GAINZ - BDC Weekly Review: The Two Steps Of BDC Analysis

Summary

- We take a look at the action in business development companies through the first week of February and highlight some of the key themes we are watching.

- BDCs notched another good week with a 1% total return.

- We discuss a two-step approach to BDC analysis based on recent Barron's comments, and highlight CSWC earnings.

- We are keeping an eye on the ARCC/OCSL relationship as well as recent WHF underperformance.

This article was first released to Systematic Income subscribers and free trials on Feb. 4 .

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company ("BDC") sector from both the bottom-up - highlighting individual news and events - as well as the top-down - providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the first week of February.

Be sure to check out our other Weeklies - covering the Closed-End Fund ("CEF") as well as the preferreds/baby bond markets for perspectives across the broader income space. Also, have a look at our primer of the BDC sector, with a focus on how it compares to credit CEFs.

Market Action

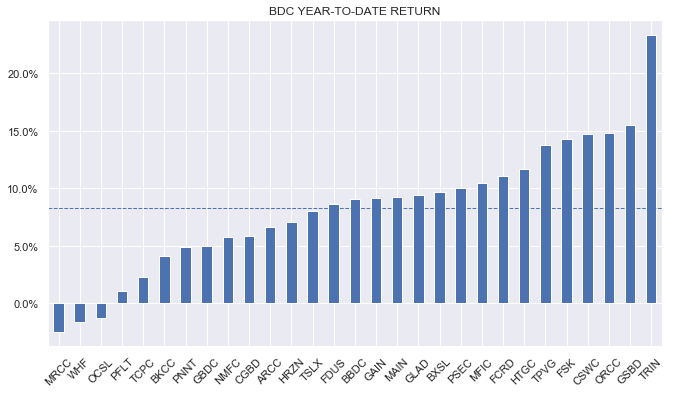

BDCs delivered another good week with a total return of around 1%. Outperformers were two of the early earnings reporters Gladstone Investment Corporation ( GAIN ) and Capital Southwest ( CSWC ), which delivered good results.

Year-to-date, Trinity Capital ( TRIN ) remains the outperformer. We earlier reduced our exposure to the company on the back of this monster move. Oaktree Specialty Lending Corporation ( OCSL ) remains one of the laggards - we rotated our position to Ares Capital ( ARCC ) prior to the recent deflation in its price.

{kind=link}

January was one of the strongest months in the sector over the last couple of years, as BDCs were supported by the rise in stocks and a fall in Treasury yields.

Systematic Income

Sector valuation continues to creep closer to 100%. We expect upcoming dividend hikes to continue to add fuel to the sector.

Systematic Income

Market Themes

A subscriber highlighted a comment from Barron's about the value in the Blackstone Secured Lending Fund ( BXSL ) which we fully endorse as we also find BXSL to be one of the most attractive holdings in the sector at the moment. However, being tiresome pedants, we can't help but make a couple of additional clarifications.

Barron’s basic message on BXSL was that it held a high-quality portfolio, enjoyed high distribution coverage (i.e., meaning likely further dividend hikes) and "reasonable" fees.

Let's take the fees point first. The comment that BXSL fees are "reasonable" is not correct – management fees are one of the very lowest in the sector and 0.5% below the average BDC level. That’s not "reasonable" – that’s fantastic. Reasonable would be a base management fee of 1.5% i.e. 50% above what it actually is.

The commentary was also missing anything about valuation which is certainly odd - after all, if BXSL traded at a 25% premium to the sector it wouldn't be as attractive as it is today.

On the face of it, this is the kind of commentary you see elsewhere and seems very helpful for investors in deciding which BDCs to allocate to. However, it’s also a good example of our pet peeve about general research commentary which is that they are all done on a standalone basis.

What is much more useful is a 2-step analysis of; 1) what the security itself is – this is what you tend to see; and, as importantly, 2) how the security compares to the rest of its sector.

Just saying BXSL has a high-quality portfolio etc. etc. isn’t actually all that actionable because we don’t know what other BDCs have high-quality portfolios (many!) and which have high distribution coverage (some!). In other words, just because BXSL has the features that it does doesn’t actually make it a buy – what makes it a buy is when we know how many other BDCs have similarly attractive features of BXSL (few) and where those other BDCs trade in valuation terms (more richly).

For instance, we can imagine a scenario where other BDCs are not as attractive as BXSL in their features but trade at a 30% better valuation in which case they probably would be more attractive overall. The reality is that BXSL trades at a valuation 3% below the sector average which makes it very attractive – it’s an above-average BDC in its features and below-average in its valuation – exactly what we like to see.

This situation is fairly unusual so the obvious question is what’s going on? In our view what’s going on is that BXSL doesn’t have a long track record as a public entity (though in its short public life it has outperformed the sector in each of the 3 quarters in total NAV terms). So most retail investors take the view that "you can’t get fired for buying IBM," i.e., people are happy to overpay for BDCs that have a long and strong track record rather than buy cheap BDCs with strong features but a short public track record. Of course, BXSL has a strong private track record but this likely escapes most retail investors.

The takeaway here is that having a good description of a particular BDC is not very actionable - investors need to know how a given BDC compares to the rest of the sector in its various metrics. However, because this is hard to do, it often goes missing in the analysis.

Capital Southwest Market Commentary

CSWC reported decent FQ3 results . Net income came in 17% above the previous quarter and the base dividend was increased by 2% with the supplemental remaining the same.

Systematic Income BDC Tool

The NAV fell by less than 2% which is larger than expected but not critical. Current valuation of 121% means the company will continue its NAV-accretive at-the-market share issuance program to drive further NAV gains which should offset the drop in Q1 soon enough.

One thing to keep an eye on is that realized losses have been elevated for the past couple of quarters. The remaining portfolio quality looks OK, with non-accruals and PIK fairly low.

Systematic Income BDC Tool

Stance and Takeaways

We are keeping an eye on the ARCC / OCSL relationship. Recall that we made a switch from OCSL to ARCC when OCSL traded up to a 5% higher premium over ARCC. This has reversed by around 11% with ARCC now trading at a valuation 6% above that of OCSL (106% vs. 100%). We are considering a partial move back to OCSL.

We are also tracking WhiteHorse Finance ( WHF ), whose valuation has widened out relative to the sector.

Systematic Income

This chart shows that its discount to the sector average has fallen to more than 10% which is fairly unusual for the last 5 years. WHF has performed in line with the sector over the last 3-5 years in total NAV terms. WHF is one of the few BDCs that have not hiked the dividend over 2022 (or declared a new special dividend) despite core net income being above its base dividend. We wouldn't be surprised if it hikes this quarter. It's trading at an 11.1% yield - slightly above the sector average.

Systematic Income

For further details see:

BDC Weekly Review: The Two Steps Of BDC Analysis