LVMHF - BCAT: Highly Diversified Fund Trading At An Attractive Discount

2023-06-07 12:50:19 ET

Summary

- BlackRock Capital Allocation Term Trust continues to trade at an attractive discount and offers a diverse investment portfolio.

- The fund has seen improved performance in 2023, but its increased distribution may not be warranted based on its prior-year performance.

- BCAT remains a compelling option for long-term income investors due to its attractive discount and potential for diversification.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 24th, 2023.

BlackRock Capital Allocation Term Trust ( BCAT ) continues to trade at a deep and attractive discount. Since our last update, the fund's discount has essentially stayed flat. That said, a fairly recently upped distribution seems to have moved the needle some on keeping the fund's discount from widening further.

This multi-asset fund can invest in just about anything, anywhere and at any time. This includes flexibility to utilize both leverage and options, among other derivative contracts.

Performance since our prior update in February 2023 shows that the fund's share price returns have slightly declined. When factoring in the distributions, the total return results show a slight positive - similar to what the broader market has done during this time.

BCAT Performance Since Prior Update (Seeking Alpha)

I believe that the fund remains an attractive buy at this time. As it is such a diverse fund, it could be seen as a sort of one-stop shop to add tons of diversification for an investor. They list 840 positions total, with some of those holdings being ETFs and some securitized debt means there could be exposure to thousands of underlying individual investments.

The Basics

- 1-Year Z-score: 1.85

- Discount: -11.20%

- Distribution Yield: 10%

- Expense Ratio: 1.45%

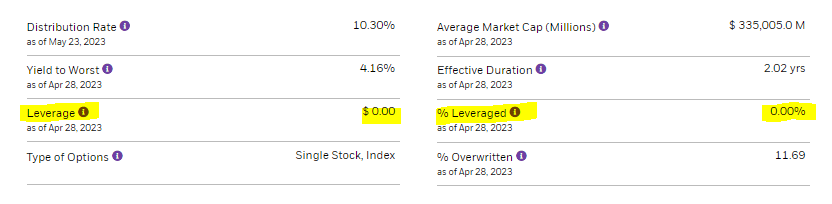

- Leverage: 0%

- Managed Assets: $1.841 billion

- Structure: Term (anticipated liquidation date of September 25th, 2032)

BCAT's investment objective is "to provide total return and income through a combination of current income, current gains and long-term capital appreciation."

To meet their objective, they simply "invest in a portfolio of equity and debt securities." They add a bit more color with, "the Trust may emphasize either debt securities or equity securities." Along with this, they will "utilize an option writing strategy in an effort to generate gains from options premiums and to enhance the Trust's risk-adjusted returns." The fund is overwritten by 11.69% currently, which could indicate that the managers are bullish.

While the fund shows no leverage at this time, they have the flexibility to incorporate leverage when they see an opportunity. That will increase the expense ratio, and they have employed leverage within the last year. Therefore, that's why we see an interest expense of 0.15% listed, which would bring their total expense ratio up to 1.60%. This also includes 2 basis points of acquired fund fees and expenses.

This is a bit on the higher end, even when excluding leverage. However, multi-asset funds that can invest anywhere and everywhere often see higher expenses in general.

{kind=link}

Performance - Attractive Discount

While the fund's discount remains attractive, it has shrunk a bit on a YTD basis. This could still be considered a newer fund and, thus, a fund that hasn't really found its range yet in terms of its discount/premium.

This reduction in discount more recently has come from the fund's share price outperforming the NAV. However, the fund's NAV has been moving in the right direction as well. Helping out the share price could be the overall market moving higher as they hold some exposure to the mega-cap growth names. Additionally, potentially Saba's involvement could be at play as they are holding a position in this fund. For the most part, this was a halfway decent performance too. It isn't beating the S&P 500, but only a handful of mega-cap tech names are largely supporting the broader markets.

BCAT holds exposure to several of those market leaders, so it has also benefited from that. Additionally, BCAT is about a 50/50 split between equities and fixed-income. So quite different from what you would get if you invested in something like ( SPY ).

Ycharts

It would seem that the fund's discount was attractive and getting quite extended when it was pushing near an 18% discount. That's where it was near when we covered the fund in the fall of 2022.

Besides just being at an overall deep and compelling discount, keeping the discount firm instead of dropping further yet again could have been the upped distribution. Additionally, BlackRock has been fairly aggressive in repurchasing shares of BCAT, at least in the fourth quarter of 2022 . During the first quarter of 2023, they weren't listed as having bought back any shares for BCAT. Stanford Chemist's article goes into more detail on those share repurchases for their other funds.

