ETD - Bassett Furniture Industries: Expect Outperformance To Continue

Summary

- Bassett Furniture Companies continues to fare well in the current environment, even though profits and cash flows have been mixed.

- Some pain could very well lie ahead for investors, but this may actually make it a prime time to consider buying stock in the firm.

- After all, shares look attractive at this moment and are still affordable even if financials worsen.

One lesson that I've learned as an investor is that some of the most boring companies can be some of the most rewarding. One great example that I can point to in this regard is a firm called Bassett Furniture Industries ( BSET ). As its name suggests, the company operates as a producer and seller of furniture and other related products. And it is a company that I previously rated a ‘buy’ only to see shares increase nicely compared to what the broader market has experienced. To be clear, this increase in price was not driven solely by fundamental data. That has actually been rather mixed as of late. Rather, the key driver seems to have been just how cheap shares were and the fact that fundamentals have not materially worsened across the board during these uncertain economic times. What's also exciting is that shares of the company still look cheap, even taking in certain assumptions regarding the near-term outlook for the firm. Because of this, I've decided to keep the ‘buy’ rating I had assigned to the stock previously, reflecting my belief that shares should continue to outperform the market moving forward.

Mixed results have been rewarded

Before we get into the newest investment data for the company, a bit of a rehash of my original argument is in order. In an article published in January of 2022, I called Bassett Furniture Industries a decent company that was trading at a great price. At that time, the company had been impacted by concerns over its long-term stability. But recent financial performance had been positive and shares were looking almost too cheap to pass up. This led me to the ‘buy’ rating that I assigned the business. Ultimately, this rating was rewarded. While the S&P 500 is down 12.1% since the publication of that article, shares of Bassett Furniture Industries have generated upside for investors of 21.7%.

