BHC - Bausch Health's Debt Dilemma: Strategic Decisions And Financial Metrics

2023-09-24 10:54:08 ET

Summary

- Bausch Health Companies Inc. faces financial and strategic challenges, with declining revenues and a concentrated portfolio.

- The company's heavy debt burden and precarious credit rating raise concerns about its financial health.

- Bausch + Lomb's strategic initiatives and the acquisition of Xiidra highlight the company's efforts to strengthen its position in the eye health sector.

- The Norwich Legal Decision threatens crucial patents, especially for Xifaxan, a major revenue source for BHC.

- My valuation analysis suggests BHC is overvalued, making it a high-risk investment, so I give it a slightly bearish outlook.

Bausch Health Companies Inc. (BHC) is grappling with many financial and strategic challenges at a pivotal juncture. In this article, I'll delve into BHC's strategic endeavors, its acquisition of Xiidra, and its significant stake in Bausch + Lomb. However, these are juxtaposed against declining revenues and an increasingly concentrated portfolio. While BHC's aggressive M&A strategy and R&D investments signal a company striving for dominance, its financial health, marked by a staggering debt burden and a precarious CCC credit rating, raises red flags. Overall, BHC's financial metrics and strategic decisions don't justify its current valuation. Hence, I lean slightly bearish on BHC at this point.

Business overview and strategic context

Bausch Health Companies Inc. is a diversified, multinational specialty pharmaceutical and medical device company across over 100 countries. While primarily focusing on gastroenterology and dermatology therapeutic areas, the company has also ventured into OTC products and medical aesthetic devices. Its majority ownership in Bausch + Lomb Corporation further diversifies its portfolio by venturing into eye health, providing branded pharmaceuticals, OTC products, and specialized medical devices like contact lenses and ophthalmic surgical equipment.

{kind=link}

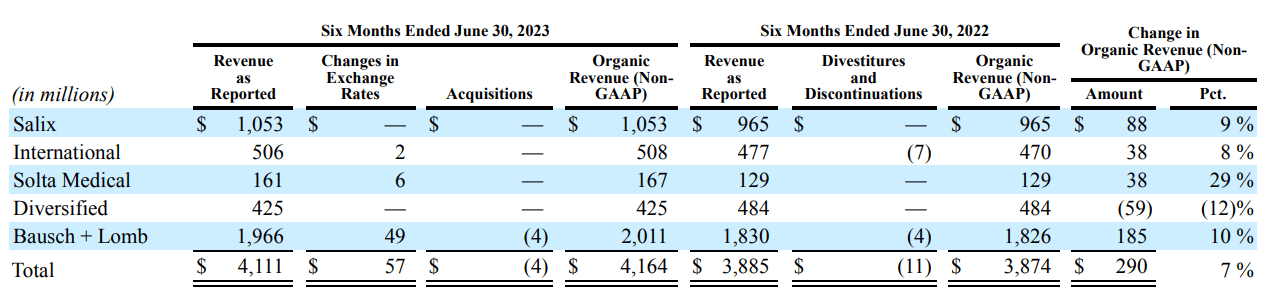

However, a closer look at its revenue streams reveals some warning signs. BHC's revenue declined from $8.434 billion in 2021 to $8.124 billion in 2022. This decline highlights an alarming trend, considering the company's increasing dependency on specific segments for its revenue. For instance, Salix , with its $1.05 billion revenue in 1H2023, is highly dependent on a single product: Xifaxan. Similarly, Bausch + Lomb contributed $3.768 billion in 2022, accounting for 46% of the BHC's 2022 total revenue. So, despite being seemingly diversified, it's quickly becoming more concentrated, increasing its vulnerability to very specific revenue sources.