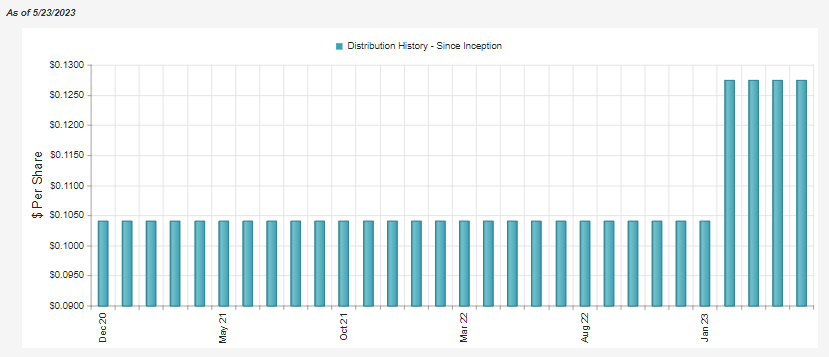

Distribution - Bump Provides Lift, But Comes With Downside

The increase that could have been the catalyst for potential discount contraction comes with some pros and cons.

{kind=link}

Distribution increases are often quite exciting, but with CEFs, they can essentially pay out what they want for however long they want to. This is because they can utilize sources of income, capital gains and return of capital - which includes both good and bad ROC. Given the challenge that this fund and the broader market had in 2022, a raise into this year seemed fairly unwarranted. To be fair, though, the fund has been off to a better 2023 and could technically be considered to be covering the distribution. This would be measured by an increase in the NAV from $16.89 to start off the year to $17.12 with the latest close.

Since the fund's still at a deep discount, the distribution rate comes to 10%. That's well ahead of the NAV yield of 8.88%.

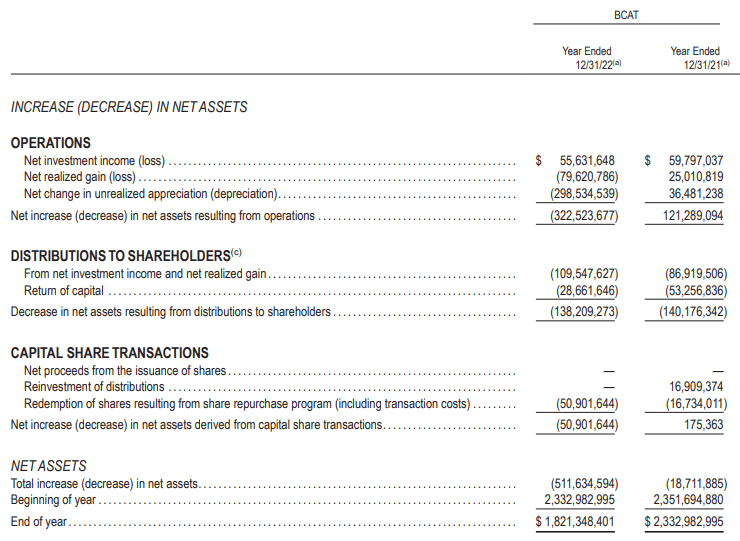

A further reason the fund's distribution seemed to have gotten an unwarranted raise was that net investment income even slipped year-over-year in the fund's last annual report . They had even employed around $688 million in leverage through some of last year. This means they deleveraged down to zero, indicating that NII could fall further, all else equal.

{kind=link}

Add it together, and this means that the increase in the distribution will require even more capital gains to fund the payout. That isn't that uncommon for a fund with heavy equity exposure. However, I believe that the main takeaway is that they likely upped the payout to get a discount contraction and not because they believe it can be covered.

