BESVF - BE Semiconductor: Might Go Lower Upside Beyond Trough

2023-03-17 10:23:48 ET

Summary

- I'm looking at BESI after a significant bout of outperformance contrary to my expectations from my last article. I'm LONG BESI but at a very attractive price point.

- In this case, I'm looking to find the price target for the 2023-2024E period, given the trough the company is currently in, and how this influences things.

- Here is my 2023E thesis for BESI - with a new, updated price target.

Dear readers/followers,

My last article on BE Semiconductor ((BESI)) (BESIY) (BESVF) was at a "HOLD", despite the rating which later turned out to be correct ("BUY", but my stance in the article was "HOLD), saw the company massively outperform overall indices despite going into 2023 with an expected decline in EPS.

BESI Article (Seeking Alpha)

In this article, I'm revisiting BESI - a company I believe you want to own, but you might not want to be "BUY" ing here at this time. To be clear, I'm taking a firm stance as a "HOLD" here, with a new PT for 2023.

BESI - It's expensive for the short term, but with a slight upside in the long term.

My position in this company remains relatively limited, unfortunately - but it's an investment that's firmly in the green despite overall market turmoil in both this and other segments.

Then again, it shouldn't perhaps be a surprise that the company with market leadership in a key industry in Semi's pretty much just gives a shoulder shrug to global turmoil and interest rate issues, as well as chaos in the financial sector.

BESI IR (BESI IR)

BESI, since my last article, has posted pretty great results, despite the current set of forecasts and issues both in the industry and the macro side.

Why am I so confident in this company's long-term prospects?

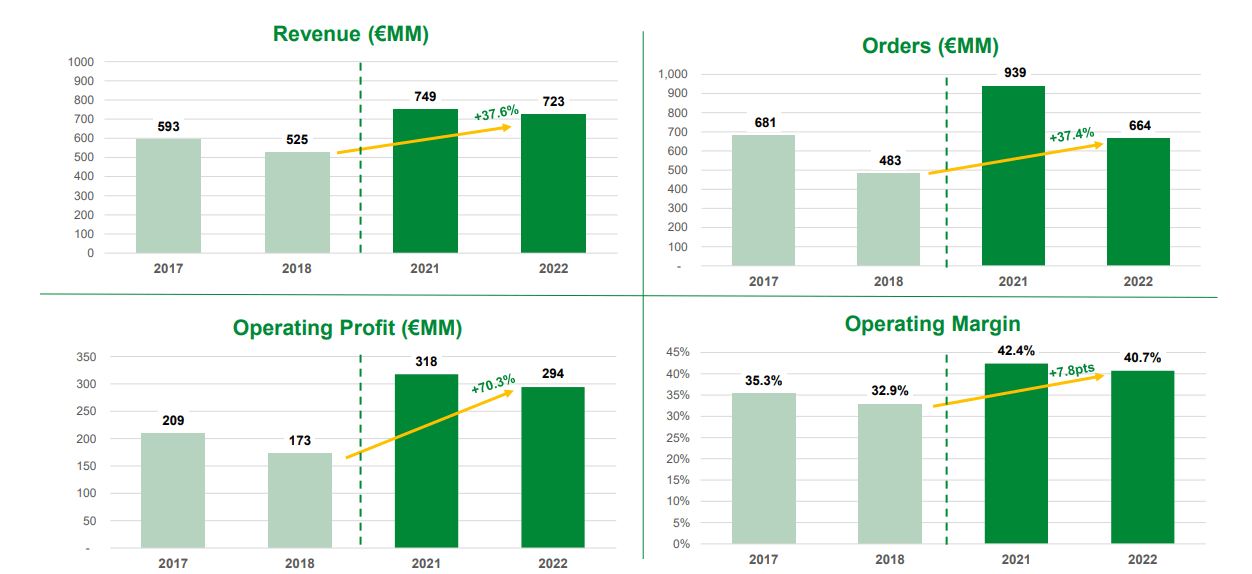

Because simply put, the company's current performance is significantly above where things have been in terms of the last industry cycle, which we saw between -17 and -18. Comparing 2018 troughs to 2022 troughs showcases massive, double-digit increases in revenue, operating profit, operating margin, and order sizes/volumes.

{kind=link}

2022 was, furthermore, a year of massive capital allocation in both dividends and share repurchases, with 2023 expected to be a down year, at around 3/5th s of the same volume. The company distributed over €400M worth of capital in 2022, which is a 132% increase to 2021 and is still working through a €300M buyback program that started back in August, part of the explanation for the company's excellent trends here.

