BESVF - BE Semiconductor: Now Buyable With A Large Upside

Summary

- With the bottom dropping out of much of the tech space, quality companies that traded at more than 22x P/E only a year ago have dropped to sub-16x P/E.

- BESI is a solid tech company that I consider highly investable at this point - and in this article update, I'll show you why.

- I was a "BUY" on BESI before - I'm even more of a "BUY" on BESI here.

This article was published on Dividend Kings on the 23rd of August.

In this article, we'll take another look at BE Semiconductor Industries (BESIY) (BESVF). I've reviewed the company before, and I believe that after another 8-9% drop, the time is ripe to update my thesis for the business and why I consider it a "BUY" here.

If you read my initial article, you'll know what the company does. It does assembly equipment for semi-manufacturing. It might be relatively unknown as far as the larger tech space goes, but this company is, in part, a market leader in the entire space, with a #1 and #2 market share in some key areas.

Let's look at the most recent set of results.

BE Semiconductor Industries - An update

There is a reason why I consider BESI to be an interesting and undervalued opportunity in the sector. I've covered the company in previous articles and established a basic thesis for the business.

The company seemed appealing two months back when things dropped in the tech sector. Since my article, the company has dropped yet another 2.5% while the market has recovered close to 10%. So without needing to look in detail at the company's valuation, I can say that BESI is even more attractive now than it was a few months back.

Remember, this is an assembly equipment supplier. Despite being relatively unknown, it has a #1 and #2 in some key markets, and boasts, according to company info, a market share of no less than 32% in terms of addressable market share (not the market share the company actually has).

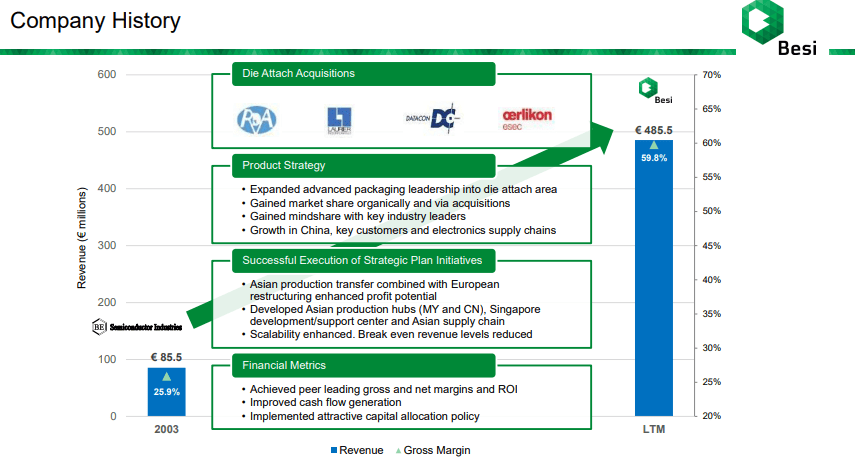

The company's operations can be found across the world, with factories or offices in 6 countries. As of 2020, the company has 1,901 employees, and it's headquartered, as the N.V. suggests, in the Netherlands.

{kind=link}

The argument here is the importance of its operations. We could speak at length about the company's business and specific processes. The process of die attaching or die-bonding semis, is the process of attaching a semiconductor die to a package, substrate, or another die. Examples of attachments are things like PCB boards. It works to essentially place the semi-device on the next level of interconnection, be this another substrate or a board. This is used in virtually every industry that uses semis and can be differentiated between adhesive bonding, eutectic bonding (attaching using a metal alloy), solder attaching (using solder or paste), or flip-chip attaching, using electrical interconnection by inverting the die on a face-down manner onto the package or substrate.

