BBN - BBN: Taxable Munis Continue To Present An Opportunity

2023-03-14 06:48:04 ET

Summary

- BlackRock Taxable Municipal Bond Trust is trading at a sharp discount to NAV, along with one of its sister funds.

- Taxable munis appear safe, as state coffers have seen their "rainy day" funds grow over time.

- The fund's distribution rate remains attractive, albeit the use of leverage continues to put it at risk of another income cut.

- If the current banking crisis prompts the Fed to take a more dovish policy stance going forward, funds like BBN will benefit.

Main Thesis & Background

The purpose of this article is to evaluate the BlackRock Taxable Municipal Bond Trust ( BBN ) as an investment option. This fund offers exposure in taxable municipal bonds, with an objective to "seek high current income, with a secondary objective of capital appreciation."

Over the years, BBN has been my preferred option for exposure to the taxable municipal bond sector. Unfortunately, fate has not been kind to it of late. The broader market (bonds and equities) has been punished over the past 12 - 15 months, BBN was no exception to this. Since my July review , it has dropped along with (mostly) everything else:

Fund Performance (Seeking Alpha)

Because of this, I was tempted to downgrade my forward outlook on the fund. After all it has not been a great performer and more downside could certainly be on the way. However, I believe in the longer term story of BBN and see a relatively high dividend yield as a big asset in this climate. With a banking sector scare that may prompt the Fed to act less aggressively, bond funds like BBN could be ripe for some upside. Therefore, I am keeping the "buy" rating in place and will explain the thought behind it in this review.

Munis Are Still Backed By Cash Reserves

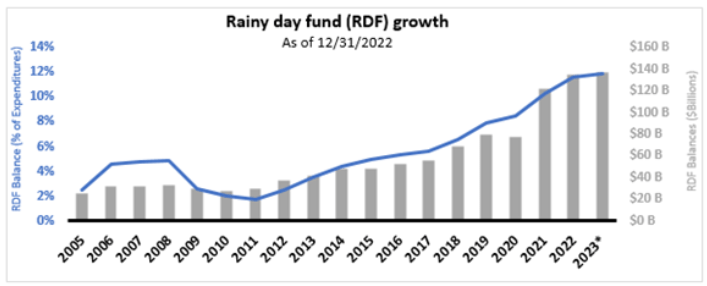

One of the primary reasons I like munis - taxable and tax-exempt - is they continue to offer strong credit quality to investors. Of course, there are varying degrees of quality within the sector like everything else. There are IG bonds, high yield bonds, non-rated bonds, etc. But, on the whole, munis continue to benefit from the perceived improvements in state's fiscal pictures across the country. As an example, "rainy day funds", which is money that state governments have in reserves to use at their discretion, have been increasing steadily over time. In fact, we entered 2023 with these balances being at their highest levels in decades:

State Rainy Day Funds (National Average) (National Association of State Budget Officers)

{kind=link}

To me this speaks to the resiliency of the muni sector. While broader market concerns and the strong likelihood of a recession are pressuring forward credit outlooks, munis are going in to this cycle well supported. Those funds may end up being utilized in the future, but that gives investors plenty of time to prepare for that eventuality and benefit for the time being.

BBN and NBB Both Have Cheap Valuations

Looking at BBN requires consideration of the other taxable muni CEFs in the market today. There is really only one true sister fund from Nuveen, the Nuveen Taxable Municipal Income Fund ( NBB ). But also worth mentioning is the Guggenheim Taxable Municipal Bond & Investment Grade Debt Trust ( GBAB ), which has a heavy allocation to taxable munis as well.

At this juncture, both BBN and NBB offer what is seemingly a pretty good value. BBN has seen its discount to NAV widen considerably since my July article. At that time the fund was trading just under par value, now it sits with a discount over 4%, as shown below:

{kind=link}

In comparison, NBB is even cheaper. While GBAB is the least attractive of the three by this standard, as shown below, respectively:

NBB Metrics (Nuveen) GBAB Metrics (Guggenheim)

{kind=link}

{kind=link}

Given this, I see both BBN and NBB as reasonable options here. I happen to choose BBN for two reasons. One, I already own it and typically prefer to add to current positions rather than start a new position unless there is a compelling reason to do so. A discount spread less than 1% is not "compelling" enough in my opinion. Two, BBN utilizes less leverage than NBB. At time of writing, BBN is 34% leveraged, while NBB is over 39% leveraged.

