BESVF - BE Semiconductor Is A Superb Play But A 'Hold' - Here's Why

Summary

- BE Semiconductor is a very solid play on assembly equipment marketing - a crucial area in semiconductors.

- The company has a market-leading position in key sectors, and I have been following and learning about the business for several years.

- My investment in BESI has yielded an impressive return, but the near term looks different.

Dear readers/followers,

I've written about BESI ( BESIY ) a number of times before - enough to call it BESI and expect that you know I'm talking about BE Semiconductor Industries N.V., as the company is actually called. I've owned the company's common shares for about a year at this point and have taken advantage of significant undervaluation in the stock.

You can view some of my rating history on the stock here, and with the exception of the first bullish call which was, in hindsight, a bit early, I've mostly tried staying consistent with this company.

BESI Article (Seeking Alpha)

So, in my current update, I'm sticking to that consistency - let's see where we have this company basically going into 2023.

Updating on BESI

Before my previous article, BESI was an interesting undervaluation play that went on for months - and obviously, I've been making good returns on my position if you take a look at where I have been buying. Even the latest recovery, which we are currently in the absolute middle of, doesn't take away from what BESI offers its investors, at least not in the long term.

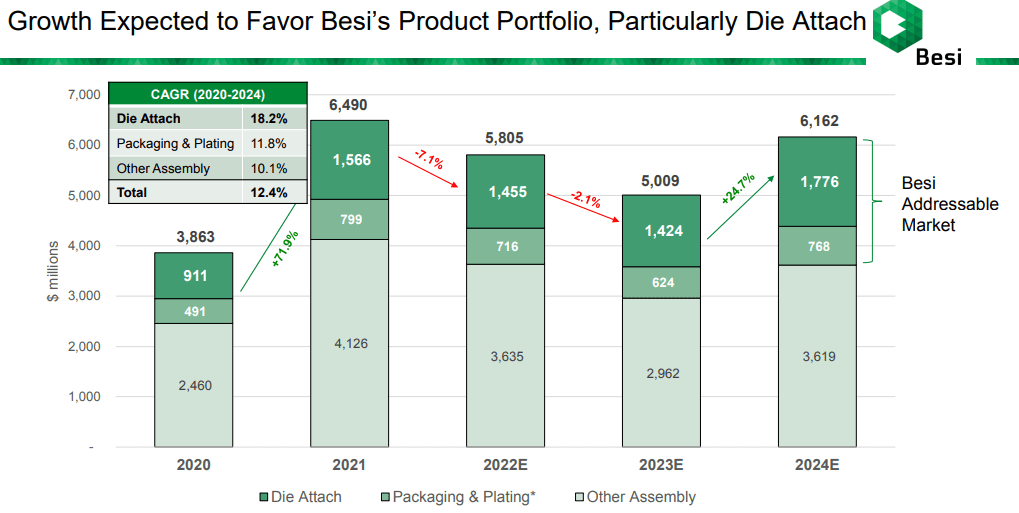

BESI is, to me, one of the safest semiconductor and semi-related plays out there - bar none. The company in its role as an assembly equipment supplier is crucial to the entire semi-industry. Despite being relatively unknown, it has #1 and #2 rankings in some key markets, and boasts, according to company info, a market share of no less than 32% in terms of addressable market share. Without assembly equipment manufacturers, the semi-world as we know it would grind to a halt, and BESI as a business is among the top-tier manufacturers, with customers and products like this in its arsenal.

BESI IR (BESI IR)

You're looking at a die attaching, packaging, and plating company - for more illustrative descriptions that go much deeper into things here, I would revisit some of my earlier articles on the company - I go through it more in-depth there, to the degree that you as an investor may need to know about what the company does.

The company's operations can be found across the world, with factories or offices in six countries, and the company's China exposure means it has some exposure to the current troubles there as well.

BESI is a standard and very traditional (as I see it) value play. The company must be bought at the trough or below fair value to make up for the following issues in its corporate/investment profile.

- The company's dividend safety is sub-par, based on a very volatile historical trend. BESI pays out what it can, but in downcycles, which we may be on the way into now, that payment is historically going to trend in one direction - down.

- There's no credit rating to speak of, even if the company can be considered "safe".

- Gauging or measuring BESI or forecasting the company is tricky due to its size and specialization. If you don't buy it cheap, you risk exposing yourself to extensive periods of a downward trend.

Now, how can such a company really be considered "safe"? Because at first glance, it might not fulfill the "safeties" I speak of.

However, I have hours and hours of looking through financials and models, and there are very few overall risks, beyond what macro and the sector specifics tell us. Again, this is a cyclical segment, and currently, analysts and the company's own forecasts tell us we might be on the way into a downcycle.

