BSET - Bassett Furniture Industries: Not A Great Play Just Yet

2023-09-01 16:14:58 ET

Summary

- Bassett Furniture Industries has experienced weak revenue, profits, and cash flows so far this year.

- The company has no debt and a significant amount of cash on its books, providing some stability.

- Recent industry data suggests that the pain for Bassett Furniture Industries and similar companies may persist in the near term.

- But once the industry shows signs of improvement again, it could make for a solid prospect.

One of the things that makes investing difficult is the fact that circumstances can change. Sometimes, those changes can occur rather rapidly. And when they do, a good picture can become a bad picture and a bad picture can become a good one. One example of a company that has seen some weakness now that I did not expect to see when I last wrote about it in January of this year is Bassett Furniture Industries ( BSET ). Revenue, profits, and cash flows have all been weak so far this year. The good news is that the company has no debt, and it enjoys a significant amount of cash on its books. Overall inventory data looks positive, but recent industry data suggests that pain for this prospect and others like it could persist in the near term. Given this recent performance, and in spite of the fact that shares have fallen significantly over the past few months, I would argue that the company still makes for a 'hold' prospect at this time. However, in the event that industry data starts showing signs of recovery, my assessment of the company could improve rather quickly.

A painful year so far

Back when I wrote about Bassett Furniture Industries in January of this year, I lauded the company for how well it was performing in what was then the current environment. Even then, I mentioned that there could be some pain ahead for shareholders. But given the overall health of the enterprise, I stated that the company made for a better 'hold' prospect than a 'buy'. Since then, the stock has taken a beating, dropping 10.7% at a time when the S&P 500 has jumped 15.5%.