BHC's causes for concern

BHC's concentration risk is not merely theoretical. Recent developments have brought its very real consequences to the forefront. The Norwich Legal Decision , stemming from a drawn-out intellectual property conflict, poses a significant threat to the validity of crucial patents related to Xifaxan. The gravity of this situation cannot be understated, given that Xifaxan represents 80% of Salix's revenues. Hence, in 1H2023, Xifaxan alone accounted for 20% of BHC's total revenue. This risk is magnified when one examines Bausch Health's deliberate investments in Salix, particularly its strategic initiative to establish a specialized sales force exclusively for Xifaxan. Should the legal winds shift unfavorably, the company could lose patent protection and grapple with the financial and operational consequences now linked to a product potentially facing generic competitors. This becomes even more pertinent when viewed in the context of Bausch Health's ongoing efforts to expand margins and boost revenue, essential steps to counteract its structural unprofitability-a topic I'll delve into subsequently.

{kind=link}

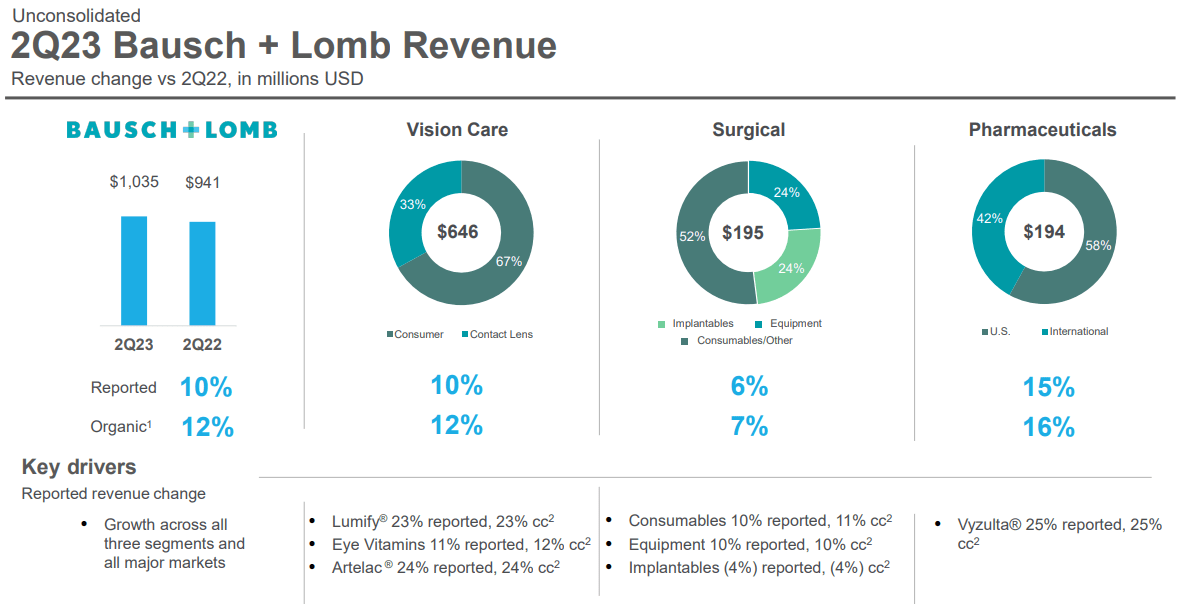

Bausch + Lomb's strategic initiatives in the eye care sector, underscored by the acquisition of Xiidra , highlight the company's embedded M&A growth strategy. Moreover, the decision to retain an 89% stake in Bausch + Lomb following its IPO signals the company's confidence in the segment's growth trajectory. Additionally, BHC's $574 million R&D investment (based on TTM figures ) and the Xiidra acquisition together showcase BHC's deliberate IP portfolio aims.

Nevertheless, the spotlight remains on Bausch + Lomb's ability to adeptly navigate the post-acquisition landscape, particularly in ensuring the seamless integration of Xiidra, capitalizing on its R&D investments, and addressing potential IP challenges. While BHC has been proactive in its M&A endeavors, its income statement suggests that the outcomes could have been more positive. This raises concerns about potential integration challenges, which are pivotal to the success of any M&A strategy.

