NVSEF - Bayer: Undervalued With Clear Catalysts

2023-09-11 11:49:04 ET

Summary

- Bayer's stock has had a volatile performance, reaching highs and lows since December 2022, when I first wrote about this company.

- Both from a relative and intrinsic standpoint, Bayer seems to be severely undervalued.

- Bayer has both short-term and long-term catalysts that can propel the stock price upwards.

- Bayer is still a classic turnaround story in the making and receives a 'Strong Buy' rating, as more positive catalysts have emerged since my last write-up.

Thesis

A while back, I wrote my first Seeking Alpha article on Bayer . Since then, the stock price has had a rocky ride and a lot of developments have taken place. I therefore figured it would be a good time to revisit the company and reassess my thesis. In this new article, I take into account a lot of new developments that have affected Bayer in recent months and find that the stock is still severely undervalued and has clear catalysts for both short-term and long-term stock price gains.

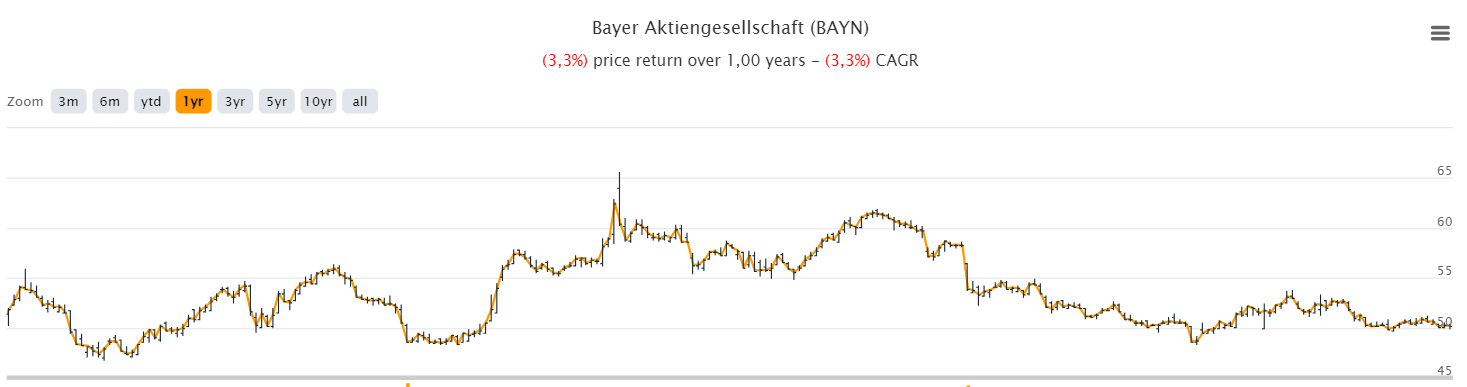

Stock performance

Since my initial recommendation of Bayer ( BAYZF , BAYRY ) in December 2022, the stock has seen a high of €65.66 and a low of €48.52. The stock outperformed the S&P 500 by a fair margin up to May 2023 and underperformed the same index since. The main catalyst behind the stock climbing to a high in May was activist investor Jeff Ubben taking a stake in Bayer back in January 2023. Since then, the previous CEO, Werner Baumann, was ousted and Bill Anderson took over (June 1st). On top of this, the call to de-merge its over-the-counter drug and pharmaceutical units has become more pronounced in recent months. A lot of new articles already discuss this potential break-up, so I will not focus on the break-up, but on Bayer's core fundamentals.

Thus, a lot has happened, but has the underlying story changed as well? Time to revisit Bayer!

