BZH - Beazer Homes: Better Resilience Than I Expected (Rating Upgrade)

2023-10-03 05:12:18 ET

Summary

- Beazer Homes reported strong Q3 results, exceeding expectations and showing resilience in a slower economy.

- The upcoming Q4 results are expected to be challenging, with a significant decrease in revenue and EPS compared to the previous year.

- BZH stock seems to currently be undervalued, with a low forward P/E ratio and a moderately good DCF model upside with my estimates.

Beazer Homes ( BZH ) reported a relatively strong Q3/FY2023 result after my previous analysis of the company. After the quarter, I re-evaluated my position on the stock - as the company seems extremely cheap with current trailing earnings ratios, I upgrade my rating into a buy rating from the previous sell rating as the stock price has fallen and the earnings prospects have grown in my opinion. I also take a different approach in evaluating Beazer's debt after a reconsideration.

Reported Q3 Results

Beazer reported Q3/FY2023 results that were above analysts' and my expectations - revenues came in 8.7% above the previous year's period, in contrast to analysts' and my expectations of a revenue fall. In addition, the company's profitability was surprisingly good as a result of higher-than-expected sales - Beazer achieved an EBIT figure only 28% below the previous year's extremely high figure .

The shown resilience seems very promising in my opinion - the achieved earnings level has partly stayed even with a significantly slower economy. Although Beazer's backlog is significantly below the previous year's figure after Q3, the shown result was way better than I would have expected.

Upcoming Q4 Results

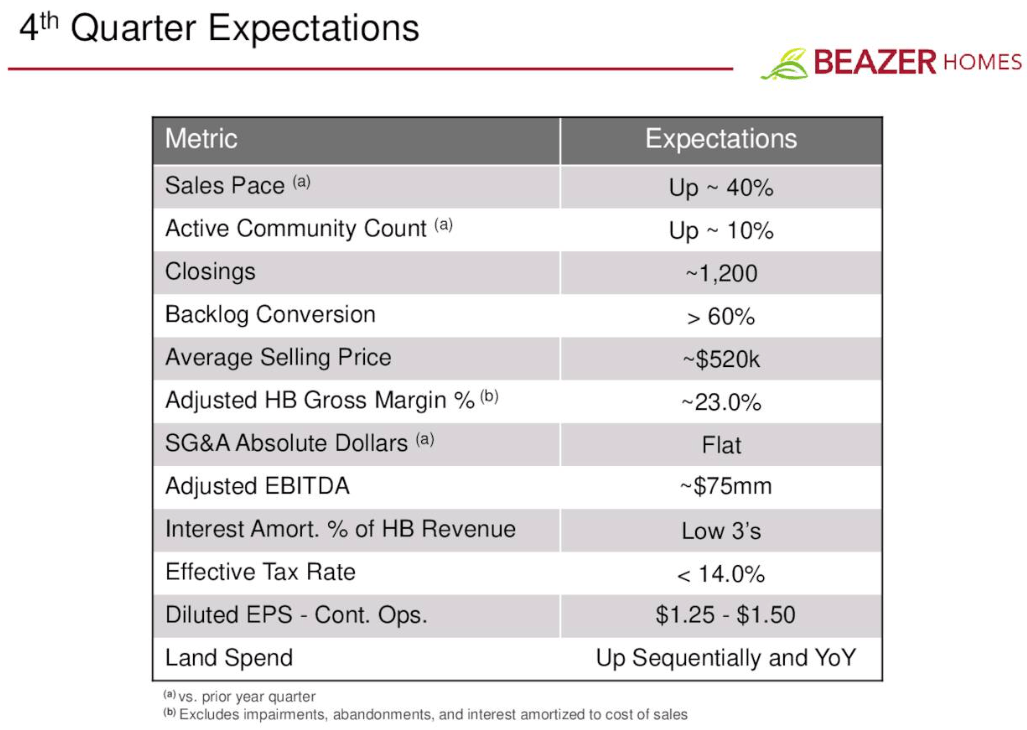

Beazer should report its Q4/FY2023 around the 10th of November, as estimated by Seeking Alpha. The company is facing very tough comparison numbers in the quarter - in Q4 of FY2022, the company's revenues grew by 40% to a figure of $828 million. Analysts currently expect a revenue decrease of 24% with an estimate of $627 million for the quarter - compared to previous quarter's shown growth, the estimate shows estimated weakness. The EPS estimate of $1.39 is around half of the previous year's figure.

