BHC - Bausch Health: $20bn Debt Is A Mighty Elephant In The Room

2023-11-30 05:33:24 ET

Summary

- Bausch Health has a solid business model with steady revenue generation and strong operating income margins - but debt & litigation are crippling the business.

- The company's heavy debt of >$20bn, and pending litigation around lead product Xifaxan pose significant challenges for its future success.

- Bausch's stock has gained slightly since last year, but the day of reckoning may be approaching due to its aggressive past business development strategy and high levels of debt.

Bausch Health Overview: A Solid Business Model - If You Ignore Debt & Litigation

At the end of 2022, when I last covered Bausch Health (BHC) in a post for Seeking Alpha , I gave the company's stock a "Hold" rating, despite my misgivings about heavy net losses, lack of top line revenue growth, litigation issues, and a massive debt pile which stood at >$20bn.

The compensation for all of these issues was a low share price and valuation - in May 2022, after the Laval, Canada based business shared a weak set of Q1 earnings immediately after spinning out its eye-care business into Bausch + Lomb, the company's share price tumbled from ~$23 per share, to ~$7 per share, and it has not recovered since. As such, since my last note, Bausch stock has risen in value by just 12%, versus the S&P 500's 19% gain over the same period.

In its latest quarterly report / 10-Q submission , Bausch describes its business as follows:

We are a global, diversified specialty pharmaceutical and medical device company that develops, manufactures and markets, primarily in the therapeutic areas of gastroenterology ("GI"), hepatology, neurology and dermatology, a broad range of branded, generic and branded generic pharmaceuticals, over-the-counter ("OTC") products and aesthetic medical devices, and, through our approximately 89% ownership of Bausch + Lomb Corporation ("Bausch + Lomb" or "B+L"), branded, and branded generic pharmaceuticals, OTC products and medical devices (contact lenses, intraocular lenses, ophthalmic surgical equipment) in the therapeutic areas of eye health. Our products are marketed directly or indirectly in approximately 100 countries.

Bausch's problems were primarily caused during the period between 2013 - 2015, when the company, then called Valeant Pharmaceuticals, attempted to grow via a strategy of acquiring pharmaceutical companies and hiking the prices of their drugs ( I shared more detail in a post for seeking Alpha published in August 2022 ). Valeant stock achieved a share price high of $250, before cracks in the business model were exposed, government investigations began, and the share price lost >90% of its value in less than one year.

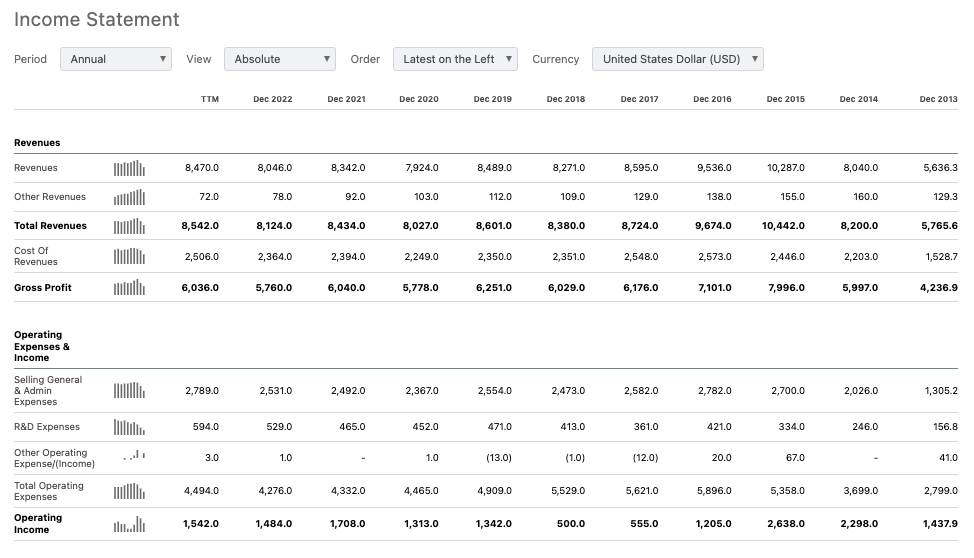

Despite the disastrous share price losses, and massive debt pile - total liabilities stood at $43bn in 2015, with >$30bn of long term debt, and a deferred tax liability of ~$6bn - Bausch has been able to keep its top line revenue generation relatively steady, and even grow its operating profits for the past several years, as shown below:

