BSET - Bassett Furniture Industries: Declining Financial Performance With More Pain Ahead

2024-01-02 22:30:41 ET

Summary

- Bassett Furniture Industries' revenue growth has been underwhelming and is coupled with volatility, as the company has struggled to consistently gain market share.

- Additionally, the company has seen limited margin development, with the recent macro developments contributing to a loss-making quarter.

- The macroeconomic environment is impacting retail spending and home purchases, both of which we expect to restrict BSET’s ability to generate alpha in 2024.

- BSET’s relative performance to its peers is highly disappointing, implying superior options for investors seeking exposure to this industry long term.

- BSET’s valuation does not adequately reflect the pressures ahead and underperformance against its peers.

Investment thesis

Our current investment thesis is:

- BSET does not appear to be an attractive company in our view. Its business model lacks unique qualities, its financial performance lacks consistency and development, and 2024 will likely be an incredibly difficult year. To invest now, we would need to see long-term qualities that help justify “getting in early.” We do not see anything.

- We expect the company to struggle in 2024 and likely reach a revenue “bottom” in Q2-Q3, although Q4 will likely be its worst quarter given it was loss-making.

- Even if we consider its pre-pandemic performance, the company does not stand out relative to its peers’ performance currently. Given the heavy macroeconomic headwinds impacting the industry, this is a damning indictment.

Company description

Bassett Furniture Industries, Incorporated ( BSET ) is a renowned American manufacturer and retailer of home furnishings. With a history dating back over 100 years, Bassett is known for its commitment to craftsmanship, quality, and customization in furniture design. The company operates a network of retail stores and licensed partnerships, providing a wide range of products to enhance home interiors.

Share price

BSET’s share price performance has been disappointing, significantly underperforming the wider market. This said, it has experienced periods of acceleration, linked to its financial performance, although Management has been unable to sustain periods of impressive expansion.

Financial analysis

{kind=link}

Presented above are BSET's financial results.

Revenue & Commercial Factors

BSET’s revenue has grown at a CAGR of +3% during the last decade, although this does not tell the story adequately. Even prior to the pandemic, the company has faced extreme volatility, unable to consistently generate gains.

Business Model

BSET has a diverse portfolio of furniture, including living room, bedroom, dining room, and home office furniture. The company allows customers to customize its furniture, allowing for tailored pieces to their preferences. This includes choosing fabrics, finishes, and other design elements.

BSET operates through a network of retail stores, galleries, and licensed partnerships. This omni-channel approach provides customers with various touchpoints to explore and purchase furniture, enhancing accessibility. This is critical in the furniture industry where consumers still have a preference to see before they buy (vs. e-commerce), although appreciating the trend is changing.

In addition to brick-and-mortar stores, Bassett engages in direct-to-consumer sales through its website. This e-commerce channel allows customers to browse products, place orders, and receive deliveries.

The company is known for its focus on quality craftsmanship and considers this a primary competitive advantage, maintaining production facilities in the US and marketing this fact. This has historically been an important fact but with globalization and access to lower-cost products, BSET’s advantage from this is waning.

In conjunction with this focus on quality, the company’s other competitive advantages revolve around its reach (storefronts) and brand. The issue is that we see these factors as being less important in the internet generation and do not sufficiently generate differentiation. Consumers can purchase products from a number of online retailers, test them, and return them if required. Further, traditional retailers can create similar products and so design and price differentiation are limited. Finally, for larger products, consumers still have a range of brick-and-mortar retailers they can compare.

We believe these factors have restricted BSET’s ability to consistently develop its margins and growth. It is not differentiated enough and lacks the ability to be so.

