BBVA - BBVA: Despite 7.5% Yield Its Shares Are A Hold On Valuation (Rating Downgrade)

2023-10-03 06:37:41 ET

Summary

- BBVA has reported positive financial performance and offers a high dividend yield, but its valuation is now fair after a strong share price rally.

- The bank has maintained strong operating momentum, beating EPS and revenue estimates in Q2 2023.

- BBVA's dividend seems sustainable and its current forward dividend yield is about 7.5%, making it a compelling income investment.

BBVA ( BBVA ) has reported a positive financial performance recently and offers a high-dividend yield, but its valuation is now fair after a strong share price rally over the past year.

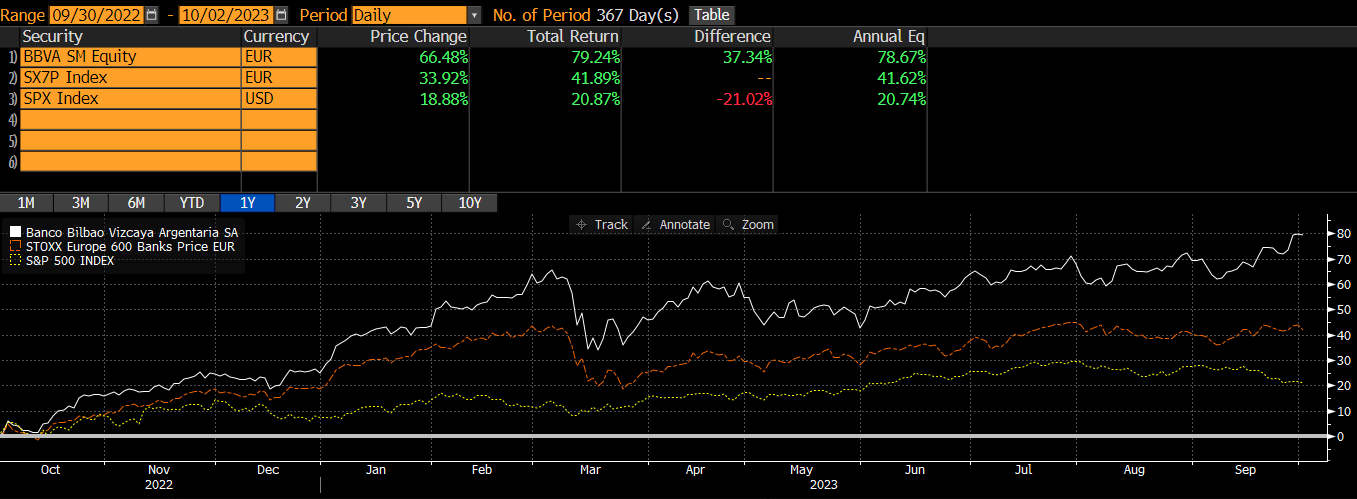

As I’ve analyzed in previous articles , I see BBVA as one of the most attractive banks in Europe, due to a high-dividend yield and relatively attractive valuation considering the bank’s growth prospects and profitability level. However, its stock has been on an uptrend over the past year (white line in the next graph, up by 79% including dividends), clearly outperforming the U.S. market (yellow line, up by 21%) and other European banks (orange line, up by 42%) during this period.

{kind=link}

In this article, I analyze its earnings related to H1 2023 and update its investment case, to see if it remains a compelling income investment or not, after its strong share price run in recent months.

Earnings Analysis

BBVA has maintained a strong operating momentum in the first half of 2023 , supported by rising rates in key markets and its exposure to growth countries, enabling it to beat both EPS and revenue estimates by some margin in Q2 2023.

Earnings surprise (Bloomberg)

Its recurrent net attributable profit amounted to more than €2 billion in the last quarter, an increase of 11% YoY. Due to strong earnings growth, BBVA’s net tangible book value per share increased by 15% YoY, to €8.27 per share, and its return on equity ratio ((ROE)), a key measure of profitability within the banking sector, was 16.2% in H1 2023 (vs. 14.3% in H1 2022).

This positive operating momentum is justified by higher interest rates and loan growth, which led to higher net interest income ((NII)) in its main markets. Its total NII increased to €5.7 billion in Q2 2023, an increase of 25.5% YoY, as the bank is highly geared to interest rates given that some 80% of its revenues are generated from NII. However, there were some currency headwinds in the past few months, and NII at constant exchange rates increased by 37.5% YoY, an even stronger growth rate than its reported NII growth.