Financial perspective: Rethinking BHC's M&A

From a financial standpoint, BHC must prioritize fortifying its balance sheet and diminishing its leverage. I believe the 89% stake in Bausch + Lomb could be reduced to garner additional capital. Prudent financial management might also entail reining R&D expenditures to bolster EBIT margins and deferring debt-funded strategic acquisitions like Xiidra. Collectively, these measures should pave the way for BHC's return to profitability, enhancing its creditworthiness and facilitating debt refinancing at more favorable rates.

The slight revenue contraction from 2021 to 2022 raises concerns. While BHC may perceive the Xiidra acquisition as a strategic countermeasure to its inherent unprofitability, it appears more as a high-stakes gamble than a prudent fiscal decision. The associated costs of this acquisition, both overt and covert, might further pressure the company's financial health.

{kind=link}

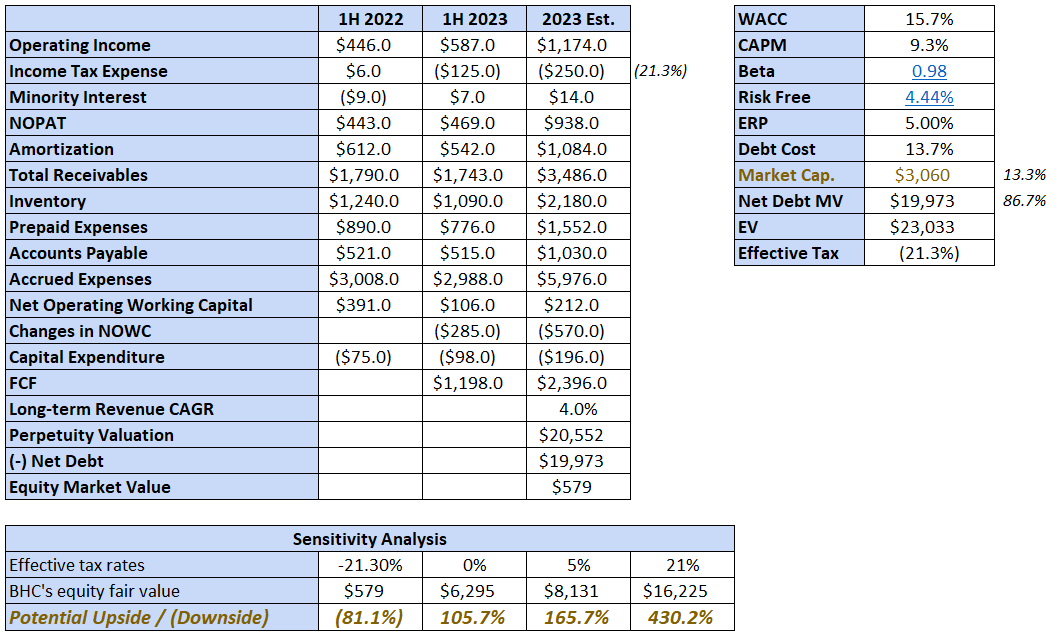

As you can see, BHC's valuation highly depends on its WACC and tax rate. This is mostly due to its excessive debt . This puts its financial health and strategic direction under intense scrutiny. The company's enterprise value of approximately $23 billion , a staggering 86.7% financed by debt, paints a concerning picture of a firm grappling with a suffocating debt burden. Given its excessive debt, BHC's interest expenses outpace its EBIT, making it structurally unprofitable . Its net interest expenses are 1.7 times its EBIT for the first half of 2023. This is alarming any way you look at it.