{kind=link}

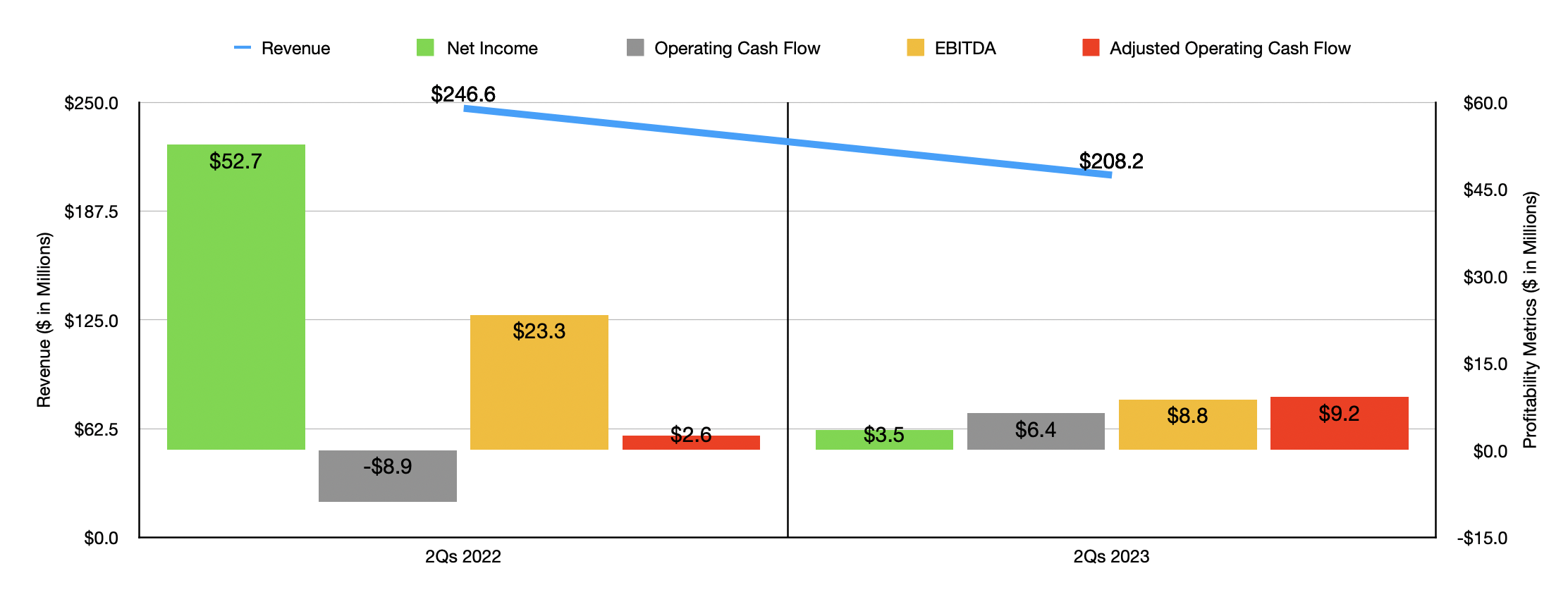

Sometimes in the market, disparities of this magnitude are unwarranted. But this is not one of those cases. The fact of the matter is that Bassett Furniture Industries did experience enough pain on both its top and bottom lines to justify an unpleasant market reaction. Consider how the firm performed during the first half of the 2023 fiscal year . Revenue for that time came in at $208.2 million. That's a 15.6% drop compared to the $246.6 million in revenue generated the same time last year.

This drop in revenue occurred across both of the company's primary operating lines. Retail sales, for instance, dropped from $139.7 million to $125.7 million on a year-over-year basis. Most of this pain came from a 14.8% plunge under the Bassett Custom Upholstery product category of the company. Truth be told, management does not provide a great deal of insight into why this drop occurred. All they mentioned was that written sales decreased year over year, though the fact that backlog for this unit dropped from $71.1 million at the end of the second quarter of last year to $32.9 million for the same time this year shows that demand is weak. Part of what is driving this is almost certainly the decrease in store count that the company has. At the present moment, Bassett Furniture Industries has 91 stores in operation, with 58 of those being company-owned and 33 as independent operations. That compares to the 97 locations one year earlier, with 63 as company-owned and 34 as independent. It is hard to grow sales or keep sales flat when the number of stores that you have drops.

