BBN - BBN: Investors Continue To Get Punished By Leverage

2023-08-05 14:36:56 ET

Summary

- BlackRock Taxable Municipal Bond Trust has registered losses and the leverage headwind has not evened out.

- Higher short-term rates on highly leveraged funds remain a stubborn headwind, making a "buy" case difficult.

- The discount on BBN has widened to almost 8%, making it look cheap compared to its historical premium or small discount.

Main Thesis & Background

The purpose of this article is to evaluate the BlackRock Taxable Municipal Bond Trust ( BBN ) as an investment option. This fund offers exposure in taxable municipal bonds, with an objective to "seek high current income, with a secondary objective of capital appreciation."

As a long-term investor in munis I saw a lot of inherent value in BBN when 2023 got underway. I thought the leverage headwind would be even-out by now and the discount to NAV and strength in the credit quality of the underlying securities would push the fund higher. In hindsight, I was dead wrong , as BBN continues to register losses:

Fund Performance (Seeking Alpha)

Looking ahead I would normally suggest continuing to buy here. At some point yields have to ease and that will be a boon for fixed-income products across the board - BBN included. But the pressure of higher short-term rates on highly leveraged funds remains a stubborn headwind for the moment. This makes a "buy" case difficult to make for those who cannot withstand potential losses in the immediate term. The positive news is the discount has widened and credit quality remains strong. So there is merit to buying in, but I have concerns. This dynamic leaves me with the feeling that "hold" is the right call and I will explain why in detail below.

Discount Has Widened To Historically Cheap Level

On the surface BBN would normally look like a buy to me. I want to touch on a key reason why to help justify why I do not feel a "sell" or more bearish outlook is warranted. This rests simply with valuation. BBN looks cheap. This is a fund that often trades at a premium or relatively small discount. But today that discount has widened to almost 8% - an enticing figure for most funds:

{kind=link}

This is a wide discount in isolation and also when we consider back in March when I last covered BBN it had a discount around 4.5%.

My thought here is value is certainly apparent, especially for those with a long-term view. Personally I think there is a good case to make for buying at these levels - save the fact that some macro-headwinds exist. The problem with buying simply because of a "cheap" valuation is that premiums and discounts alone do not move markets or funds. BBN had a "cheap" valuation in March and the return has been negative. Other factors got in the way that did not bring in enough buyers to narrow the valuation gap towards par. While we don't know yet what the next few months can bring, that serves as a lesson that discounts do not always narrow now (or ever) and readers should still approach this one cautiously for now.

Leverage Hurdle Has Hurt, And Could Continue To

My next thought touches on the high use of leverage for this fund. That has been key to the poor performance over the past year and in the past few months. Simply put, this fund borrows excessively to try to boost returns:

BBN's Leverage (BlackRock)

Now, when conditions are favorable, this can work out in a very lucrative way. The problem is that conditions have not been favorable for a while and the net result has been a bit of a disaster for BBN:

BBN's 1-year Chart (Seeking Alpha)

Now, fixed-income took it on the chin in 2022 across the board. So it is fair to say that BBN was not alone in this weakness. But there has been a rebound this calendar year that this CEF has not really taken advantage of. This should be the obvious question of - "why"?

The answer lies with the use of leverage. The underlying muni securities are doing just fine. They have rebounded with fixed-income modestly and credit quality remains strong. But the use of leverage this excessively in a rising short-term rate environment has dramatically increased the borrowing costs for the fund. This has led to income pressure on BBN and resulted in two income cuts in less than a year:

BBN's Distribution Stream (BlackRock)

It would be easy to suggest the worst is passed here. And, honestly, it very well could be. Nobody wants to ride a fund lower, sell at the low, and watch it rebound. So holders of this fund should weigh this very carefully before dumping it.

