BDORY - BB Seguridade Stock: A Premier Choice For Dividend Investors

2023-06-29 17:25:36 ET

Summary

- BB Seguridade reported a net income increase of almost 50% year-over-year in the first quarter of this year due to higher premiums in an inflationary and high-interest rate environment.

- Despite the strong performance in trading and a notable 70% appreciation of BB Seguridade's shares over the past two years, the company's compelling yields remain a fundamental aspect of its investment thesis.

- There are risks due to the eventual deceleration of interest rates in Brazil, which I believe should not hinder the growth of the company's earnings.

BB Seguridade Participações ( BBSEY ) is a company controlled by Banco do Brasil ( BDORY ) and established in 2012 after the separation of the insurance division of the Brazilian bank. The company operates in a series of insurance lines such as life, housing, rural, and others.

The company's historical results have offered stability during periods of macroeconomic stress. BB Seguridade has presented attractive multiples, mainly concerning its efficiency, evidenced by the return on equity (ROE) of 66%. This extremely high percentage comes from a competitive advantage due to the access to Banco do Brasil's sales channel.

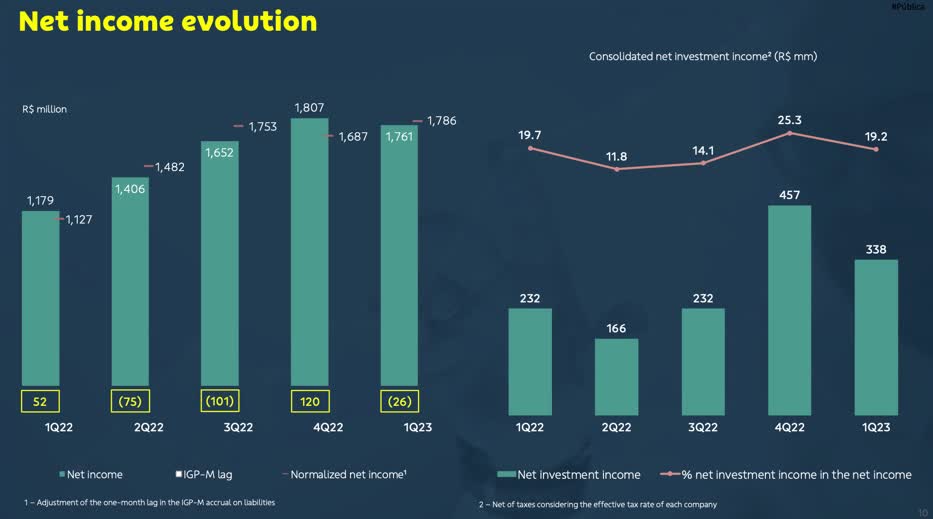

In its most recent quarter, BB Seguridade registered its highest net income since its IPO, growing almost 50% year-over-year, driven by higher premiums in an inflationary and high-interest rate environment. As prices rise, the value of insurance policies also increases, resulting in higher revenues.

I believe that the company will continue to present good results, with the increase in premiums issued by its subsidiaries, especially the growth in contributions to the Brasilprev pension plans, and the continuity of solid financial results, even in a scenario of falling interest rates in Brazil, which tends to be slow. Moreover, dividend distribution should continue to be very attractive, the main highlight of the investment thesis.

Solid Latest Results

In its most recent earnings , on May 15th, BB Seguridade reported a net profit of approximately R$1.76 billion in the first quarter of 2023, representing a 49.6% year-on-year growth.

BB Seguridade's consolidated financial result reached R$338.2 million, a year-over-year increase of 45.7%. The company's non-interest income grew 40.6% year-over-year, exceeding the targets in the guidance for 2023.

BB Seguridade's Investor Relations

{kind=link}

Upon analyzing BB Seguridade's results by segment, we can provide a comprehensive explanation for the company's impressive performance as outlined below:

- Brasilseg : the subsidiary engaged in the retail and wholesale insurance market was one of the protagonists in delivering robust operating results. Brasilseg saw a 35.2% increase in revenue from written premiums in Q1 2023.

- Brasilprev: operating in the pension sector, it recorded a net income of R$438.3 million, an increase of 8.9% from the previous year. The subsidiary registered net funding of R$1.93 billion and total pension and insurance revenues of R$14.79 billion. These revenues from management fees represented an increase of 5.3% and 3.7% year-over-year.

- Brasilcap: in its capitalization securities segment, Brasilcap collected around R$1.43 billion, representing an increase of 3.6% year-over-year. Revenues from the financial result grew 23.6% compared to 1Q22. Capitalization operations registered a net income of R$62.7 million, an increase of 17.9% year-on-year.

- BB Corretora: finally, BB Corretora reported an increase in brokerage revenues that caused a 23% growth in net income, totaling R$707.7 million. The solid commercial performance was the driver that caused revenues to soar by 18.9%, with insurance brokerage revenues standing out. It also increased the broker's operating margin by 0.3 p.p. due to selling products with lower reimbursement amounts.

Dividends to Remain Super Attractive

Despite the significant trading performance witnessed over the past two years, resulting in a remarkable 70% appreciation of BB Seguridade's shares, the continued distribution of dividends remains a crucial component of the investment thesis.