{kind=link}

Author - SEC EDGAR Data

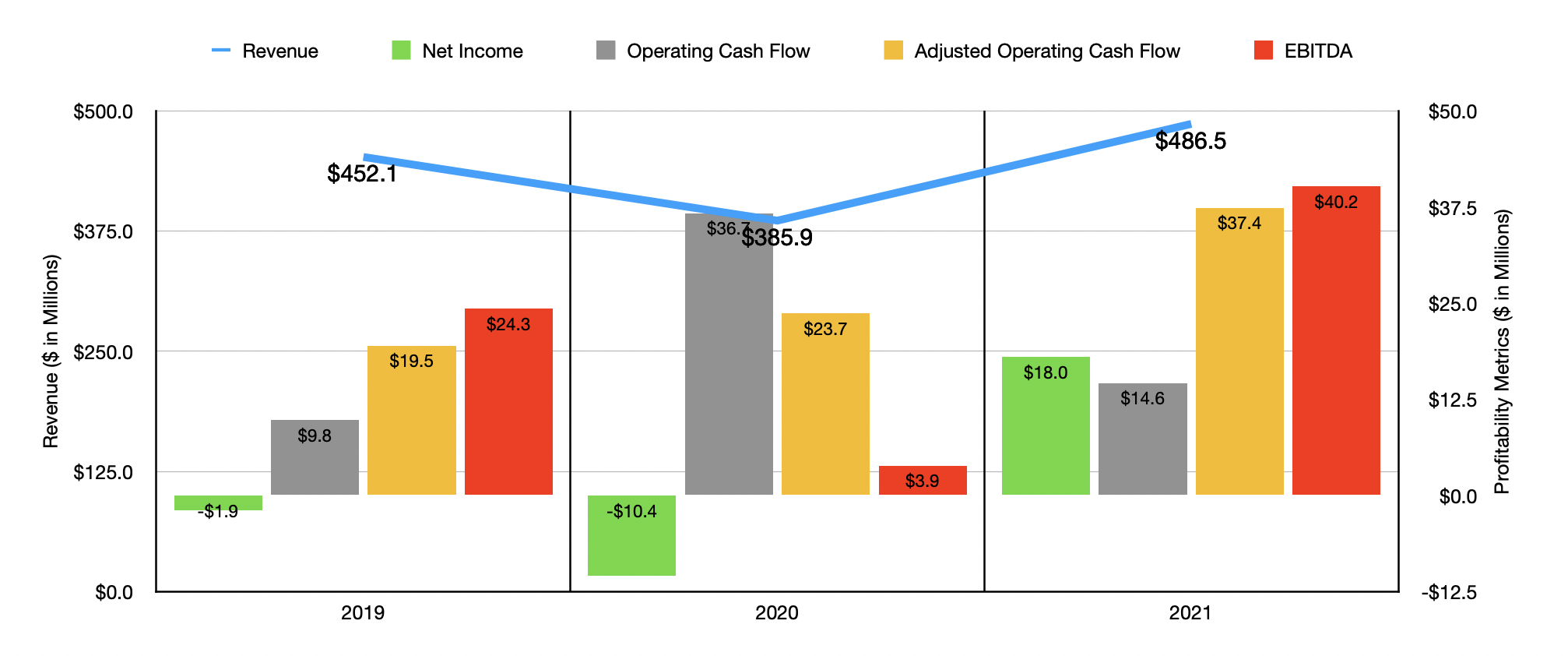

To start with, I would like to review data from the 2021 fiscal year for the firm. At the time that I last wrote about it, we only had data through the third quarter. For the year as a whole, revenue totaled $486.5 million. That's 26.1% higher than the $385.9 million generated in 2020 and compared to the $452.1 million seen in 2019. Growth in 2021 was across the board. And dollar terms, the largest increase came from the company's wholesale operations, with revenue shooting up from $221.1 million to $295.3 million. According to management, this 33.6% rise was driven largely by the recovery following the COVID-19 pandemic that had negatively impacted sales in 2020. On the retail side, sales expanded from $211.9 million to $247.8 million. This was a 16.9% increase and, according to management, it stemmed from the fact that, in 2020, the company's retail operations were shattered from late March through early May.

On the bottom line, the picture for the company also improved. The firm went from generating a net loss of $10.4 million in 2020 to generating a profit of $18 million in 2021. Operating cash flow actually declined, dropping from $36.7 million to $14.6 million. But if we adjust for changes in working capital, it would have risen from $23.7 million to $37.4 million. And over that same window of time, EBITDA for the company increased from $3.9 million to $40.2 million.