{kind=link}

Recent results and outlook

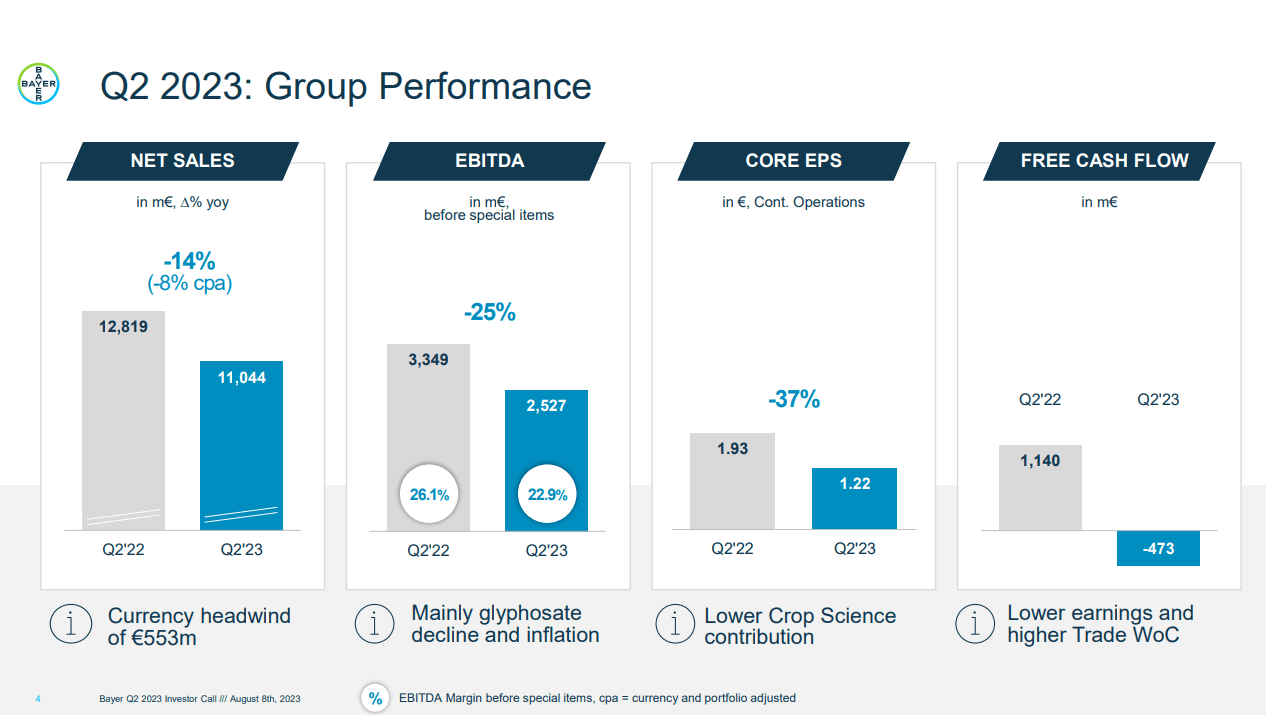

On the 8th of August, Bayer posted its Q2 results of 2023. Revenue dropped from €12.8 billion in Q2 20222 to €11.0 billion in Q2 2023. This was mainly a volume (-7.7% YoY) and currency (-4.3%) effect, mostly attributable to decreasing sales of glyphosate. As Bayer's Wolfgang Nicki put it:

Group sales declined by 8% on a currency and portfolio adjusted basis to EUR11 billion. Out of that, the drop in glyphosate-based herbicide sales accounted for EUR1.2 billion, driving the 18.5% drop in our Crop Science business for the quarter. Our Pharma top-line was flat and Consumer Health grew by 5%.

Sales were down most in Latin America and least in Bayer's core market, Europe. EBITDA was down even more, from €3.2 billion in Q2 2022 to €2.6 billion in Q2 2023. Both basic EPS (-€1.92) and free cash flow per share (-€0.12) turned negative in Q2, 2023. The figure below shows slightly different measures, as it focuses on EBITDA excluding special items and core EPS instead of basic EPS. It's picture clear, though, this was not a pretty quarter for Bayer.

However, these poor results can be mainly attributed to poor management in recent years under the former CEO, Werner Baumann. New management, under Bill Anderson, needs to prove itself in the upcoming quarters. If Bill Anderson can pull of a turnaround of the company, these figures will look a lot prettier in the near term.

Bayer: Group Performance (Bayer)

