BBN - BBN: The Security Of Municipals And A 7.05% Yield

2023-08-04 18:11:18 ET

Summary

- The high rate of inflation in the U.S. is causing the cost of living to rise significantly, putting financial strain on American consumers.

- Investors can consider purchasing shares of closed-end funds specializing in income generation to combat the rising costs.

- The BlackRock Taxable Municipal Bond Trust is one such CEF that offers a 7.05% yield and invests in municipal bonds, appealing to risk-averse investors.

- The fund invests in government securities, which tend to be safer than corporate issues. That might appeal to those investors that are worried about losses.

- The BBN fund trades at a reasonable valuation, but it might be best to wait until it releases its semi-annual report before purchasing shares.

There can be little doubt that one of the biggest problems facing the average American today is the incredibly high rate of inflation that is plaguing the economy. This inflation is causing the cost of living to rise at the highest rate that the nation has experienced in several decades. This is clearly evidenced by looking at the consumer price index, which claims to measure the price of a basket of goods that is regularly purchased by the average consumer. This chart shows the year-over-year rate of change in this index during each month over the past 25 years:

{kind=link}

As we can see here, ever since the pandemic in 2020, the year-over-year change in the consumer price index has been much higher than it was during most of the trailing 25-year period. This has been a major problem for the average person, as wages have not risen nearly as rapidly as the cost of living over the period. As such, the budgets of many households are being pinched. We are even seeing people resort to extreme measures such as dumpster diving and pawning possessions just to get the money that they need to eat their next meal. In short, American consumers are desperately hurting financially right now.

As investors, we are certainly not immune to this. After all, we all need to eat, travel, and heat our homes and workplaces. We might also want to enjoy certain luxuries on occasion. The cost of all of these things has risen significantly over the past two years. Fortunately, we do not have to resort to the extreme tactics that many other consumers have been forced to employ. After all, we have the ability to put our money to work for us to earn an income.

One of the best ways to accomplish this is by purchasing shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are unfortunately not very well followed in the investment media and many financial advisors are somewhat unfamiliar with them. As such, it can be difficult to obtain the information that we would really like to have in order to make an informed investment decision. This is a shame as these funds have a number of advantages over ordinary open-ended or exchange-traded funds. In short, a closed-end fund is capable of employing certain strategies that have the effect of boosting their portfolio yields well beyond that of the underlying assets or indeed pretty much anything in the market.

In this article, we will discuss the BlackRock Taxable Municipal Bond Trust ( BBN ), which is one fund that can be employed to earn an income. The fund's current 7.05% yield is certainly enough to attract the attention of anyone seeking to earn some income from their portfolios and the fact that it invests in municipal bonds as opposed to corporates might appeal to risk-averse investors. I have discussed this fund before, but nearly two years have passed since that time so obviously a great many things have changed. This article will specifically focus on those changes and provide an updated analysis of the fund's finances. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage , the BlackRock Taxable Municipal Bond Trust has the stated objective of providing its shareholders with a high level of current income. This makes a great deal of sense considering that this is a bond fund. As we can clearly see here, the fund's portfolio is entirely invested in bonds:

CEF Connect

The fund has a negative position to cash, which is hardly unusual for a closed-end fund. This comes from the fact that this fund uses leverage as a way to boost its yield, which we will discuss later in this article. The important thing for right now is that the fund is entirely invested in bonds, specifically municipal bonds. The reason why the fund's focus on current income is unsurprising given this is that bonds are by their nature an income vehicle. After all, an investor purchases a bond at face value when it is first issued, receives a stream of interest payments over the life of the bond, and then receives face value back when the bond matures.

In short, the only net investment return provided by a bond is the regular coupon payment. There are no net capital gains over a bond's lifetime because a bond has no inherent exposure to the growth and prosperity of the issuing entity. In the case of a municipal bond, there is no growth or prosperity of the issuing entity anyway because governments do not generate a profit in the same way that a business does.