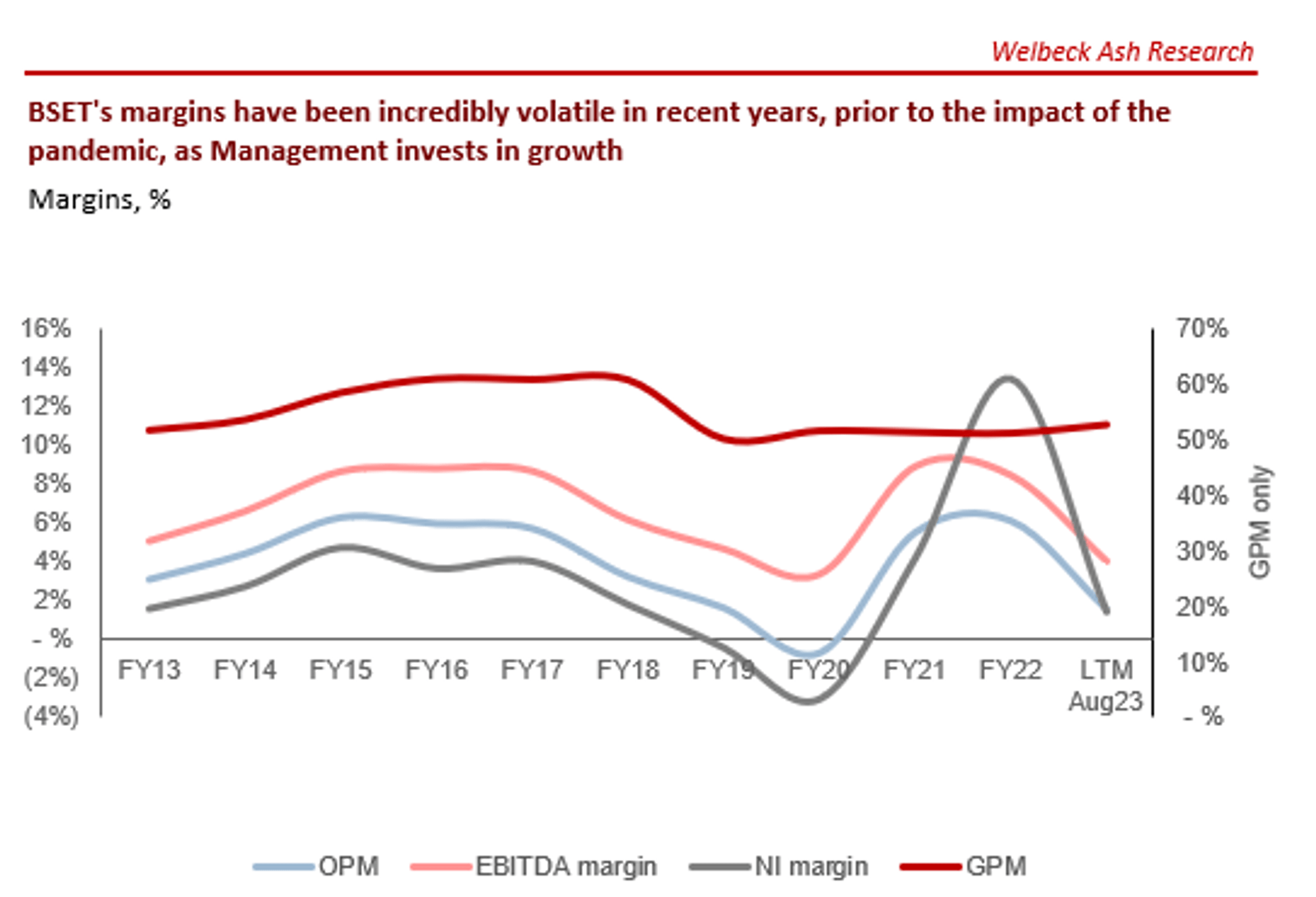

Margins

{kind=link}

BSET has observed limited margin progress during the last decade, with its EBITDA-M hovering between 7-9%. This is partially due to the limited growth in scale achieved, as well as competitive pressures. The company’s GM% has struggled to consistently improve and is well below its peak levels, while S&A spending as a % of revenue is not benefiting from economies of scale.

With changing industry dynamics in favor of online retailers, such as Wayfair (W), as well as a shift toward lower-cost production in the Far East contributing to downward pressure on price, we struggle to see how BSET can achieve margin improvement. It faces pressures on price (GM%) and on generating demand through investment in marketing (S&A).

Quarterly results

BSET’s recent performance has been highly disappointing, but not surprising, with top-line revenue growth of +12.5%, +5.8%, (8.6)%, and (26.1)%. In conjunction with this, its margins have continued to step down, with the company’s EBITDA-M negative in Q3.