{kind=link}

It's rare to find a company generating >$8bn revenues per annum that is trading at a market cap valuation of ~$2.6bn, or a historical price to sales ("P/S") ratio of ~0.3x, or <2x operating income, unless the company is distressed in some way, and if we consider Bausch's recent net income, we can certainly identify a major problem.

{kind=link}

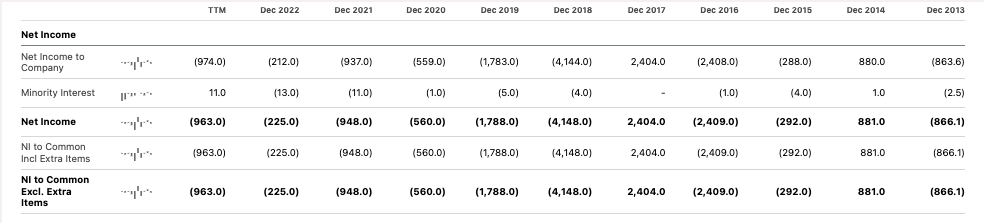

Since 2018, Bausch has racked up net losses of nearly $8bn, and net loss across the first nine months of 2023 was reported as $(564m), on $6.28bn of product sales - up 7% year-on-year. Had it not been for interest expense of $(965m), and a goodwill impairment charge of $(402m), Bausch may have returned a small profit, as was the case across the same period last year, although this was primarily due to a $683m "gain on extinguishment of debt".

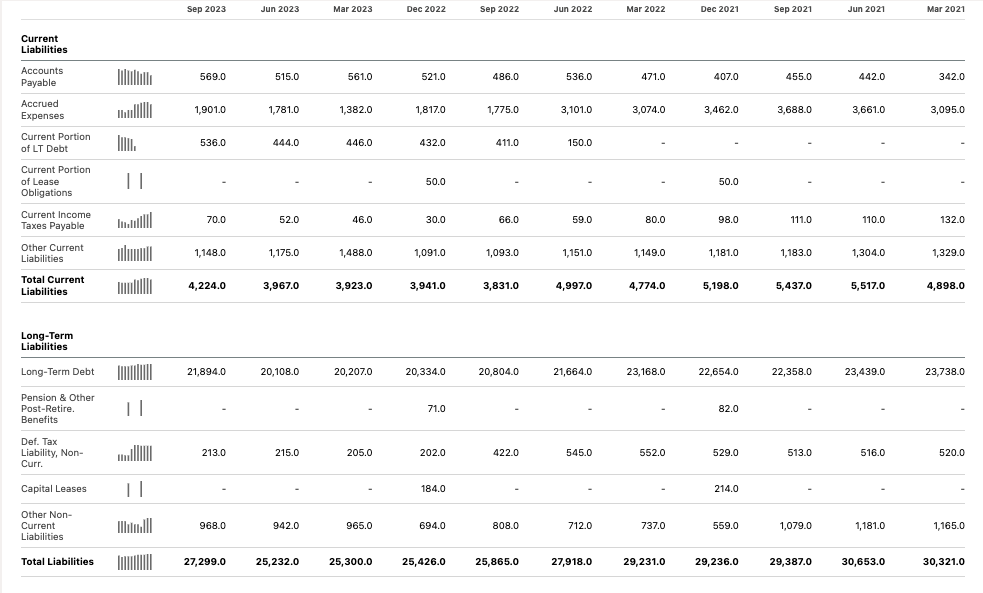

In some ways, such a bonus feels almost laughable, when, as we can see below, Bausch's balance sheet actually looks worse than it did one year ago.

