BESVF - BE Semiconductor: Continued Underestimation But Now I Rotate

2023-12-27 06:08:05 ET

Summary

- BESI is currently overvalued, trading at a normalized P/E of over 60x.

- The company's earnings have dropped by 20%+ while the share price has tripled in less than a year.

- Analysts struggle to forecast BESI's performance, making it a risky investment at its current valuation.

Dear readers/followers,

If there's a single positive thing I can say about my thesis and my following of BESI, or BE Semiconductor (BESIY), it's the fact that I have a documented long position in the company that I have not yet sold. However, I've also made the mistake of underestimating the pathway to overvaluation that this company might take in an environment such as this.

Yes, I believe BESI to be firmly overvalued here - even more than in my last article. Even with the company's tendency to beat estimates, we have at €137/share levels where the company would need to average 30-35x P/E to really continue to deliver forward growth.

How problematic this is in the historical context and why this company is not a valid investment for me as a value investor any longer, is something I will show you in this article.

I'll also try and caution you, and show you why I'm so careful about being too positive on this sector.

I realize that much of this will be shouting on deaf ears. The entire market seems to be caught in an AI and Semi-mania at this time. That's fine. I have my own investment strategy, and it works for me - and in this specific case, I actually managed to include a few stocks where I now have triple-digit RoR from "tech".

This company is one of them.

Let's recap on BESI.

BESI - The company's upside after trading at over 60x P/E

Yes, you read that right. This company currently trades at a normalized Price to earnings of over 60x. You should go back in history to look at the exact situations when this has been a continuous trend for a longer period of time, say 5-20 years.

With certain ridiculous exceptions, you'll likely come up very empty when it comes to that list.

This entire sector is fascinating, especially given the trends we're now going into. In essence, what you're investing in here is betting on just "how high" the trends from things like AI and continued digitization are going to drive the results of companies within the sector. BESI is in a very good position to take advantage of this, despite a current forecasted earnings decline of almost 25% for the 2023 period. What BESI has been doing here for the past year, is trade in exact opposition to its 2023E earnings expectations.

The company has good qualities without a doubt. Being a massive market leader with customers including the largest electronics players on earth, the largest OEMs out there, no one doubts that BESI is doing well, or that its future is looking up.

But in less than a year, this company's share price has tripled.

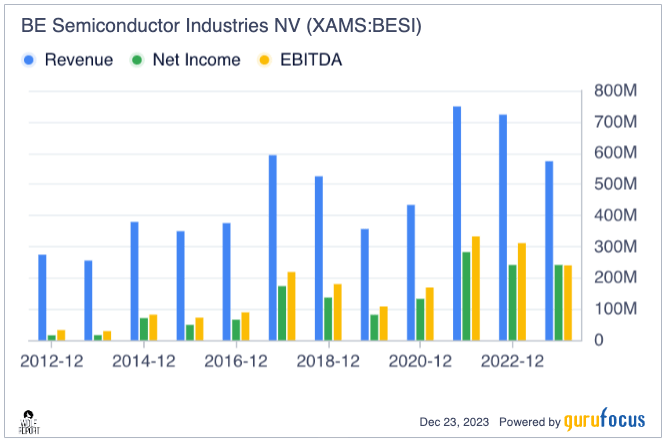

At the same time, the company's earnings have dropped by 20%+, and we're talking about earnings that look like this over time.

BESI revenue/net earnings (GuruFocus)

{kind=link}

While the company has certainly seen impressive growth, please note that much of that growth came in 2021. The current upswing is in no way based on significant, current earnings growth, but rather expectations. And whenever this happens, I become very watchful.

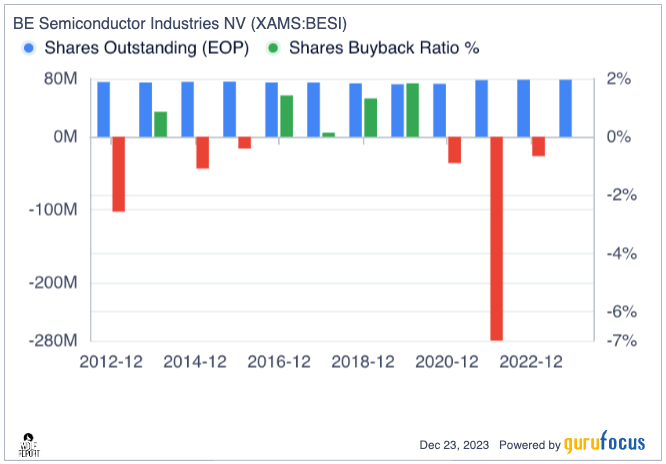

Let me point out other things that have happened in the past few years. Significant dilution and reduction in overall shareholder equity compared to how things were around a decade ago.

