BESIY - BE Semiconductor: A Solid Dividend (Growth) Stock In The Semiconductor Manufacturing Space

2023-04-04 14:55:16 ET

Summary

- BE Semiconductor Industries is a market leader in assembly equipment for advanced packaging applications.

- With a strong balance sheet, excellent profitability and revenue growth throughout the cycles and hybrid bonding as the main catalysts, the company has set itself in the pole position for strong future growth.

- Based on my own discounted cash flow analysis, the fair value of BESIY stock is $72.52, which is 16.6% above the current share price.

- There is a lot of turbulence in the stock market: inflation and geopolitical friction can put pressure on the share price in the short term.

Editor's note: Seeking Alpha is proud to welcome Dutch Dividend Therapist as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment case

The demand for chips will be high for the next years or even decades. Growth drivers like digital- and cloud infrastructure, smart everything, 5G, artificial intelligence, high performance computing, data centers and vehicle electrification will create a high demand for chips. This might be a good reason to analyse companies that are linked to the semiconductor industry.

Most people know ASML Holding N.V. (ASML), the world's innovation leader of chip-making equipment from the Netherlands. A far less known company that has its headquarter in the Netherlands is BE Semiconductor Industries (BESIY). In the past 10 years, BE Semiconductor has created a lot of shareholder value in the form of dividends and share buybacks. The dividend growth in particular has been spectacular. In my opinion, BE Semiconductor has a lot of room left to grow the dividend in the decade to come. In this article, I am going to explain why you need to consider BE Semiconductor as a nice long-term holding in a well-balanced dividend (growth) stock portfolio.

Company overview

BE Semiconductor is a relatively small company with a market cap of € 6.14 billion. Shares are listed on Euronext Amsterdam and the level 1 ADRs trade on the OTC markets (BESIY). BE Semiconductor operates a global network of sales & services in Europe, USA and Asia. It operates seven facilities in Asia and Europe for production and development activities. Based on their last investor presentation of March 2023 BE Semiconductor has a total staff of 1893 fixed and temporary employers (67.2% were based in Asia and 32.8% in Europe and the rest of the world).

At the moment, BE Semiconductor is one of the world leaders in the "back-end" part of the chipmaking process. The machines produces assemblies or packages. The packages provide the electronic interface and the physical connection of a semiconductor device, chip or electronic components. The services BE Semiconductor provide will result in higher miniaturization, chip density and higher performance for its consumers.

The company has an industry-leading equipment portfolio comprising

- Die attach (82% of 2022 revenue).

- Packaging and plating (18% of revenue).