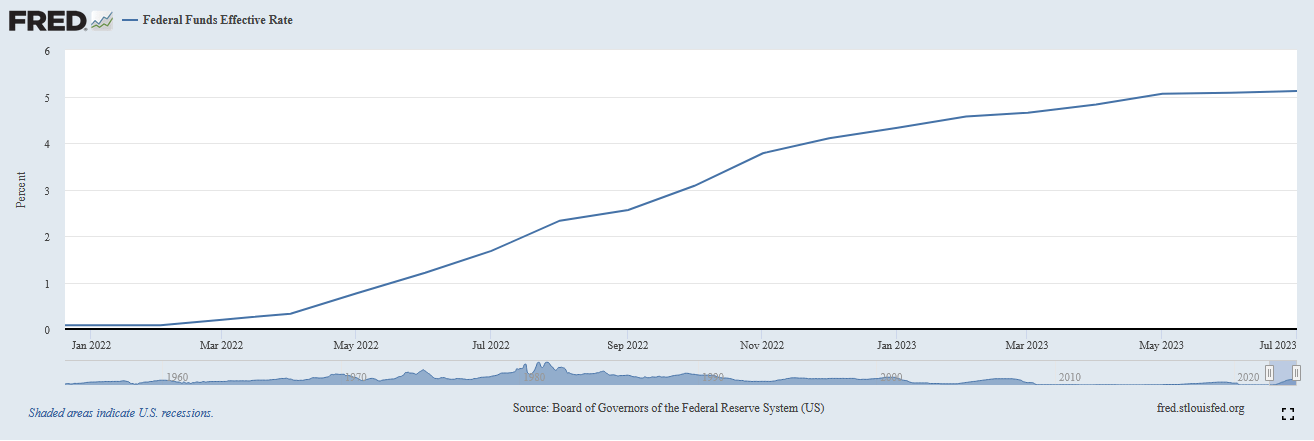

With that said, it is possible to make some capital gains by trading bonds prior to their maturity date and taking advantage of the fact that the market price of bonds changes with interest rates. It is an inverse relationship, so when interest rates go up, bond prices decline. The reverse is also true. This is something that is very important today because the Federal Reserve has been aggressively raising interest rates over the sixteen months in an effort to combat the incredibly high inflation that has been dominating the American economy. As we can see here, the effective federal funds rate has risen from 0.08% in January of 2022 to 5.08% today:

{kind=link}

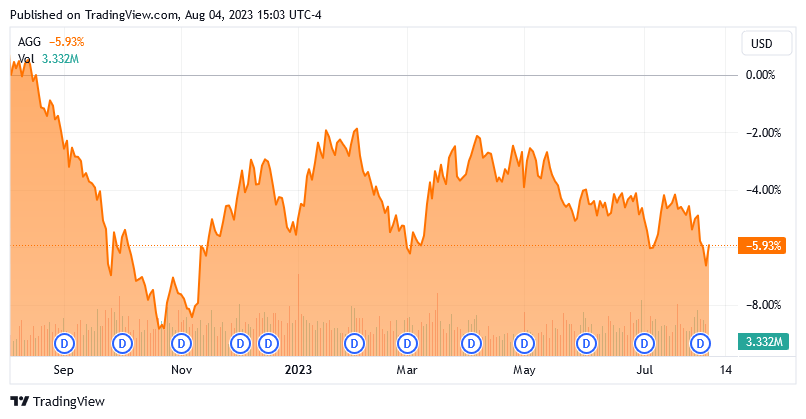

This was one of the most rapid increases in interest rates in history. There were, in fact, a few times last year when the Federal Reserve increased its federal funds target by a full 75 basis points every month. This is triple the historical usual change of 25 basis points. As might be expected, this had a devastating effect on bond prices in the market. As we can see here, the Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 5.92% over the past twelve months:

{kind=link}

The BlackRock Taxable Municipal Bond Trust was certainly not spared from this carnage either. Over the same twelve-month period, the fund declined 19.34%:

{kind=link}

The reason for this decline in bond prices should be fairly obvious. After all, bonds are issued with a coupon that gives them a yield that is competitive with the prevailing interest rate in the market. As such, a bond issued after a series of interest rate hikes will have a much higher yield than a bond that is issued during a period of low-interest rates. There is, therefore, absolutely no reason for anyone to purchase an existing bond in a rising rate environment when they could purchase a brand-new one with otherwise identical characteristics but a much higher yield. As such, the existing bond must decline in price by a sufficient amount to cause it to deliver a similar yield-to-maturity as an otherwise identical brand-new bond.