The company’s declining fortunes are almost wholly attributable to the current macroeconomic environment. Consumers are grappling with a cost of living crisis that has continually compounded as rates and inflation eat away at finances. This has discouraged discretionary and non-core purchases, impacting the demand for furniture. As the following illustrates, both consumer affordability and sentiment sit at 5Y record lows / near record lows.

Compounding this dissuasion is the nuance associated with the impact of home purchases on furniture demand, as the two are directly linked. With rates at levels unseen in over a decade, the US housing market has ground to a halt, with consumers waiting out this period of elevated rates or unable to afford a new home. This is evidenced in the below data sets. New housing starts remaining flat despite a US housing shortage, pending home sales are down, and US home prices remain flat.

The only positive here is that despite the cost of living crisis, consumers are able to hold onto their properties, as evidenced by the relative stickiness of prices. This is why we believe many are “waiting it out.” This bodes well for the medium-term revival of the industry.

Looking more broadly once again, many are predicting a recession in 2024 (US recession probability indicator has exceeded 50%), to the extent that discussions are now around the depth of such. This will only act to compound the negative impact on sales. Despite the negative factors we have discussed above, US consumer sales remain positive. Should this reverse into negativity, we could see a greater decline in 2024.

Key takeaways from its most recent quarter are:

- The decline in sales is primarily driven by the wholesale segment, as retailers continue to be cautious, although a similar decline is observed in its Retail segment.

- Inventory levels remain elevated while Management continues to write down stock and markdown products. Inventory turnover remains below its 5-year average of 3.1x (2.5x).

- BSET’s domestic upholstery team is a small shining light that was able to increase margins while dealing with a 31% decline in shipments. This will be important for growing margins as demand improves.

- Over the coming quarter, BSET will seek to open two new stores and re-open an existing location that was being remodeled. Further, the company recently relaunched its website after an extended period of development, noting an improvement in traffic and conversion.

Balance sheet & Cash Flows

BSET is conservatively financed, with an ND/EBITDA ratio of 1x. The company has recently disposed of a business, shoring up its cash position. Given the negative margins in the recent quarter and the bleak near-term ahead, we are supportive of this decision.

{kind=link}

Outlook

We expect BSET to materially struggle in the coming year, with a decline in sales of 15-25%, although this estimate will be a moving target as macroeconomic conditions develop. This will negatively impact margins, although to a far lesser extent given the pain felt in 2023. Wholesale demand will need to stabilize by virtue of stock requirements. We suspect a mid-single-digit EBITDA-M and breakeven, to negative, FCF. In our base case, BSET will experience a genuine improvement from Q4 onward, appreciating that a lower comparable will likely create the perception of an improving Q2-Q3.

Industry analysis

Home Furnishing (Seeking Alpha)

{kind=link}

Presented above is a comparison of BSET's growth and profitability to the average of its industry, as defined by Seeking Alpha (10 companies).

When compared to its home furnishing peers, BSET materially underperforms. The company has grown at a lower level and is forecast to continue this, while its margins are comfortably below the average. Even if we consider the company at its FY17-FY19 levels, it is still underwhelming.

This is a reflection of an underwhelming business model in our view, limiting the company’s ability to financially outperform its peers. Not only this, but BSET is clearly more greatly exposed to market conditions, suggesting its peers are doing better to mitigate conditions.

