BBVA - BBVA: Time To Take Profits (Rating Downgrade)

2023-12-30 00:55:40 ET

Summary

- BBVA shares are currently overvalued due to potential interest rate cuts in 2024 and higher loan losses.

- BBVA has outperformed the European banking sector and the S&P 500 index since January 2021.

- The bank's strong performance may not be sustainable due to the cyclical nature of the banking business and changing interest rate environment.

Banco Bilbao Vizcaya Argentaria ( BBVA ) is likely to suffer from interest rate cuts in 2024 and higher loan losses, thus I see its shares as overvalued right now.

As I’ve covered in the past , I have been bullish on BBVA for a long time, especially after its decision to sell the U.S. business in 2021, which led to a strong capital position and very good capital return prospects. Moreover, the bank is highly geared to net interest income ((NII)) which makes it one of the best ways to have exposure to rising interest rates in Europe, plus it offered a high-dividend yield that seems to be sustainable over the long term.

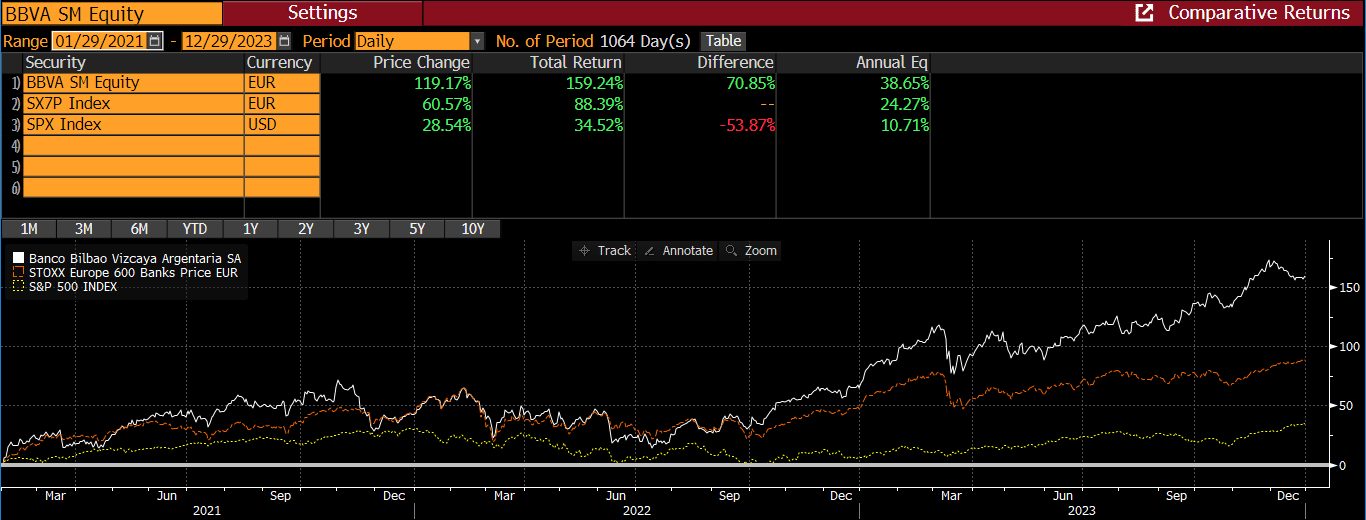

Not surprisingly, BBVA has outperformed the European banking sector since my January 2021 ‘Buy’ recommendation, up by 159% including dividends (white line in the graph), compared to 88% for the European banking sector (orange line) and only 34.5% for the S&P 500 index (yellow line) during the same period.

share price performance (Bloomberg)

{kind=link}

However, despite this strong performance, I took a more cautious view back in October , downgrading my recommendation to ‘Hold’, and now I think it’s time for investors to take profits as the risk-reward profile of its shares is no longer attractive in my opinion.

Investment Thesis

While I consider BBVA to be one of the most attractive banks in Europe, due to a combination of good geographical diversification and exposure to banking markets with good growth prospects, which Mexico is the most important one, investors should take notice that banking is a cyclical business and is highly exposed to interest rates.

The inflationary environment following the pandemic led to higher interest rates across the majority of western economies, being a strong tailwind for revenue and earnings growth in the banking sector. For BBVA, its two most important markets are Mexico and Spain, which together account for 70% of the bank’s total revenues.

Revenue (BBVA)

In Mexico, the central bank has raised its key rate from 4% at mid-2021 to 11.25% in March 2023, having been stable at that level over the past nine months. In Europe, the European Central Bank has raised its key rate from 0% to 4.5%, being stable at this level since last September.

As I’ve analyzed in previous articles , BBVA is one of the European banks more geared to interest rates because NII represents about 80% of the bank’s total revenues, plus most of its loans have adjustable rates. This means that BBVA benefits of higher interest rates both from the production of new loans, but also from its legacy loan book.

Not surprisingly, the rising interest rate environment has been a strong tailwind for NII growth over the past couple of years, increasing from €14.7 billion in 2020 to an expected value of €24.2 billion in 2023, representing an increase of 64% in three years and €9.5 billion in absolute terms.

While costs have also increased somewhat in recent years due to the inflationary environment, cost growth was naturally lower than revenue growth, being a major driver of pre-provision profit growth during this period.

Key operating metrics (BBVA)

Despite higher interest rates and the cost of living crisis over the past couple of years, credit quality has remained quite resilient, which has to a large extent been a surprise for banks and analysts in general. While an economic recession was expected during 2023, this has not happened so far, and excess savings following the pandemic have been a strong support for strong credit quality across the banking sector, of which BBVA has not been an exception.