This is critical going forward because if the Fed does not back off its rate hiking plans and the yield curve remains inverted, leveraged funds are likely to suffer. This has been a sore spot for BBN, and most of the leveraged CEFs I cover. With a distribution cut back in December still a recent memory, followers of this fund are keenly aware of how the climate is impacting this investment theme:

December Income Cut Announcement (Seeking Alpha)

This is something I have touched on in many reviews recently so I won't repeat myself too much here. But suffice to say that leveraged options are getting punished by an aggressive Fed and an inverted yield curve driven by recession worries. If those market trends continue in the months to follow, investors in BBN are not out of the woods. This is a critical risk to keep in mind when evaluating whether this fund is right for you.

Taxable Issuance Has Been Tight

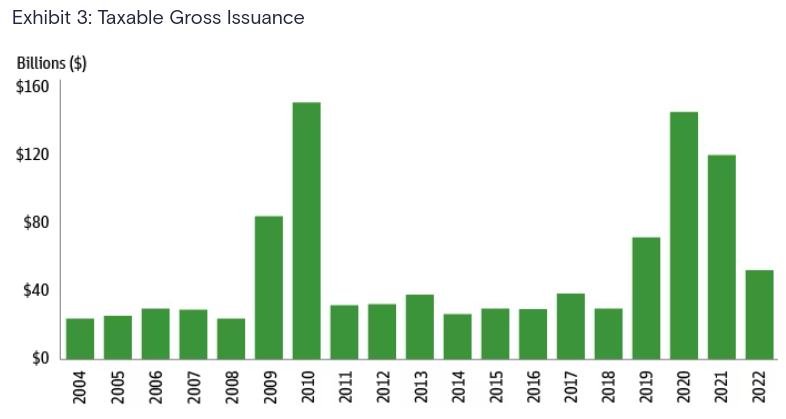

Another aspect the taxable muni sector has going for it is a historically low level of supply. This can benefit current holders of the bonds if supply remains tight - since new investors/buyers will have to "pay up" in order to access this sector. If I expect demand to rise this year (and I do) then front-running this demand by getting in now is the right move.

This extends to BBN because there are only so many ways investors can access this sector. Owning a quality CEF like BBN sets us up nicely for a rebound if demand does rise on the backdrop of this low level of supply:

Taxable Muni New Issuance (By Year) (Goldman Sachs)

{kind=link}

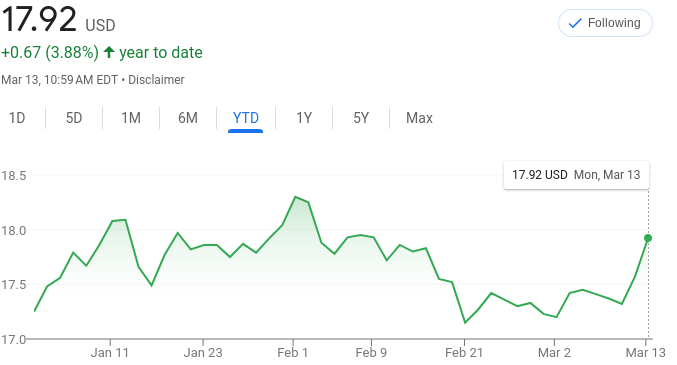

What I take away from this is that taxable munis have seen new issuance decline probably due to higher interest rates. This means that state governments are getting more creative with funding options and are also exercising some fiscal prudence (how long that will last is certainly up for debate!). In the meantime, that suggests to me that BBN can benefit from some of this market scarcity if investors rotate back in to the sector. This is something that has already started happening in early 2023:

BBN's YTD Performance (Google Finance)

{kind=link}

Simply, it is very feasible this performance will continue.