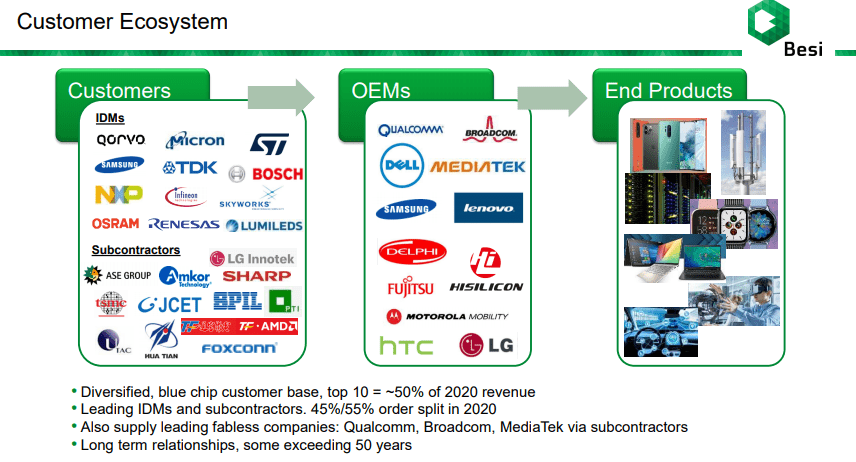

But in the end, what's important is that our modern semiconductor world would not function as it currently does without this process or even BESI's products. Take a look at some of the company's customers.

{kind=link}

I make a clear case for why this company is fundamentally attractive in my very first article BESI - as well as some of the overall risks that should be considered prior to invest seriously in the business. But the latest set of results does show a bit of encouraging trends here.