The bonds that comprise this fund are Build America Bonds, which were a special kind of municipal bond that was issued during the 2009 to 2010 recession. This was the beginning of the long-lasting zero-interest rate environment, so it is a fair bet that all of the bonds held by this fund were issued with a very low yield relative to their face value. Thus, it makes sense that they would be trading for a lot lower than face value today as they need to be competitive with U.S. Treasury securities and high-quality corporates, especially because Build America bonds do not have the same tax advantages as normal municipal bonds.

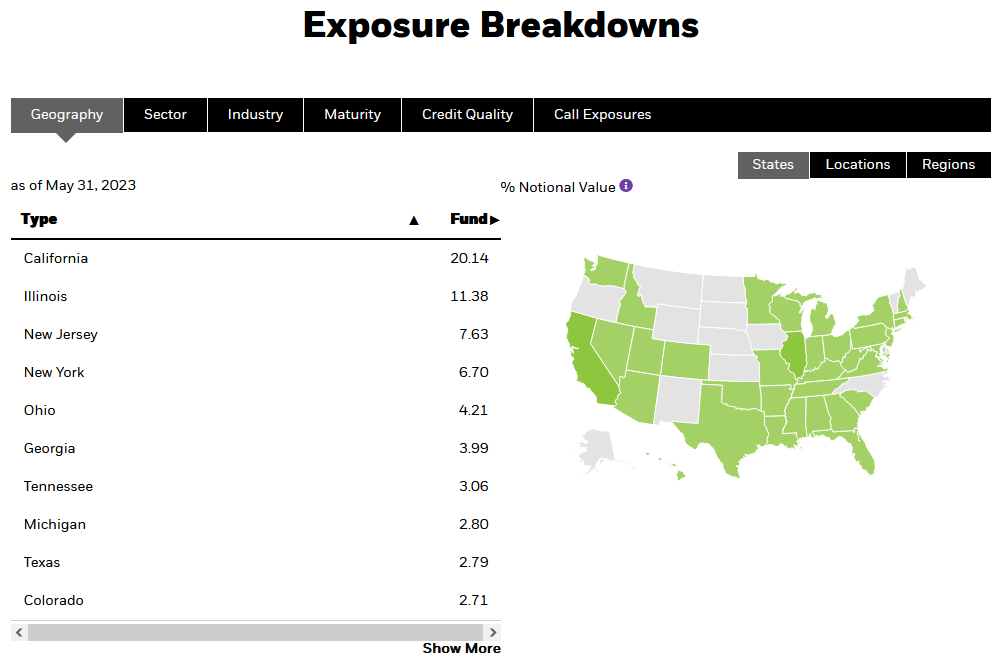

One of the nice things about this fund right now is that it appears to be well-diversified across states and municipalities. We can see that quite clearly here:

{kind=link}

This is somewhat in line with what the fund had the last time that we discussed it, except for its allocation to Illinois increased slightly. The fund also added Tennessee and Colorado bonds to the portfolio while dropping West Virginia and Florida bonds. As we can see, though, the fund does still contain Build America bonds issued by these states, it simply reduced its weighting to them. For the most part, though, we do not see much in the way of changes.

The fact that the fund does not seem to be changing its portfolio by very much even over a two-year period could lead someone to believe that the fund has a very low turnover. This is certainly the case as the fund's annual turnover for the full-year period that ended on July 31, 2023 was only 11.00%. This is a very low annual turnover even by the standards of fixed-income funds, so it is fairly nice to see. The reason why this is nice is that it costs money to trade bonds or other assets, and these expenses are billed directly to the fund's shareholders. This creates a drag on the portfolio's performance and makes management's job more difficult. After all, the fund's managers need to earn sufficient returns to cover the additional expenses and still have enough left over to satisfy the shareholders. That is a challenging task that very few management teams are able to do on a consistent basis.