{kind=link}

Author - SEC EDGAR Data

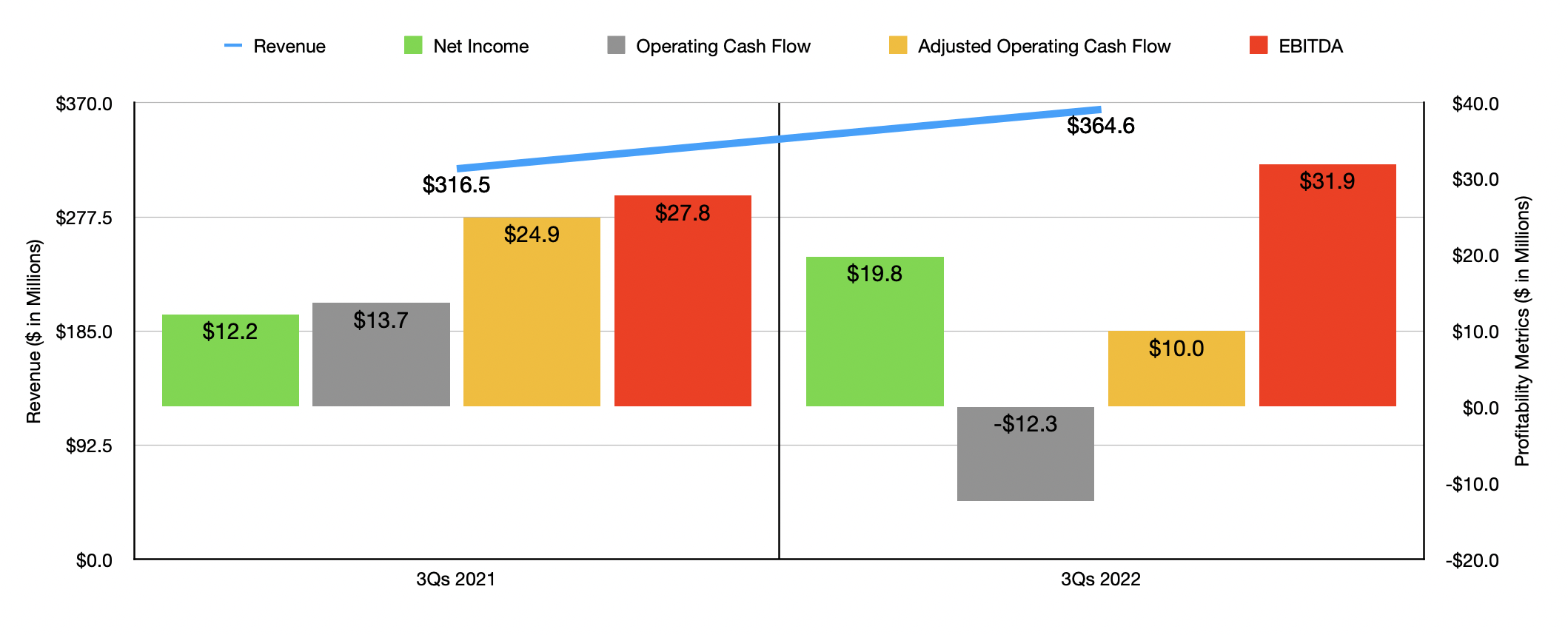

Growth for the company continued into the 2022 fiscal year. In the first three quarters of that year , sales totaled $364.6 million. That represents an increase of 15.2% over the $316.5 million reported the same time one year earlier. This increase came at a time when management sold, in the first quarter of 2022, its Zenith Freight Lines assets to J.B. Hunt Transport Services in a deal valued at $86.9 million. Under the wholesale side of the firm, revenue jumped by 14% for the year, driven largely by increases in shipments of 13% to its BHF store network and a 12% increase in shipments to the open market. And on the retail side, revenue expanded by 16%. Perhaps more important than revenue right now is backlog. According to management, wholesale backlog in the latest quarter was $41.6 million. That's down from the $92.8 million reported one year earlier. Retail backlog, meanwhile, totaled $60 million, down from $73.5 million one year earlier. Although this is bad to see and indicates some weakness ahead, it is worth mentioning that these numbers are more in alignment with what backlog looked like prior to the pandemic. This suggests that business is returning to normal for the firm.

On the bottom line, the picture of the company has been a bit mixed. On the good side, net income from continuing operations for the company totaled $19.8 million in the first nine months of its 2022 fiscal year. This is compared to the $12.2 million reported one year earlier. On the other hand, operating cash flow fell from $13.7 million to negative $12.3 million, while the adjusted figure, which ignores changes in working capital, dropped from $24.9 million to $10 million. Other than net income, the only profitability metric that improved year over year was EBITDA. Based on the data provided, it increased modestly from $27.8 million to $31.9 million.

