ENB - BCAT: Best To Watch From The Sidelines For Now

Summary

- BlackRock Capital Allocation Trust invests in a blended portfolio of stocks and bonds in an attempt to maximize total return and current income.

- The closed-end fund is likely to struggle to generate capital gains in the current environment, so income will be most of its returns.

- The portfolio is quite decent and includes a few asset classes that we may not expect.

- The fund failed to cover its distribution in 2021 or YTD in 2022, so it may be forced to cut in the near future.

- The fund is currently trading at a very attractive price that appears to indicate a market belief that a cut is coming.

One of the biggest problems faced by many Americans today is the high rate of inflation that has been pervading the economy. This has forced many people to seek out additional sources of income, such as a second job, simply to obtain the money that they need to keep their bills paid and food on their tables. Fortunately, as investors, we have other means that we can employ in order to obtain the additional income that we need to maintain our lifestyles. One of the best of these methods is to purchase shares of a closed-end fund ("CEF") that specializes in the generation of income. These funds are nice because they provide an easy way to obtain a diversified portfolio of assets that can employ certain strategies to generate higher yields than pretty much anything else in the economy.

In this article, we will discuss the BlackRock Capital Allocation Trust ( BCAT ), which is one CEF that can be used by investors for this purpose. This fund yields a very impressive 8.95% at the current price, which is certainly enough to turn anyone's head. The fund is trading for a very attractive valuation right now, so let us investigate and see if it could be a good addition to a portfolio today.

About The Fund

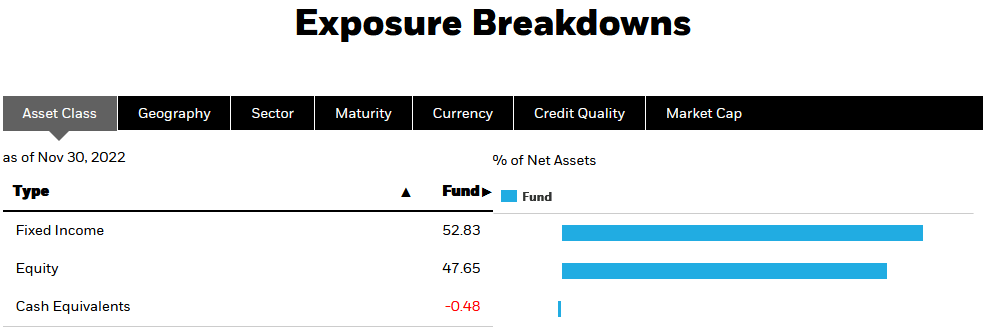

According to the fund's webpage , the BlackRock Capital Allocation Trust has the stated objective of providing its investors with a high total return and current income. It seeks to do this through the use of current income, current gains, and long-term capital appreciation. This is not an unusual objective for a closed-end fund as most of them have somewhat similar objectives. However, normally we see this objective for an equity fund, not a blended fund like this one. As we can see here, the fund is invested in both fixed-income securities and common stocks, although its fixed-income position is larger than the common stock one:

{kind=link}

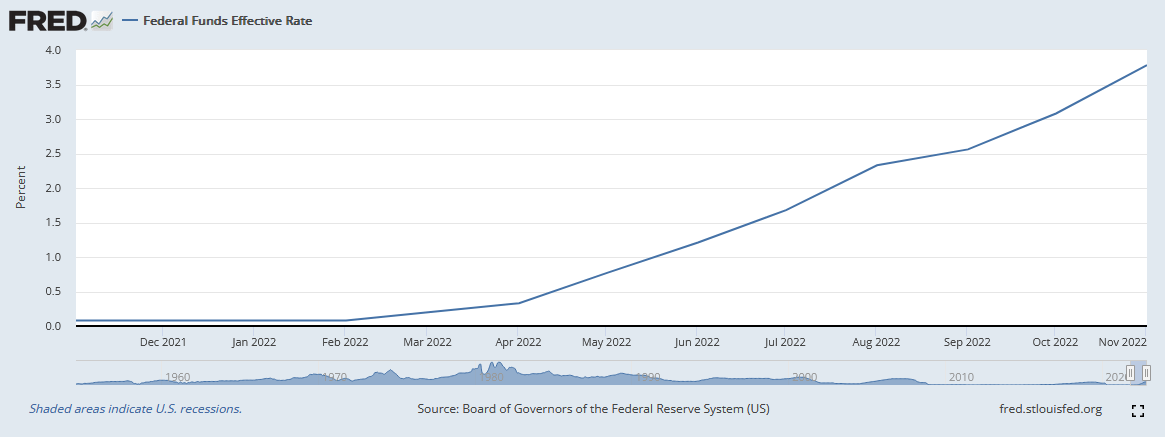

This could, unfortunately, reduce the fund's ability to generate capital gains. This is because bonds do not have very much potential for it because their prices are not linked to the growth and prosperity of the underlying business. After all, a company does not pay its creditors more money just because its profits increased. Bonds instead are priced inversely to interest rates. Therefore, when interest rates rise, bond prices fall, and vice versa. There is a limit as to how far interest rates can go though since nobody will willingly make loans at negative rates since that means that the lender is essentially paying the borrower to take money. This concept puts an effective cap on the level that bond prices can reach. As everyone reading this is no doubt well aware, the Federal Reserve has been very aggressively raising interest rates over the course of this year in order to combat the high level of inflation permeating the economy. We can see this clearly by looking at the federal funds rate. Back in February 2022, the federal funds rate was at 0.08% but today it is at 3.78%:

{kind=link}

This has caused bond prices to fall. In fact, as of the time of writing, the Bloomberg U.S. Aggregate Bond Index is down 13.23% year-to-date. The central bank has implied that it will continue to raise rates as necessary until inflation is back down to its goal of 2%. As I stated in a recent blog post , this will require rates much higher than today's level. Thus, it seems likely that bonds will not really see any price increases in the near future.

Therefore, all of the fund's capital gains in the near future will likely come from its stock positions. Unfortunately, other than the energy sector, capital gains have been quite hard to come by. The S&P 500 Index ( SP500 ) is down 20.31% year-to-date as of the time of writing and the NASDAQ 100 ( NDX ) is down 33.61%, which is largely due to the Federal Reserve's interest rate hikes. This is a direct effect of the market becoming addicted to the easy money policy that has dominated most economies over the past decade. As the Federal Reserve is unlikely to reduce rates in the near future, we likewise should not expect much in the way of gains here.

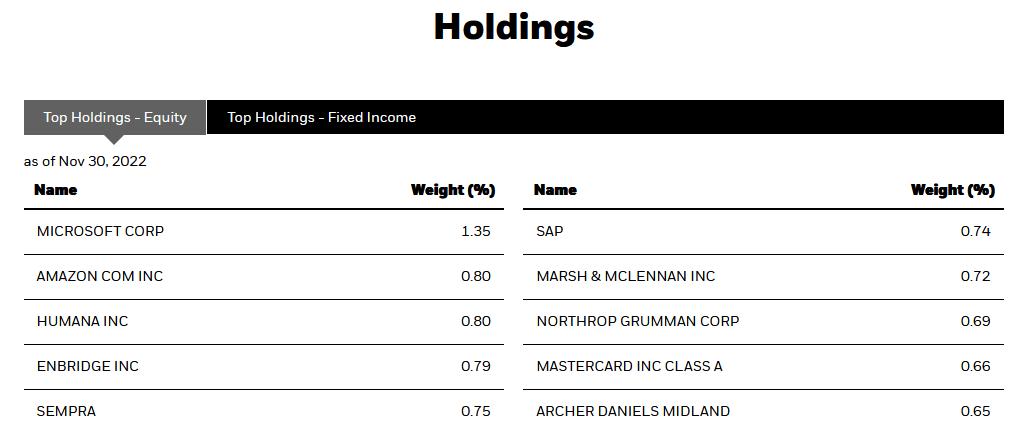

The fund will therefore likely be generating most of its returns just from the direct payments that it receives from the dividend stocks and bonds in its portfolio. From this perspective, the largest positions in it make a certain amount of sense. Here they are:

{kind=link}

With the notable exception of Amazon ( AMZN ), all of the stocks that are listed here pay a dividend. Unfortunately, many of them do not really have a particularly high yield. The notable exception here is Enbridge ( ENB ), which has long been a favorite of dividend investors because of its stable cash flows and high yield. In fact, that stock yields 6.83% as of the time of writing. Enbridge's market price is also basically flat year-to-date so it is outperforming the market as a whole. Sempra ( SRE ) is another very attractive holding right now as the utility is up an impressive 16.87% year-to-date and boasts a 2.92% dividend yield. The solid performance of these companies has helped to offset the weak performance of Microsoft ( MSFT ) and Amazon and overall, this portfolio looks quite reasonable as we head into a bear market dominated by soaring food and energy prices.

