LOVE - Bassett Furniture: Future Operating Income Available Almost For Free No Really

2023-06-21 01:03:35 ET

Summary

- Bassett Furniture is a top vertical furniture manufacturer/retailer in the U.S., with close to 100 stores.

- BSET enterprise value is approaching zero, with no debt and a large cash hoard.

- Overall valuations are similar to past recession lows, which opened strong buy opportunities for investors.

- Long-term chart price support levels should limit downside to -15% to -20% in a recession scenario.

Bassett Furniture ( BSET ) is a leading furniture maker and seller in the U.S. The company has around 100 dedicated retail locations in the United States and Puerto Rico. Custom furniture orders can be made with a variety of options for upholstery, beds, dining, home storage and home entertainment items.

The bullish investment argument is based on a stock price decline over the last 12 months, pushing the equity value of the company minus cash holdings on the balance sheet closer to zero (with no real debt held). Having an enterprise value ratio on EBITDA multiple approaching 1x on a trailing basis, it is entirely possible the next 18-24 months of earnings will cover the rest of equity capitalization. Translation: investors (or an acquiring enterprise) at $14 a share today could theoretically pocket future income, cash flow and dividends past 2024 for effectively "free" vs. net liquid assets.

The Business

The 2022 Annual Report explains the company's integrated operations best, alongside listing important changes to the business in 2021-22,

We operate six factories in the United Stated today – three in North Carolina, two in Virginia, and one in Alabama. Each serves a distinct portion of our product strategy created in conjunction with complementary product offerings that are manufactured in Mexico, Vietnam, India, or China in mind. We opened a new factory in NC in 2021 to manufacture our starting price point upholstery and we purchased an aluminum outdoor furniture manufacturing facility in Alabama in 2022. The vertical nature of our business is no more apparent than when considering the synergistic relationship between the merchandise footprint displayed in our stores with the factories that support it...

Our quick response manufacturing model has fueled domestic production to 78% of total output, enabling us to plough through our wholesale backlog much faster than our competitors. At year end, our wholesale backlog stood at $35.3 million compared to $90.0 million at the end of 2021. Still, the year-end backlog was more than double the $15 million of orders that we had in the house at the onset of the pandemic. With raw material procurement woes now largely behind us, we have returned to a normalized manufacturing environment where aligning demand, output, and staffing levels rule the day.

Last year began with the culmination of our ownership of Zenith Logistics, which dated back to the initial investment in 1998. Our retail network developed hand in hand with Zenith from the opening of the first Bassett store in 1997. Zenith provided the manpower and the strategic blueprint for distribution and logistics for our corporate and licensed stores from the beginning and still does today as part of JB Hunt. As warehousing and “middle mile” logistics in support of our industry has evolved, it became apparent that aligning with a much bigger player equipped with vast resources offered a clear path for us to competitively offer high levels of service in the years ahead. Accordingly, we completed the sale of Zenith to JB Hunt Transportation Services Inc. for $87 million on February 28th, 2022. We have a long-term service agreement in place upon which Zenith/JB Hunt has performed masterfully.

Company Website - Bassett Store Company Website - Store Experience Reviews, June 19th, 2023 Company Website - Living Room Furniture

{kind=link}

{kind=link}

{kind=link}

Bargain Valuation Story

When we review the valuation setup, it quickly becomes apparent Bassett is valued the same today as the lows of the 2008-09 Great Recession and 2020 pandemic panic which experienced a complete shutdown of its retail locations. In fact, one can argue the stock is by far the cheapest of peer and competitor furniture/retail business models in America.

When we look at the share price vs. basic underlying fundamentals, Bassett is trading at relative ratios less than HALF of 10-year averages on earnings, sales and book value. The cash flow multiple on an adjusted basis for one-time changes would be sitting closer to 5x. Including the sale of Zenith Logistics it stood around 2x.

YCharts - Bassett, Price to Basic Fundamental Results, 10 Years

A quick review of profit margins also highlights a business hitting on all cylinders during 2022-23. There is no legitimate operating excuse for the share price to be under pressure from a long-term perspective.

YCharts - Bassett, Various Profit Margins, 10 Years

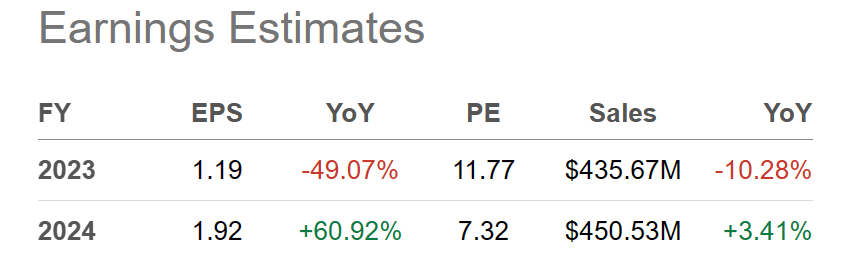

Analyst estimates for 2023-24 are calling for a normalization of business operations and sales after the wild pandemic demand and inventory fluctuations end. A P/E less than 12x for this year and slightly over 7x for 2024 are the consensus forecast.

Seeking Alpha Table - Bassett, Analyst Estimates for 2023-24, Made June 18th, 2023

{kind=link}

7x forward 1-year EPS is also the least expensive setup of the major furniture makers and sellers, pictured on the graph below. My peer/competitor sort list includes La-Z-Boy ( LZB ), Hooker Furnishings ( HOFT ), Flexsteel ( FLXS ), Ethan Allen ( ETD ), Tempur Sealy ( TPX ), Mohawk ( MHK ), and The Lovesac ( LOVE ). Essentially, Wall Street is expecting a slower retail environment in the second half of 2023 (mild recession), to be followed by better macroeconomic growth next year.