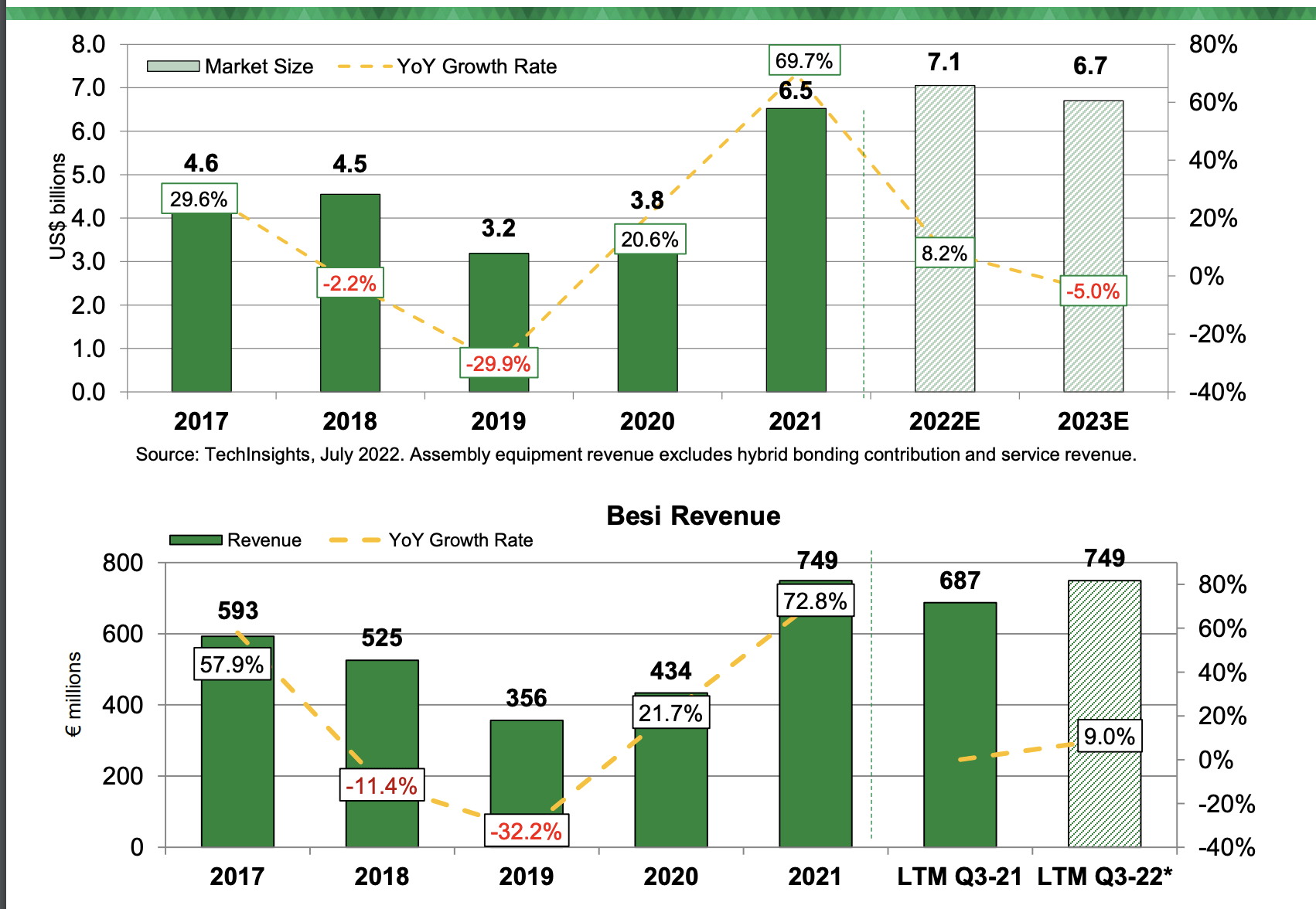

What's important to consider is that the company's gross margins, despite everything, really haven't seen any sort of drawdown but have stayed steady at above 58%, while revenue has steadily been climbing toward the €1B mark. This is also the company's target - to increase revenue, the TAM market share, to maintain that 58-62% GM level, and a net margin of above 35%. The company manages this at this time.

I'm personally not that interested in BESI's ESG ambitions, more interested in the headcount split targets and the capital allocation trends. BESI has distributed over €300M YTD already, including share purchases. This is already more than 3x the capital allocated to shareholders in all of 2020 and nearly double the 2021 level.

BESI is a perfect example of a company that's highly correlated to high-level macro and being the best at what they do. The assembly equipment market is a highly demanding market in terms of the production environment - because these environments usually run 24/7, putting a high demand and strain on the company's products.

The company's current forecast calls for a relatively stable, high-level Assembly market with revenue sticking very close to the current levels.

{kind=link}

There was a small, general deterioration of overall market conditions in 2Q22 due to CapEx hikes, a slowing world economy, inflation, shortages and continued COVID-19 issues in China. But the bullish thesis for the company is still mostly intact. EUV adoption, IC expansion, 5G and 5nm expansion, and the overall increased use cases for these technologies will continue to drive things upward.

These growth expectations in a very real way favor the company's portfolio, in particular, the die attach market. There are no realistic scenarios where the company's business sees significant deterioration fundamentally, and where revenue or net income craters. The expected 2022E growth of 20% for die attach technologies in terms of revenues, and 2.5% in the year after is even on the conservative side, all things considered here - even if earnings themselves are actually expected to drop in 2022E.

The fundamental upside for BESI is beyond cyclical tendencies and trends.

{kind=link}

Based on this, I see any significant drop-down to conservative levels as a "BUY" potential here. And I believe, very realistically, that this is a situation we are currently in.

Now, the company has no credit rating. It's a $4B market cap Semi company with around 34% debt/Cap, with both a native Netherlands listing and an active, liquid ADR called BESIY, which we are currently looking at. The company's fundamentals, however, can be seen as very positive in the long term. While the company has definite cyclical tendencies, the margins and revenue tendencies over an averaged-out through-cyclic perspective is impressive, and BESI considers a 4-year cycle to be the average of what the company is seeing.

This company carries extremely strong gross margins of over 60% at times, related to the company's "flexible" Asian production and workforce. BESI also executes extremely tight overhead management, which leads to a very significant operating leverage with excellent baseline OpEx based on the company's revenues.

The company holds to its dividend policy of paying out 40-100% of net income each year and seeks to expand its current €4-5B market cap.

BESI's native ticker is on the Euronext AEX market, and the top 10 shareholders own 45% of SO. Most of the shareholders are either from the US/UK (57%) or NL (17%). Foreign shareholding from the US is small.

Let's look at what the valuation looks like - because this looks very interesting now.

BESI's Valuation

This is not the sort of company you want to buy at expensive multiples when its everyone's darling. This is the sort of business you want to buy when everyone is telling you what garbage the company is - and you know your stuff.

The company has traded down significantly, and while it's no longer troughing at 15x P/E lows, it's still pretty damn low here.