As my regular readers on the topic of closed-end funds are no doubt well aware, I do not usually like to see any individual position in a fund account for more than 5% of the fund's portfolio. That is because this is approximately the level at which an asset begins to expose the portfolio to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification but if an asset accounts for too much of the portfolio, then it will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market does not, and if it accounts for too much of the portfolio then it may end up dragging the entire fund down with it. As we can clearly see above though, this does not appear to be something that we really need to worry about here. There is no asset that accounts for an outsized proportion of the portfolio and it does appear quite reasonably diversified.

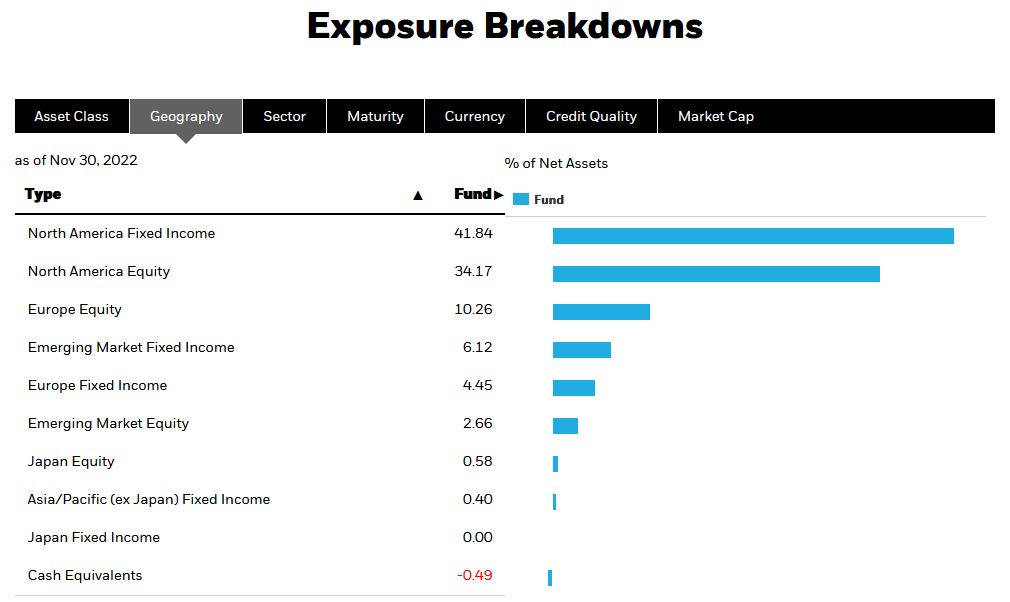

A look at the largest positions in the fund may lead one to think that the fund is heavily invested in the United States. After all, with the exception of Enbridge and SAP SE ( SAP ), all of the fund's positions are in American companies. However, nothing could be further from the truth. In fact, 23.99% of the fund is invested outside of North America:

{kind=link}

This is nice because of the protection that it provides us against regime risk. Regime risk is the risk that some government or other authority will impose a policy or take some other action that has an adverse impact on a company in which we are invested. The only real way to protect ourselves against this risk is to ensure that only a relatively small percentage of our assets are invested in any given country. This fund does this to a degree, although it is still more weighted toward North America (the United States and Canada) than I would really like to see. As such, it might make sense to ensure that the rest of your portfolio is properly internationally diversified before making an investment in the fund.

One thing that is nice to see is that this fund is invested in fixed-income securities from emerging markets, even if these do only constitute 6.12% of the portfolio. The presence of these securities makes this one of the few funds that are invested in this area of the market, which is nice because emerging markets have some advantages over developed ones. In particular, the debt levels of many emerging countries are substantially lower than those of developed nations. For example, the United States currently has a national debt-to-GDP ratio of 121.85% but many emerging markets are well below 40%. This should reduce the default risk of these securities somewhat. In addition, most emerging nations have higher interest rates than the developed nations of North America and Europe so the presence of these securities provides the fund with higher income than it could obtain by investing the same amount of money into developed-nation fixed-income securities. Naturally, the more income the fund receives, the better off we are as investors in the fund.

