BEEM - Beam Global: Why I Didn't Buy The EV Charging Story

2023-09-15 07:29:50 ET

Summary

- The collapse of sentiment in the EV sector has led to a significant drop in the valuation of Beam Global.

- BEEM's revenue has been surging, but its market cap has decreased due to the current macroeconomic conditions.

- The pending acquisition of Amiga is expected to boost Beam's revenue, but profitability is still a distant goal.

Whilst the Fed's hawkishness is needed to bring inflation back to its 2% target, it has had the unintended impact of shattering the EV dream as valuations and liquidity for tickers across the space collapse. Beam Global ( BEEM ) has dipped nearly 40% over the last 1 year as 2023 has seen a range of electric vehicle bankruptcies. Proterra and Lordstown Motors both filed Chapter 11 this year to shake investor confidence in a sector now seen as the future of transportation. This collapse of sentiment has come on the back of a Fed funds rate that currently sits at a 22-year high of 5.25% to 5.50% with expectations that there will be a further 25 basis points hike in 2023 building. Critically, this great dip in sentiment has expressed itself as a pullback in the valuation of Beam with the EV charging upstart now swapping hands at a 1.94x price-to-sales multiple.

What does this all mean? That every dollar of revenue earned by Beam is being translated to an ever smaller amount of market cap gains. To be clear, a dollar of revenue earned by Beam in early 2021 was valued at more than 75x but is now valued at less than 2x. Hence, even with the company's revenue surging over the last two years, its market cap is down markedly due to the current macroeconomic backdrop. A dovish Fed pivot and the eventual march of the Fed funds rate back to its pre-2021 average should help spark positive price returns for the San Diego-based EV charging company.