{kind=link}

I pointed to similar worrying underlying trends when I wrote on Altria (MO). I say the same thing here that I said there. None of these trends are in themselves cause for fundamental worry or concern, they're things to note and observe.

BESI has sector-leading margins and profitability - but at the same time, it's valuation on every single method, no matter how you estimate it - Asset values, tangibles, median P/S, Graham, Lynch, or DCF modeling, no model grounded in reality shows a valuation possible over €65-€80/share. And yet here're talking about almost double that.

The company without a second's doubt understands very well how to operate the very cyclical industry they're in. It's also optimized its assets and its workforce, with much of its staff working flex hours, and its focus on products with high-margin potential has been superb.

However, as with any cyclical industry, you cannot and should not underestimate the power of the swings , in this case, the swing going down. BESI also has an incredible level of revenue concentration, where the loss of even a singular customer would have dire impacts on the company's earnings and sales.

There's no doubt in my mind based on the latest set of earnings results and the overall industry forecasts, that BESI will enjoy double-digit growth rates going forward. Most foundries and device companies still have to build their hybrid assets, and this in turn will mean good growth for a company like BESI. I fully expect the Hybrid Bonding sector to account for over 40% of the company's forward revenue starting in -26 and -27, which also will ratchet up the overall service revenue - and this is high margin services because these machines cannot be serviced by third parties as many of the others can.

But no matter how you model the company's financials and upside here, I cannot find a single scenario outside of a hundred-percent growth estimate for several years, where this valuation actually makes sense.

The last quarter was as positive as we might expect - and the company's 2% yield is safe - obviously, my own yield is well above this, given that I invested in the low € 40s in this company - so you can imagine that I'm wishing I put $100k to work here. I obviously didn't - that's not how I invest, and this is not a situation or a valuation that I believe anyone could have reasonably forecasted.

However, now that we're in the situation we need to handle it.

I'm fully on board with the company's estimated growth. My own modeling shows a 50%+ growth rate potential going into 2024E and another 20-35% in 2025E. But the certainty of these numbers is highly in question.

BESI is one of the most cyclical industries out there. The company's cyclicality can be easily expressed in that analysts cannot forecast it. FactSet analyst forecasts have a miss rating of 100%. Not once, in a decade, have analysts even with a 10% margin of error managed to estimate where this company would go. They either miss the estimates negatively, most of the time at 58% , or the company beats them (the rest).

Usually, I would say beats are "good". But in this case, all it shows me is that BESI is a beast that no one can realistically forecast.

And that, when we're at 60x+ P/E, is a massive problem for me.

Let's look at Risks & Upside

Risks & upside for BESI

The core risk to BESI at this time, is without a doubt it valuation, which is incredibly inflated. No model I can find, no analyst I follow or that I can find, finds this to be a good target for the company. Some S&P Global analysts have raised their targets well beyond €80/share, but these are in a minority, and most following BESI are in agreement here - this is now a significantly overvalued company, and marks a real risk in terms of holding it.

How exactly continued growth will impact this company's valuation is unclear. It might grow to €200/share. Maybe it'll go to €1,000, and trade at over 200x P/E. But these sorts of scenarios are so far outside of my risk tolerances as an investor, that I will not invest in them, nor risk them.

You never know when the market "wakes up". Holding this one as long as I have has been a significant risk to me.

The continued upside is based on estimates that the valuation inflation will continue on here. I do not believe that to be a realistic potential, but it's a possibility nonetheless.

The valuation for the company is as follows.

