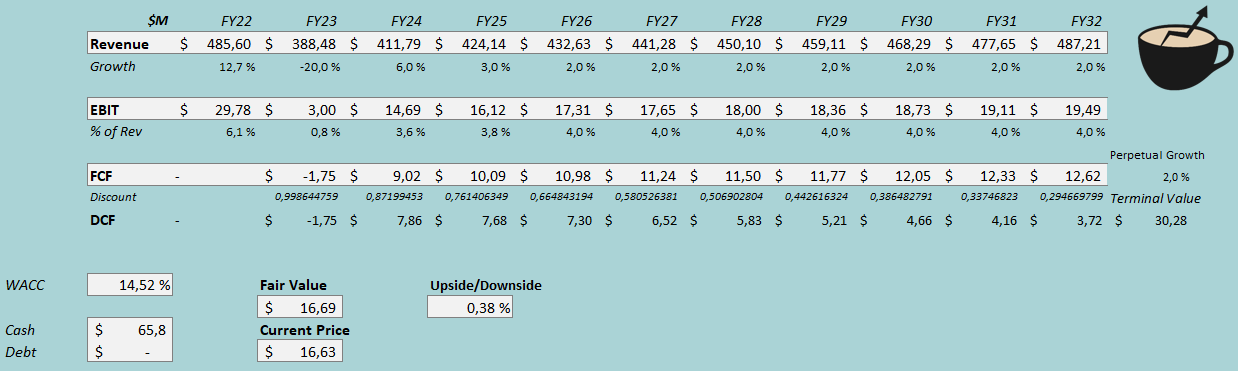

To contextualize Bassett’s valuation, I constructed a discounted cash flow model in my usual manner. In the DCF model, I factor in a sales recovery after FY2023 with a growth estimate of 6% for FY2024 and a 3% growth for FY2025. After the recovery, I estimate a perpetual revenue growth of 2%, in line with Bassett’s historical growth. For the margins, I estimate a recovery after a weak FY2023 into an eventually achieved level of 4.0% - I believe that this figure represents a fair estimate of an achievable long-term level.

With the discussed estimates along with a cost of capital of 14.52%, the DCF model estimates Bassett’s fair value at $16.74, very near the stock’s price at the time of writing – I believe that Bassett is priced with fair estimates of the company’s future financials.

{kind=link}

DCF Model (Author's Calculation)

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Bassett’s balance sheet is very strong – the company’s liabilities don’t include interest-bearing debts excluding very minimal interest payments from leases. I don’t see a scenario where Bassett leverages financing as very likely at least in the medium-term as the company’s cash balance is quite large and earnings are on a lower level – I estimate a debt-to-equity ratio of 0% for the future.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.45% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Bassett’s beta at a figure of 1.62 . Finally, I add a small liquidity premium of 0.5%, crafting a cost of equity and WACC of 14.52%.

Takeaway

Bassett seems to be priced for a partial revenue and margin recovery after FY2023. I believe that the priced-in financials represent fair estimates of Bassett’s capabilities as the company should be able to scale back its gross margin, and achieve some operating leverage from recovering sales. The previous divesture of Zenith Freight Lines clouds the financial picture a bit, but I expect the transaction to prove to be worthy in the long run as J.B. Hunt has the capabilities for more efficient management of the logistics department. At the moment, the risk-to-reward seems balanced – I have a hold rating for the time being.

For further details see:

Bassett Furniture: Eyeing A Financial Recovery