But we also have to be realistic. The reason behind this income pressure is that short-term rates have increased faster than long-term ones. This has led to increased borrowing costs while income opportunity down the maturity curve has been limited. The challenge for the moment is this headwind - which has been paramount to BBN's poor performance - has not gone away. In fact, short-term treasury yields have continued to rise recently and that has left the yield curve severely inverted:

Yield Curve (showing inversion) (Bloomberg)

{kind=link}

The takeaway here is that until this changes BBN, as well as many other highly leverage CEFs, will remain under pressure. Unless they deleverage, which they are not going to by all accounts, this macro-headwind remains as relevant and challenging as ever. This is central to why I don't see a "buy" rating as appropriate given this consistent backdrop.

Munis Remain A Source Of Quality

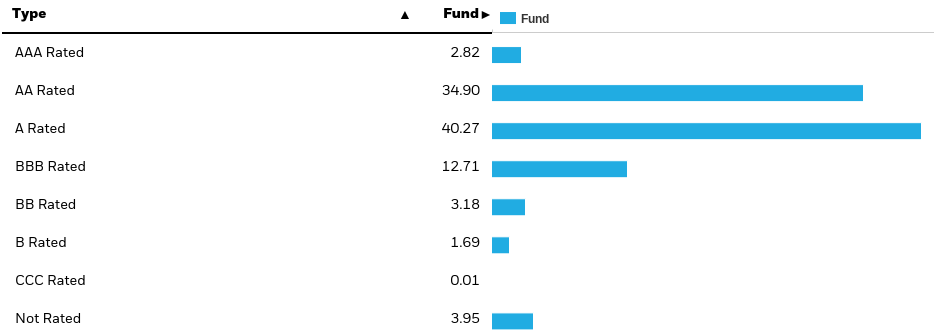

I want to take a moment to dig in to the underlying securities. Muni bonds, whether tax-exempt or taxable (which BBN predominately holds) continue to represent a safer asset class for conservative investors. When we factor in the tax savings, munis can be very rewarding, but even taxable options like the ones BBN holds offer relatively high yields right now. BBN's current yield is near 7% - and that is certainly attractive in isolation. It is well above what other IG bonds are offering and bank savings accounts too. When I consider the BBN is backed by mostly IG-rated debt, this looks enticing:

BBN's Credit Ratings (BlackRock)

{kind=link}

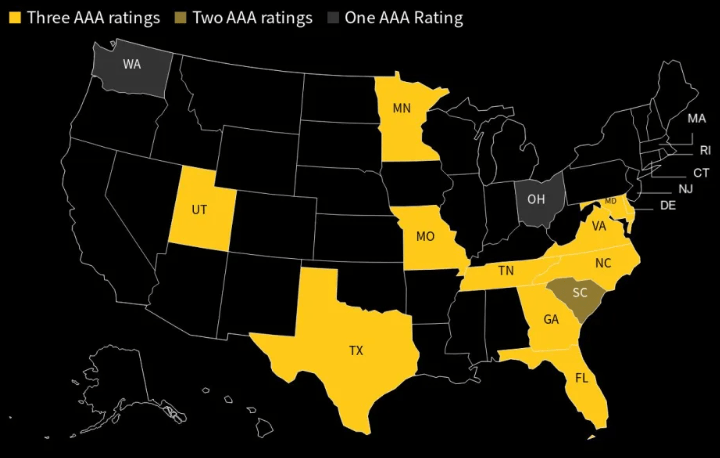

Furthermore, on the news of the downgrade by Fitch on US treasures, state and local government debt may even look more attractive by comparison! For example, a number of different individual states now hold better credit ratings than the federal US government - quite a shock to start the month of August!:

States With Stronger Credit Ratings Than Feds (Yahoo Finance)

{kind=link}

This is a striking development that may have longer term implications down the line. Time will tell is the US government gets its house in order. If history is a guide, it probably won't. With state and local governments needing to have a balanced budget (imagine that!), this could make muni debt a relative bargain versus treasuries in the months and years ahead (less drama, higher yields).