Utility-Backed Bonds Can Be An Inflation Hedge

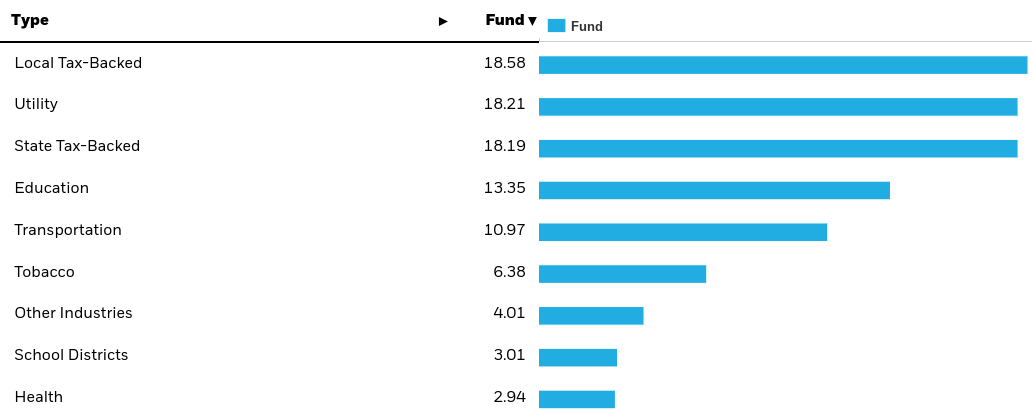

My final point on BBN specifically has to do with the fund's sector holdings. It is largely exposed to state and local government debt, which is something I view favorably because of the rainy day fund backdrop I discussed earlier. But BBN also holds quite a bit of utility-backed bonds, coming in at over 18% of total assets in the portfolio:

{kind=link}

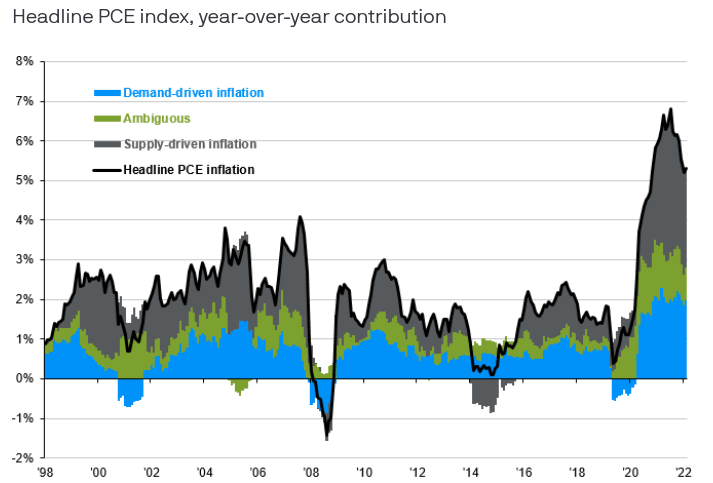

I view this as an asset because utility-backed bonds offer investors a relative inflation hedge. With inflation continuing to be a major pain point for the market, finding even a modest hedge can have a big impact on a portfolio's total return:

PCE Inflation (YOY Change) (St. Louis Fed)

{kind=link}

So, how do utility-backed taxable muni bonds fit in?

Well, for one thing utility companies can often act as a built-in inflation hedge across the board because they are mostly able to hike rates along with inflation. While these increases mostly need regulatory approval, they often get at least some of the increases they want since their agreements with local and state regulators often use inflation as a guideline. In short, when inflation goes up, utility companies are generally entitled to raise rates along with it.

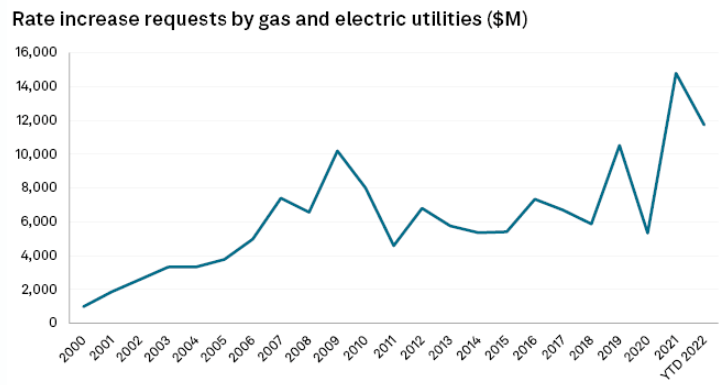

And this is absolutely a theme we have seen in the past few years. Utility requests for higher rates have soared along with inflation:

Rate Increases (Utility Requests) (S&P Global)

{kind=link}

What I conclude from this is taxable munis, and BBN by extension, are at least a partial inflation hedge. While there are many other factors at work here, I see the utility exposure as a net positive.

Bottom-line

BBN has seen a nice tick higher since the year got underway and this is definitely welcomed momentum. Still, readers should approach carefully, since the longer term trend is not as rosy and key headline risks remain. But I do see a path forward that suggests buying in has merit. The fund's leverage is less than its peers, the discount to NAV is wide, and taxable munis have a number of tailwinds broadly speaking. Therefore, I believe a "buy" rating is the right call and I suggest investors give this idea some thought at this time.

For further details see:

BBN: Taxable Munis Continue To Present An Opportunity