IDCC - BCV: Signs Of Stabilizing With An Attractive Discount

Summary

- The overall market and BCV have been stabilizing since our previous update.

- Being towards the end of interest rate hikes should mean that this stabilization could continue.

- The fund offers a wide discount with diversified convertible bond exposure.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 11th, 2023.

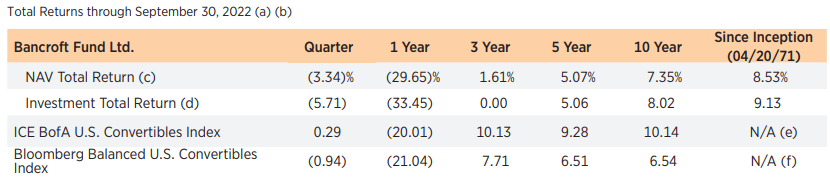

Bancroft Fund ( BCV ) saw interest rates have a huge impact on their performance in the last year. In 2022 the total NAV return came in at a decline of around 28%. On a total share price return basis, results were even more dismal, sliding almost 34%.

Interest rates impacted the fund by making the convertible bonds they carry much less attractive. After all their successes in 2019 and 2020, with convertible bonds particularly attractive in 2020, that play was less attractive in 2021. Then in 2022, it completely deflated as their portfolio was full of low-yielding bonds. As rates rose, the almost non-existent yields have lost out to the U.S. Treasury debt that yields ~4% these days.

However, it also pushed BCV to an attractive discount, and the Fed should be close to the end of the rate-hiking cycle. This has played out a bit with the fund stabilizing since our last update . We are seeing some slightly positive results since that October publication.

BCV Performance Since Previous Update (Seeking Alpha)

With the expectation for minimal hikes coming, this stabilization should continue. That is as long as the Fed doesn't have to ramp up the interest rate hiking pace again. Basically, the future still looks bright for BCV from here, while it's still showing an attractive entry level.

The Basics

- 1-Year Z-score: -1.56

- Discount: 14.52%

- Distribution Yield: 7.52%

- Expense Ratio: 1.15%

- Leverage: 20.52%

- Managed Assets: $146.185 million

- Structure: Perpetual

BCV's investment objectives are "...providing income and the potential for capital appreciation; which objectives the Fund considers to be relatively equal over the long term." Their approach is quite simple; they "operate as a closed-end, diversified management investment company and invest primarily in convertible securities..." Along with convertible securities, they can mix in various other equity and fixed-income securities.

The fund carries a moderate amount of leverage. For a convertible bond fund, this isn't often too detrimental. At the end of the day, convertible bonds are still bonds that do have a floor of sorts. If a company doesn't go bankrupt while holding these bonds, BCV should at least get the face value back if the conversion to common shares doesn't make sense. If conversion makes sense, that would indicate a potential upside or that the company's shares had done well. That being said, leverage of any level will increase both the potential upside but also the downside.

The other potential problem from leverage can come in depending on what type of leverage the fund carries. Primarily, closed-end funds overwhelmingly utilize credit facilities or borrowings based on a floating rate. However, BCV carries a 5.375% Series A ( BCV.PA ) - a fixed-rate preferred. That had been a high yield relative to a credit facility.

With rates rapidly rising, this is now a competitive or better leverage cost from what we see from the credit facilities other CEFs draw on. It became callable in 2021, but clearly, redeeming these shares wouldn't make a lot of sense as they would have to issue higher-cost debt if they wanted to replace it. This is partially why it trades below its own face value at around $23.90.

Performance - Attractive Discount

When comparing BCV to its benchmark, the longer-term results were more attractive. More recent returns have shown poor selection and the damages of being leveraged. The expense ratio will also play a role.

The biggest detraction from their benchmark appears on a 3-year basis, but the last five years haven't been anything to brag about either. The results are worse on a total share price basis but also the total NAV return.

{kind=link}

Since our last update that reflected the results through June 30th, 2022, the results have worsened. At that time, the 5-year results aligned closer with the Bloomberg Balanced U.S. Convertibles Index.