Valuation and debt analysis

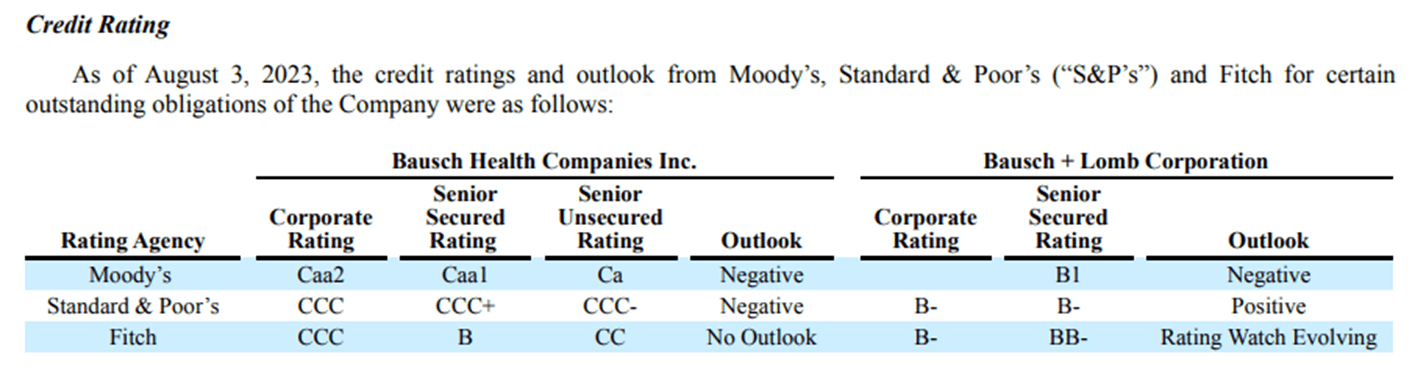

The CCC credit rating BHC holds from Standard & Poor's and Fitch isn't merely a low rating; it serves as a distress signal , indicating minimal financial flexibility. This is further exacerbated by BHC's aggressive M&A strategy, notably its intent to acquire more assets from Novartis (NVS), which seems more of a desperate bid than a strategic move. While the underlying hope appears that these acquisitions will eventually lead to profitability, leveraging an already strained balance sheet is a high-risk strategy, especially given BHC's current financial health.

{kind=link}

Despite the potential of the company's tax assets to reduce its effective tax rate, they remain largely untapped due to its lack of profitability. This, coupled with the prevailing high interest rates for BHC's risky debt , makes every new debt acquisition a double-edged sword. Furthermore, from a valuation perspective, BHC's WACC isn't benefiting from its highly leveraged profile. As you can see in my valuation model, there's an inversion of the typical relationship between equity and debt costs. BHC's CAPM at 9.3% is lower than its forward-looking debt cost of approximately 13.7%. This underscores the financial missteps the company has taken. The Modigliani-Miller theorem's real-world implications further emphasize the adverse effects of BHC's excessive debt.

Springer. BHC's excessive debt now increases its WACC.

Overall, BHC offers a complex picture. While there's potential for a financial turnaround, the company's current path raises concerns. My DCF analysis indicates overvaluation, and when combined with its significant leverage, BHC becomes a high-risk investment. Also, despite the shaky financial footing, management's ongoing focus on debt-driven acquisitions prompts questions about its commitment to shareholder interests. Consequently, considering these factors, I lean towards a slightly bearish outlook on BHC stock.

Conclusion

Bausch Health Companies Inc. stands between potential growth and financial peril. While ambitious, the company's strategic M&A endeavors and promising IP are overshadowed by a looming debt crisis and a series of financial missteps that challenge its viability in the long run. My valuation model shows how BHC is excessively leveraged, giving it a high-risk profile. While there are glimmers of potential, notably in its strategic acquisitions and R&D commitments, the overwhelming debt and associated financial challenges cannot be ignored. Investors must tread cautiously, weighing the potential rewards against the real risks of a debt spiral. Given the current landscape and the company's trajectory, I believe a cautious, slightly bearish outlook on BHC seems prudent.

For further details see:

Bausch Health's Debt Dilemma: Strategic Decisions And Financial Metrics