BTE - Baytex Energy Turns Its Focus Towards The Eagle Ford

Summary

- Baytex Energy Corp. is acquiring Eagle Ford producer Ranger Oil Corporation for approximately US$2.5 billion.

- A bit under 50% of the consideration is in cash plus assumed net debt.

- Baytex is also increasing its share count to around 870 million, with Ranger shareholders owning 37% of the combined company.

- Around 60% of Baytex's production will now come from the Eagle Ford.

- Baytex's projected heavy oil production goes down from around 41% of total production to 22%.

Baytex Energy Corp. ( BTE ) is acquiring Eagle Ford producer Ranger Oil Corporation ( ROCC ) for approximately US$2.5 billion . The purchase price is in-line with my prior estimates of Ranger's value and appears to be a fair deal for both companies.

The deal does shift Baytex's focus from being a primarily Canadian producer that was aiming to increase heavy oil production to being a primarily Eagle Ford producer (although with close to 40% of production coming from Canada). Baytex's heavy oil production has more torque to oil prices, with a 36% jump in WTI from US$55 to US$75 oil increasing its realized price for heavy oil (assuming a static US$17.50 differential) by 67%. The Eagle Ford production has less pricing risk since it isn't exposed to both volatile differentials and changes in the benchmark WTI and Henry Hub prices.

I estimate Baytex's value at approximately US$4.85 per share in a long-term $75 WTI oil scenario, along with WCS differentials in the low-$20s. Thus, at under US$4 per share, Baytex has a reasonable amount of upside.

This report uses U.S. dollars unless otherwise noted and an exchange rate of US$1.00 to CAD$1.35.

Acquisition Details

Baytex is paying approximately US$2.5 billion for Ranger Oil, which includes the assumption of an estimated US$650 million in net debt at closing (estimated late Q2 2023). Ranger shareholders are receiving 7.49 Baytex shares plus US$13.31 in cash for each Ranger common share they own. This adds up to total consideration of US$44.36 per share based on Baytex's share price at market close on February 27. This is a 7% premium to Ranger's closing price on February 27. Ranger shareholders will own 37% of the combined company, while Baytex shareholders will own 63% of the combined company.

Baytex's stock reacted negatively to the deal, dropping 8% at the time of this report. This reduces the total consideration to approximately US$42.75 per share based on Baytex's current price, which is a 3.5% premium to Ranger's closing price on February 27.

My initial impression is that the deal price is fair for both companies. I had previously estimated Ranger's value at US$45 to US$46 per share at the end of 2023. This did assume that Ranger could generate around US$1 per share in quarterly free cash flow during 2023, so a US$42 to US$43 valuation at this point in time seems reasonable.

Stand-alone Ranger's 2023 Outlook

While Ranger hadn't provided formal guidance for 2023 yet, it did mention that it expected high-teens production growth during 2023 if it went with a three-rig drilling program.

Thus, my model for Ranger's 2023 production has it at 48,700 BOEPD (71% oil) in average net production, which is 18% production growth compared to Ranger's full-year 2022 guidance (as it hasn't reported final 2022 production volumes yet). Ranger is expected to exceed 50,000 BOEPD in production later in 2023.

Baytex mentions Ranger's net production of approximately 53,000 BOEPD in its presentation, but that is for the July 2023 to June 2024 period. Given that, it appears that expectations are for a fair bit of continued production growth into 2024.

At the current 2023 strip of approximately $76 WTI oil, stand-alone Ranger was projected to generate $1.059 billion in revenues after hedges in 2023.

Ranger has a small amount of hedges in 2024, with an approximate value of negative $2 million at current strip.

| Barrels/Mcf |

| $ Per Barrel/Mcf (Realized) |

| $ Million |

| Oil |

| 12,702,000 |

| $76.00 |

| $965 |

| NGLs |

| 2,536,750 |

| $28.00 |

| $71 |

| Natural Gas |

| 15,220,500 |

| $2.75 |

| $42 |

| Hedge Value |

| -$19 |

| Total Revenue |

| $1,059 |

I've been estimating Ranger's 2023 capex at $600 million with a three-rig drilling program. This leads to an estimate that stand-alone Ranger could generate $173 million in positive cash flow in 2023 at the current strip.

| $ Million |

| Lease Operating Expense |

| $94 |

| Gathering, Processing and Transportation |

| $46 |

| Production and Ad Valorem Taxes |

| $59 |

| Cash G&A |

| $44 |

| Cash Interest |

| $43 |

| Capital Expenditures |

| $600 |

| Total Expenses |

| $886 |

Stand-alone Baytex's 2023 Outlook

I've updated the model for Baytex's stand-alone performance to reflect current strip prices, along with a WCS differential of negative US$17.50. While 2023 WTI oil prices have gone down by around $5 since I looked at Baytex in January, the WCS differential has improved, resulting in no real change to Baytex's expected realized prices for heavy oil.