Indeed, as shown in the next graph, its cost of risk ratio has been relatively stable in recent years, showing that rising interest rates were not a major burden for households and corporates, despite the steep jump in interest rates over the past couple of years.

Cost of risk ratio (BBVA)

This combination of strong revenue growth, manageable cost growth, and stable asset quality, has translated into higher levels of profitability, with BBVA reporting a very significant improvement in its return on tangible equity ratio over the past three years, to 17% over the first nine months of 2023 .

RoTE ratio (BBVA)

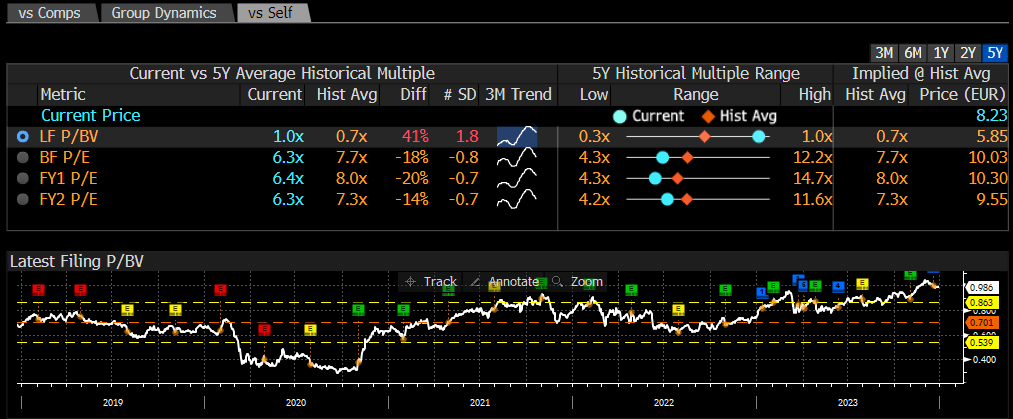

Investors obviously took notice of this strong performance and have pushed the bank’s share price higher, which is justified by strong book value growth during this period (book value of €6.70 per share in 2020 vs. €8.30 in Q3 2023 – up by 23%) and a higher valuation multiple. While investor sentiment toward the banking sector was quite low in 2020, this has improved considerably since then, leading to much higher price-to-book value multiples across the board.

For BBVA, it was trading at a bottom P/BV of 0.3x at the end of 2020, while it has re-rated aggressively to more than 1x book value some couple of months ago.

{kind=link}

While looking at the bank’s recent history, there seems plenty of reasons to like the bank and be bullish, I think investors should not overlook the fact that banking is a cyclical business and the interest rate environment is quite likely to change completely in the near term. This means that BBVA’s share price has likely reached its peak one month ago, given that since then its shares are down by more than 5% as the market is increasingly betting that interest rates will come down during 2024, thus more downside may lie ahead.

Indeed, inflation figures in Europe and Mexico show a clear downtrend trajectory over the past few quarters, and the market is already expecting rate cuts in Mexico next January. Current estimates is for the Mexico key rate to be at 9% by the end of 2024, some 225 basis points (bps) lower than its current level. In Europe, interest rate cuts are only expected in Q2 2024, while the market expects the ECB key rate to be at 3.75% by end-2024, or 75 bps lower than its current level.

Despite these rate cuts expectations, current consensus expect the bank’s NII to grow in 2024, to €24.6 billion (up 1.7% vs. 2023). This doesn’t seem to make much sense in my opinion, as I also expect interest rates to come down during the next year, thus there is clearly a good margin for street estimates to come down, which will be a headwind for BBVA’s share price in the coming months.

Another factor that may also lead to lower earnings and put pressure on valuation and share price is credit costs, as the cost of risk ratio increased by 20 basis points in 2023, and is quite likely to maintain an upward trajectory in 2024. While credit quality has remained strong in the recent past, there is usually a time gap between interest rate hikes and higher loan defaults (around eighteen months), thus the negative impact of higher interest rates on the bank’s loan quality is likely to really start to kick in the next few quarters.

Regarding this view, the market seems to agree, given that current estimates expect an uptick in provisions for loan losses in 2024, from €4.4 billion in 2023 to more than €5.2 billion in the coming year. This is an increase of 18% YoY and will impact BBVA’s bottom-line by some €800 million, putting pressure on its net income and RoTE level.

Due to the combination of lower revenues, higher loan losses, and a declining RoTE, I also expect its valuation multiple to reverse to its mean over the past five years, at around 0.7x book value. Given that current consensus expect its book value per share to remain relatively stable at €8.40 in 2024, this leads to a valuation of about €6 per share by end-2024, or 28% below its current share price.

One final note about its dividend , which was also a main reason why I was bullish on the bank in the past, it currently offers a dividend yield of 5.7%, compared to 7-8% in the past. While this yield is still good, it’s no longer much higher than the European banking sector average, being another sign that BBVA’s share are no longer undervalued and from an income perspective there are better alternative within the European banking sector.

Conclusion

While BBVA is a solid bank in Europe and has performed quite well over the past three years, the prospects of lower rates ahead and higher credit losses should be important tailwinds for its NII and earnings growth in 2024. The market is not yet discounting this view on its share price, but in my opinion there is more downside risk than upside potential, and therefore investors should take profits after a very strong share price rally over the past three years.

For further details see:

BBVA: Time To Take Profits (Rating Downgrade)