{kind=link}

Total liabilities rose to $27.3bn in Q3 2023, with long-term debt rising to $21.9bn, and current liabilities increasing by ~$500m year-on-year. Meanwhile, current assets have increased ~$1bn year-on-year, to $5.05bn, and total assets by ~$800m, to $27.1bn, including $11.2bn of goodwill.

In terms of its business today, Bausch breaks down its business into 5 segments - as per the Q3 10-Q submission:

- The Salix segment consists of sales in the U.S. of GI products. Sales of the Xifaxan® product line represented approximately 80% of the Salix segment's revenues.

- The International segment consists of sales, with the exception of sales of Bausch + Lomb products and Solta Medical aesthetic medical devices, outside the U.S. and Puerto Rico of branded pharmaceutical products, branded generic pharmaceutical products and OTC products.

- The Solta Medical segment consists of global sales of Solta Medical aesthetic medical devices.

- The Diversified segment consists of sales in the U.S. of: (i) pharmaceutical products in the areas of neurology and certain other therapeutic classes, (ii) dermatology products, (iii) generic pharmaceutical products and (iv) dentistry products.

- The Bausch + Lomb segment consists of global sales of Bausch + Lomb (BLCO) Vision Care, Surgical and Pharmaceuticals products.

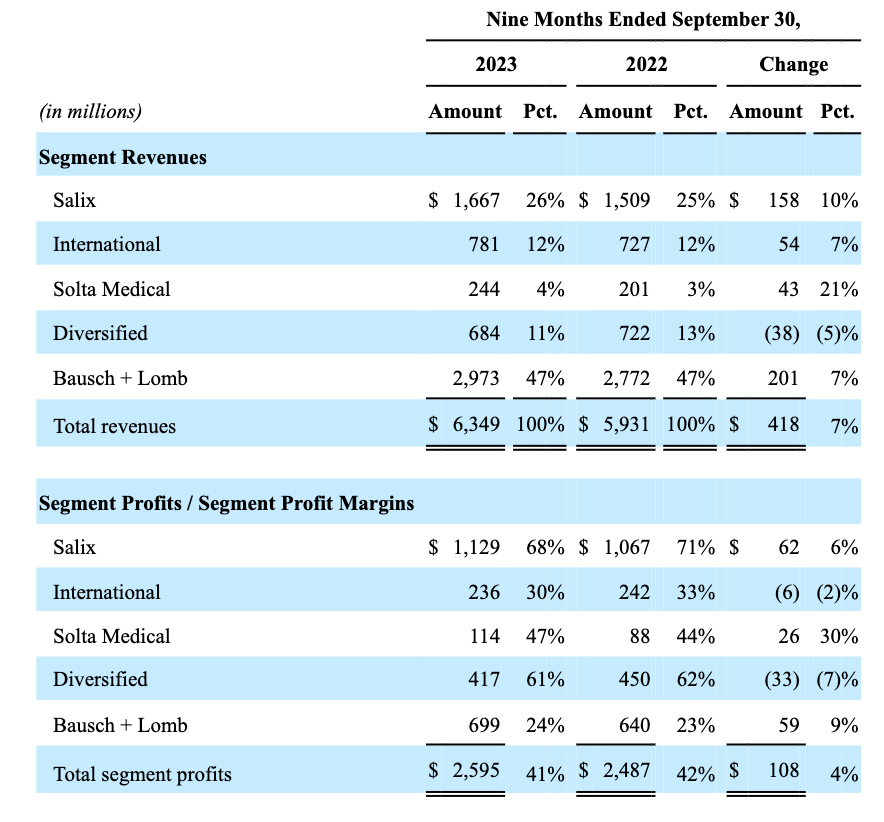

Revenues and margins by division (Bausch Q3 10-Q submission)