Baytex is now projected to generate US$1.681 billion in revenues after hedges in 2023.

| Units |

| $ Per Unit |

| $ Million USD |

| Heavy Oil |

| 13,094,375 |

| $51.00 |

| $668 |

| Light Oil and Condensate |

| 11,497,500 |

| $74.00 |

| $851 |

| NGLs |

| 2,555,000 |

| $30.00 |

| $77 |

| Natural Gas |

| 28,743,750 |

| $2.40 |

| $69 |

| Hedge Value |

| $16 |

| Total |

| $1,681 |

It can now generate around US$381 million in positive cash flow at the current strip.

| $ Million USD |

| Royalties |

| $350 |

| Operating Expenses |

| $340 |

| Transportation |

| $47 |

| Cash General And Admin |

| $39 |

| Cash Interest |

| $48 |

| Capital Expenditures |

| $454 |

| Leasing Expenditures |

| $3 |

| Asset Retirement Obligations |

| $19 |

| Total Expenses |

| $1,300 |

Other Notes

The reported production from Ranger's assets will increase after the deal closes. U.S. companies report production on a net revenue interest basis (net of royalties), while Canadian companies report production on a working interest basis, with royalties as an expense. There is no difference to the bottom line, but the reported production from Ranger's assets will increase by approximately 30% as a result of these accounting changes.

Post-closing, Baytex will be more of an Eagle Ford focused company, albeit with a significant Canadian presence. Approximately 60% of Baytex's production will come from the Eagle Ford after the deal closes.

Baytex's Dividend

Baytex intends to introduce a CAD$0.0225 (US$0.01667) per share quarterly dividend after the deal closes. With around 870 million shares outstanding, this adds up to around CAD$78 million (US$58 million) per year in dividend payments. Baytex intends to increase shareholder returns (including dividends) to 50% of free cash flow. The combined company would generate around US$554 million in proforma free cash flow in 2023 at current strip prices, along with around US$1.7 billion EBITDAX.

Ranger shareholders are receiving a roughly 66% increase in dividends based on the Baytex shares they are receiving.

Notes On Valuation

While I believe the Ranger acquisition price was fair, my estimated value for Baytex (based on long-term $75 WTI oil) has been tweaked to approximately US$4.85 if WCS differentials average in the low-$20s (U.S. dollars) going forward. With WCS differentials of US$12.50 in the long term, Baytex's estimated value is around US$5.45 per share.

Baytex has less exposure to Canadian differentials going forward, with the majority of its production now receiving Gulf Coast pricing. Baytex's Canadian heavy oil assets benefit more from higher oil prices, though.

For example, a scenario with $55 WTI oil and a WCS differential of US$17.50 would result in a realized price of around US$30 for Baytex's heavy oil production. At $75 WTI oil and the same differential, Baytex would realize around US$50 for its heavy oil, a 67% increase in realized prices. The realized price for a barrel of Eagle Ford oil would increase by around 36% in a jump from $55 to $75 WTI oil.

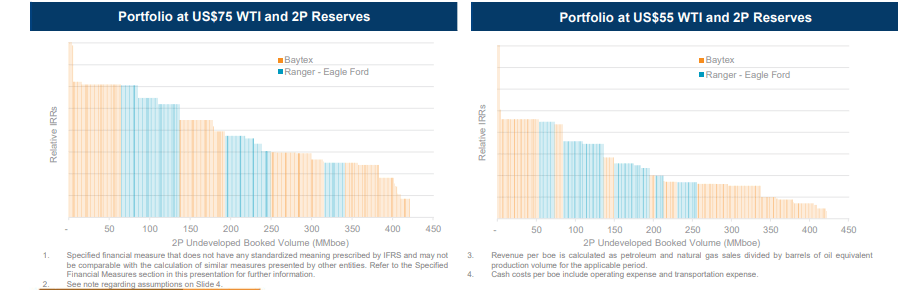

Baytex's Inventory Portfolio (baytexenergy.com)

{kind=link}

Conclusion

Baytex Energy Corp.'s acquisition of Ranger Oil Corporation appears to be at a fair price. This shifts Baytex's focus to the Eagle Ford, which will now account for approximately 60% of its total production. Eagle Ford production has less torque to higher benchmark commodity prices but is not affected by the volatile differentials that can cut into Baytex's heavy oil margins.

There is less sensitivity to changes in heavy oil differentials now, although those will still have some effect on Baytex's value. I now estimate Baytex's value at approximately US$4.85 per share in a scenario with long-term $75 WTI oil along with a WCS differential in the low-$20s. Baytex's value is estimated at approximately US$5.45 per share in a scenario with long-term $75 WTI oil along with a WCS differential of around US$12.50.

With Baytex Energy Corp.'s stock taking a hit and falling below US$4 now, it appears to have a decent amount of upside in a long-term $75 WTI oil scenario.

For further details see:

Baytex Energy Turns Its Focus Towards The Eagle Ford