When comparing the fund over the last five years to the iShares Convertible Bond ETF ( ICVT ), we can see more precisely when the divergence began. It looks like heading through 2020; it started to drop off in the latter half of the year. Then when things started to decline, the NAV really started to fall short, as leverage would have amplified these results.

Ycharts

At the same time, you can't get the discount that is currently present on shares of BCV from an ETF. The fund has historically traded at a deep discount, but this is pushing near its lowest levels in years - excluding the swift drop and subsequent recovery in 2020 due to COVID.

Ycharts

If most of the declines are over and rates do stabilize, BCV's portfolio can once again become more competitive, in my opinion. That also includes a potential rebound for the discount to narrow from here.

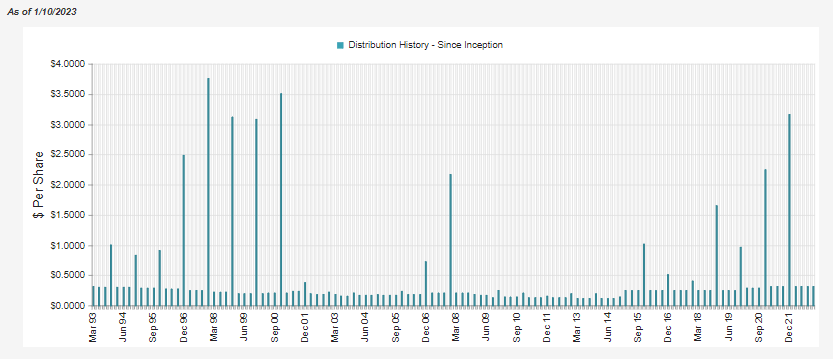

Distribution - 5% Minimum Policy

The fund pays a regular quarterly distribution, with a year-end to top of its 5% minimum distribution policy. With such poor results in the last year, there was no need for a further year-end. Therefore, investors only had to look forward to the regular $0.32 paid.

{kind=link}

The regular has been bumped up over the last ten years after they were cutting around the GFC. The latest distribution yield comes to 7.52%, with a NAV rate of 6.43%. With such a large discount, investors can receive a much higher yield relative to what the fund has to earn to fund that distribution.

That being said, the fund doesn't cover its distribution with income generated in the portfolio. That income generated from the underlying holdings is far too low to cover what they are distributing. ICVT yields around 1.89%, really highlighting the low yields.

The ratio of NII to average net assets for BCV comes to just 0.59%. After preferred shareholders are paid, it's actually negative for BCV. So clearly, income isn't enough.

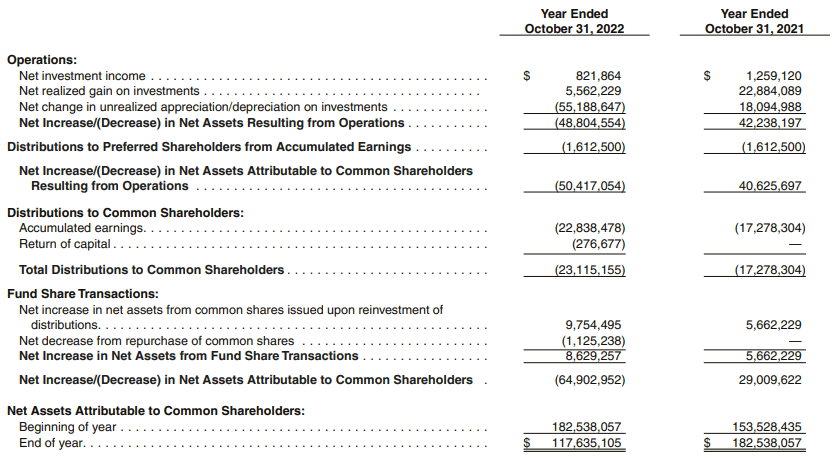

The latest annual report shows us that net investment income has actually declined. Given they don't have rising interest rate costs, this is one thing that I didn't necessarily expect before giving this fund another review.

{kind=link}

What seems to have changed year-over-year is that total investment income dropped. More interesting to note is that the decline was so large that even a decline in expenses didn't offset the decline in TII. Expenses went from $1.972 million to $1.613 million. TII went from $3,229.5 million to $2.433 million.