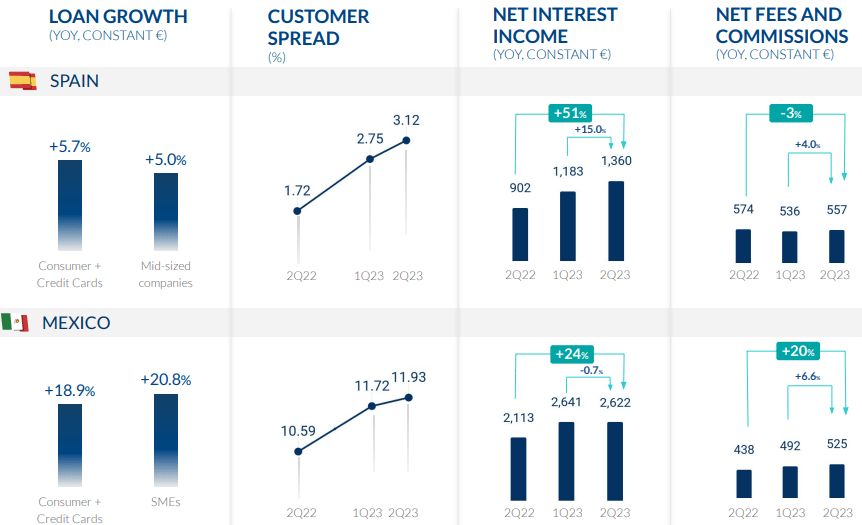

This positive top-line evolution was supported by the bank’s two largest markets, Spain and Mexico, which reported strong loan growth and higher NII due to improved customer spreads. This was particularly significant in Spain (NII +51% YoY in Q2), where a great part of loans are based on floating rates, while on the liabilities side the cost of deposits has not increased much so far, as banks have a lot of liquidity and don’t need to pay for deposits, making BBVA very exposed to higher interest rates (customer spread 3.12% in Q2 2023 vs. 1.72% in Q2 2022).

Key indicators (BBVA)

{kind=link}

Despite strong growth in NII, other revenue lines had a more mixed performance, given that fees and commissions increased by 4.1% YoY to €1.47 billion, but net trading income was down by 35% YoY to only €334 million in the quarter, as higher bond yields led to lower gains from trading. Overall, its total revenues amounted to nearly €7.2 billion in Q2, up by 19.4% YoY.

On the cost side, BBVA remained pressured by the inflationary environment and higher staff costs, leading to cost growth of 11.6% YoY, to €2.9 billion operating expenses in the last quarter. Nevertheless, this cost growth remains below the bank’s revenue growth, leading to positive operating jaws and improved efficiency in the period. Indeed, its cost-to-income ratio, a key measure of operating efficiency in the banking sector, was 40.6% in Q2, which makes BBVA among the most efficient banks in Europe.

Regarding its credit quality, while the economic slowdown, increasing cost of living, and higher interest rates pressuring households and corporates disposable income, its cost of risk has increased marginally over the past few quarters. In Q2 2023, BBVA’s cost of risk ratio was 104 basis points (bps), an increase of 23 bps from the same period of last year.

While this has some negative impact on the bank’s bottom-line, it’s still quite manageable and credit quality remains quite good and doesn’t seem to represent a major threat to earnings growth and profitability in the next few quarters. Nevertheless, due to its high exposure to emerging markets, it’s natural that BBVA’s credit quality may deteriorate faster than other European banks in the near future, which could potentially be the main headwind for further earnings growth in the short term.

Another potential concern is lower interest rates in Mexico, as the central bank has maintained its key rate unchanged in recent months, but the current consensus expect lower rates in the months ahead. Indeed, according to Bloomberg data, the market expects the key rate to drop from 11.25% to some 9% by end-2024, which can put some pressure on NII growth in the medium term.

Nevertheless, BBVA’s guidance is to achieve net income growth in 2024 and have a RoTE ratio in the high teens next year (16.9% in H1 2023), compared to its original goal of some 14%, showing good confidence about its operating outlook over the next year.

RoTE ratio (BBVA)

Regarding its capital position, BBVA’s CET1 ratio was 13% at the end of last June, giving it a comfortable position given that this ratio is well above its capital requirements and its own medium-term target of 11.5-12%. Taking into account this backdrop, it’s not surprising that BBVA has recently started a share buyback program of €1 billion, something that may continue to do in the future if its shares remain undervalued and opportunities for sizable acquisitions don’t arrive.

Management is likely to repurchase shares if valuation remains below book value, while its dividend is also likely to remain on a growing trend as the bank has a good capacity to generate capital organically and its excess capital position is a strong support for a growing dividend in the next few years.

Indeed, BBVA has recently announced an interim dividend of €0.16 per share, an increase of 33% from the previous interim dividend related to 2012 earnings. This interim dividend is expected to be paid on October 11, 2023, while its final dividend is usually paid in April.

According to current street estimates , its total dividend related to 2023 earnings is expected to be around €0.58 per share, representing an increase of 35% YoY. Given that its EPS is expected to be €1.26, BBVA’s dividend payout ratio should be 46%, which is a very conservative level. Therefore, BBVA’s dividend seems to be sustainable given that is well covered by earnings, plus BBVA has a good organic capital generation capacity and a solid CET1 ratio.

Based on this expected dividend per share, its current forward dividend yield is about 7.5%, being higher than when I last analyzed the bank as it was yielding some 6.8% at the time. This yield is quite attractive for income-oriented investors and is above the average of the European banking sector, showing that BBVA remains a compelling income investment.

Conclusion

BBVA has maintained a very positive operating momentum in recent quarters, as the bank is highly exposed to interest rates due to a significant weight of NII in total revenues. However, as most likely the hiking cycle may be over in Europe and there is some potential for rate cuts in Mexico ahead, further significant earnings growth may be difficult to achieve.

Moreover, BBVA stock is currently trading at 0.94x book value, a higher multiple than compared to my last article (0.8x book value) and its own historical average of 0.7x book value over the past five years. Therefore, despite remaining a compelling income investment, BBVA’s shares seem to be fairly valued and I’m downgrading my recommendation to ‘Hold’.

For further details see:

BBVA: Despite 7.5% Yield, Its Shares Are A Hold On Valuation (Rating Downgrade)