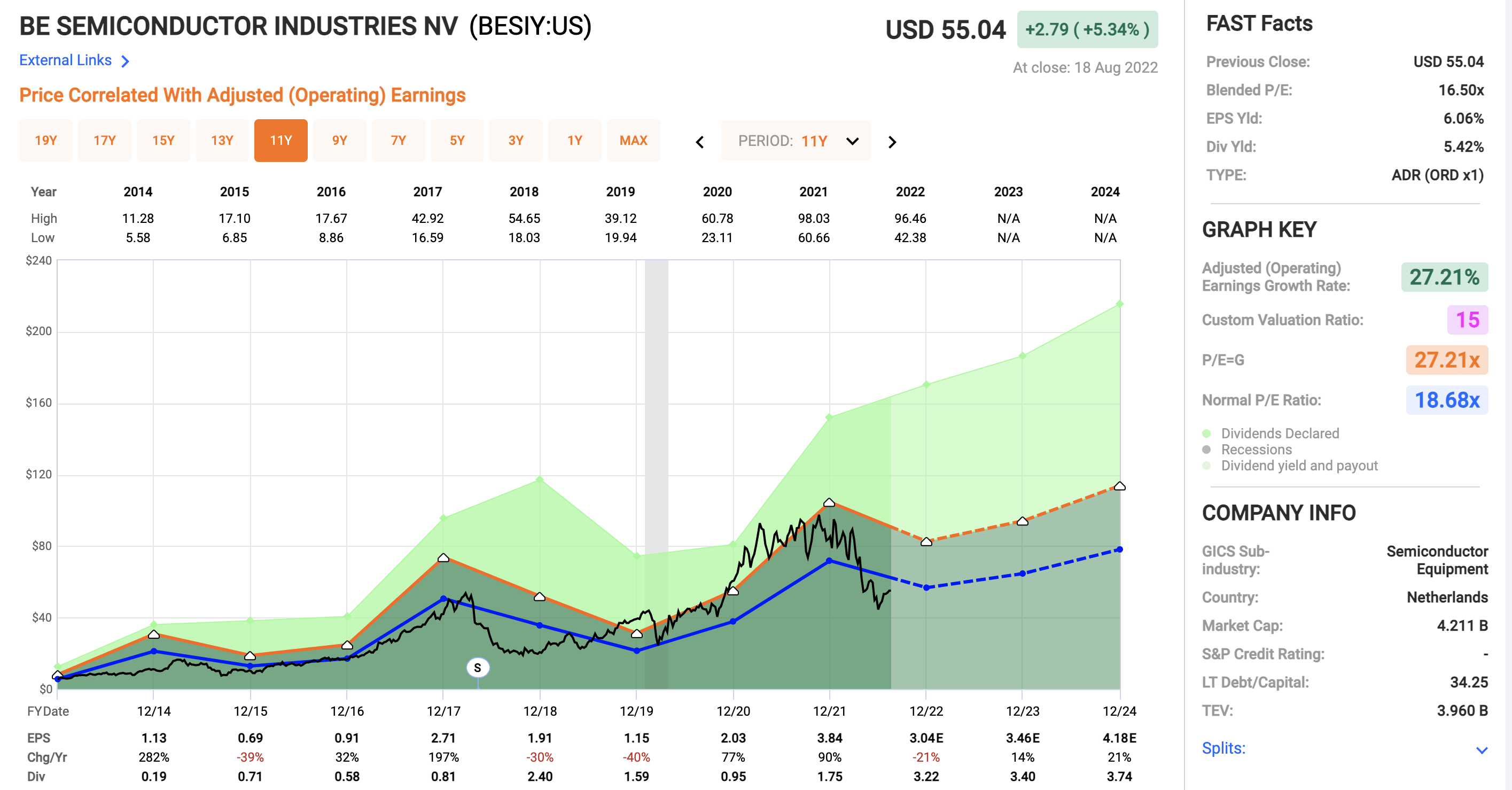

BESI valuation (F.A.S.T Graphs)

{kind=link}

Note the cycles. Note the way the company moves from ups to downs and back again. Note that despite the drop in 2022E and the expected bounce in the coming years, the company is trading lower than it has for very many years - since 2018, I would argue.

This stance is not based on actual, believable forecasts.

What makes me say this?

I want you to look at current EPS forecasts from S&P Global, coupled with considering the company's market position.

