ECF - BCV And ECF: Convertible Bond Exposure Offering Yield With Upside Potential

2023-11-13 04:32:00 ET

Summary

- Bancroft Fund and Ellsworth Growth and Income Fund offer diversified exposure to convertible debt investments.

- Convertible bonds offer yield as fixed-income investments but also potential upside through conversion into common stock.

- Higher interest rates are leading to higher yields and more issuances of convertibles by higher-rated companies.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Bancroft Fund ( BCV ) and Ellsworth Growth and Income Fund ( ECF ) provide investors with diversified exposure to convertible debt investments. They are closed-end funds that are both trading at deep discounts on an absolute basis and a relative basis. Both of these funds share quite a few similarities, and I cover both of these funds regularly, so today, we are looking at a quick update for both as well as discussing the convertible bond market in general.

Convertible bonds have unique characteristics that make them a fixed-income security to provide some yield to income investors. However, they also offer potential upside should the underlying issuer do well and the price of their common stock also climb. The potential upside comes from this possible upside move when these instruments can be converted into the common stock of the issuer.

Should the stock falter and not perform well, then there is a downside floor - which is where the other side of the fixed-income feature kicks in aside from the yield. They have a par value and must be repaid to the investor upon maturity.

Of course, the usual caveat is at play here: it can only be repaid assuming the company hasn't faltered so bad that it enters bankruptcy. In the case of a liquidation, convertible bonds are often below secured debts but above equity, preferred and subordinated debts.

Corporate Capital Structure (Calamos)

Convertible bonds can trade on a secondary market; however, they are largely 144A-issued securities , and that means sales are going to be reserved for qualified institutional buyers. They also come unrated and have generally been issued by lower-rated companies that might not be profitable yet. However, Calamos noted that historically, only about 1% of convertible bonds have defaulted, which is lower than traditional high-yield bonds.

Additionally, in a higher interest rate environment, that is starting to change. As noted by Calamos earlier this year , they see higher yields being offered by convertibles, but not only that, they are seeing higher-rated companies issuing convertibles as well.

The reason for this is pretty simple: as the walls of debt start maturing in the coming years, a lot of this debt will be refinanced. Now, with a higher rate environment, these companies would have to issue debt with higher yields to be competitive. At the same time, if they go the convertible route, they can issue lower yields than straight debt because of the convertible feature.

BCV and ECF might not be the best equipped to handle a rising rate environment, and that can be seen as they were absolutely crushed in the last couple of years. However, with their portfolio starting to yield higher income generation from holdings that are moving higher up in quality, they can make a lot of sense. That's not to mention the substantial discounts of these funds to their NAV per share and buying an asset class while it's down - while one of the harder things to do psychologically - can often lead to a better chance for upside potential.

BCV Basics

- 1-Year Z-score: -1.90

- Discount: -16.71%

- Distribution Yield: 7.54%

- Expense Ratio: 1.38%

- Leverage: 21.89%

- Managed Assets: $137 million

- Structure: Perpetual

BCV's investment objectives are "...providing income and the potential for capital appreciation, which objectives the Fund considers to be relatively equal over the long term." Their approach is quite simple; they "operate as a closed-end, diversified management investment company and invest primarily in convertible securities..." Along with convertible securities, they can mix in various other equity and fixed-income securities.

Since our last update , the fund's discount has become even wider. It is now trading well below the average in more recent years and even trading meaningfully below its decade-long average. That puts it in a situation where it isn't just trading at a deep discount on an absolute basis, but relative to its history, it also represents a compelling time to consider putting capital to work in this name.

Ycharts

The fund is leveraged, and that is also adding to volatility. That being said, unlike other closed-end funds that are leveraged through borrowings, they don't have to deal with a higher interest rate environment. This is because they have a fixed rate preferred as their form of borrowings.

This preferred is also publicly traded: 5.375% Series A Cumulative Preferred ( BCV.PR.A ). The 5.375% might seem high, and it was when it was originally issued in a zero rate environment, but most CEFs are experiencing borrowings coming in at 6%+ now on their credit facilities. Having a fixed-rate cost also comes with some peace of mind; it takes away one more moving part to consider before investing.

The preferred is callable and has been since mid-2021, but it has no maturity. They are authorized to repurchase preferred when they find it advantageous to do so, which they've done periodically at a discount to par.