{kind=link}

As we can see above, Salix & Bausch & Lomb lead the way both in terms of revenues and margins - although Bausch + Lomb is now an independent company, Bausch Health continues to own 89% of the company. The Solta Medical business is another segment the company has considered spinning out, although ultimately it chose not to after the Bausch + Lomb IPO underwhelmed the market. According to a statement in the 10-Q:

The completion of the full B+L Separation, which includes the transfer of all or a portion of BHC's remaining direct or indirect equity interest in Bausch + Lomb to its shareholders (the "Distribution"), is subject to the achievement of targeted debt leverage ratios and the receipt of applicable shareholder and other necessary approvals. The Company continues to evaluate all relevant factors and considerations related to completing the B+L Separation, including the effect of the Norwich Legal Decision (see "Xifaxan® Paragraph IV Proceedings" of Note 17, "LEGAL PROCEEDINGS") on the B+L Separation.

That takes us to the Salix business - a business that Bausch could arguably also consider spinning out, were it not for litigation. 80% of the Salix division revenues are derived from sales of the Xifaxan product line, and Bausch has been engaged in long running litigation with Norwich Pharmaceuticals, a subsidiary of the generic drug giant Alvogen, over rights to market and sell a generic version of Xifaxan.

With Xifaxan being a critical revenue driver for Bausch, the company has managed to secure agreements with other generic drug manufacturers, including Actavis, Novartis' (NVS) generics subsidiary Sandoz, and Sun Pharma, to prevent them marketing Xifaxan generics until 2028.

Bausch holds patents relating to Xifaxan's hepatic encephalopathy indication that expire in 2029, but Norwich has been pushing for the FDA to accept its Abbreviated New Drug Application ("ANDA") for the irritable bowel syndrome diarrhea (IBD-D) indication. This month, however, a court ruled in Bausch's favour, preventing Norwich from launching its copycat drug. The issues are not yet fully resolved however, with a decision on whether to reinstate some Salix patents expected in Q1 2024.

Away from Salix and Bausch + Lomb and Solta, and the intricacies around when or if the latter two companies will ever be fully divested, and what that might do for whatever is left of Bausch Health the business, management has at least declared itself satisfied with recent progress, at least on the product development front.

The company is attempting to secure approvals for Xifaxan - or rifaximin soluble solid dispersion ("SSD") formulation - for prevention of overt hepatic encephalopathy ("OHE") in patients with early decompensation in liver cirrhosis (RED-C). Two Phase 3 studies will complete enrollment early next year, management, says.

The company is also developing a drug - at the Phase 2 stage - for Sickle Cell Disease ("SCD"), whilst its S1P modulator Amiselimod is being evaluated in a Phase 2 study in the lucrative indication of ulcerative colitis. Meanwhile, the FDA approved CABTREO, a triple-combination topical treatment for acne, in October, and a launch is planned for early next year.

In ophthalmology, Bausch + Lomb has been making a series of strategic acquisitions, including dry eye disease ("DED") therapy XIIDRA from Novartis, plus other clinical stage assets, the "Blink" OTC product line of eye and contact lens drops from Johnson & Johnson Vision, and AcuFocus - an "ophthalmic medical device company that has delivered small aperture intraocular technology to address the diverse unmet needs in eye care." Within Solta Medical, the focus has been on developing a "next generation Fraxel, a "fractionated laser device for skin resurfacing".

Looking Ahead - What Can Bausch Health Achieve In 2024 & Beyond

As mentioned in my intro, if you were to ignore Bausch's debt and assume the business is not about to be broken up into disparate pieces, you could make a reasonable case that the business model is a good one, with substantial, and growing (at close to a double digit percentage rate) revenue generation, strong operating income margins, and the ability to develop a pipeline of new products and opportunities.