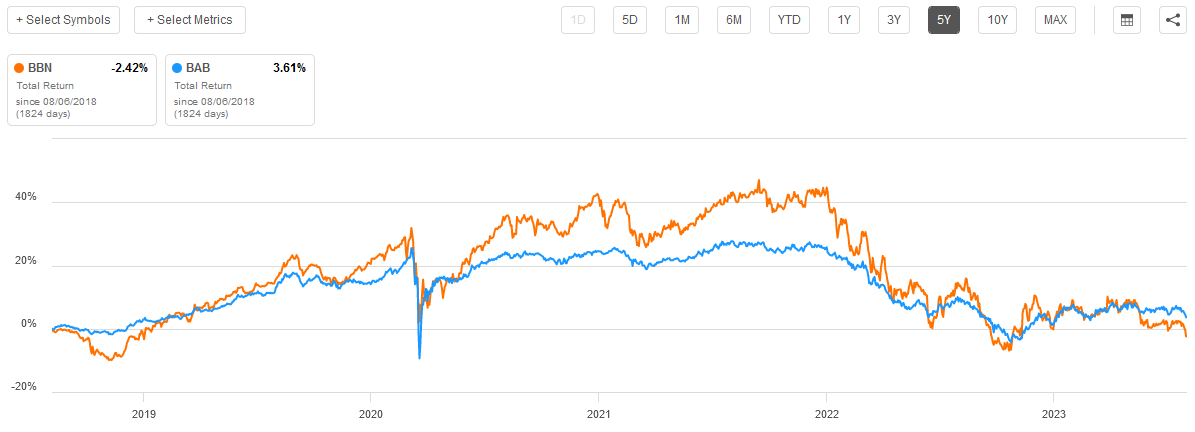

This is one major reason why most actively-managed funds fail to outperform a comparable index fund. This one is no exception to this rule, as it has underperformed the Invesco Taxable Municipal Bond ETF ( BAB ) on a total return basis over the past five years:

{kind=link}

With that said, the difference between the two funds is not as great as we sometimes see. In fact, there were a few periods of time during which the BlackRock Taxable Municipal Bond Trust outperformed the index fund. The BlackRock fund also has a substantially higher yield, which may appeal to some investors.

Leverage

In the introduction to this article, I stated that closed-end funds such as the BlackRock Taxable Municipal Bond Trust have the ability to employ certain strategies that boost their effective portfolio yields beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund borrows money and then uses this borrowed money to purchase Build America bonds and other taxable municipal bonds. As long as the yield of the purchased assets is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

With that said, this strategy is less effective today, with interest rates at 6% than it was at the start of last year, when rates were at 0%. This is because the difference between the borrowing rate and the yield of the bonds is much less than it once was.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This could be one reason why this fund was outperforming the comparable index fund back in the 2020 and 2021 bond bull market. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of assets for that reason. This fund, unfortunately, does not satisfy that requirement today as its leveraged assets comprise 34.73% of the portfolio. While this is above the level that we may like, it is probably not a big deal in this case.

This fund is invested in very low-risk municipal bonds so it can probably carry a bit more leverage than an equity closed-end fund. In addition, the fund's leverage is not very much above that one-third level. As such, its balance between risk and return is probably acceptable today. We do want to keep an eye on it going forward though as we do not want this fund to take on much more leverage.

Distribution Analysis

As mentioned earlier in this article, the primary investment objective of the BlackRock Taxable Municipal Bond Trust is to provide its investors with a high level of current income. In order to achieve this objective, the fund invests in a portfolio of Build America bonds and other taxable municipal bond issues. These securities deliver the lion's share of their total returns to the investors via direct payments. The fund then applies a layer of leverage to artificially boost the yield that it receives from the bonds. The fund then pays out all of the net investment returns that its portfolio generates to its shareholders. As such, we can assume that this fund would have a very high distribution yield.