Some of BCV's top holdings are still lower in terms of offering meaningful yields on the convertible debt holdings. These are the top ten as of September 30, 2023 .

BCV Top Ten Holdings (Gabelli)

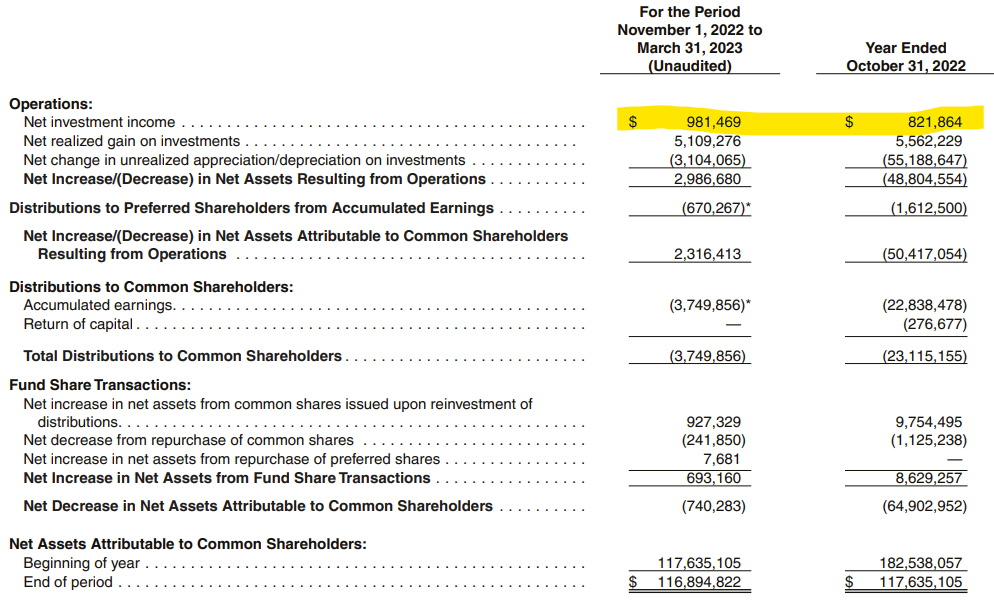

That said, these are generally higher than what we saw in the last couple of years, where they were holding convertible debt with 0% coupons. This has led to substantially higher net investment income being generated by the fund. In their last report , they listed NII at more than the entirety of fiscal 2022. On a per-share basis, it was $0.17 in the last six months compared to $0.18 for fiscal 2022. However, it should be noted that this is a shortened period as it only shows a 5-month period. This was because the fund had a fiscal year end of September 30 but switched to October 31.

This higher NII could come from the higher yields that are being offered by convertibles and also shuffling their portfolio around, as they are an actively managed fund with turnover last coming in at 20%.

BCV Semi-Annual Report (abbreviated period) (Gabelli (highlights from author))

{kind=link}

NII still isn't enough to cover the entire payout for the fund, so they'll require capital gains to fully fund it. However, the higher the NII goes, the fewer capital gains they'll have to find.

The fund also has a 5% minimum managed distribution policy. This has generally led to a year-end special that tops off the payout for the year. However, with 2022 and 2023 being down years, the fund has seen its NAV distribution rate easily eclipse the 5% policy, as it currently stands at 7.44%. Therefore, a special doesn't look likely this year - or at least it doesn't necessarily look like it would be required. They may still choose to pay a special if they are still sitting on a hefty amount of realized gains for the year that they want to avoid an excise tax.

{kind=link}

ECF Basics

- 1-Year Z-score: -1.13

- Discount: -15.12%

- Distribution Yield: 7.02%

- Expense Ratio: 1.39%

- Leverage: 25.30%

- Managed Assets: $166 million

- Structure: Perpetual

ECF's objective is quite simple: "... providing income and the potential for capital appreciation; which objectives the Fund considers to be relatively equal, over the long term, due to the nature of the securities in which it invests." They attempt to achieve this by simply "primarily investing in convertible securities and common stocks.

Much of what is discussed above BCV is exactly the same for ECF. These two funds might be under the Gabelli umbrella after their 2015 acquisition , but they also took along their managers, Thomas Dinsmore and James Dinsmore. These managers have continued to manage these funds today. That said, where they do diverge a bit is that ECF will incorporate a higher allocation to equity securities. Their last six-month report showed common stock exposure at around 19.3%. (ECF has presumably decided to keep the September 30 fiscal year-end date, which is an immaterial difference between the funds as it doesn't impact performance.)