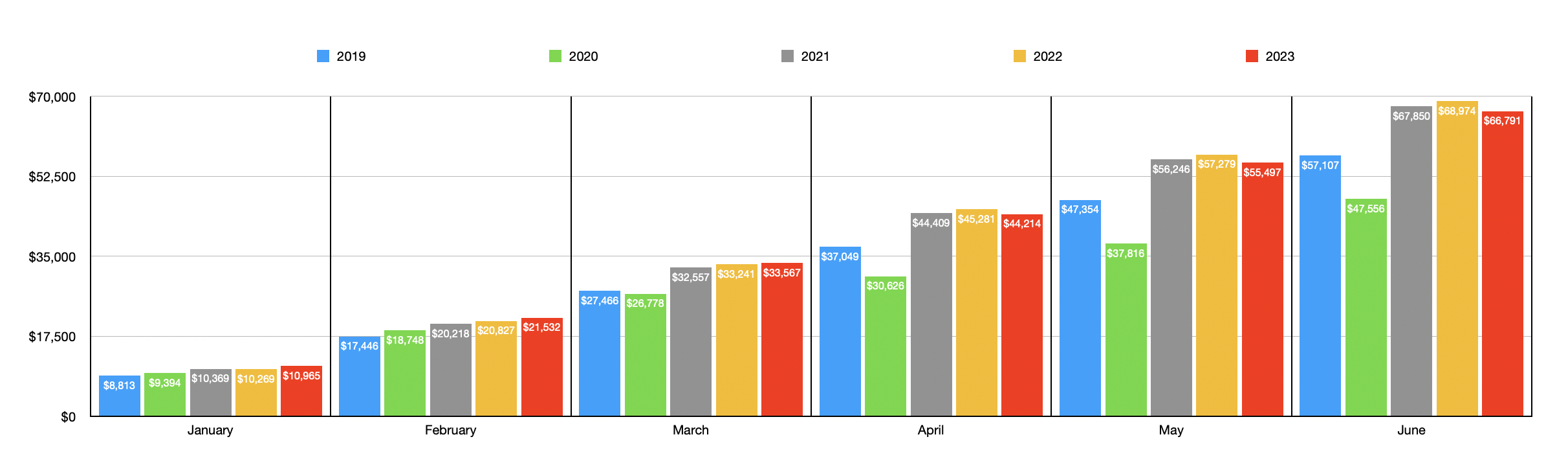

There is also, of course, the wholesale side of things. Revenue under this unit dropped from $109.2 million last year to $83.9 million this year. That 23% drop was driven by a 29% decline in shipments to the open market and a 17% drop in shipments to the company's own retail store network. Lane Venture shipments also declined, dropping 19% year over year. This is where it might be helpful to dig into some of the economic data regarding furniture sales. According to one source , for the first seven months of this year, overall furniture stores in the retail sector are down 3.8% year over year. That took revenue for the space down to $77.5 billion. In the month of June, sales of $11.3 billion translated to a 3.4% drop year over year compared to the $11.7 billion reported in June 2022. In fact, as the chart below illustrates, cumulative sales for the first six months are lower this year than they were in each of the past two years. And sales estimates for July showed a drop of 4.1% year over year, with revenue dropping from $11.8 billion to $11.3 billion. This covers only the retail side of things, but it's important to understand the role that the wholesale market plays in the retail side.

{kind=link}

On the bottom line, the picture has been even worse. During the first half of the year, net profits totaled $3.5 million. That is a massive drop from the $52.7 million the company reported one year earlier. Although Bassett Furniture Industries enjoyed a 2.8% increase in its gross profit margin for this window of time, driven largely by higher margins under the wholesale segment and a greater portion of total sales for the company coming from its owned retail stores, these improvements were offset by higher costs elsewhere. Namely, management oversaw a 7.9% rise in selling, general, and administrative costs in relation to sales. A deleverage of fixed costs resulting from lower sales volume, as well as a greater portion of the company's revenue coming from its owned stores, ended up hitting this cost item rather considerably. Truth be told, had the explanation been something different, such as management voluntarily stepping up advertising spending in order to lure customers in during times of weakness, I would have been much more bullish. But that was, unfortunately, not the case.