You can even make the case - debt aside - that the business is undervalued. But you cannot simply ignore the debt altogether, and neither can you ignore the fact that the business may be officially split into two, or even into three, within the next couple of years, or the pending litigation.

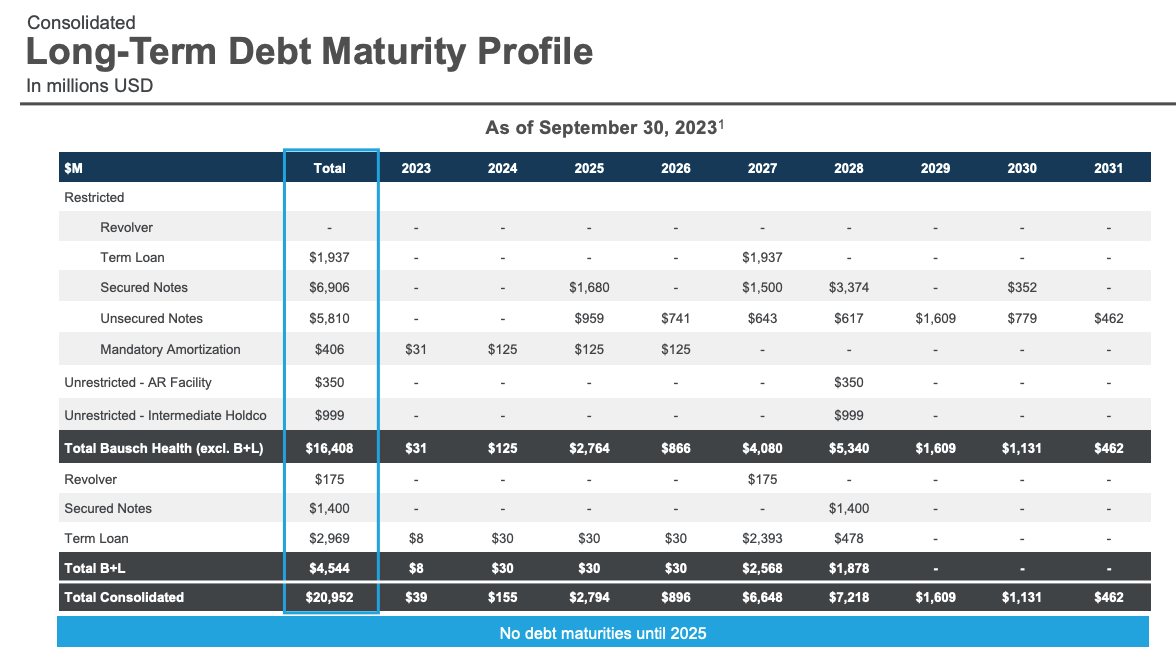

Bausch long-term debt maturity profile (Q3 earnings presentation)

{kind=link}

As we can see above, Bausch has structured its debt so that there are no debt maturities until 2025, which is perhaps what makes the market forgiving of it, and accounts for the 12% gain in the company's share price in 2023 to date.

If we look at the repayments that fall due in 2025, then 2027, and 2028, however - ~$17bn altogether - it is hard to avoid the feeling that running a small pharmaceutical business - which is precisely what Bausch Health is minus Salix, Solta and Bausch + Lomb - in the face of so much debt falling due is akin to rearranging the deckchairs on the deck of the titanic. The tidal wave of debt is coming, even if it is not coming today, or tomorrow.