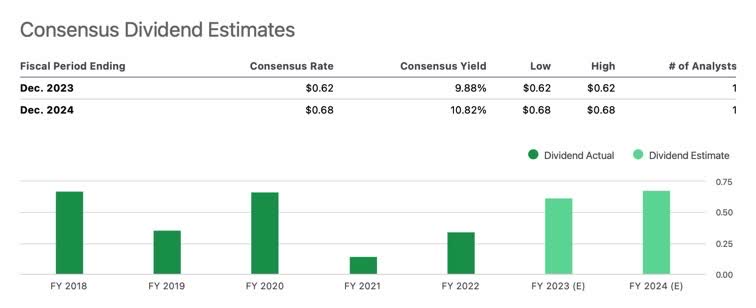

The company's policy is to payout at least 25% of profits, but over the last decade; it has paid an average of 94%. Last year, BB Seguridade's payout was 95% – giving it an average yield of 5.83% in 2022.

While BB Seguridade's bottom line gradually increased due to higher interest rates of 13.75% in Brazil since September last year, the Brazilian insurer's current yield is a whopping 9.56%. For the end of next year, the consensus is that the percentage will be even more attractive, reaching 10.82%.

{kind=link}

The confidence that BB Seguridade will continue to report robust profits rests on the prospect that the Brazilian Central Bank will keep interest rates high for some time, even as inflation shows signs of easing.

Brazilian inflation forecast for 2024 is at a level below 4.0%. The projection of the introductory interest rate of the Brazilian economy (Selic) remains at 12.25% for the end of this year, and for 2024 should be slightly below double digits at 9.50%.

Mind the risks; BB Seguridade is State-Owned

BB Seguridade is controlled by Banco do Brasil, a state-owned bank where 50% of its shares belong to the Federal Government. Considering the political and financial instability in Brazil, this is a very relevant risk for the thesis of investing in BB Seguridade.

The risks are further exacerbated considering that the current Brazilian government, led by President Luiz Inácio Lula da Silva, has an interventionist bias. Although BB Seguridade's controller, Banco do Brasil, is listed at the highest level of corporate governance on the Brazilian stock exchange, called " New Market ."

The "New Market" requires companies to issue only common shares with voting rights, regardless of the shareholder. Additionally, Banco do Brasil's board comprises half independent members and two representatives of minority shareholders.

However, it is worth noting that BB Seguridade's governance is slightly different from Brazil's average state-owned companies. Private companies control BB Seguridade's subsidiaries Brasilseg, Brasilprev, Brasilcap, and BB Corretora. Thus, Banco do Brasil is a relevant shareholder but a minority shareholder in its subsidiaries. It tends to mitigate the state risk, resulting in fewer governance problems.

Valuation Offers a Good Entry Point

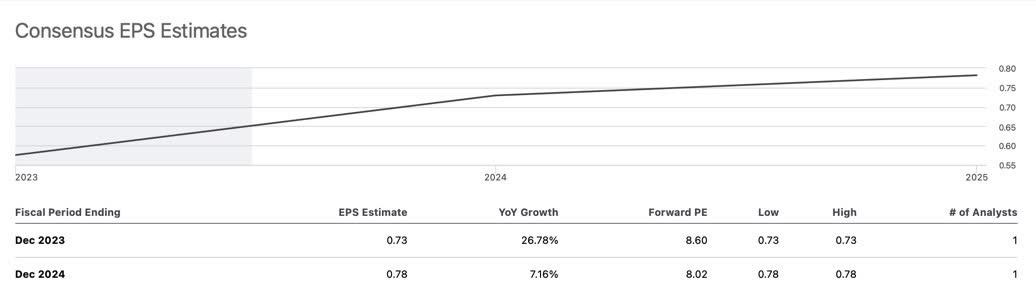

BB Seguridade's shares currently trade at a forward price-to-earnings (P/E) ratio of 8.61 times, in line with the industry average. This multiple, however, should remain at a similar level until the end of next year as the consensus is a 34% increase in the company's EPS from now, resulting in a forward price-to-earnings multiple of 8 times.

{kind=link}

Still, I consider it a low multiple mainly because the risk of being a state-owned company is priced in, considering the high dividend yield expected above 9% for this year.

The revenue estimate, however, is that there will be a 32% growth until the end of this year, making BB Seguridade trade at a forward price-to-sales (P/S) ratio of 6.6 times.

By the end of 2025, the consensus is more conservative, forecasting revenues to rise another 17%, making the company trade at a multiple of 5.7 times – still well above the industry average of currently about two times. This also could be that the market may be giving more weight to revenue generation and growth prospects than current earnings.

The recent drop in the company's share price, especially since the beginning of this year, coupled with a strong performance, could be a good entry opportunity, considering that the company was trading at a P/E ratio above 12 times in February of this year.

BB Seguridade's weaker stock performance, which resulted in a more attractive valuation, can be explained by the market's pricing and the effect on the company's earnings of a potential drop in interest rates. In any case, based on recent results, BB Seguridade's profitability metrics may remain strong for longer than expected, even if there is a drop in operating income.

The Bottom Line

BB Seguridade stands out as a highly profitable company, exemplified by its exceptional ROE. Moreover, the company maintains a generous dividend payout, underscoring its ability to fuel growth through a dividend distribution. This position provides BB Seguridade with significantly stronger profitability indicators than other insurers and banks, giving the company a notable competitive advantage.

Even though there are risks linked to a further deceleration of interest rates that should impact BB Seguridade's operational result from now on, The Brazilian Central Bank has been taking an extremely cautious stance in reducing interest rates, and even in the next two years, the projection is of interest rates still at high levels.

Therefore, I see the company continuing to report increased profits leading to shareholders' excellent distribution of dividends, as the payout should remain close to 95% of the company's earnings.

For further details see:

BB Seguridade Stock: A Premier Choice For Dividend Investors