{kind=link}

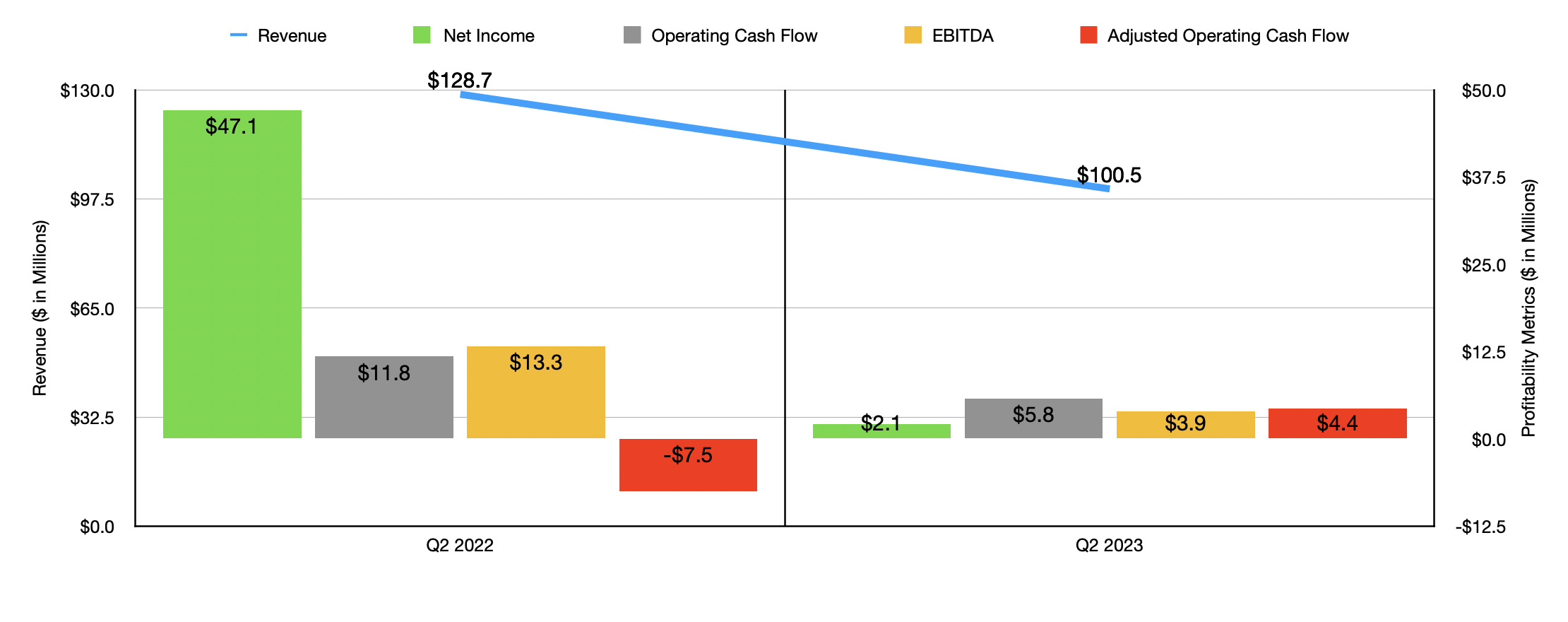

While net profits dropped year over year, other profitability metrics were rather mixed. Operating cash flow, for starters, went from negative $8.9 million to positive $6.4 million. Even if we adjust for changes in working capital, we would see the metric jump from $2.6 million to $9.2 million. On the other hand, EBITDA for the company declined from $23.3 billion to $8.8 billion. Before we move on, I would like to point out that, in the chart above, I provided financial results for the company for just the most recent quarter on its own. The overall trend here is virtually the same, with the exception of operating cash flow, which managed to drop year over year in the second quarter. The sales decline, totaling 21.9%, suggests that the picture is worsening at an accelerating rate.

Given the tremendous changes that we have seen from year to year when it comes to profits and cash flows, we cannot really value the company from a profitability perspective. However, we do have the fact that the firm has a fantastic balance sheet. As I mentioned previously, it has no debt on its books. It also enjoys cash and cash equivalents of $73.3 million. With a market capitalization of $134.9 million, this brings the company's enterprise value down to only $61.5 million. It does not take a lot of profit to justify that kind of valuation. On top of this, the firm is trading at 69.8% of its book value and at 78.6% of its tangible book value. That also provides a great deal of safety.