Munis Yielding More Than Comparable Corporates

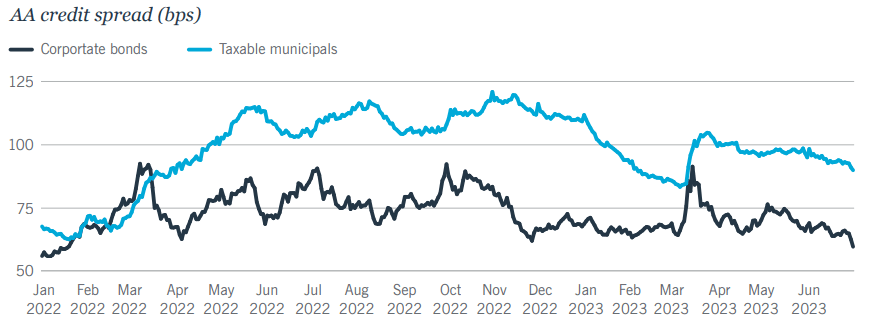

Another positive for taxable munis - and BBN by extension - is how they compare to corporate debt. This is often a more relevant comparison for a fund like BBN than comparing it to tax-exempt munis since income investors want to know how their after-tax yield stacks up. It is a more complicated formula with options that have a different tax status, so a direct look at taxable munis versus corporates can help keep things simple.

In this vein taxable munis win out for the time being. Yield spreads are wider and that could draw investor interest going forward. If it does, BBN has a good chance of pushing higher and/or seeing its discount narrow:

Credit Spreads (AA-rated debt) (Nuveen)

{kind=link}

The differential is a little narrowers for A-rated bonds right now but the positive balance still exists. Given that BBN holds a majority of its debt rated AA or A, this is a tailwind for the fund in my view.

What this shows me is there is indeed value in taxable munis. The question simply is whether or not BBN is the way to play it. With leverage remaining a sore spot for me, I think weighing it carefully against other options (non-leveraged funds or individual issues) could be the safer play.

Reminder: This Is A Cali-Heavy Fund

My last thought is a reminder that BBN is top-heavy with just a few states. The most notable is California, representing over 20% of total fund assets:

State Breakdown (BlackRock)

This means investors in the fund will want to keep a close eye on the Golden State. In recent months this has caused a little bit of volatility (for not just BBN but the muni market as a whole). California, once famous for its surplus, has gone on a spending binge and has faced lower tax receipts due to its over-reliance on high-income residents that saw stock market losses in 2022. The net result has been a switch from surplus to deficit for the fiscal year ahead:

California Budget (Yahoo Finance)

{kind=link}

In order to front-run this, the newly signed budget has a mix of spending cuts, delays, and borrowings to cover the shortfall. This means in the short-term I don't see much risk to muni bonds. Some of these securities are from local or utility backed issuers, so they are not directly at risk from state budgetary problems anyway. But, many are, so this should be at least considered going forward. California is used to dominating the muni market and those bonds tend to have more volatility than others due to the state's tax structure and tendency to make news headlines. The state has a large economy and strong history of paying its dues. But headline risk remains something investors should consider when looking at this sector - and BBN as a result.

Bottom-line

My followers know I am not a cheerleader for any sector/idea/fund. That is why I am often critical of positions I have owned, currently own, or am looking to own in the short-term. In fact, I am perhaps more critical of those options since they will have a direct impact on my personal health!

In this light it is fair to say that BBN, while once a darling of mine, doesn't quite past the muster at this exact moment. I will continue to watch it closely because I favor muni bonds over corporate debt and treasuries and the discount is beginning to look like a level I can't pass up. But leverage has hurt it via income cuts and lack of investor enthusiasm. Those who have been scarred over the past 12 - 18 months may not be in a mood to rush in, and that means the opportunity may be limited for now. For these reasons I believe "hold" is the right call, and I suggest readers approach new positions selectively at this time.

For further details see:

BBN: Investors Continue To Get Punished By Leverage