Revenue Surges

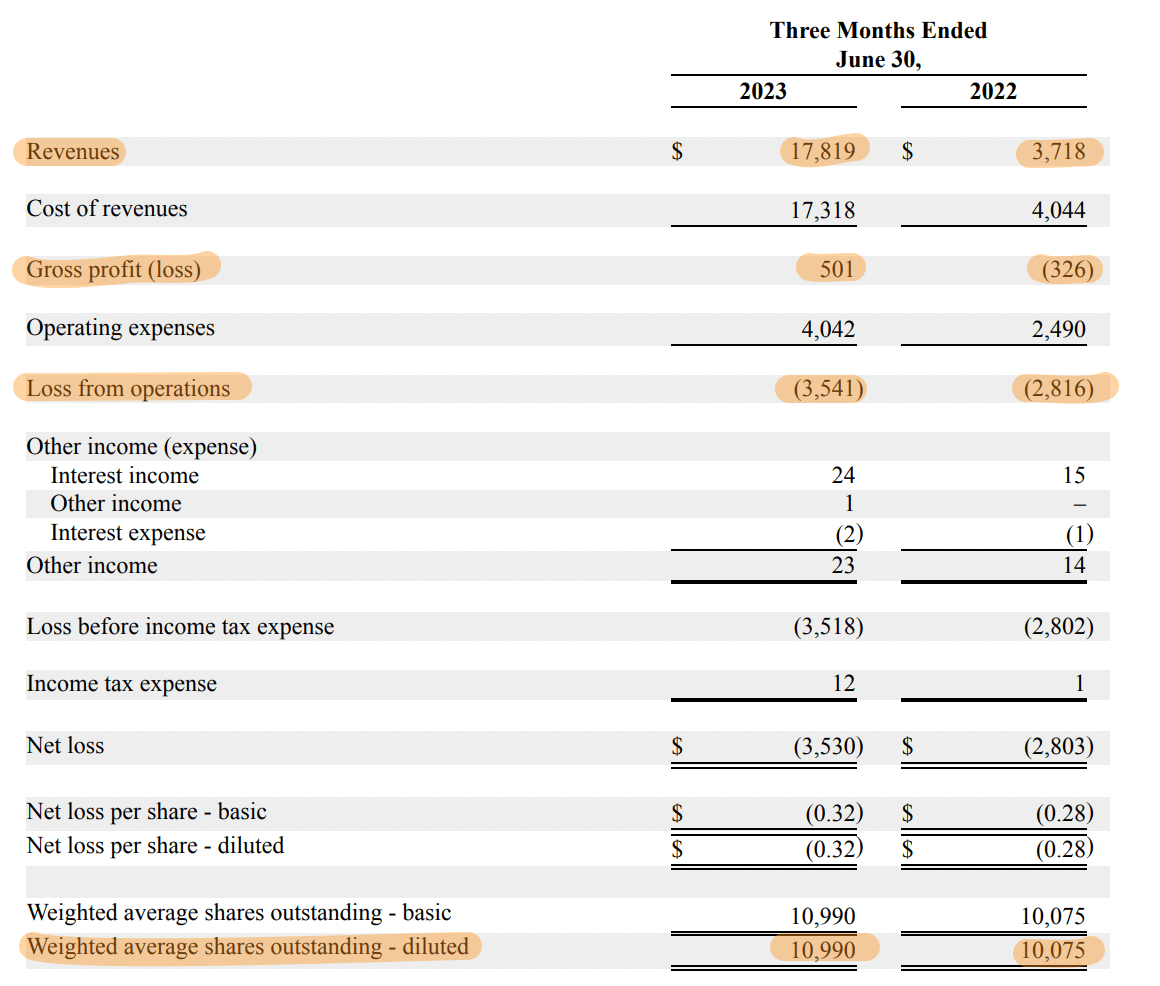

Beam's fiscal 2023 second-quarter revenue at $17.82 million was growth of 379% over its year-ago quarter and a beat by $3.8 million on consensus estimates. This growth was driven by a 589% increase in the deployment of the EV ARC charging system and a ramp-up of AllCell's battery production. Beam acquired the energy storage company back in February 2022 to diversify its revenue base, boost revenue growth, and enhance its broader position within the green economy. Further, Beam recently announced that it had signed a binding letter of intent to acquire Serbia-based Amiga, a specialized structures manufacturer that produces street lights, energy, and communications infrastructure.

Beam Global Fiscal 2023 Second Quarter Form 10-Q

{kind=link}

Whilst no acquisition price was provided, Amiga is forecasting revenue for its second quarter, ending on the 30th of June 2023, to be between $15.5 million to $17 million . The acquisition is set to see revenue for Beam ramp to new highs with fiscal 2024 second-quarter revenue likely to be north of $40 million. It has also placed Beam liquidity in view. Gross profit during the second quarter of $501,000 , around a 3% gross profit margin, was a huge improvement from a $326,000 loss in the year-ago period but came with a loss from operations of $3.54 million. This outpaced the $2.8 million loss realized in the year-ago period.

The Bittersweet Macro Backdrop

Beam's second-quarter cash flow from operations was negative at $4.4 million , an improvement from a loss of $5.5 million in the year-ago period with cash and equivalents as of the end of the period at $23.7 million. This end of period position was a jump from cash and equivalents of $1 million in the prior first quarter and came on the back of an oversubscribed June equity offering to raise $25 million. Critically, Beam held no debt on its balance sheet as of the end of the quarter and had an unused $100 million line of credit.

Bulls would be right to flag that Beam is primed for more growth with a balance sheet that can somewhat comfortably support further bolt-on acquisitions, fund the continued deployment of its EV ARC systems, and realize a $34 million sales backlog. This relatively strong liquidity position for Beam is critical against what's been two EV company bankruptcies in 2023. This backdrop has necessitated investors to pay particular attention to balance sheet strength and cash burn in order to avoid the fate of Proterra and Lordstown investors.

Cox Automotive

EVs are the future with 2022 a blockbuster year for their growth in the US with 809,000 cars sold, around 5.7% of total cars sold. 2023 will likely see at least 1 million units sold to further consolidate EV sales growth above the 5% EV tipping point. This essentially describes the percentage threshold of mass adoption. However, this positive EV charging story will not resonate with shareholders in the current macro backdrop until profitability is reached. This is a point that's likely many years in the future for Beam. The company's shareholders might struggle to realize strong price returns as the ticker is still dependent on dilution for its liquidity and as it continues to realize a significant level of cash burn from its operations.

For further details see:

Beam Global: Why I Didn't Buy The EV Charging Story