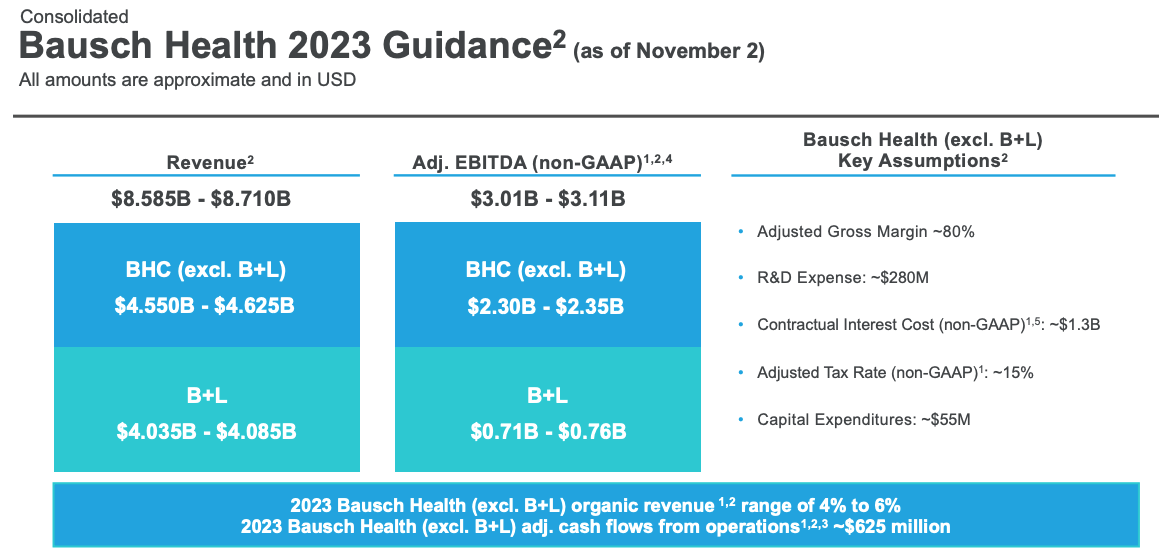

Bausch Health FY23 guidance (Bausch Q3 earnings presentation)

{kind=link}

If we now consider 2023 guidance, again we can see there is a profitable - at least in terms of adjusted EBITDA - business in there, but once again, strip out Bausch + Lomb, and $625m of cash flow from operations is simply not enough to pay down >$20bn of debt long term - plus, there is no guarantee that Bausch will win its court case against Norwich - if it does not, cash flow will likely shrink substantially.

Concluding Thoughts - Surely There Is No Way Back For Bausch?

Although Bausch stock has actually gained since I gave the business a "hold" recommendation 1 year ago, and the company has (arguably) made progress on the litigation front, and even found time to make a series of acquisitions for Bausch + Lomb, and launch new products with reasonable revenue potential, I can't escape the feeling that the day of reckoning is not far away for a business that pursued an extraordinarily aggressive business development strategy under its former name of Valeant, and has successfully managed to evade the full implications of that misadventure to date.

In some ways, you could compare Bausch Health to the spinouts Viatris (VTRS) and Organon (OGN), 2 companies spun out of major pharmaceuticals, and saddled with very high levels of debt. If you look past the debt, both companies are performing adequately, but the reality is you cannot look past the debt, because one day, eventually, the debt has to be paid back.

Using some creative accounting and fully actioning its plans to divest the business could be one way in which Bausch could farm out debt without confronting it in the medium term, but my suspicion is that Bausch is ultimately not a large enough company to succeed with a strategy like that. The company is already throwing M&A money at Bausch + Lomb to keep it growing, while a negative outcome to the Salix litigation has not been fully baked into the share price, in my view. That is why, at the end of 2023, I am giving Bausch a "sell" recommendation.

Fans of contrarian trades or business turnaround opportunities may believe there is unrealised value in Bausch stock, and although I have some sympathy with that argument, and can even envisage a spike in the share price should Q124 court decisions fall in Bausch's favour, my view is that the sun may be setting on Bausch's business, on account of the business flying too close to the sun in the first place, in its Valeant days.

For further details see:

Bausch Health: $20bn Debt Is A Mighty Elephant In The Room