This fund has similarly seen its discount widen since our prior update . That's pushed it to trade at a relatively attractive discount relative to its history as well.

Ycharts

ECF also has fixed-rate preferred being utilized for their borrowings. One of these is publicly traded, the 5.25% Series A Cumulative Preferred ( ECF.PR.A ), while the 5.20% Series B Cumulative Preferred is a private placement. Though they did raise the Series B dividend from the 4.4% rate it was previously, noted in a recent N-2 filing that ECF has.

An N-2 filing is a registration for the potential of new shares being issued. That can be through a rights offering, which generally sees a fund's discount widen even more as shares sold at a discount are dilutive to shareholders. For that reason, that will be something to watch if they go through with a rights offering.

In looking at ECF's top holdings as of September 30, 2023 , we can see that they are also carrying some higher coupon positions these days. However, they also have several of their common stock holdings as large positions.

ECF Top Ten Holdings (Gabelli)

Like BCV, ECF also maintains a 5% minimum distribution policy. The NAV rate currently suggests that they won't need any year-end distribution to meet this target, though it is currently lower than BCV's, with a 5.96% NAV rate.

{kind=link}

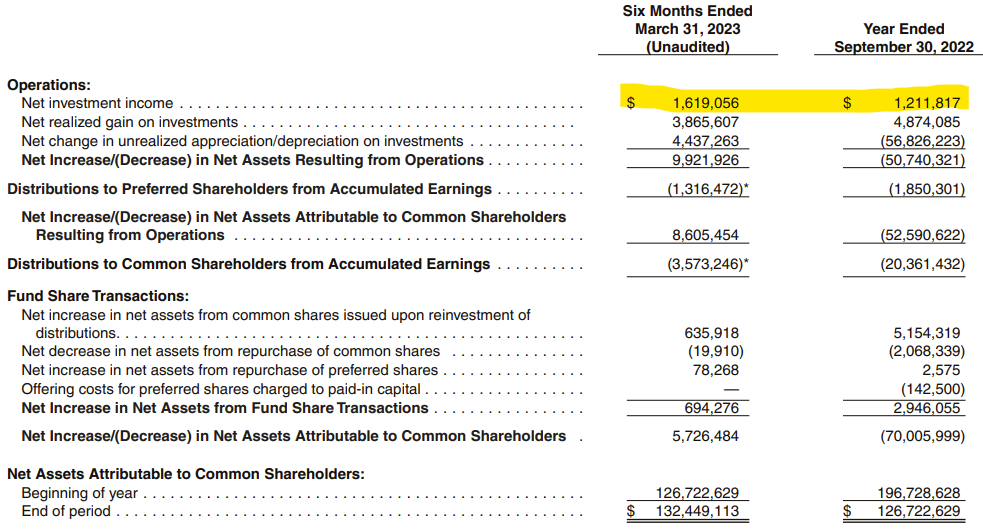

ECF has also seen its NII rise quite dramatically, topping out last full fiscal year's NII in a six-month period. On a per-share basis, this works out to $0.12 in the semi-annual period compared to $0.09 last fiscal year.

{kind=link}

Of course, that still means they are not earning enough to cover their distribution from income only. They will also require capital gains to fully fund their distribution, which has been harder to come by in the last few years for convertible heavy funds. The iShares Convertible Bond ETF ( ICVT ) is representative of that, as it exploded in 2020 and into 2021. After that, it started to sink in late 2021 and was hammered in 2022. It has essentially gone nowhere for nearly three years now based on total returns.

Ycharts

Though, the higher the NII that ECF brings in, the less reliant they become on capital gains in the future.

Conclusion

BCV and ECF provide investors with steady distributions while waiting for potential upside through their convertible exposure. ECF also carries some higher allocations to equities, which fits the 'growth' part of its name. Convertible securities offer investors both characteristics of fixed income and equities, which helps add further diversification to one's portfolio. Additionally, BCV and ECF are deeply discounted on an absolute and relative basis, which makes them more appealing to consider at this time.

For further details see:

BCV And ECF: Convertible Bond Exposure, Offering Yield With Upside Potential