{kind=link}

Fundamentals

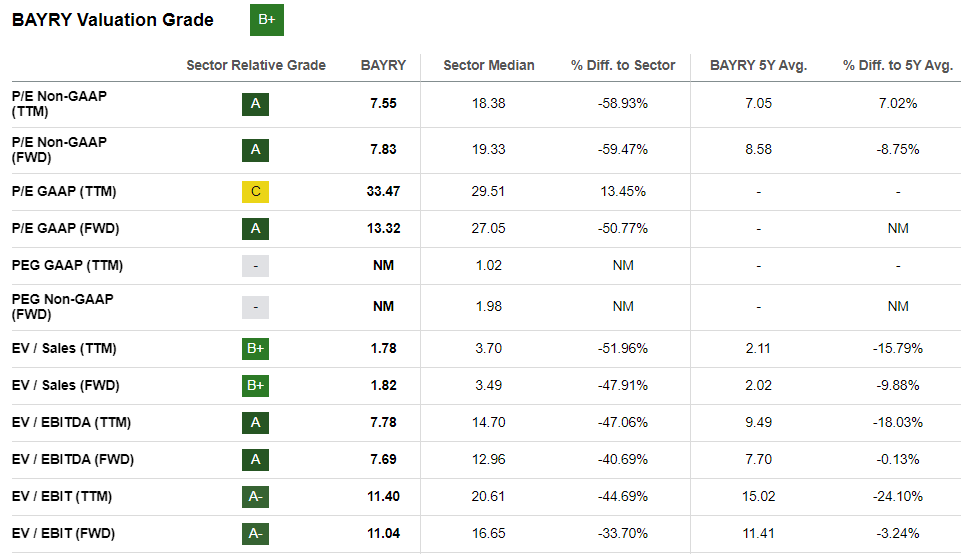

So how do, Bayer's fundamentals look like after this quarter's performance? Since my previous article, the stock price has decreased, but the P/E ratio has actually risen (P/E of 34). This is due to Bayer being in a transitionary phase and having abnormal low returns. If a turnaround of the company unfolds, EPS will most probably return to a long-term level of approximately €4-€5. This would result in a P/E ratio of slightly below 10. EV/EBIT wise, Bayer is valued at a more attractive 11.4.

Diving deeper into the balance sheet, one can see that both assets and liabilities have decreased YoY, to €122 billion and €85 billion respectively. Book value per share has decreased as well, to €37.61 in Q2 2023, down from €38.7 in Q2 2022. This results in a P/B ratio of approximately 1.3, which is quite favorable. Long-term debt is still very high, though, at €35.4 billion, resulting from the Monsanto takeover. This is clearly a risk, as interest rates are rising. In Germany, they haven't risen as fast as in the US, but nonetheless this warrants extra caution, especially since a growing portion of Bayer's outstanding long-term debt is due in the near term.

{kind=link}

Catalysts

So far for the financials. How does the background story look like for Bayer? I identified a few catalysts for Bayer to actually pull off a turnaround in the upcoming months:

- Bayer being, for a large part, a crop science company is a major macro tailwind for me. Both population growth and climate challenges demand new products that Bayer can supply. It is one of the world's premier firms on crop science and has a proven track record of products and know-how.

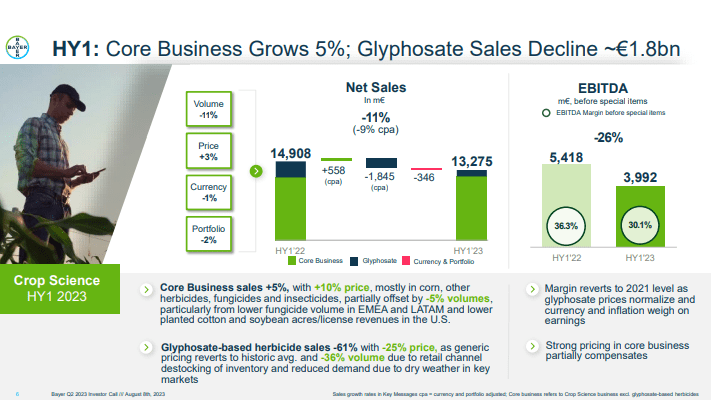

- Bayer's core business within its crop science department is still growing. The poor financial performance of the most recent quarter is mostly due to a big decline in sales of Bayer's crop science department and more specifically glyphosate. As Rodrigo Santos, head of the Crop Science Division, put it:

Starting with our results for the first half of the year and building on the Q2 results, you can see on our appendix, total Crop Science sales declined 9%, currency and portfolio adjusted. This was the net effect of nearly EUR560 million or 5% growth in our core business and EUR1.8 billion or 61% decline in our glyphosate-based herbicide sales. The growth in our core was driven by 10% pricing gains supported by new product launches, which outpaced the volume decline.

- Management has changed. Anyone familiar with Bayer knows that previous management was not popular. Bayer's previous CEO, Werner Baumann, was running the firm during the disastrous Monsanto takeover and all the litigation cases stemming from it. Since then, he has clearly failed to get the company back on track. Bill Anderson has taken over recently, which can definitely lead to a culture (and financial) change within Bayer.

- Activist Jeff Ubben took a stake in Bayer and got a seat at the table. This is not per se a catalyst by itself, but it can definitely advance the needed changes within the company to get back on track to increased profitability.