After the preferred distributions of $1,612,500, there would have been a deficit of nearly $800k left to pay the $23,115,155 to common shareholders. Therefore, the fund will rely entirely on capital gains to cover their distributions. We can see in the latest year, realized gains didn't come close to covering the distribution. That, of course, is a big negative for the fund, but it isn't all bad news.

One of the reasons that the distribution last year came out to such a large amount was the $2.85 special that's being reflected in this fiscal year for the fund. They had 5,517,786 shares outstanding at the end of fiscal 2021, which would come out to approximately $15.726 million being paid out. That would put the regular distribution payout around $7.389 million, or about a third of what we see paid out.

That still means there is a significant shortfall, but the shortfall is much more minimal than we see at first glance. It can also help us understand why NII per share went from $0.24 to $0.18. Besides portfolio positioning, they paid out such a large special that it knocked off around 8.5% of the NAV. That's 8.5% of their assets that no longer produce income for the fund. That works out to just around $0.02 NII per share or a third of the $0.06 decline we see year-over-year.

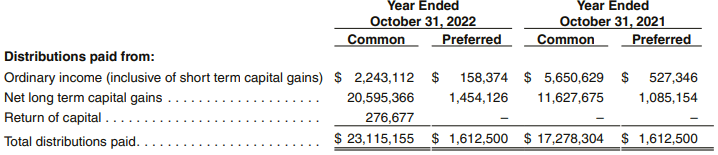

For tax purposes, the majority of the distribution was classified as long-term capital gains. This is a good reminder that taxes don't necessarily have to line up with the results in the portfolio.

{kind=link}

BCV's Portfolio

Turnover for BCV comes in at 52% in the latest fiscal year, around where they have been in the last five years. That makes them a fairly active fund, which can help explain why we would see a variance from year-to-year from income generation on the underlying portfolio.

The portfolio is generally overwhelmingly positioned in convertible bonds or convertible preferred. As of their last report, it would have accounted for just over 95% of their total managed assets. The remainder would have been in common stocks.

In looking at the top sector allocation of the fund, computer software and services make up the largest weighting. This is generally the case as most convertible funds allocate to tech-related sectors. Tech is often associated with growth, so those companies often try to raise capital to invest in that continued growth.

BCV Sector Exposure (Gabelli)

Still, the fund also carries a fair bit of exposure outside of the tech sector. We see a fair bit of diversification in the top holdings at the end of 2022.

BCV Top Ten Holdings (Gabelli)

Ford Motor's ( F ) convertible zero coupon is the largest. This is a position that comes due March 15, 2026. The cost for the fund is nearly $3.8 million, with a face value of around $3.5 million. At the end of their fiscal year, they had a market value of $3.535 million. Given this, shares of F would have to rally for this position to pay off. I'm bullish on Ford, but it certainly isn't guaranteed to happen from now until 2026.

BCV Holding (Gabelli)

Crown Castle ( CCI ) is an example of their common stock holding, as is the Broadcom ( AVGO ) position. In fact, those are the only two equity positions in the fund listed in their report.

Their third largest holding is InterDigital Inc's ( IDCC ) 3.5% convertible bond with a maturity of June 1, 2027. That's certainly yielding something but is quite low compared to what the risk-free rate is at this time. Once again, we see that their cost is above the face value. Fortunately, it isn't too above the face value, and the market value is currently lower. All else being equal, one could expect some upside from the current level.

BCV Holding (Gabelli)

Conclusion

Convertibles were one of the areas to get hit pretty hard by increasing interest rates. The risk-free rates being above many of these not only make the convertibles less attractive to hold but also take the wind out of the sails of most of these growth stocks issuing the convertibles. When their price declines came in as more speculative names got hit, that also hit the value of the convertible security prices.

With rates potentially stabilizing over this year, we have seen a more stable market. That has translated into BCV becoming more stable, and if this stabilizing can continue, we should see more attractive results going forward

For further details see:

BCV: Signs Of Stabilizing With An Attractive Discount