BEAM - Beam Therapeutics: Rich In Cash Poor In Punctuality (Rating Downgrade)

2023-10-03 09:49:31 ET

Summary

- Beam Therapeutics' Q2 2023 shows moderate revenue growth but rising operational costs, mainly in R&D, affecting net loss and diluting shares.

- Despite robust liquidity and a 33-month cash runway, operational inefficiencies in the BEACON sickle cell trial raise concerns over long-term viability.

- Investment Recommendation: Downgrade Beam Therapeutics from "Hold" to "Sell" due to operational inefficiencies and high R&D costs amidst a risky clinical landscape.

At a Glance

Beam Therapeutics' ( BEAM ) Q2 2023 financials reaffirm trends noted in my previous analysis but also reveal new concerns. While the company maintains robust short-term liquidity, operational expenses continue to rise, primarily driven by R&D activities. Since my last review, their clinical pursuits remain a double-edged sword: diverse assets across therapeutic areas mitigate some risk, yet operational inefficiencies, such as the protracted recruitment timeline in the BEACON trial for sickle cell disease, warrant attention. These inefficiencies could exacerbate capital allocation issues, particularly concerning given the company's already scrutinized burn rate. The financial and clinical landscape still advises caution; hence, key markers to watch are forthcoming early trial data and strategic capital moves as they will reflect Beam's risk tolerance and long-term viability.

Q2 Earnings

To begin my analysis, looking at Beam Therapeutics' most recent earnings report for Q2 2023, there's a discernible pressure on their financials. The company reported $20.1M in license and collaboration revenue, up from $16.7M YoY, showing moderate growth. However, operating expenses surged to $122.3M from $98.6M, with R&D alone costing $97.6M. The net loss widened to $82.8M from $71.9M, increasing the net loss per share to $1.08 from $1.02. Moreover, a 9% increase in weighted-average common shares outstanding to 76.3M indicates share dilution, diluting existing shareholder value.

Financial Health

Turning to Beam Therapeutics' balance sheet , the company shows robust liquidity with cash and cash equivalents at $225.5M and marketable securities at $847.5M, making the total liquid assets $1.07B. The current ratio, calculated by dividing the total current assets ($1.095B) by the total current liabilities ($209.5M), stands at approximately 5.2. Based on the "Net cash used in operating activities," the company has a monthly cash burn rate of $32.4M, calculated over the last six months with a net cash outflow of $194.5M. The cash runway, therefore, is about 33 months, given the monthly cash burn. Please note that these figures are based on past data and may not directly reflect future performance.

The likelihood of Beam needing additional financing in the next twelve months appears to be low. With a cash runway extending nearly three years and a strong current ratio, they have a comfortable financial cushion to continue operations without an urgent capital infusion. However, strategic moves like acquisitions or accelerated R&D could necessitate quicker capital needs. These are my personal observations, and other analysts might interpret the data differently.

Equity Analysis

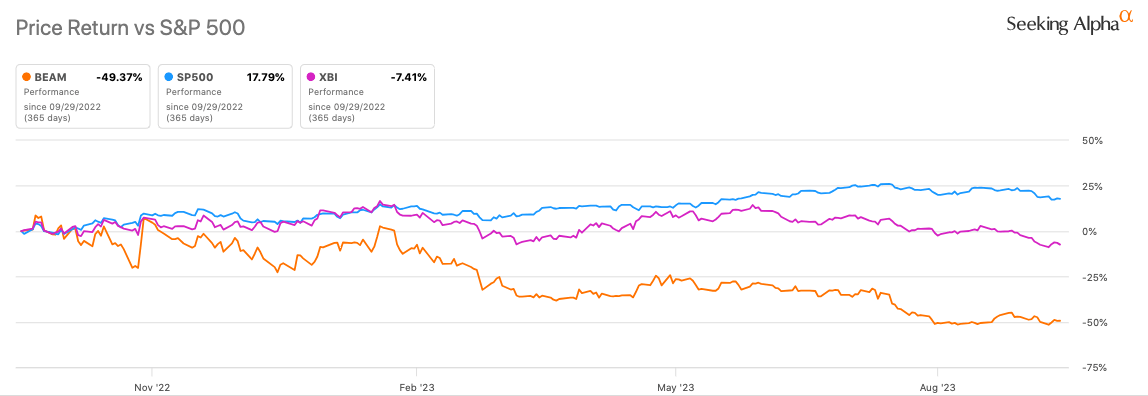

According to Seeking Alpha data, Beam Therapeutics' market cap of $1.85B against a widening net loss suggests moderate market confidence, cushioned by a strong cash runway. Analysts project a YoY sales growth of +27.24% for 2023 but a decline for 2024, raising questions on long-term growth. BEAM's stock performance lags SPY considerably across all timeframes, signaling weak momentum. 24-month Beta of 1.64 indicates higher volatility compared to the market.