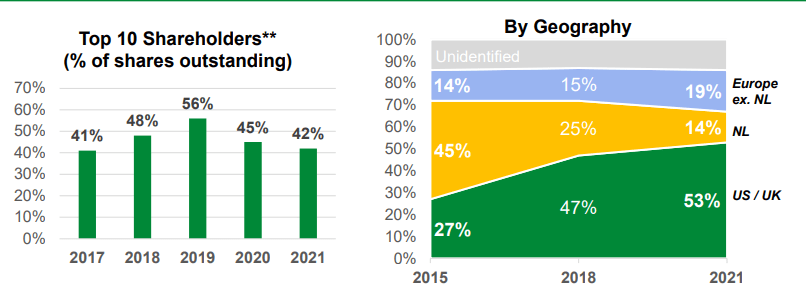

BESI has seen a significant market cap expansion compared to the last 5 years, and an internationalization of its shareholder structure, with major shareholder positions going from local NL shareholders to US/UK, a typical sign that a publically traded company is growing. This graphic expresses this trend fairly clearly.

{kind=link}

The company has also set new targets for the coming 3-4 years. This includes revenue well over €1B, growing its addressable market share to 40%+, and improving and maintaining GM between 57-62%. with a corresponding net margin above 30%, and as high as 35%. The company wants to improve the headcount split as well, doing an 80/20 between Asia and Europe respectively.

The high-level upside for this company is unchanged. The reason I'm convinced that BESI will outperform going forward is the company's correlation to macro GDP trends, the increasing technical demands on the technologies which BESI serves and offers, and the competition - where BESI is really bigger than most.

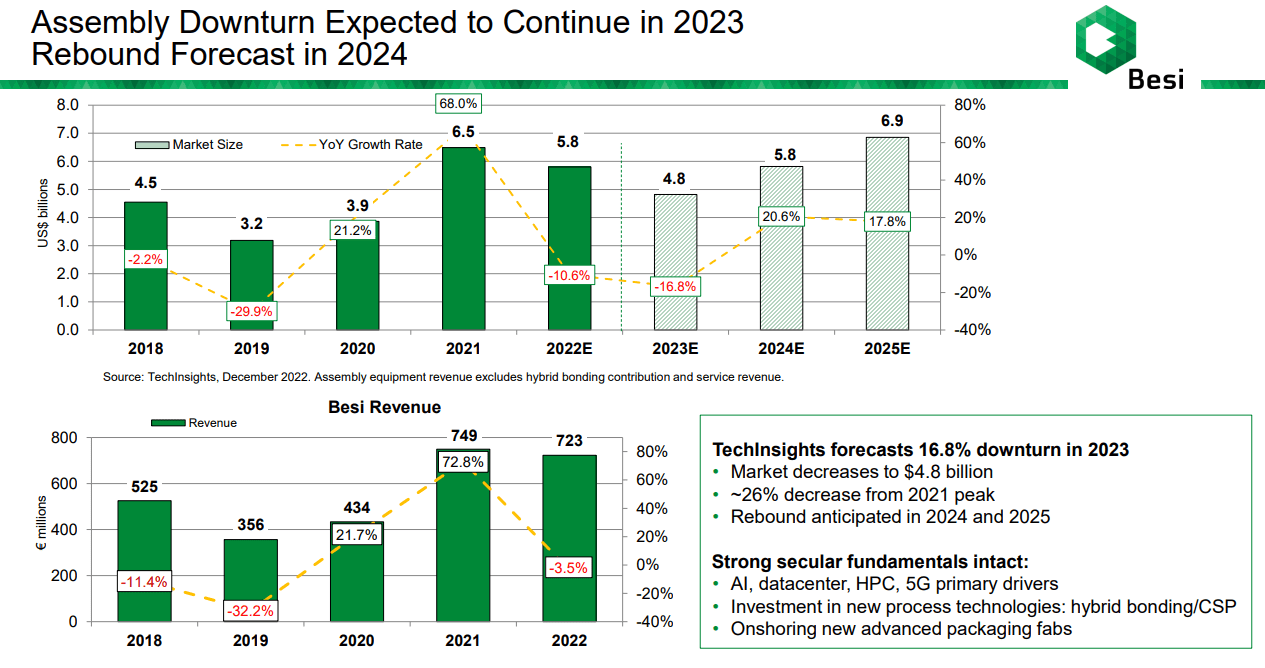

BESI has been expecting this industry downturn for some time - it was already in full swing back in 3Q22, beginning about 2Q22, and the company has historically been very apt at forecasting these specific trends. But this also includes when the market is expected to turn back up again.

{kind=link}

Because from a much higher level, the long-term semi-trends are completely unchanged. The demand grows and is set to expand even more going forward.

We're talking about things like Big Data, AI, Quantum, and other things. I'm not typically a tech-friendly or tech-positive sort of investor, but when it comes to what I choose to invest in this sector. BESI is right up there. It's in #1st place, along with companies like SAP (SAP) and other data, IT leaders, and other businesses which even compared to giants like Google ( GOOG ) can be said to be relatively independent - and Google of course has a certain degree of independence as well, given the penetration of its services. However, given BESI's expertise in the die attach sector, I consider it to actually be more "core" than even something like Google, in some ways.