Leverage

As stated in the introduction, the BlackRock Capital Allocation Trust has the ability to employ certain strategies that have the effect of boosting its yield beyond that of any of the underlying assets. One of these strategies is the use of leverage. Basically, the fund is borrowing money and using that borrowed money to purchase stocks and fixed-income assets. As long as the return that it receives from the purchased assets is higher than the interest rate that it needs to pay on the borrowed funds, this strategy works pretty well to boost the yield of the overall portfolio. As the fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of leverage is a double-edged sword because it increases both gains and losses. This is something that is pretty important right now because both stocks and fixed-income securities are likely to decline for a while due to the Federal Reserve's monetary tightening policy. We discussed this over the course of this article. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I do not typically like to see a fund's leverage exceed a third of its assets for this reason. Fortunately, the BlackRock Capital Allocation Trust fulfills this requirement. Its levered assets currently comprise only 5.17% of the portfolio. Thus, the fund is clearly exercising discretion with its leverage, which is a very good thing in today's market.

Distribution Analysis

As mentioned earlier in this article, the BlackRock Capital Allocation Trust has the stated objective of providing its investors with a high level of total return and current income, although right now its capital gains are likely to be limited. It does this by lightly leveraging up a portfolio of dividend stocks and fixed-income securities so we can expect that it will have a respectable distribution yield. This is certainly the case as the fund currently pays out a monthly distribution of $0.1041 per share ($1.2492 per share annually), which gives the fund an 8.95% yield at the current price. This fund only has a short history, but it has been quite consistent about its distribution over the period:

{kind=link}

This overall consistency is something that will certainly appeal to those investors that are seeking a stable and secure source of income with which to pay their bills. However, 2021 was a much stronger year than 2022 for both common stocks and fixed-income so the fund likely had an easier time paying its distributions last year than it did this year. We can see this in the fact that the fund has been making numerous return of capital distributions this year, which may be a bit concerning:

{kind=link}

The reason why this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors' own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be considered a return of capital, such as the distribution of unrealized capital gains. As such, we should investigate to ensure that the fund can actually afford the distributions that it is paying out to its shareholders.

Fortunately, we have a fairly recent document that we can consult for this purpose. The BlackRock Capital Allocation Trust's most recent financial report corresponds to the six-month period ending June 30, 2022. As such, it should give us a pretty good idea of how well the fund handled the volatile market during the first half of this year, which is the time period during which the Federal Reserve began to tighten its monetary policy. During the six-month period, the fund received a total of $11,693,411 in dividends and $35,717,007 in interest from the assets in its portfolio. When we combine this with a small amount of income received from other sources and net out foreign withholding taxes, the fund had a total income of $46,900,235 during the six-month period. The fund paid its expenses out of this amount, leaving it with $29,314,837 available for the shareholders. This was, unfortunately, nowhere close to enough to cover the $69,619,147 that the fund actually paid out in distributions during the period.

However, the fund does have other methods through which it can obtain the money that it needs to cover its distributions. The most important of these is capital gains. As might be expected, however, the fund failed miserably at this task during the first half of the year. The BlackRock Capital Allocation Trust reported net realized losses of $2,689,416 and suffered another $364,515,241 in net unrealized losses. Overall, the fund's assets declined by $423,874,841 after accounting for all inflows and outflows during the half-year. This is certainly concerning but the fund may still be okay if it managed to offset this during the strong market in 2021. That was also not the case as the fund's assets declined by $18,711,885 during the full-year 2021 period after accounting for all inflows and outflows. This is certainly concerning as the fund is clearly failing to cover its distribution even during raging bull markets like we saw in 2021. It appears that the fund may have to cut its distribution in the very near future.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Capital Allocation Trust, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current value of all of the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. That is fortunately the case with this fund today. As of December 22, 2022 (the most recent date for which data is available as of the time of writing), the BlackRock Capital Allocation Trust had a net asset value of $16.89 per share but the shares only trade for $13.78 per share. That gives the shares an impressive 18.41% discount to net asset value. This is quite a bit more attractive than the 15.93% discount that the shares have traded at on average over the past month and could be a sign that the market expects this fund to have to cut its distribution. Overall, though, the price certainly appears to be right here.

Conclusion

In conclusion, the BlackRock Capital Allocation Trust may struggle in the current market environment. It is unlikely to see much in the way of capital gains from either the fixed-income or the common stock portions of its portfolio for a while. As the fund is failing to cover its distribution even in strong bull markets like 2021, it may also be overdistributing. This is a very clear sign that anyone buying today could expect a near-term distribution cut. However, the BlackRock Capital Allocation Trust's price is very reasonable right now, so it appears that the market is pricing such a cut in. Overall, though, I'd watch this one from the sidelines for the time being.

For further details see:

BCAT: Best To Watch From The Sidelines For Now