BBVA - BBVA Remains An Interesting Income Play

2023-05-17 15:08:41 ET

Summary

- BBVA reported a very good operating momentum, supported by rising interest rates.

- It has an excess capital position and can distribute a good part of earnings to shareholders.

- On top of its 6.8% dividend yield, it’s likely to announce a share buyback program in the coming months.

BBVA ( BBVA ) reported strong earnings recently and offers a high-dividend yield, making it one of the best income play in the European banking sector.

As I've analyzed in previous articles , BBVA is one of my favorite European banks due to an attractive valuation and good income prospects. Since my last article on BBVA back in November, its total return is greater than 38%, thus in this article I analyze the bank's most recent earnings and update its investment case, to see if it's still a good income pick in the European banking sector or if now its shares are fairly valued after a strong run in recent months.

Article performance (Seeking Alpha)

Recent Earnings

BBVA reported strong financial figures in 2022 , supported by a rising interest rate environment and its exposure to growth markets, specifically Mexico, where it has a leading position in the banking market.

Indeed, while more than half of its assets are in Spain (57% in 2022), the region that generates most income is Mexico (43%) due to an above-average profitability compared to other business units. Spain is the second-largest, representing some 24% of gross income, followed by South America (17%) and Turkey (13%).

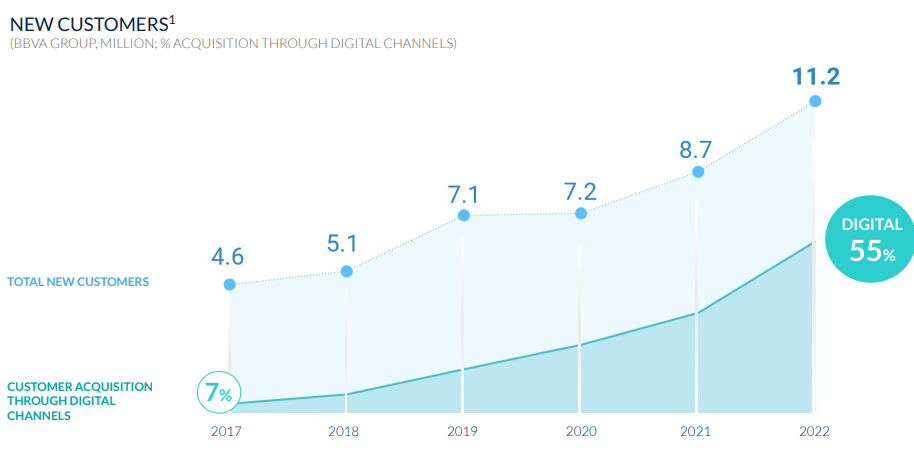

During the last year, BBVA maintained a solid growth path regarding customer acquisition, which is key for sustainable revenue and earnings growth over the long term. It set a new annual record, gaining some 11 million new customers, of which more than half came from digital channels, a big improvement from some years ago showing that the bank's digitalization strategy is bearing fruit.

New customers (BBVA)

{kind=link}

Supported by a growing number of customers and rising interest rates, BBVA's total revenues increased to €24.8 billion (+18.2% YoY), of which net interest income ((NII)) was the major revenue growth driver. Indeed, NII amounted to €19.1 billion, representing some 77% of total revenue, and was up by 30.4% YoY. This big improvement in NII clearly shows that BBVA is significantly exposed to interest rates, which is justified by a large part of its loan book being based on floating interest rates.

On the cost side, BBVA was pressured by the inflationary environment and higher staff costs but was able to grow expenses at a smaller rate than revenues (expense growth of 12.9% YoY vs. 18% for revenues), which led to improved efficiency. Measured by its cost-to-income ratio, its efficiency improved to 43.2% in the last year, being among the most efficient banks in the world.

As credit quality remained strong, provisions and impairment on financial assets remained at similar levels compared to the previous year, its net income increased by 38% YoY to €6.4 billion, and its return on equity (ROE) ratio, a key measure of profitability in the banking sector, was 14.6%.

ROE (BBVA)

During the first three months of 2023 , BBVA maintained a very positive operating momentum, acquiring 2.6 million new customers, achieved loan growth of 9.8% YoY, and core revenues (NII plus fees) were up by 36.7% YoY. NII continues to be supported by rising interest rates, increasing by 43% YoY to €5.6 billion and should maintain a positive trend in the coming quarters.

While total revenues increased by 29% YoY to nearly €7 billion in Q1, its operating expenses also increased by 25% YoY, which means efficiency did not improve that much despite the big increase in revenues. Despite the economic slowdown in recent months, asset quality remained quite good and BBVA's cost of risk ratio was 106 basis points, within the bank's guidance and stable over the previous quarter. Its quarterly profit amounted to more than €1.8 billion, an increase of 39.4% YoY, and its ROE improved to 15.5%.

Going forward, BBVA is expected to maintain a positive operating momentum as the positive effect of rising interest rates is not yet completed, even though further rate hikes have become less likely in recent weeks. I also expect its customers spread gains to moderate in the coming quarters, as the cost of deposits takes some time to reflect higher market rates, plus the recent turmoil in the banking sector has led customers to seek other income alternative to bank deposits. Therefore, BBVA is likely to increase its deposit rates, which will have a negative impact on customer spreads in the near future.

Despite that, according to analysts' estimates , BBVA's revenues are expected to increase to more than €27 billion in 2023 (+10.3% YoY) and its net income should be above €6.8 billion (+3% YoY). This seems to be somewhat conservative and BBVA may be able to beat current expectations, given that BBVA has recently increased its guidance for NII both in Spain and Mexico, while the market seems to be already forecasting some possible rate cuts in the last few months of 2023.

Regarding its capitalization, BBVA has maintained a very solid capital position, a balance sheet profile that is not expected to change much in the coming quarters. At the end of March, its CET1 ratio was 13.1% at the end of Q3, a level that is above its capital requirements and its medium-term target range of 11.5%-12%.

This means that BBVA has an excess capital position, and can therefore return capital to shareholders in a sustainable way. Thus, BBVA is not expected to change much its shareholder remuneration policy in the near term, distributing excess capital to shareholders both through dividends and share buybacks, while small bolt-on acquisitions are possible in a few selected areas, such as fintech.

Capital Ratio (BBVA)

Its last annual dividend was €0.43 per share, considering both its interim and final dividend, which at its current share price leads to a dividend yield of about 6.8%, which is quite attractive for income investors. As the bank has a solid capital position and is increasing significantly its earnings, it's quite likely that its annual dividend will be raised in the coming months, plus a new share buyback program may be announced in the second half of this year, if operating conditions remain resilient in the next few months.

Conclusion

BBVA is a solid bank in Europe with better growth prospects than its peers due to its exposure to growth markets in Mexico, South America, and to some extent, Turkey. While this last country is currently undergoing some political uncertainty, investors should see any share price weakness as an opportunity to buy, as the bank's fundamentals and income appeal are quite strong.

Regarding its valuation, BBVA is currently trading at some 0.8x book value, at a small premium to its own historical average, but considering its improved fundamentals and good income appeal, I still this valuation as warranted, and therefore, BBVA remains an interesting income play in the European banking sector.

For further details see:

BBVA Remains An Interesting Income Play