Still, the company has some fundamental valuation issues as an investment that need to be fulfilled before it can be invested in effectively. These also include considerations - and these are the following:

- The company's dividend safety is sub-par, based on a very volatile historical trend. BESI pays out what it can, but in downcycles, which we may be on the way into now, that payment is historically going to trend in one direction - down.

- There's no credit rating to speak of, even if the company can be considered "safe".

- Gauging or measuring BESI or forecasting the company is tricky due to its size and specialization. If you don't buy it cheap, you risk exposing yourself to extensive periods of a downward trend.

I've been through earlier why this company is safe, despite the lack of an overall credit rating. You can find the case for this safety in articles like this one here .

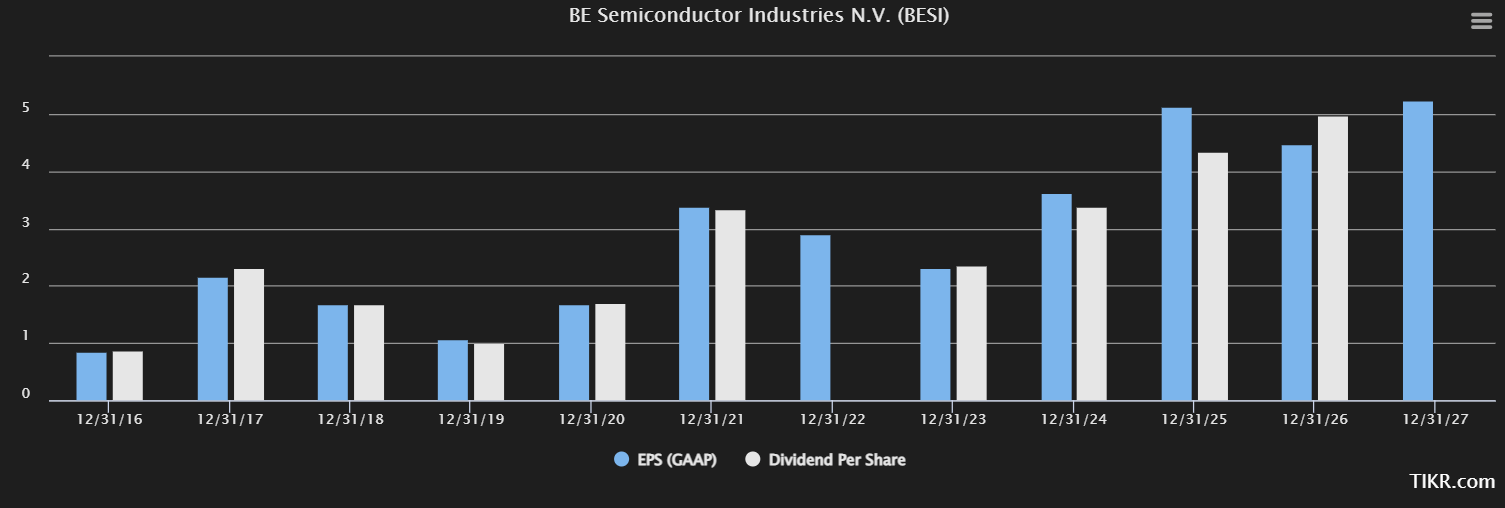

Here are the currently updated expectations as from S&P Global for what is likely to happen to BESI's earnings here.

BESI forecasts (S&P Global/TIKR.com)

{kind=link}

The company remains heavily correlated to the overall semi industry and its ups and downs. The BESI downcycle began, as I said, in mid-2022, or around there. The specific trends are GDP growth and inflation , as well as higher interest rates.

There is also the capacity for the market to absorb the capacity and volume that BESI is bringing to market, due to how high the last upcycle went. That upcycle ended in late 2021.

That's why things will go down this year, and this coming year. Remember, cell phone demand seems to be teetering a bit. COVID-19 lockdowns have been a major impact as well, and slowing growth across the world in data centers and automotive have seen the company's near-term forecasts go down as well. This is not even accounting for global supply chain disruptions and the ongoing conflict in Ukraine.

However, this will turn around eventually, and inventory/demand with those trends as well, which in turn will drive demand upward again, currently expected in 2024 and beyond.

Based on this, and expecting the trough to continue this year, I look at BESI the following way from a valuation perspective, and when it comes to assigning the company a new PT for the coming year.

BESI's valuation - how deep can it fall during the trough?