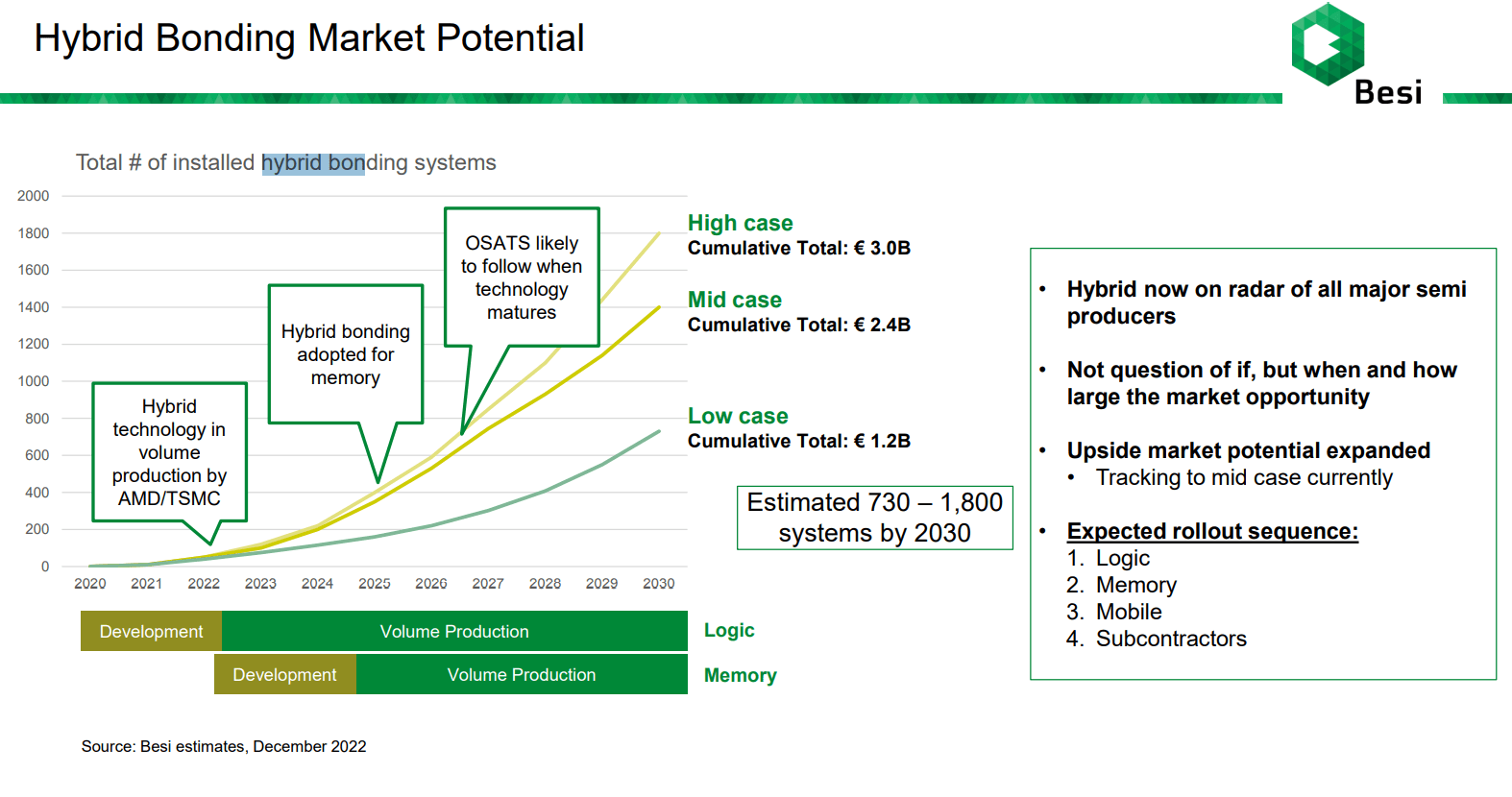

Especially in the die attach segment BE Semiconductor had managed to increase its market share from 30.4% in 2016 to 41.4% in 2021. One of the most important growth drivers of BE Semiconductor is a technique called Hybrid Bonding. This technique is on the radar of all major chip-makers such as Taiwan Semiconductor Manufacturing (TSM), Qualcomm Incorporated (QCOM) and Advanced Micro Devices (AMD). Hybrid bonding enables faster, more complex devices with submicron placement accuracy, resulting in increased performance, design flexibility, and lower cost of ownership.

Image 1 (BE Semiconductor investor presentation March 2023)

{kind=link}

As shown in image 1, Hybrid Bonding can be a large market opportunity for BE Semiconductor. This can lead to a lot of additional revenue.

BE Semiconductor is involved in a lot of growing end-user markets, such as:

- Mobile internet devices (biggest market so far)

- Intelligent automotive components

- Hardware (PCs , tablets etc.)

- Data-mining

- Cloud computing

- Virtual reality

- Advanced medical equipment

- Artificial intelligence

In my opinion there are a lot of potential growth drivers to trigger dividend growth in the future.

Financials

Income statement and balance sheet

As most of you know the chip industry is cyclical. Looking at the financials of the last ten years, the numbers are impressive. Through the cycles BE Semiconductor has managed to grow its revenue from €351 million ($380.61 million) in 2010 to €723 million ($783.99 million) in fiscal year (FY) of 2022. The peak revenue was €749 million ($812.18 million) in FY 2021.

Image 2 (BE Semiconductor investor presentation March 2023)

What is even more impressive is the consistent increase in gross margin during every cycle (2010: 34.1% to 62.3% in Q4 2022). Even during economic headwinds , when the demand is dropping the margins were still good. Their margins are also significantly higher compared to their peers. In FY 2022 ASMPT had a gross margin of 44.6% and Kulicke and Soffa (KLIC) 50.3%. One of the reasons why BE Semiconductor can maintain high margins is their leading market position and their ability to downscale the amount of employers when they face economic headwinds.

The balance sheet is showing the strong financial health of the company. BE Semiconductor has €491 million ($526.5 million) in cash on hand and a long-term debt of €322 million ($345.7 million). The long-term debt isn't increasing over time and is in my opinion manageable.