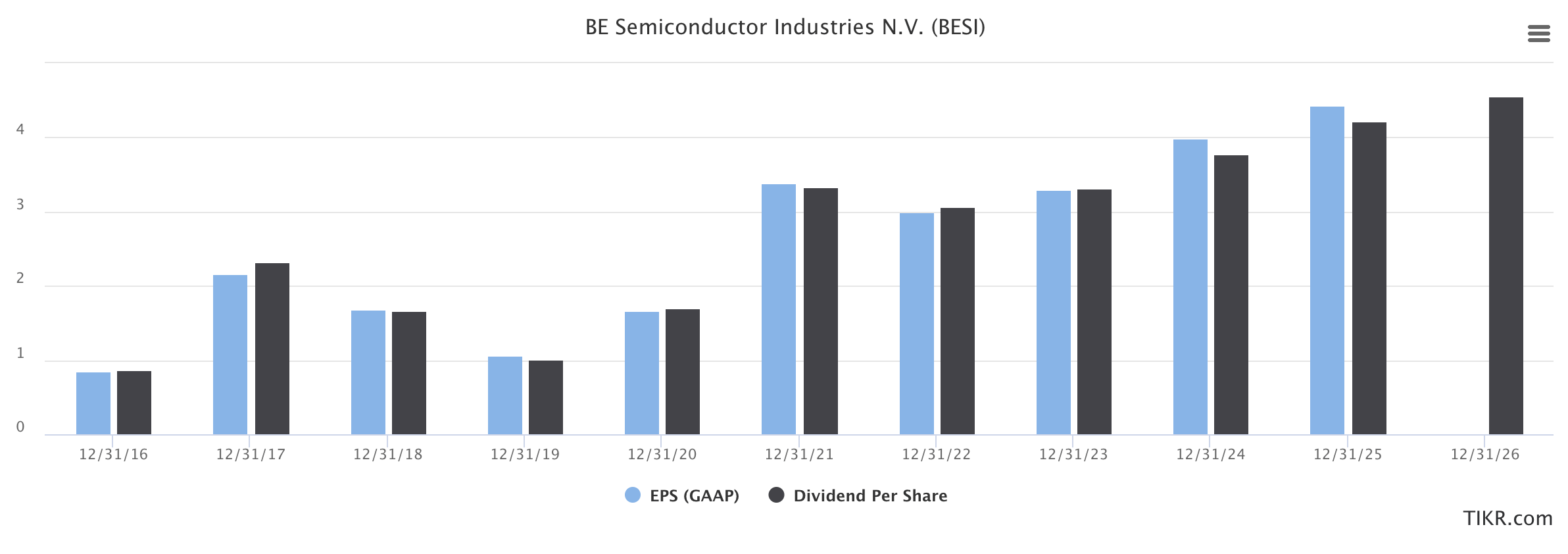

BESI Forecasts (TIKR.com/S&P Global)

{kind=link}

I also want you to consider the fact that the company's gross margin is expected to expand over the coming years to around 61-62%. I want you to know that analyst forecast accuracy is over 68% here, with a tendency of 48% on a 2-year forward basis for the company to actually significantly beat overall estimates (Source: FactSet). While it's tough to forecast, there is a trend here.

My last stance for this business was a "BUY". I'm still at a "BUY", but I'm lowering my PT to account for the changing market dynamics. BESI was at $78/share for the ADR initially, I'm sticking to my earlier $65/share. This is still at a premium, allowing for the company to grow to slightly beyond that 15X P/E, but it's well below any sort of valuation that's currently the average for analysts.

It's a proven company that's delivered returns of no less than 4 00-500% in less than 6 years , and that's even after the current crash. If you'd sold closer to peak valuation, your RoR would have been around 850%.

This space is exciting if you can buy the right company at the right price.

I believe BESI Is a sort of "right" company, and I do believe that at below 16-17X P/E, we're at a good price.

That's why I'm still a "BUY" here, and why I am now getting more excited about the company's prospects.