The estimated figures are quite in line with the management's guidance:

4th Quarter Guidance (Beazer Homes Q3 Investor Presentation)

{kind=link}

The management's estimates were presented in the company's Q3 presentation on July 27th - the actual figures still have had time to vary from the management's expectations.

Valuation

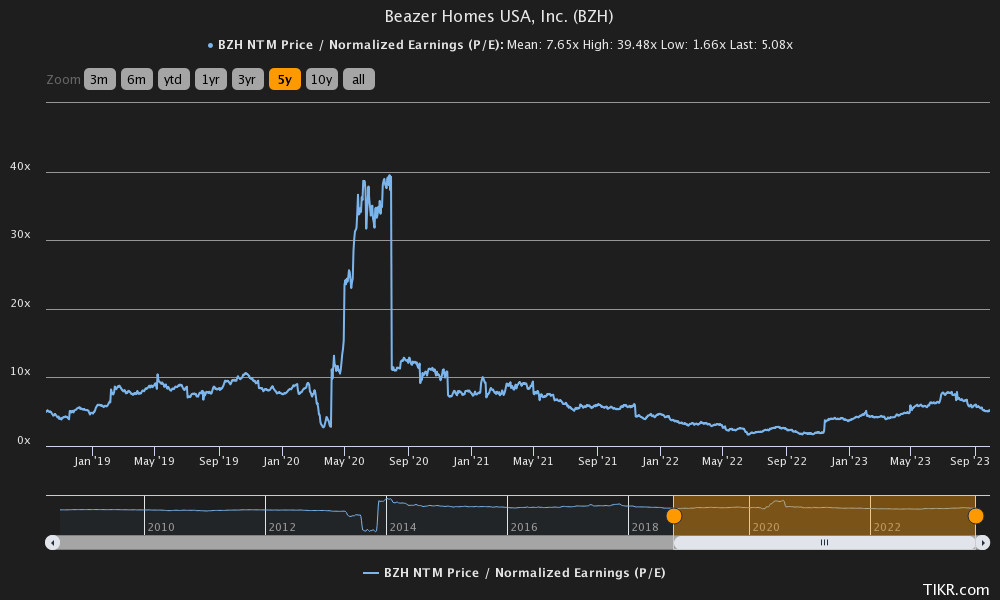

Currently Beazer trades at a forward price-to-earnings ratio of 5.1, below the already low five-year average of 7.7:

{kind=link}

The forward ratio seems to price in a large decrease in earnings after the period. To further analyse the valuation, I constructed a discounted cash flow model as usual to try to determine an estimated fair value for the stock.