Dividend

I am a dividend growth investor. I tend to look for companies paying a reliable and growing dividend. At the time of writing this article, the stock price was $86.90. Since the next dividend is € 2.85 ($ 3.09) this comes down to a dividend yield of 3.6%. BE Semiconductor pays a dividend on an annual basis. The amount is based on its annual financial and prospective performance. The pay-out ratio will be in the range of 40-100% to net income. The last five years (2017-2022), it was in the 90-100% range. A possible reason why the pay-out ratio can be lower in is a possible acquisition or another opportunity to strengthen its market position.

Image 3 (BE Semiconductor annual report 2022.)

The table shows how fast the dividend was growing during this market cycle. The amount of dividend paid is heavily dependent on the profit BE Semiconductor has made in that particular year. The company is highly cyclical, so don't expect a growing dividend every year. A dividend cut is fairly common, but in the long run , throughout different cycles, the dividend grows fast. Based on the numbers of Seeking Alpha , the dividend growth rate 10Y (to 2022) is 38.08%. In January 2010 the stock price was only €1.40 ($1.52), the yield-on-cost would be extraordinary if held for a 10-year period. Based on the numbers it might be worth it to look at BE Semiconductor to add to a diversified dividend portfolio. If you prefer a more consistent, less cyclical, dividend grower in the same segment of the industry, a company like ASML will probably be a better choice.

Last quarterly results

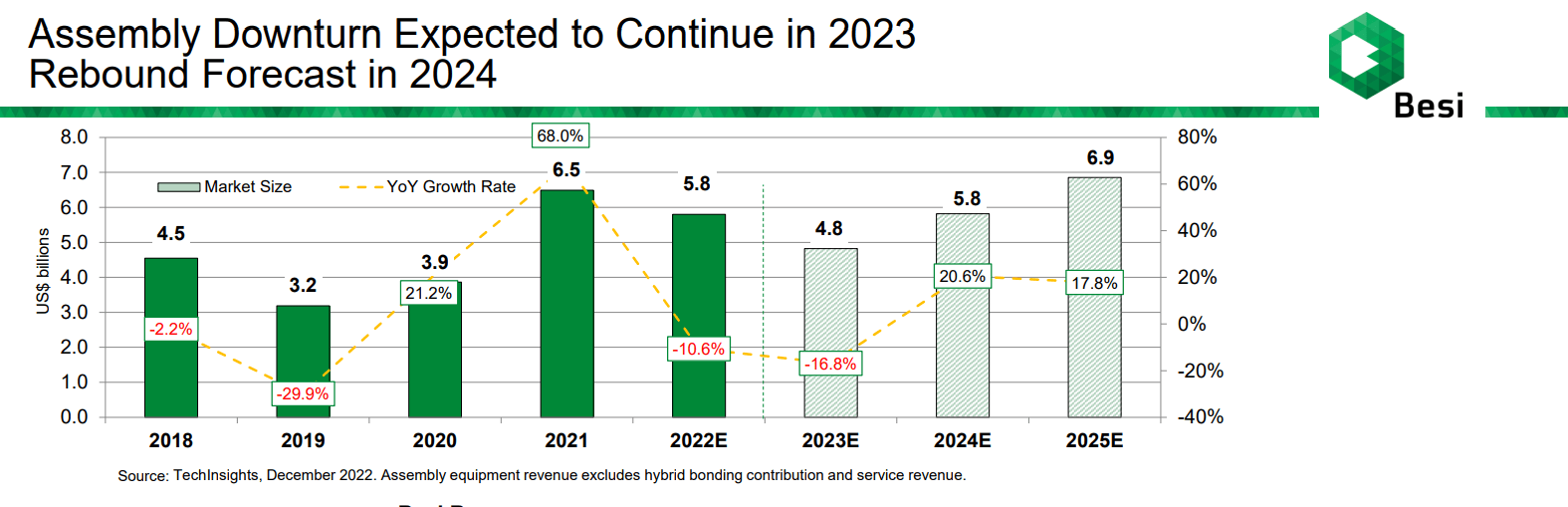

As expected, the 4Q22 revenue was 19.8% lower (guidance down 15-25%) compared to 4Q21. This was mainly due to a decrease in demand for mobile phones compared to 2021. There were also positive things to mention. BE Semiconductor was able to increase their gross margin to 62.3%, despite the economic downturn in the chip industry. Surprisingly their orderbook was up 44.1%, mainly due to their new Hybrid Bonding systems. The market was satisfied with the Q4 results. However, there is still a good chance that the next few quarters will be rough. BE Semiconductor expects a decrease in revenue for the next quarters as a result of the lower demand for smartphone devices. TechInsights forecasts a further decline in revenue of 16.8% for 2023 , although, a strong rebound is expected to happen in 2024-2025.