{kind=link}

Author - SEC EDGAR Data

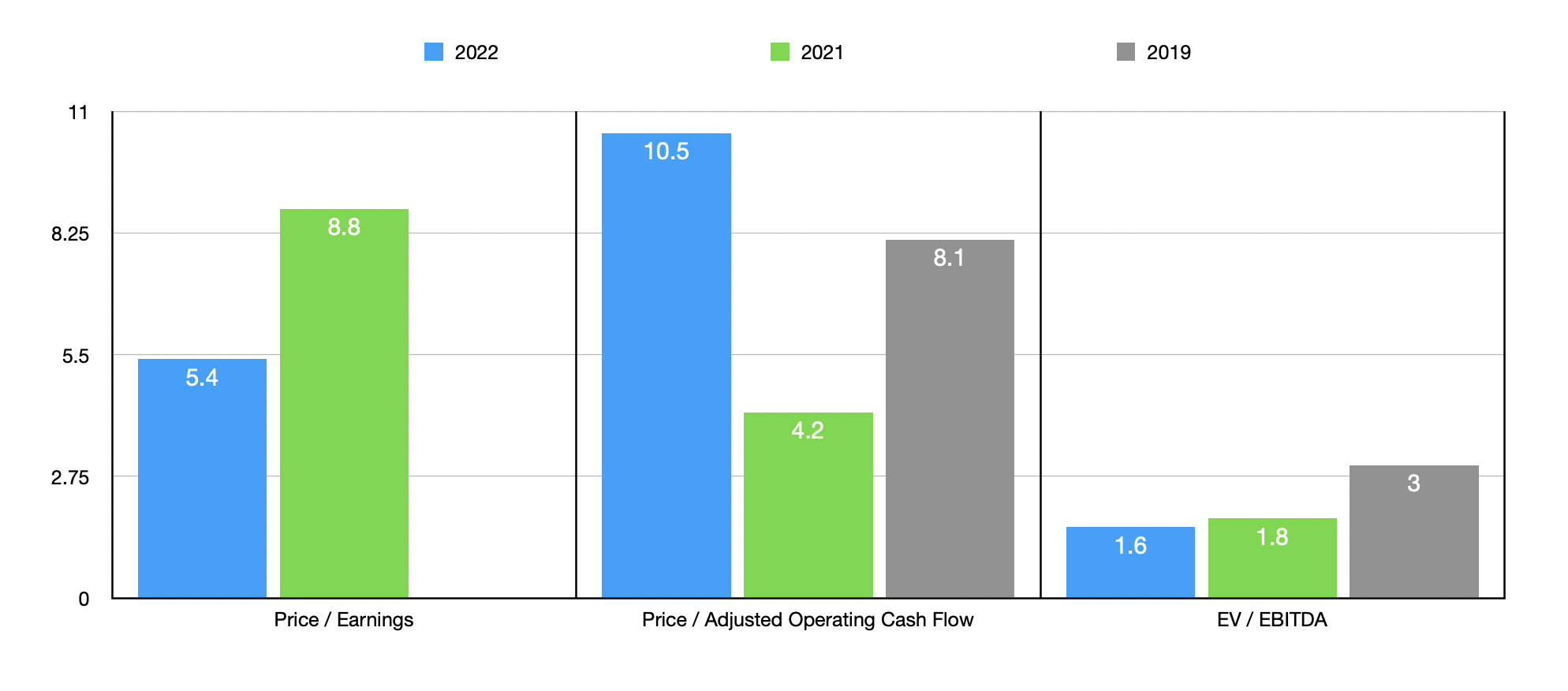

We don't really know what to expect when it comes to the 2022 fiscal year in its entirety. But if we simply annualize results experienced so far for the year, we would anticipate net income of $29.2 million, adjusted operating cash flow of $15 million, and EBITDA of $46.1 million. As you can see in the chart above, this makes shares quite cheap on an absolute basis. In two of the three cases, shares are actually cheaper than what we would get if we used data from 2021. But of course, as I mentioned already, we are not dealing with normal economic conditions. The significant decline in backlog experienced year over year suggests that some additional pain could lie ahead. But even if we were to assume that financial performance were to revert back to what it was in 2019, shares would still be cheap relative to cash flow and EBITDA. As part of my analysis, I also compared the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 6.2 to a high of 12.7. And when it comes to the EV to EBITDA approach, the range was from 2.3 to 10.5. In both cases, was the cheapest of the group. Meanwhile, using the price to operating cash flow approach, the range was from 7.8 to 23. In this scenario, only two of the five companies was cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Bassett Furniture Industries |

| 5.4 |

| 10.5 |

| 1.6 |

| Ethan Allen Interiors ( ETD ) |

| 6.3 |

| 7.8 |

| 3.3 |

| Tempur Sealy International ( TPX ) |

| 12.6 |

| 16.2 |

| 9.5 |

| La-Z-Boy Inc. ( LZB ) |

| 6.2 |

| 11.2 |

| 2.3 |

| The Lovesac Company ( LOVE ) |

| 12.7 |

| 23.0 |

| 10.5 |

| Mohawk Industries ( MHK ) |

| 7.7 |

| 4.3 |

| 5.3 |

Takeaway

I stand by my original claim that Bassett Furniture Industries is more or less a mediocre company. There is nothing exceptional about it in any way and I wouldn't be surprised if it faces some pain as a result of changing economic conditions. In some ways, the company has already demonstrated that pain in the form of reduced cash flow. But given the fact that the company has cash in excess of debt totaling $84.6 million and is trading at a low valuation, I believe that a ‘buy’ rating is still appropriate at this time. Although not all that relevant anymore, it should also be mentioned that, in October of last year, management turned down a buyout offer of $21 per share. That would be 21% higher than where shares are currently trading. Given the amount of time that has lapsed, I believe that the probability of another suitor or the same suitor coming back to the table is quite small. But that could also be an added catalyst for shareholders to consider.

For further details see:

Bassett Furniture Industries: Expect Outperformance To Continue