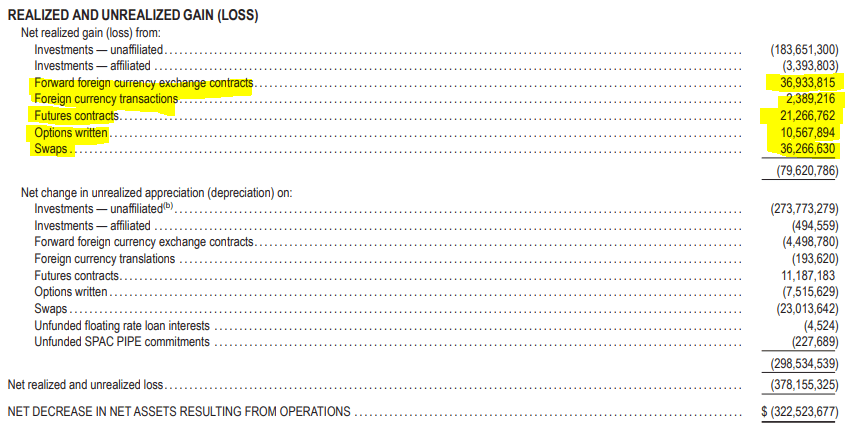

In our prior update, we touched on the fund's sources of appreciation and depreciation, both realized and unrealized. This is an important factor for BCAT because, as I mentioned, they can invest in any derivative contracts they want. We saw realized gains in each of these categories in the last fiscal year. That would have helped offset the realized and unrealized losses - which were substantial - in the fund's underlying portfolio.

Unfortunately, some of these realized gains were also offset by losses in the corresponding unrealized basket. For example, swaps contributed to around $38.267 million in gains, which were offset by the $23.014 million in unrealized swaps. Futures contracts were the only type of derivative that showed both realized and unrealized gains that contributed to minimizing the fund's downside.

BCAT Realized/Unrealized Gains/Losses (BlackRock (highlights from author))

{kind=link}

This is important to highlight for the fund's distribution coverage because these gains in derivatives are just as good as gains in their underlying portfolio when it comes to covering the payout to shareholders.