{kind=link}

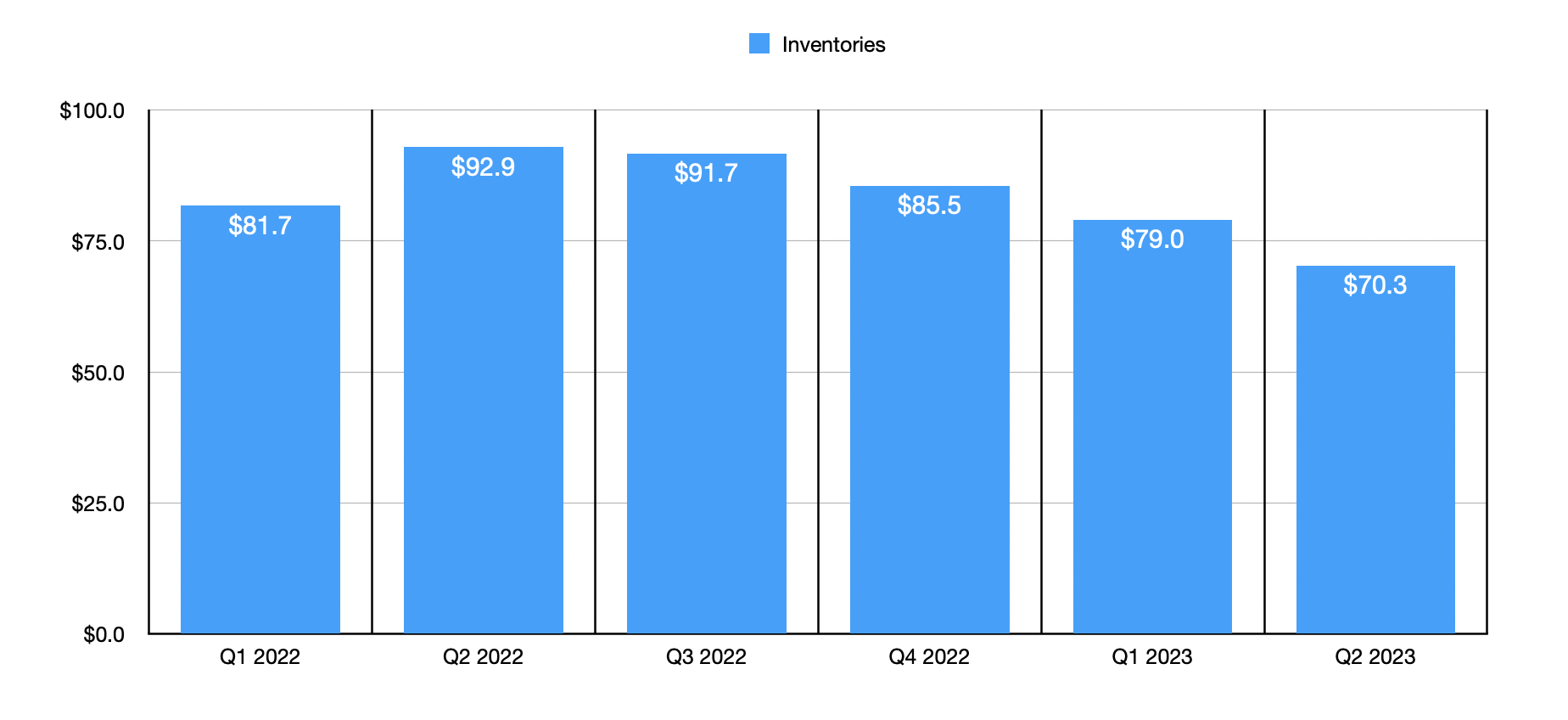

One other thing that I would like to discuss briefly involves inventory levels. Investors would be wise to pay special attention to inventories. After all, it wasn't too long ago that many industries faced bloated inventories. The good news for shareholders of Bassett Furniture Industries is that inventory levels have been dropping over the past several quarters. In the first quarter of 2022, for instance, inventories for the company totaled $81.7 million. This metric then popped up to a high of $92.9 million in the second quarter of last year. Fast-forward to the end of the second quarter of this year, and inventories are down to only $70.3 million. The company will need to keep inventories down because of weak industry conditions. And at some point, when the market does turn, they will have to reverse course. But it is nice to know that they are not sitting on a significant amount of inventory that they might have to take a haircut on in the near term.

Takeaway

Truth be told, I struggle with Bassett Furniture Industries to some extent. I want to be bullish about the company because of its balance sheet, how cheap the company is, and some other factors. But I also see some problems with it, such as recent financial weakness, declining backlog, and the fact that management is closing stores. I think that if we start to see some recovery in the furniture industry itself, that could tip the company in the direction of being an attractive prospect. But until that time occurs, I would say that a more cautious approach is warranted.

For further details see:

Bassett Furniture Industries: Not A Great Play Just Yet