YCharts - Major Furniture Stocks, Price to Forward 1-Year Estimated Income, Since June 2022

What's a little mind-boggling to me is Bassett's ultra-low valuation is accompanied by a super-strong balance sheet with ZERO debt. In fact, cash held at the bank of $72 million in late February is approaching the total worth of its equity market capitalization near $125 million today.

YCharts - Bassett, Quarterly Financial Debt, Cash Holdings, Equity Market Cap, 10 Years

Putting all three financial ideas together, Bassett is left with an "enterprise value" of just $52 million vs. trailing annual cash EBITDA of $40 million. And, if all cash generation was funneled into a bank account (not reinvested in the business or paid as a dividend), I figure total cash may approach the current market capitalization by the end of 2024. In other words, if you could buy out the whole company at $14 per share, putting all cash in the bank now and coming from operations through early 2025 into your pocket, future earnings/cash flow generation after 18-24 months will be gravy and yours to keep as inflation and business results grow over time.

YCharts - Bassett, Enterprise Value vs. Annual EBITDA, 10 Years

What I am saying is the 1.3x EV to EBITDA number is crazy cheap, as is the 0.11x EV to sales ratio. Bassett is back to the depths of the COVID-19 panic valuation of March 2020, when the stock price was $4! For reference, at the March 2009 Great Recession low share price of $0.20 (adjusted for stock splits), EV to sales was 0.15x and EBITDA was a negative number.

YCharts - Bassett, Enterprise Value to EBITDA & Sales, 10 Years

Compared to furniture peers, EV to EBITDA is extremely low vs. a median average of 7x. Sure, this number includes the one-time gain from selling the Zenith unit. However, a normalized number for future projected operations is still in the 2x to 3x range.

YCharts - Major Furniture Stocks, Enterprise Value to EBITDA, Since June 2022

Even less expensive vs. peers is the EV to revenue number. At 0.11x, Bassett is trading well below the peer median average around 0.4x.

YCharts - Major Furniture Stocks, Enterprise Value to Revenues, Since June 2022

Lastly, Bassett paid a nice dividend yield of 4.5% over the last year at $14 a share. You can see on the graph below, this upfront cash return for owners handily beat the main SPDR S&P 500 Trust ETF ( SPY ), iShares Russell 2000 ETF ( IWM ), SPDR Retail Sector ETF ( XRT ), and iShares Long-Term Treasury Bond ETF ( TLT ) rates by a wide margin. Good news is the dividend yield is projected to be easily covered by earnings during 2023-24 at a level of 35% to 50% of after-tax income.

YCharts - Bassett Dividend vs. Yield Alternatives, 5 Years

Final Thoughts

For sure, the biggest risk investing in Bassett right now would be a serious recession creating a big drop in demand for furniture. While the odds of such an event are much higher than normal, I believe the stock price slide from $23 last summer is already discounting most of the damage of a prolonged downturn. Remember, the enterprise value has fallen from nearly $300 million last July to $50 million currently.

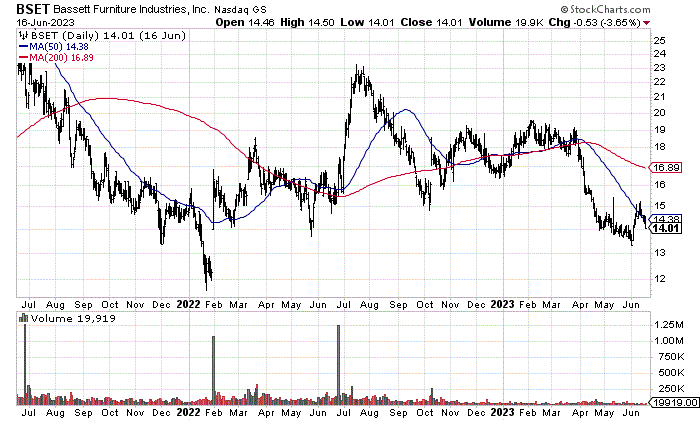

I really question how much lower the share price can trade, absent a stock market crash generally on Wall Street. On the 2-year chart of daily price and volume trading below, the $11.50 to $12 price zone bottom in January 2022 should hold, meaning downside risk may be limited to -15% to -20% from $14.

StockCharts.com - Bassett, 2 Years of Daily Price & Volume Changes

{kind=link}

On the other side of the risk/reward equation, upside is rather unlimited over the long term. Over the short run, CSC Generation Holdings made an all-cash takeover bid of $21 in October , which was rejected by management as too low. New bids could appear into the end of 2023 by this enterprise or another, especially with Bassett's valuation remaining incredibly low.

Otherwise, I am targeting a fair value range of $25 to $30 per share in 12 months, assuming a deep recession is avoided. This zone would represent a closer fit to long-term averages of price to earnings, sales, cash flow and book value.

All told, trading just above cash holdings is quite illogical. Management could easily announce a huge share buyback plan to repurchase 25% to 50% of outstanding ownership interests, using cash already at the bank to finance the idea. If I were running the business, a decent increase in the dividend payout combined with a major stock repurchase effort might get price back above $20 permanently over the next six months.

I rate shares a Strong Buy . Against potential total return downside of -20% as a worst-case scenario ($11 a share plus dividends), 12-month upside projections of +45% ($20 per share) to +110% ($30 per share) are worth serious consideration for your portfolio.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Bassett Furniture: Future Operating Income Available Almost For Free, No Really