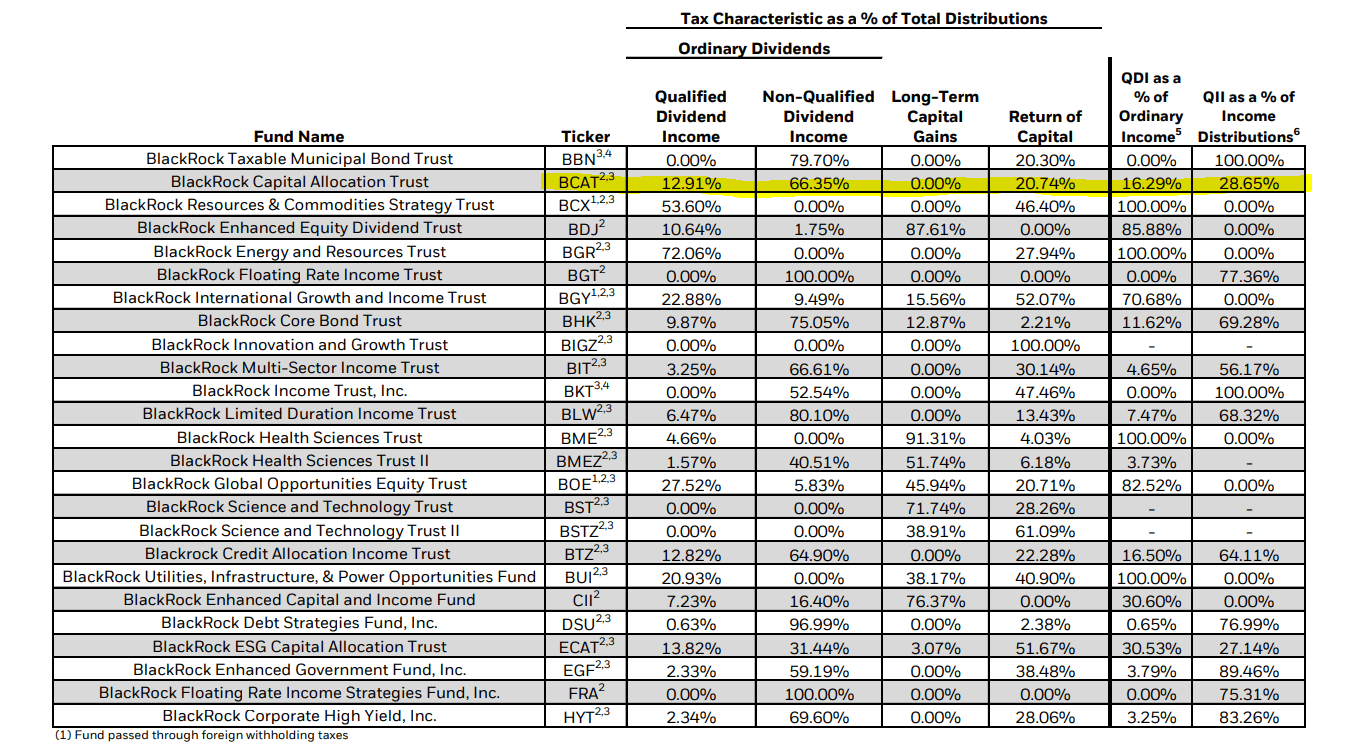

2022 saw the fund's distribution tax classification as mostly non-qualified dividend income. That could indicate the fund isn't so tax-friendly and could be best held in a tax-sheltered account. Given the sizeable exposure to fixed-income investments that pay interest payments, this could be the case going forward. However, we also have ROC identified, which is a way to defer tax obligations as it reduces an investor's cost basis. If the fund is successful, long-term capital gains would likely also show up.

{kind=link}

The breakdown going forward is likely to change materially, and hard to predict year to year for the reasons listed above. Overall, that makes this fund a bit difficult to determine which would be more appropriate in general.

BCAT's Portfolio

The fund is fairly evenly split between equity and fixed-income investments at this time. Despite listing no leverage, the fund has a negative cash equivalent balance. This was consistent when we last looked at the fund. However, this is a higher weighting to equity investments than we saw last year . Around a year ago, we actually saw nearly 58% in fixed income, with around 45% in equities.

{kind=link}

With this change, it would seem as though when they were deleveraging that they were undoing their fixed-income investments. Additionally, equities performance would have been better, which could have also contributed to a higher weighting. While that is the case, the fund is still highly diversified. It could be considered slightly more aggressive now, and management appears to be more bullish on equities than they were previously.

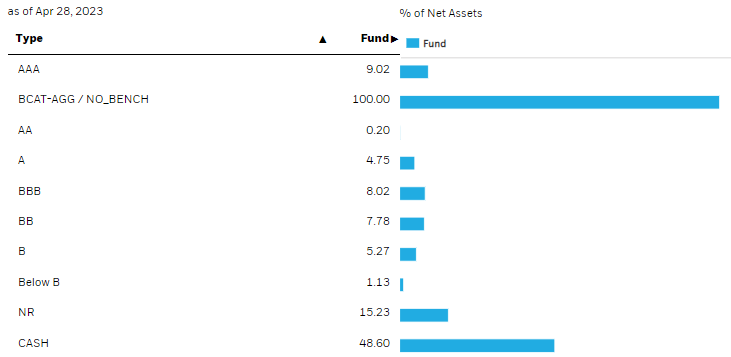

On the debt side of their portfolio, reflecting the overall flexibility and diversification of the fund, we can see that it is split amongst different credit qualities. That includes not rated.

{kind=link}

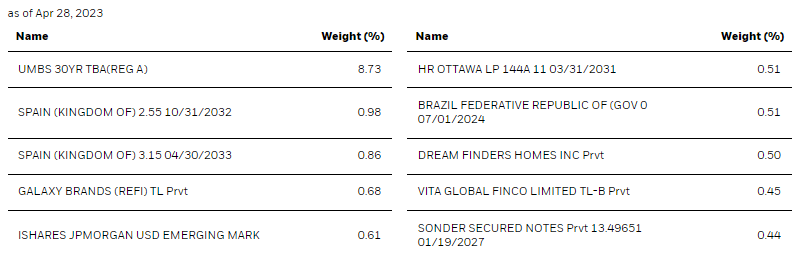

When looking at the largest fixed-income investments, we even see the iShares JPMorgan USD Emerging Markets Bond ETF ( EMB ). That's one of those holdings that represent even further diversification as it contains 606 holdings within that ETF. At a weighting of only 0.61% for BCAT, each underlying position certainly carries a negligible amount of exposure on its own.

{kind=link}

The largest holding for the debt sleeve belongs to the UMBS 30-Year TBA ( to-be-announced .) At a near 9% weighting, that's substantially larger than anything else the fund carries - even on the equity sleeve. However, an MBS is going to be backed by a bundle of mortgages, meaning hundreds or thousands of different loans pooled together.