Image 4: Expected growth year-over-year (BE Semiconductor Investor presentation 2023)

{kind=link}

Valuation

Based on my own analysis of the company's financials and its future prospects, BE Semiconductor can be a solid investment. Now it's time to look at the valuation. To determine the fair value of BE Semiconductor I used a discounted cash flow analysis. The company is highly cyclical. For example in 2018 Q2 orders declined by 58% and in 2017 and 2021 order grew by 82.2% and 98.9%. It is really hard to forecast future growth and it's likely that the volatility in consumer spending is likely to persist in the future. As seen on Image 4 the year-over-year growth rate is improving from 2024. Based on these numbers I used an average 5-year growth rate of 10% and a 10-year growth rate of 12.5%, which is in my opinion very conservative. This estimation of 12.5% is a combination of the current revenue and its future revenue from the Hybrid Bonding machines. There is a possibility that the 10-year growth rate will be higher than the 5-year because I expect a decrease in revenue in the short-term. And if things go well Hybrid Bonding can unlock a lot of value after they further increase their production. I used a discount rate of 10%, because I want a return on my investment of at least 10% per year. I applied relatively high terminal multiple of 20, because of the company's market dominance and its average 5-year PE-ratio of 23 .

Discounted cash flow analysis in USD (My own Google spreadsheets)

This comes to a fair value per share of $ 72.52. If we subtract a margin of safety of 10% it comes down to $ 65.26 per share. At the moment the share price of BE Semiconductor is $ 86.90. Compared to my own fair value it is 16.6% overvalued.

Short-term headwinds

In 2022 there was a lot of negativity around semiconductor stocks and BE Semiconductor went from $ 96.09 to $ 38.10, a 60.4% decline in share price. In October 2022, the share price regained its positive momentum. After the Q4 results the share price skyrocketed from $71 to $81. The main reason was the surprise in the increased orderbook. This could be a beginning of a new uptrend in the semiconductor cycle. However, there are some possible headwinds that can have an impact on its future performance and its share price.

At the moment there is a lot of turbulence in the stock market. BE Semiconductor has a beta of 1.46 , so it tends to move more than the market over time. Also the possibility of a hawkish FED and ECB can put pressure on the stock price of the company. Last year BE Semiconductor's share price has proven to be sensitive to a hawkish central bank policy. Inflation and further economic downturns can cause a slowdown in the demand for their products and can even lead to cancellations by costumers. Fluctuations in the macroeconomic environment are still likely to occur in the short term. The geopolitical and economic frictions between China and the US can also play a role for BE Semiconductor and might lead to trade disruptions and a potential negative impact on their revenue and profitability. Companies like ASML already has problems like this, because they aren't allowed by the Dutch government to sell their most advanced technology to China . This can also be the case for BE Semiconductor in the future. China has started his own state-sponsored initiatives to build their own supply chain, which is hard for BE Semiconductor to compete with. Since 75.9% of its revenue comes from Asia it can have a lot of impact.

Conclusion

BE Semiconductor is a market leader in assembly equipment for advanced packaging applications. The strong balance sheet, excellent profitability and revenue growth throughout the cycles and hybrid bonding as the main catalyst, BE Semiconductor has set itself in pole position for future growth. BE Semiconductor is also attractive for the dividend growth investor who does not rely on a year over year dividend growth. However, the total dividend growth on a multi-year basis should totally make up for it. There is a lot of turbulence in the stock market, inflation and geopolitical friction can put pressure on the share price in the short-term. Although the long term prospect of the company looks very promising and it is well worth it to do further research yourself.

I am bullish on this stock in the long term, but at the current share price I won't buy more. I also think that my assumptions used in the discounted cash flow analysis are quite conservative. On the short-term I give BE Semiconductor a HOLD rating. Personally BE Semiconductor is already my largest position and I took the opportunity to buy more shares around the $ 46 range. If it drops again to the $65 range I will be more than happy to add more to my own dividend stock portfolio.

For further details see:

BE Semiconductor: A Solid Dividend (Growth) Stock In The Semiconductor Manufacturing Space