{kind=link}

Options show increased puts, hinting at bearish sentiment and elevated volatility. Short interest at 21.85% is noteworthy, signifying the potential for a squeeze but also a considerable bearish outlook. 73.44% of shares are institutionally held; increased positions (99 holders) outnumber decreased ones (77), implying cautious optimism. Insider activity shows a net selling trend over 12 months, subtly flagging caution. Overall, a mixed bag with leans toward caution in the near term and questions around long-term sustainability.

Slow and Steady? Beam's Twist on the Tortoise and the Hare

Beam Therapeutics' multi-pronged clinical pipeline - spanning hematology, immunology/oncology, and genetic diseases - is progressing, albeit with some potential speed bumps. In the hematology sector, the BEACON trial targeting sickle cell disease has managed to fill its sentinel and expansion cohorts. However, the extended recruitment timeline - a year thus far and counting - warrants scrutiny. While having sufficient patients for both cohorts may be framed as a logistical achievement, the slow pace could suggest operational inefficiencies or patient recruitment challenges, a critical aspect for future studies and for investor confidence.

The slow recruitment might be seen as a red flag for some investors, particularly because Phase 1/2 trials are generally not this protracted. This elongated timeline could have broader implications, such as resource allocation and potentially higher capital requirements.

Turning to immunology and oncology, BEAM-201 is on track, with multiple sites now open for enrollment and the first patient expected to be dosed this quarter. Although the therapy is progressing to clinical trials, the CAR-T landscape is fraught with safety and scalability concerns. The multi-site strategy perhaps indicates a prudent risk-mitigation tactic.

In the realm of genetic diseases, Beam is showing agility by leveraging insights from BEAM-301 to expedite the development of BEAM-302. This could signify a learning-driven ethos and a certain level of confidence in their in vivo base-editing technologies.

This ability to pivot based on internal learnings is an attribute that could serve Beam well in the dynamic biotech arena. However, the company will need to balance speed with caution, especially considering the novel technologies it's developing.

To summarize, Beam has made considerable, albeit uneven, advances across its clinical pipeline. The firm offers a diversified risk profile, with multiple assets at various development stages. The looming milestones - especially early safety and efficacy data - could either validate or challenge the company's standing in the fiercely competitive gene-editing sector.

My Analysis & Recommendation

In light of Beam Therapeutics' Q2 2023 performance, coupled with a clinical pipeline fraught with both promise and uncertainty, there is significant fodder for investor contemplation. Financially, Beam appears solvent in the short term, with a cash runway of approximately 33 months at the current burn rate. While this provides a certain comfort, let's not lose sight of the surging operating expenses - particularly in R&D - that contributed to an increased net loss of $82.8M.

From a clinical perspective, the extended recruitment timeline for the BEACON trial in sickle cell disease raises concerns about operational efficiency and casts shadows on timelines for commercialization. In a sector where speed to market is often as critical as efficacy, this languid pace could be an Achilles' heel, especially with a burn rate that's already stoking investor concern. Beam's immunology/oncology endeavors via BEAM-201 seem cautiously optimistic, albeit set against a backdrop of an increasingly complex CAR-T safety landscape.

In the coming weeks and months, investors should keenly watch for:

-

Early safety and efficacy data from ongoing trials, which could serve as critical inflection points for stock valuation.

-

Any strategic capital moves, such as acquisitions or partnerships, which may significantly alter the existing cash runway and indicate a heightened risk tolerance.

-

Short interest fluctuations, as the currently high 21.85% could catalyze significant price volatility, either via short squeezes or heightened downward pressure.

-

Insider trading patterns. Current net selling trends subtly flag caution; further sales could corroborate the sense of an internal lack of confidence.

-

Look out for institutional investor moves. They currently hold 73.44% of the shares, and any significant changes could move the needle considerably.

Based on the integration of these factors, slow progress in key clinical trials, and the burgeoning cost structures, I am downgrading my recommendation from "Hold" to "Sell" for Beam Therapeutics. The company's multiple trials in diverse therapeutic areas, although promising, do not offset the financial and operational headwinds it currently faces. Risk-tolerant investors might find some aspects appealing, but a prudent approach suggests capital might be better allocated elsewhere in the gene-editing or broader biotech sector.

Risks to Thesis

While my recommendation is a "Sell" for Beam Therapeutics, several counterpoints could defy this stance. First, the 33-month cash runway and robust liquidity may provide a sufficient buffer for Beam to weather temporary setbacks and possibly even accelerate R&D, potentially adding shareholder value. Second, though the clinical trial timelines appear prolonged, the industry knows well that breakthroughs often suffer initial delays. The first-to-market advantage isn't always decisive; often, it's the best-in-class that wins. Third, with a high short interest, any positive news could trigger a short squeeze, rapidly inflating the stock price. Lastly, the multi-pronged approach across different therapeutic areas can act as a natural hedge within Beam's own portfolio, diluting risk. Therefore, underestimating the potential upsides of their diverse clinical portfolio could be an oversight.

For further details see:

Beam Therapeutics: Rich In Cash, Poor In Punctuality (Rating Downgrade)