Bayer: Core Business Still On Track (Bayer)

{kind=link}

Risks

Besides the catalysts discussed above, there are also some clear risks (besides the long-term debt) associated with investing in Bayer. The main ones, in my opinion, being:

- The disastrous Monsanto takeover is still causing major problems for the company. Numerous lawsuits have been started against Bayer, because of alleged health risks associated with Monsanto's main product, Roundup. A lot of lawsuits have been settled already, and Bayer has also been winning lawsuits. It thus seems that the peak of lawsuits may be behind us. It has, however, caused a lot of bad PR for the company and this will stick with it for a long time.

- Macro headwinds in Bayer's home country, Germany. Germany's economy is in bad shape. For a brief period it was in a recession and its growth has been stagnating since . The direct cause is of course the rising energy costs resulting from the war in Ukraine, but there are indirect causes as well. Germany's competitiveness is increasingly looking more worrisome. Even more so since its main industry, automotive, is being majorly disrupted by numerous EV firms. Bayer is very diversified, though, so it should be less affected by this than other German firms.

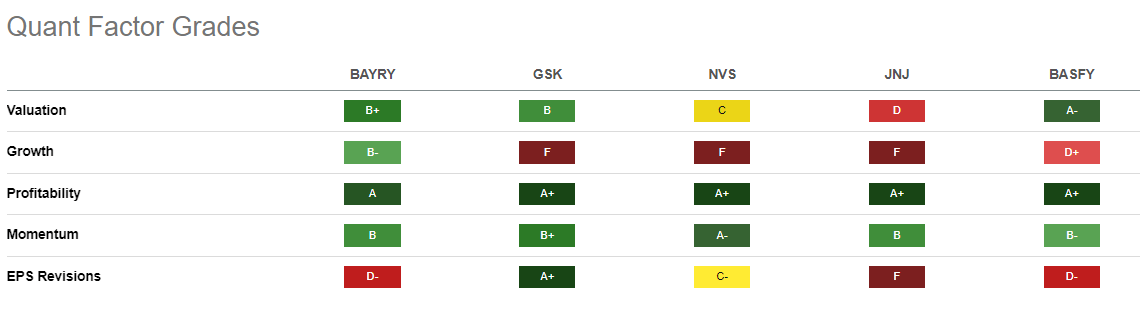

Valuation

So how does Bayer compare to its peers? If we compare Bayer to some of its closest peers such as GSK ( GSK ), Novartis ( NVS ), Johnson & Johnson ( JNJ ) and BASF ( BASFY ), we can see that it compares quite favorably. According to Seeking Alpha's quant factor ratings, it is cheaper than the other firms (except BASF, which is more at risk because of Germany higher energy costs). Growth wise, it also compares favorably, which is reinforced by my identified macro tailwind of it being one of the foremost companies in the world of crop science. Profitability wise it performs slightly worse than its closest peers though. The recent change in management can however boost its profitability, but this remains to be seen.

{kind=link}

Further, quantifying my thesis, I also performed a DCF analysis. As I expect Bayer's short term headwinds to persist for the following year (following guidance), I pessimistically estimate no free cash flow for both 2023 and 2024. From 2025 and onwards, I expect Bayer to return to its long-term free cash flow level of approximately €5 euro per share. As Bayer operates in a market that should grow faster than the average economy, I estimate its growth rate to be in the region of 5%. In order to calculate the terminal value, I used a terminal growth rate of 3%, which is in line with general economic growth. Finally, I used a discount rate of 10%. In the figure below, one can see that this gives us an intrinsic value of almost €70 euro per share. This yields us a margin of safety of almost 28%, which is quite comfortable in my opinion.

It thus seems likely, on the basis of both relative and intrinsic value, that Bayer is undervalued.

{kind=link}

Takeaway

Bayer is one of the main chemical companies of Germany and seems to be undervalued according to both a relative and intrinsic valuation. Besides this, there are clear catalysts for Bayer to improve its financials in the short-term (new management and activist investors taking a stake) as there are in the long-term (crop science being a major growth market). There are, however, also some risks associated with Bayer, such as bad PR and lawsuits from its Monsanto takeover and macro headwinds in its home country Germany. All in all, however, I think that Bayer is severely undervalued and back on track to become very profitable. Therefore, I rate Bayer a 'Strong Buy'.

For further details see:

Bayer: Undervalued With Clear Catalysts