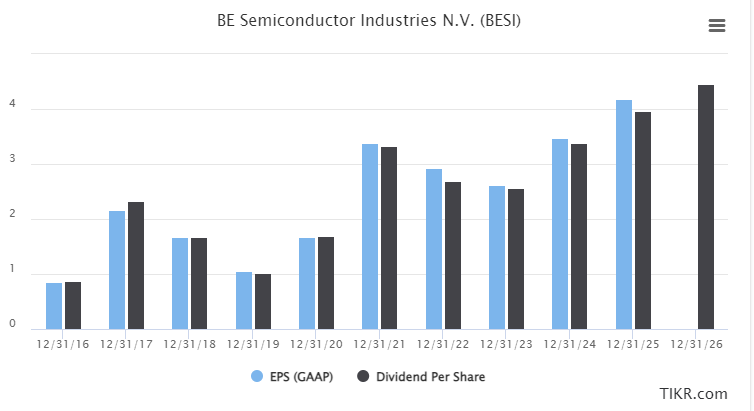

These are the current expected EPS trends for BESI.

{kind=link}

As you can see, company deliveries and macro are likely to see declines in FY22 and FY23, impacting not only EPS but the dividend given how high the payout is. S&P Global is seeing these trends, FactSet analysts are, and the company forecasts are seeing the same trend.

The BESI downcycle began in mid-2022, or around there. The specific trends are GDP growth and inflation , as well as higher interest rates. There is also the capacity for the market to absorb the capacity and volume that BESI is bringing to market, due to how high the last upcycle went. That upcycle ended in late 2021.

Mobile and Cell demand are down - especially for high-end, coming out of both iPhones and other major manufacturers. COVID-19 lockdowns have been a major impact as well, and slowing growth across the world in data centers and automotive have seen the company's near-term forecasts go down as well.

There are continuing disruptions to the global supply chain - and two growing conflicts between the US/China and EU/US and Russia, all of which are impacting things.

So, it's not an easy macro environment the company is working with here, and that is what forecasts are seeing, despite the market leadership and positioning the company has.

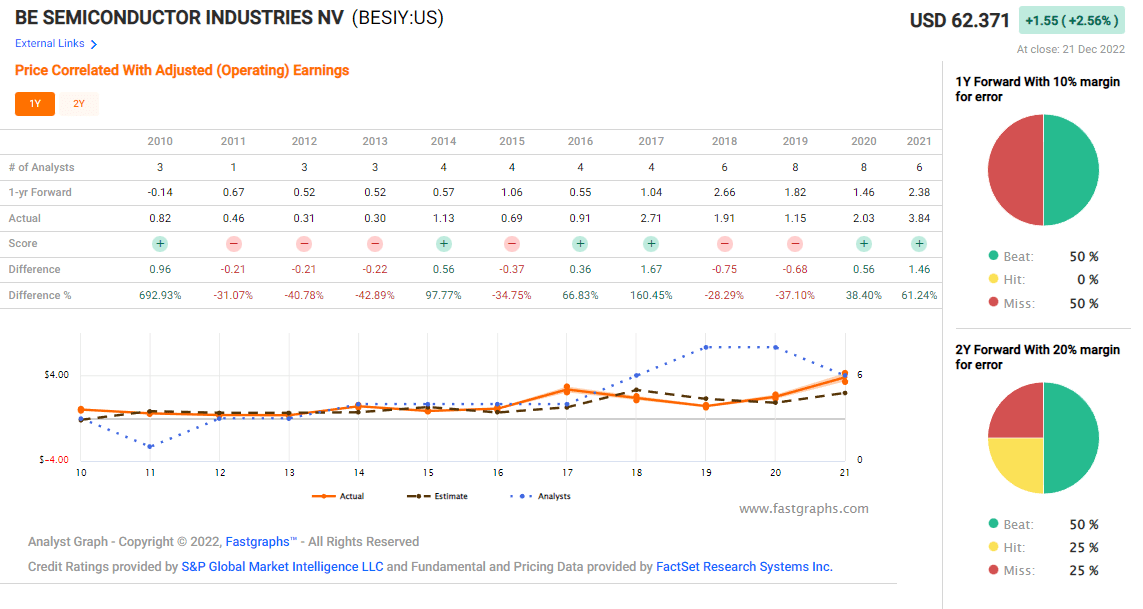

However, there aren't just negatives here. I told you that there comes a downcycle here - and I believe that. But there will come a reversal as well, and the company's supposed visibility for this is good as well.

{kind=link}

The same upcycle beginning is being forecasted by analysts following the company as well.

The uncertainty here lies in how deep the downcycle goes, how long, and how strong the upcycle is. That part is the tricky thing here. Main and fundamental trends continue in the company's direction. We're talking about advanced packaging being critical for future applications, higher density requirement, and transistor scaling, new 3d structures, and hybrid bonding - all of which the company is targeting.

But we don't really want to "BUY" the business at any price - and that's my point here. Let me show you.