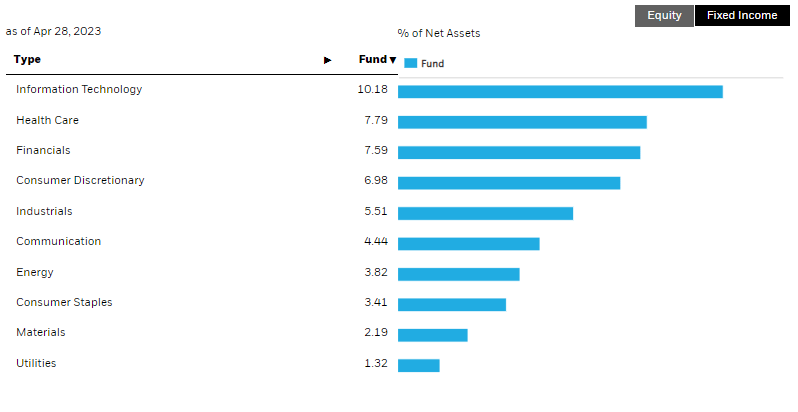

On the fund's equity sleeve, the sector exposure is fairly diverse. Tech represents the largest weighting, but overall it still provides varied exposure. This weighting is similar to what we saw at the end of 2022. However, the tech sleeve has come up from the 8.68% level it was previously. That could have been helped driven by strong results from a few select top equity positions.

{kind=link}

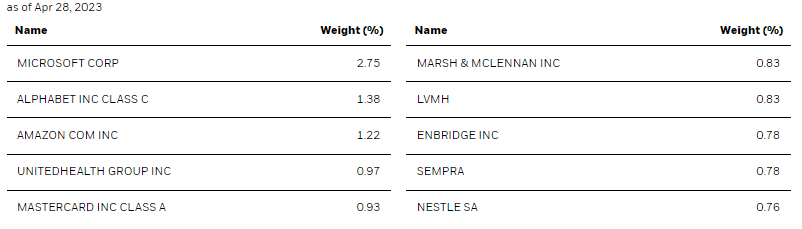

Several of the top equity positions in BCAT are the same names that are really supporting this market through 2023. Perhaps unsurprisingly, BCAT has provided decent results on a YTD basis.

{kind=link}

Of course, those are the positions of Microsoft ( MSFT ), Alphabet ( GOOG ) and Amazon ( AMZN ) that we consistently hear about. LVMH Moet Hennessy Louis Vuitton SE ( LVMHF ) is also having quite the year. We also have a few names putting up what would usually be considered strong single-digit results too. It's just that the tech titans have dominated in terms of performance in 2023.

Ycharts

MSFT and AMZN were listed as top holdings previously. The weightings have increased with the latest update, as they were previously 1.43% and 0.95% weighting.

The fund also contains some private exposure . At a weighting of 11.8% of the portfolio at the end of 2022, it is a material but not overly aggressive allocation. They specifically state that they want to build up this weight gradually over time. They also want to put a general focus "but not exclusive" on private innovation investments in the tech space.

Private exposure can be a huge win for the fund over the long term if they are successful. However, it comes with its own pitfalls. With the IPO market pretty much shut down for now, exiting these illiquid investments can be an issue. Some of these holdings are restricted, meaning certain criteria - generally a time frame - have to be hit before selling is even possible. For BCAT, that remains a fairly low concern at just 0.7% of the fund.

Private investments can also include smaller, less financially stable companies with a higher chance of failure. Valuations also become a concern, as these are often level 3 securities. BCAT carries a fairly meaningful weighting to level 3 securities due to the private investments. That can explain some of the discounts, as valuations aren't always the most reliable for level 3 securities, and this skepticism leads to caution from investors.

Conclusion

BCAT is a highly diversified fund that provides exposure to almost everything. That includes anywhere around the globe and in the public and private markets. Up and down the capital structure and credit quality. With the flexibility to enter various derivative contracts at will. All this really takes a lot of faith that the management team is doing the right thing.

The fund has been seeing better results so far in 2023 after a rough 2022. However, it could still be argued that the fund's history is too short. They haven't operated in more 'normal' times either, as they launched in the raging bull market that finished up in 2020 and bled into 2021. Then the fund has now gone through one of the most aggressive rate hiking cycles in decades through 2022. Now, 2023 is showing some rebounding for the 'market,' but the breadth has been terrible, and it's mostly the tech titans alone carrying the market higher. It's been one year after another of unprecedented times.

BCAT's increased distribution earlier in the year can be seen as a positive. It can help support the fund from sinking to a deeper discount as eventually yield chasers can jump in. However, with a fairly weak performance in the prior year, it wouldn't necessarily be something that was seen as warranted. At least in terms of what coverage could look like going forward for the payout.

Overall, the fund still provides an attractive discount at this time, even with a bit of narrowing through 2023. I believe that a long-term income investor could see this as a compelling time to add to this fund or initiate a position.

For further details see:

BCAT: Highly Diversified Fund Trading At An Attractive Discount