This is indeed the case, as the BlackRock Taxable Municipal Bond Trust pays a monthly distribution of $0.0929 per share ($1.1148 per share annually), which gives it a 7.05% yield at the current price. The fund has not been particularly consistent with its distribution over the years, as it has increased and cut the distribution several times over its lifetime. In fact, the fund has cut its distribution twice in the past twelve months:

{kind=link}

The fact that the distribution has exhibited considerable volatility over the years is likely to reduce the appeal of this fund in the eyes of those investors that are seeking a stable and secure source of income to use to pay their bills or otherwise finance their expenses. However, it is understandable because the performance of bonds depends heavily on interest rates and they vary over time. We can see this quite clearly in the simple fact that most fixed-income closed-end funds have exhibited considerable variation in their distributions over the years.

It is important to keep in mind though that anyone buying today will receive the current distribution at the current yield. A new buyer will not be adversely impacted by the distribution changes that the fund has implemented in the past. The most important thing for our purposes today is determining how easily the fund can sustain its current distribution.

Unfortunately, we do not have an especially recent document that we can consult for that purpose. The fund's most recent financial report corresponds to the full-year period that ended on December 31, 2022. As such, it will provide us with no insight into the fund's performance so far this year, which is a shame as the bond market has generally been stronger year-to-date in 2023 than it was last year. That strength may have allowed the fund to garner some profits. On the other hand, this report will give us a pretty good idea of how the fund performed over the course of 2022, which was the most challenging environment for bond funds that we have seen in many years. The way that a management team handles a challenging environment can speak more about its skills than how well it does in a raging bull market.

During the full-year period, the BlackRock Taxable Municipal Bond Trust received $316,011 in dividends and $92,259,291 in interest from the investments in its portfolio. This gives the fund a total investment income of $92,575,302 over the full-year period. The fund paid its expenses out of this amount, which left it with $70,324,962 available for the shareholders. That was, unfortunately, not enough to cover the $81,048,591 that the fund actually distributed over the period. This is something that is concerning at first glance since we generally like fixed-income funds to be able to cover their entire distributions out of net investment income.

With that said, the fund does have other methods through which it can obtain the money that it needs to cover its distribution. For example, it might have been able to earn some capital gains by trading bonds and taking advantage of price variations. As might be expected from the challenging bond market of 2022 though, the fund failed at this task. It reported net realized gains of $2,097,099 but this was more than offset by $472,605,404 net unrealized losses. In total, the fund's net assets declined by $439,307,441 after accounting for all inflows and outflows during the period. In fact, the fund did a capital raise of $40,961,004 over the course of the year and this did nothing to stem its overall losses.

This certainly explains why the fund had to cut its distribution twice over the past twelve months. It seems highly unlikely that the fund has managed to earn enough money year-to-date to completely offset this net asset decline, although it may have been able to earn enough to at least cover the distribution at the new level. We need to wait until the fund releases its semi-annual report to know for sure. This should occur within the next few weeks.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Taxable Municipal Bond Trust, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. That is, fortunately, the case with this fund today. As of August 3, 2023 (the most recent date for which data is available as of the time of writing), the BlackRock Taxable Municipal Bond Trust had a net asset value of $17.15 per share but the shares only traded for $15.98 each. This gives the fund's shares a 6.82% discount to the net asset value at the current price. This is in line with the 6.97% discount that the shares have had on average over the past month, so the price looks right today.

Conclusion

In conclusion, the BlackRock Taxable Municipal Bond Trust may be worth keeping an eye on if you are searching for income. The fund invests in government-issued bonds, which tend to be somewhat less risky than corporate issues. That could appeal to anyone that is concerned about losses. The fund also trades at a reasonably attractive discount to the net asset value. The biggest concern here is the sustainability of the distribution at the current level. The fund took some severe losses last year and it almost certainly has not managed to make them up, but it also trades at a lower price and has a lower distribution today. It might be advisable to wait until the fund releases its semi-annual report before purchasing shares. Overall though, this BlackRock Taxable Municipal Bond Trust does have some things going for it.

For further details see:

BBN: The Security Of Municipals And A 7.05% Yield