BESI's updated valuation

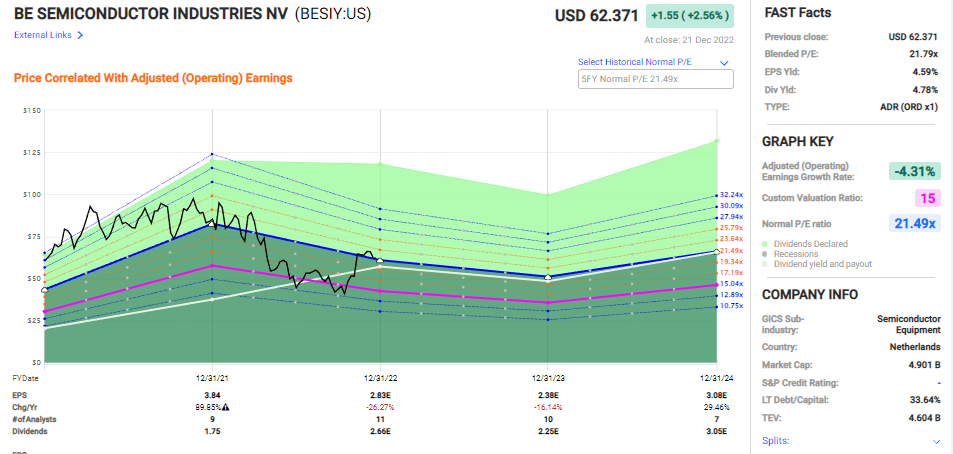

The company trades at ranges between 15-20x, with 20-22x P/E being the typical premium that the company, by the market, typically warrants. However, this time around, I want to show you some of the problems with that valuation and those forecasts - namely that forecasting this company's stability, going by historical data, seems next to impossible even with high accepted margins of error.

{kind=link}

The company's EPS yield is now below 5%, and this is despite what would be considered a baseline normalized Premium of 21.7x P/E. It's almost exactly the 5-year P/E of 21.5x. But even where the company is at 21.5x P/E, I wouldn't be investing in BESI at an incoming downcycle.

The fact is, earnings this year are very likely going to be down. 2023 is going to be another down year. To me, that translates into one simple reality going forward.

Most of the upside has been earned here, and things are likely to remain pressured and probably even move down even more.

{kind=link}

And even if things don't drop down, but remain at 21x or even go up to 22-23x, the upside is nothing beyond mere double digits at this time. At 21.5x, the upside is 2.5% per year. That's not enough to get me interested, and it shouldn't be enough for you.

This is the sort of business you want to buy when everyone is telling you what garbage the company is - and you know your stuff and the company - as I do.

That's why I was loading up on BESI's native shares back during the past few months, and why I haven't bought in a little over a month at this point. BESI not that long ago traded at multiples of 13.5x P/E.

That's the trough valuation for this company, at least historically.

I certainly did not expect the massive bounce that resulted in market-beating returns for my position, and this overreaction was enjoyable. I have since sold off about 55% of my position in small cuts, and I'm probably going to continue trimming here.

Why?

Because the visibility of the downcycle is very high - and there are companies with significantly better upsides than we're seeing here. The market overreaction this time puts BESI above its premium at a time when earnings are expected to go down, not up. Take very good and close notes of these cycles, because they very much steer the way this company goes.

As you can see, at current valuations and trends, BESI is trading at a "full" and above valuation for this year's results, and at an above premium for the next year at least.

In my last article, I wrote this:

You might look at this and wonder if it could not be time to rotate or reinvest part of the position here. I would say that is a very good consideration to start looking at this point. We're still in a fluctuating market, and despite BESI being a very fundamentally attractive business with sound forecasts, a 30-40% RoR as I have on parts of my position isn't something that should be ignored, if that money can generate equally safe returns at better valuations elsewhere.

I've done exactly that. My position in BESI has started to be seriously cut down - and I'm planning to slowly continue this if we see more expensive valuations. The important thing here is that if you invested in BESI, you don't sell quality at a loss - at least I don't. I was up 35% when I started trimming my BESI position - and it's even better now.

I've reinvested that capital at very attractive overall valuations with far better upsides than BESI. The company's current valuation targets can be summarized as follows.

We've seen a significant reduction in the relative street targets for BESI. 10 analysts now follow the company - up from seven when I started, and the share price they give the business is down from almost €100/share for the common back in March and €80/share back in June when I did my heaviest buying at below €45/share, and it's now down to below €69/share, from a range of €55 low to €90 high. To compare, the high back in March was €160.

Viewing things conservatively is absolutely crucial, as I see it. I sold most of my stake above €63/share. The ADR is currently at $62/share, and my last PT was $65. I do believe it's worth over $60 in the long term, but I'm shifting my target down $5 to $60/share to account for the significantly higher near-term valuation risks.

Based on this, I remain at my "HOLD" stance for BESI, and that is my current justification for it.

Thesis

My thesis for BESI is as follows:

- BESI is a class-leading and market-leading company in the semi-sector, with several advantages over peers and similar companies. It has excellent RoR and a good yield.

- At the right valuation, BESI represents a solid "BUY", and I've been loading up on BESI since this past March.

- However, the current valuation calls for a "HOLD" for the company, my PT is $65/share.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is neither cheap nor at an attractive enough upside. I'm calling it a "HOLD" here.

For further details see:

BE Semiconductor Is A Superb Play, But A 'Hold' - Here's Why