Valuation for BESI

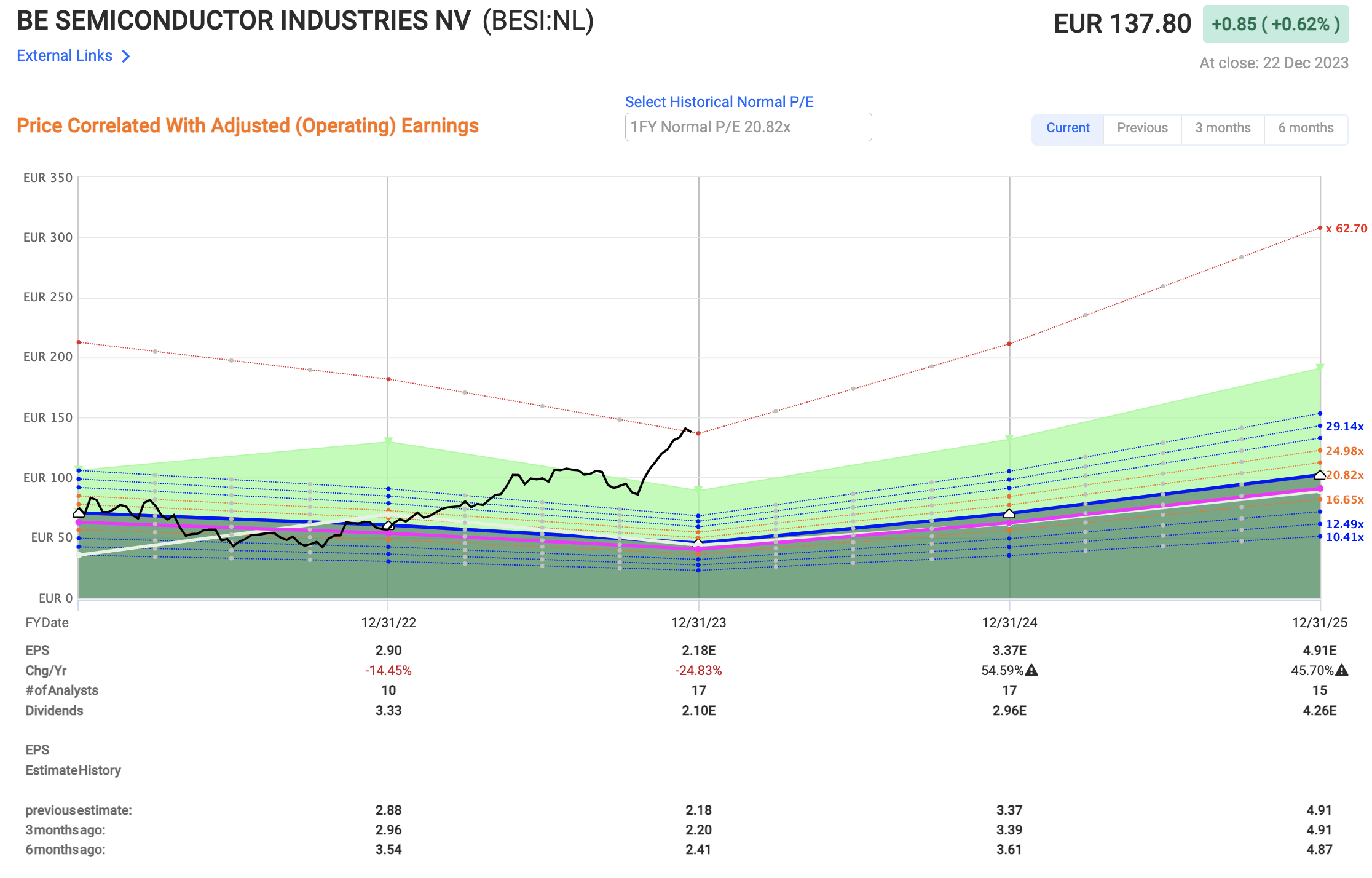

Going from my last article where the company traded at almost 40x, and I already rotated part of my position at a triple-digit profit, after going back in in a small way, I now am ready to more or less rotate the rest.

A simple graph should serve to illustrate the heights that this company has reached, and why I am no longer interested in owning it long-term when we have these price levels.

BESI Valuation (F.A.S.T graphs)

{kind=link}

I want to clearly point out that the long-term valuation trend for BESI calls for the company to trade at close to 16x P/E. That would imply a downside of nearly 40%, even with a double-digit 40-50% annual EPS growth rate. This is one of the most documented volatile businesses in the entire semi-industry , with swings that, if you do not recognize or act on them, can result in losses of 40-60%, just as was the case back in 2021-2022.

I've already held this far longer than I should have, given my risk parameters.

S&P Global analysts forecast BESI at a target range at a low of €85, which a year ago was €45, and a high of €150, which a year ago was about €95. The average here is €122/share, a year ago it was €70. Only 5 out of 17 analysts consider the company to be a "BUY" here, with over 12 considering it either a "HOLD" or an "Underperform". So while targets are up, the general sentiment is one I can get behind.

I want to make clear in this article that by the time it's published, I may no longer own any BESI shares. This may be something I have cause to regret if the company keeps climbing, but one risk I am willing to take - the other one I am not, based on my risk/reward considerations.

This one is a "HOLD" and here is my thesis for BESI updated for 2024.

Thesis

- BESI is a class-leading and market-leading company in the semi-sector, with several advantages over peers and similar companies. It has excellent RoR and a good yield but needs to be bought at a good valuation to offer a compelling, long-term upside. It can also be sold as sort of a trading play, offering good returns in the short term as well.

- However, the current valuation calls for a "HOLD" for the company, my PT is €84/share, up from my previous share price target of €79/share.

- What remains of my original position will now be trimmed in the next few weeks in order to ensure a no-exposure at these inflated valuation levels. "SELL" ratings for me imply a poor business, and BESI is not that - but the company is still risky enough for me to be very clear here that I view it as a rotation potential.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is neither cheap nor at an attractive enough upside. I'm calling it a "HOLD" here.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

BE Semiconductor: Continued Underestimation, But Now I Rotate