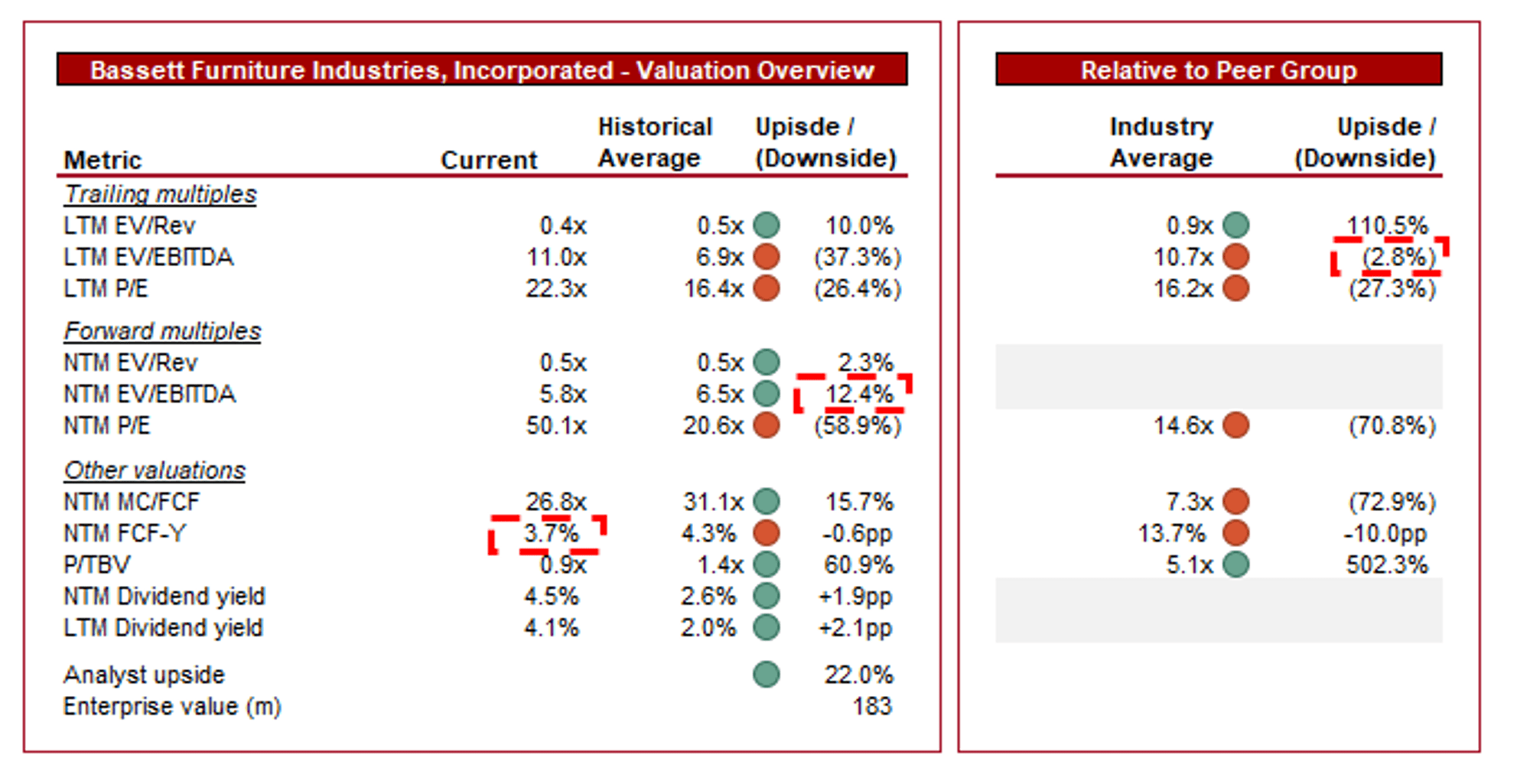

Valuation

{kind=link}

BSET is currently trading at 11x LTM EBITDA and 6x NTM EBITDA. This is a discount to its historical average on a NTM basis.

BSET’s uncomfortable position is illustrated by its inconsistent valuation, with a premium on an LTM basis but a discount on an NTM basis. The premium on an LTM basis is undeniably unwarranted.

Investors are uncertain as to how BSET will develop, thus assigning a forward discount. We are supportive of a discount, particularly as we are not wholly convinced BSET can achieve a ~$30m EBITDA. Given the discount is only 12% on a valuation we are unconvinced by, we believe this indicator suggests the company is overvalued.

Further, BSET is trading at a premium to its peers, while facing a coming year of relative underperformance. Given the comparison discussed above, this further suggests downside risk in our view.

Valuation evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- “Soft landing” economically, restricting a decline in demand.

- Earlier than expected reduction in interest rates.

- Market share growth during this period of difficultly (although acknowledging we do not see any specific strategic action that will achieve this).

- E-commerce market growth.

Final thoughts

BSET is not an overly attractive business in our view. The company’s financial performance has been mediocre, its business model is uninspiring, and its performance relative to its peers is disappointing.

The US is facing a shortage of homes and so BSET is not facing obsolescence, but we do think there are likely many better alternative options.

Given the pain ahead in 2024 and the inconclusive valuation, we rate this stock a sell.

For further details see:

Bassett Furniture Industries: Declining Financial Performance With More Pain Ahead