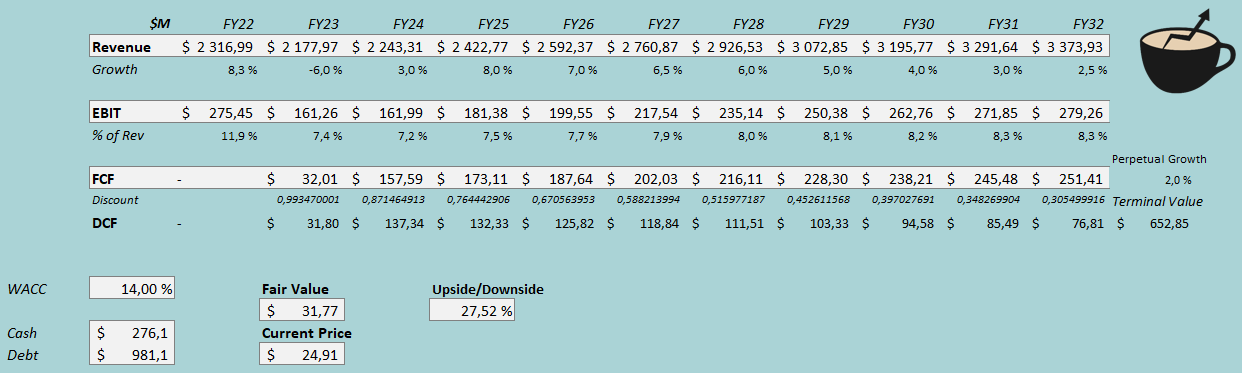

Compared to my previous estimates, I am slightly more optimistic about the current year's revenues - I estimate a decrease of 6% in the year. As I am expecting a better fiscal year 2023 than before, I have a more conservative revenue jump in fiscal year 2024 - I estimate a growth of 3% as FY2023 revenues aren't as slow in demand. Also, as the economy is still at a very volatile place with interest rates reaching new highs, I estimate a slow demand to continue into FY2024. Going further from FY2024, I estimate a growth of 8% for FY2025 which slows down into a perpetual growth rate of 2%. Compared to my previous estimates, I estimate revenues of $3410 million for FY2032 - in the previous model I had a revenue estimate of $3141 million for the year, representing a 9% rise in the estimate for the year.

I also revisited my EBIT margin estimates. Currently I estimate the company's margin to be 7.4% in FY2023, slightly above my previous estimate. Compared to my previous analysis, though, I estimate the margin to hold better and even achieve some growth after the currently slow demand has been eliminated - I estimate the EBIT margin to scale into 8.3%, compared to my previous model's estimate of 7.1%.

I also have a better cash flow conversion in my current model as opposed to my previous analysis - the company seems to amortize its interest expenses, and as I construct my DCF model with unlevered free cash flow, interest expenses shouldn't count into free cash flow - I add the estimated interest amount back into the free cash flow figure after the EBIT estimate. The mentioned estimates along with a cost of capital of 14.00% craft the following DCF model scenario with an estimated fair value of $31.77, around 28% above the current price:

DCF Model (Author's Calculation)

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

As opposed to my previous analysis, I count for the company's debt in a different way as mentioned in the FCF estimates - Beazer amortizes the company's interest expenses into the costs of goods sold; interest is already counted for in the company's EBIT row as the company doesn't have any interest expenses in its income statement. I count for financing expenses in the CAPM as the DCF model is modelled with unlevered cash flows.

In the company's Q3 earnings call , the management estimated that the company's amortized interest expenses should be in the low 3's as percentages of homebuilding revenues. With my DCF model estimate for 2023, the company's revenues are $2178 million - 3% of the revenues would translate into an interest rate of 6.66%, which I use in the CAPM. As in my previous model, I estimate the long-term debt-to-equity ratio to be 35%.

The United States' 10-year bond yield, which I use as the risk-free rate, has risen significantly after my previous analysis to a yield of 4.58% . The Aswath Damodaran's estimated equity risk premium of 5.91% still stands. Yahoo Finance estimates Beazer's beta to be 2.33 , slightly above the figure of 2.17 in my previous analysis. Finally, I add a liquidity premium of 0.5% crafting the cost of equity at 18.85% and the WACC at 14.02%.

Risks

The investment doesn't come without risks, though. As home building has historically very cyclical in nature, Beazer is highly exposed to economic turbulence - the beta of 2.33 represents the leveraged risk level of the stock. The coming quarters are likely to be quite turbulent, and I would expect large fluctuations in the stock price in either direction.

In addition, Beazer's high debt balance raises the risk level. Although Beazer is trying to pay off the debts as the company generates cash flows, repaying most of the debt should still take a relatively long time. As the debt still stands, it further leverages shareholders' exposure to macroeconomic risks.

Takeaway

Compared to my previous analysis, the company has a widely higher fair value estimate. As I reconsidered my stance on Beazer's debt consideration and raised estimates after a higher-than-expected Q3 result, the stock seems to be worth way more than I expected in my initial analysis. As the stock price has also fallen after my first analysis, the current price represents a good opportunity to buy in my opinion; I have a buy rating for the stock.

For further details see:

Beazer Homes: Better Resilience Than I Expected (Rating Upgrade)