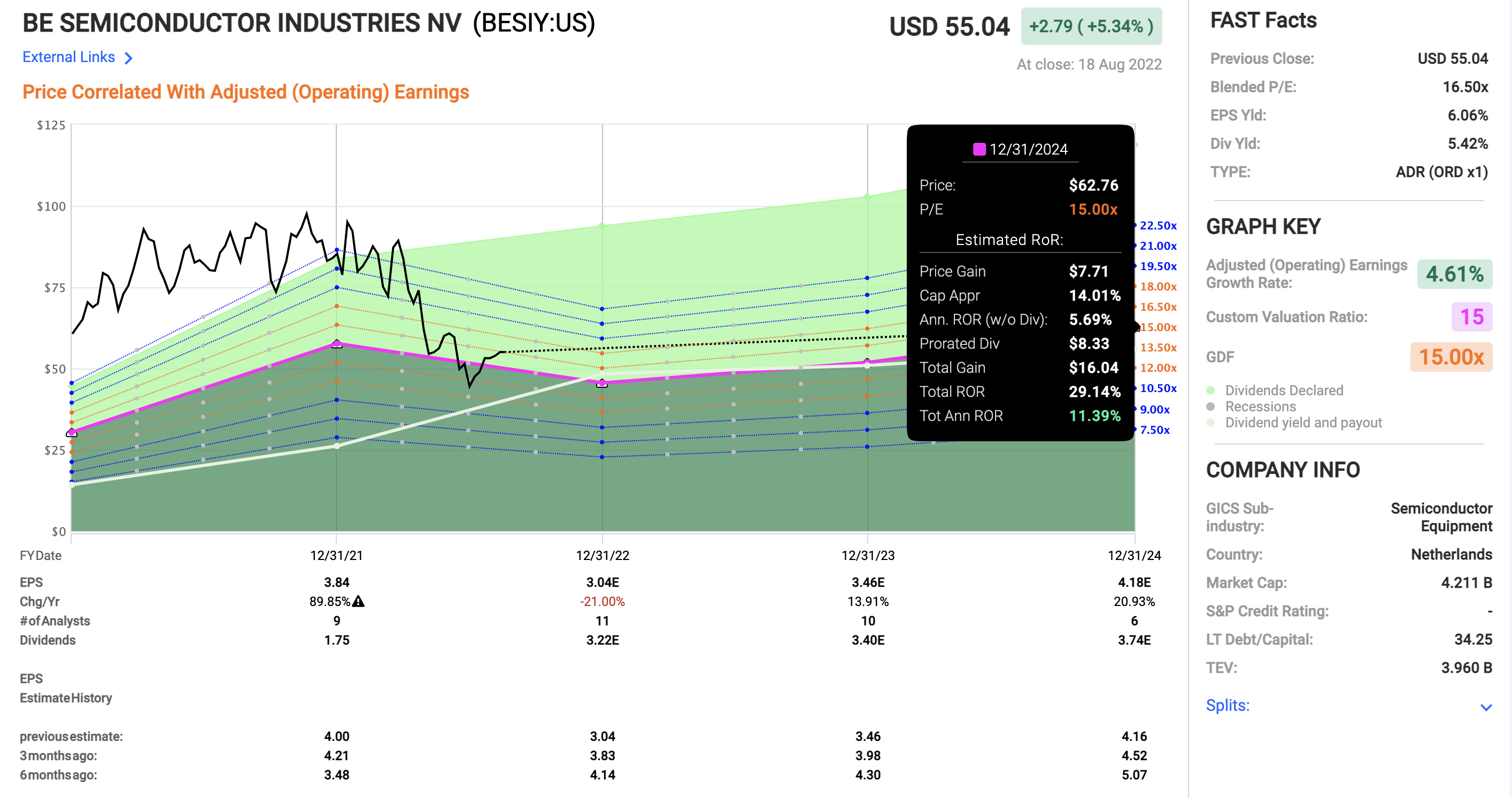

Look - even considered only at a 15x forward P/E, the company is now likely (as I see it) to generate returns of at least double digits per year or nearly 30% in 3 years.

{kind=link}

Even allowing for a very slight potential of a premium here, the potential outperformance for BESI goes all the way up to 30% per year in the case of 22x P/E forward multiple - and this is not at all outlandish given where the company has been trading for the past few years.

BESI now commands an average analyst PT of €72.5/share, down from almost €100/share back in march of this year. This illustrates how quick these analysts are in shifting their long-term targets. I personally stick to my conservative €65/share target for the native here.

For the 2024E P/E target of 18x, the company has a more than 98% total RoR (or 80% conservatively, considered down to 16-17x P/E), from an annualized RoR of 34%.

7 out of 9 analysts consider this company to be a solid "BUY" here - that's the same number of analysts with the stance as we had some months ago, so overall things haven't shifted all that much.

The only thing that's shifted to any meaningful degree is that the company can now clearly be considered "cheap".

That is rare enough for me to highlight it, and purchase stock here.

So, based on all of this and what I've said in the article, I view BESI as a "BUY" here with an upside of at least 14% annually and a price target of $65/share for the native.

Questions?

Let me know!

For further details see:

BE Semiconductor: Now Buyable With A Large Upside