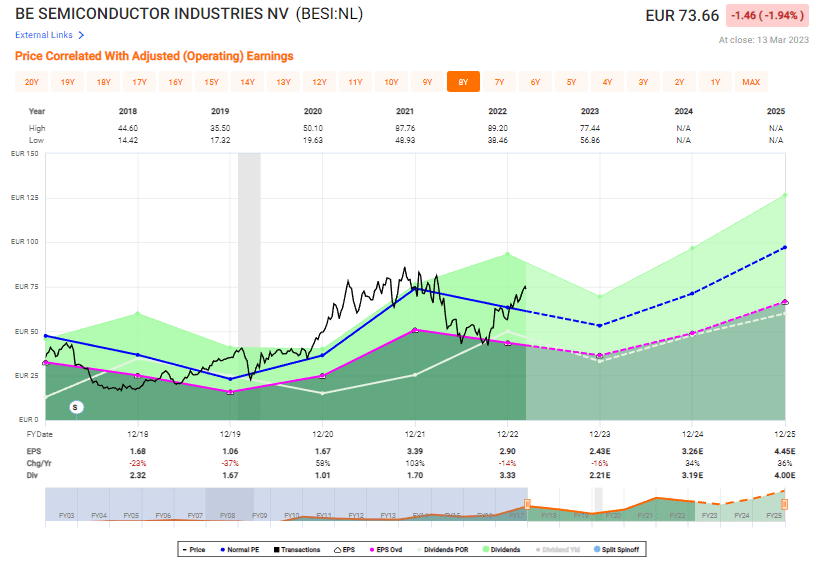

So, the company is currently expecting a low during 2023. That means the valuation this year will have to "fight" against the trends on a quarterly basis, which is difficult in a position of inflation, cost increases, and global macro. This visual representation of where earnings might go this year is a good example of what you may expect.

BESI Valuation (F.A.S.T graphs)

{kind=link}

Be careful and don't underestimate how volatile this company be, is what I can tell you here. Look at how low the company has gone, only a few months ago, and how overvalued it can be. Then look at how high it currently is, relative to its overall expectations.

The company might be able to bridge the negative expectations for 2023, but betting on that is a bit too far, as I see it. The long-term thesis for BESI based on a 21x forward P/E gives us a €97/share PT, which currently implies a 13.9% annualized RoR, or 44% until 2025. But again, this assumes bridging that negative EPS gap - which might, or might not happen.

This is a risk/reward consideration and given a 3-4% yield even in a positive case, it's not a risk/reward relationship I consider to be favorable at this particular time. The current analyst targets from S&P Global more or less confirm the problematic picture here, with a target range of €55 up to €94, with an average of €75.5, with a current price of €74/share. Even based on relatively bullish estimates, the upside is less than 4%. Out of 11 analysts, 6 are either at "HOLD", underperform, or don't have an opinion on the company.

Before, the EPS yield for the company was below 5%. Now it's below 3.9%. I believe whatever upside was present in the stock is now gone. from here, it would take a complete break from historical premiums to send the stock trading higher - and through a combination of fundamentals, forecasts, and company expectations, I don't see there being a massive further positive case to be made here.

This is the sort of business you want to buy when everyone is telling you what garbage the company is - and you know your stuff and the company - as I do. That's why I was loading up on BESI's native shares back during the past few months, and why I haven't bought in a little over a month at this point. BESI not that long ago traded at multiples of 13.5x P/E.

Compare that to where the company is now - over 20x. Valuation really is a big part of things. If you can get a quality company at discount, that really brings things in a positive light. I certainly did not expect the massive bounce that resulted in market-beating returns for my position months ago, and this overreaction was enjoyable. I'm now at around 20% of my original position, and what I have left are things I am like as not to hold, not divest further. But I made over 60-70% profit with my investment here.

Why am I trimming, and being relatively negative here?

Because the visibility of the downcycle is very high - and there are companies with significantly better upsides than we're seeing here. Especially after the financial crash, we've seen over the past couple of years. Viewing things conservatively is absolutely crucial, as I see it. I sold most of my stake above €70/share in the end, and I'm very pleased with this selling price.

As of this article, and based on the aforementioned expectations and forecasts, I'm going with the following thesis on BESI.

Thesis

My thesis for BESI is as follows:

- BESI is a class-leading and market-leading company in the semi-sector, with several advantages over peers and similar companies. It has excellent RoR and a good yield but needs to be bought at a good valuation to offer a compelling, long-term upside. It can also be sold as sort of a trading play, offering good returns in the short term as well.

- At the right valuation, BESI represents a solid "BUY" - but most of my position at this time is down to around 20% of my original stake.

- However, the current valuation calls for a "HOLD" for the company, my PT is €68/share.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is neither cheap nor at an attractive enough upside. I'm calling it a "HOLD" here.

For further details see:

BE Semiconductor: Might Go Lower, Upside Beyond Trough