BZH - Beazer Homes USA: Cost Reduction Initiatives Beneficial Expectations And Undervalued

2023-10-18 23:43:43 ET

Summary

- Beazer Homes USA reported impressive expectations for Q4 2023, including sales pace growth, backlog conversion, and beneficial figures for 2023.

- The company operates in 13 states and offers a range of homes for different price options and categories.

- Market analysts expect double-digit net sales growth, operating margin growth, and positive free cash flow in the coming years, indicating potential for the stock price to increase.

Beazer Homes USA, Inc. ( BZH ) recently delivered impressive expectations for Q4 2023 with regards to sales pace growth, backlog conversion, and beneficial figures for 2023. Also, with an impressive number of energy efficient tax credits that may last for more than 7 years and recently announced cost reduction initiatives, Beazer Homes USA does appear a bit undervalued. I do see risks from the total amount of debt, potential changes in the interest rates, or changes in the price of land. However, I believe that there is a potential in the stock price.

Beazer Homes USA

With activities in 13 states distributed in the East, West, and Southeast of the United States, Beazer Homes is a company dedicated to the construction of homes with various price options and categories for future homeowners.

The activities are divided into three segments that correspond to each of the geographical areas indicated above: East, West, and Southeast. The company's activity is similar in the three segments, and is aimed at the construction of single family homes and multifamily homes, after acquiring land and developing it to adapt it to the realization of the project.

Diversification in 17 states - of which Arizona, Nevada, California, and Texas stand out, because the largest amount of annual revenue comes from these states - serves to avoid exposure to the risk of a particular regional market. Within this framework and recently in 2016, Beazer Homes introduced the Gatherings program, which offers the construction of homes for age segments of the population, with properties with low maintenance costs and aimed mainly at those over 55 years of age. Within its portfolio, the company, in addition to offering the construction of homes with customized designs, includes more than 200 home models, which cover decoration, furniture, and landscaping around the home, and are one of the main sales channels.

I believe that it is a great time for reviewing Beazer Homes USA mainly because of the recent quarterly results reported in Q3 and the expectations for Q4. The company reported 29% increase y/y in new home orders as well as 28.3% y/y sales pace growth. As a result, adjusted homebuilding revenue growth was close to 9%. In my view, if the company continues to deliver such impressive figures in the coming quarters, the stock price will most likely trend higher.

Source: Presentation To Investors

The expectations delivered for Q4 are quite beneficial. Sales pace is expected to be close to 40%, with backlog conversion of about 60%, and an adjusted EBITDA of about $75 million.

Source: Presentation To Investors

The numbers for 2023 were also given in the last presentation. 2023 Adjusted EBITDA is expected to be close to $250 million, with a book value per share close to $35 per share. Taking into account the current stock price and the expected book value per share, I believe that Beazer Homes USA appears cheap.

Source: Presentation To Investors

Beneficial Expectations

I believe that market expectations for Beazer Homes USA are quite beneficial. Some numbers are worth mentioning. Let's keep in mind that I did take a look at the figures of other analysts before designing my own expectations.

Market analysts expect double digit net sales growth in 2024 and 2025 as well as operating margin growth in 2023, 2024, and 2025. Additionally, the net margin is expected to be around 6% and 7% from 2023 to 2025, and the company would report positive free cash flow in 2025.

More in particular, analysts expect 2025 net sales to be close to $2691 million, with net sales growth of 11%, EBITDA close to $324 million, and net income close to $205 million. Finally, the EPS is expected to be around $6, with free cash flow close to $69 million, and FCF/net sales of close to 2.57%.

Source: Market Screener

Balance Sheet

As of June 30, 2023, the company reported cash and cash equivalents close to $276 million, with restricted cash of about $39 million, accounts receivable of $33 million, and owned inventory close to $1741 million. Considering the total amount of cash in hand and the list of current liabilities, I believe that liquidity does not seem an issue here.

Finally, with property and equipment of about $28 million, operating lease right-of-use assets close to $16 million, and goodwill of $11 million, total assets were equal to $2.318 billion. The asset/liability ratio is larger than 1x, so I would say that the balance sheet appears pretty clean.

Source: 10-Q

The list of liabilities include trade accounts payable of $136 million, operating lease liabilities close to $17 million, total debt of close to $981 million, and total liabilities worth $1.273 billion.

Source: 10-Q

I do believe that the total amount of debt appears a bit elevated. With that, it is quite beneficial that the leverage decreased significantly in the last three years, and management promised to decrease it even more.

Source: Presentation To Investors

I studied the maturity of the debt. Considering the current free cash flow generated and debt payments required, I think that Beazer Homes will most likely be able to negotiate or pay its debt obligations.

Source: Presentation To Investors

Tax Benefits May Bring Net Income Increases In The Coming Years

Beazer Homes recently reported significant energy efficiency credits coming from building industry-leading energy efficient homes. The company talked about tax benefits in 2024 and 2025 besides mentioning the tax benefits from 2026 to 2033. I believe that these tax benefits will most likely enhance future income statements and cash flow statements. It is a relevant factor that analysts out there will most likely take into account.

Source: Presentation To Investors

FCF Catalyst: Cost Reduction Initiatives Will Most Likely Bring FCF Growth

In the last quarterly presentation, Beazer Homes USA reported significant cycle time improvements and construction cost reduction initiatives. As shown in the images below, production cut-off is expected to lower significantly, and direct costs also decreased from Q1 2023 to Q3 2023. In my opinion, further cost reduction initiatives would most likely lead to FCF margin increases and FCF growth.

Source: Presentation To Investors

Further Acquisition Of Land Will Most Likely Accelerate Net Sales Expectations

Beazer Homes' strategy is long-term, and seeks to maintain balanced revenue growth, with low margins and high returns on capital. The acquisition of land plays a fundamental role in this sense, as they are a key factor in the total cost account and the reduction of costs, which generate the increase in profits despite maintaining similar income numbers at an annual level. I assumed that the know-how accumulated for acquiring land will most likely enhance future net sales growth and building capacity.

Despite the current global economic uncertainty, I believe that the long-term construction market will continue to grow in activity, and the low-cost strategy and renegotiation of construction contracts will be important development points to achieve access to liquidity that allows reinvestment in the purchase of future lands for development.

Assuming Previous Financial Figures From Beazer And Considering Previous Assumptions, My Financial Model Indicates That Beazer Homes Appears Undervalued.

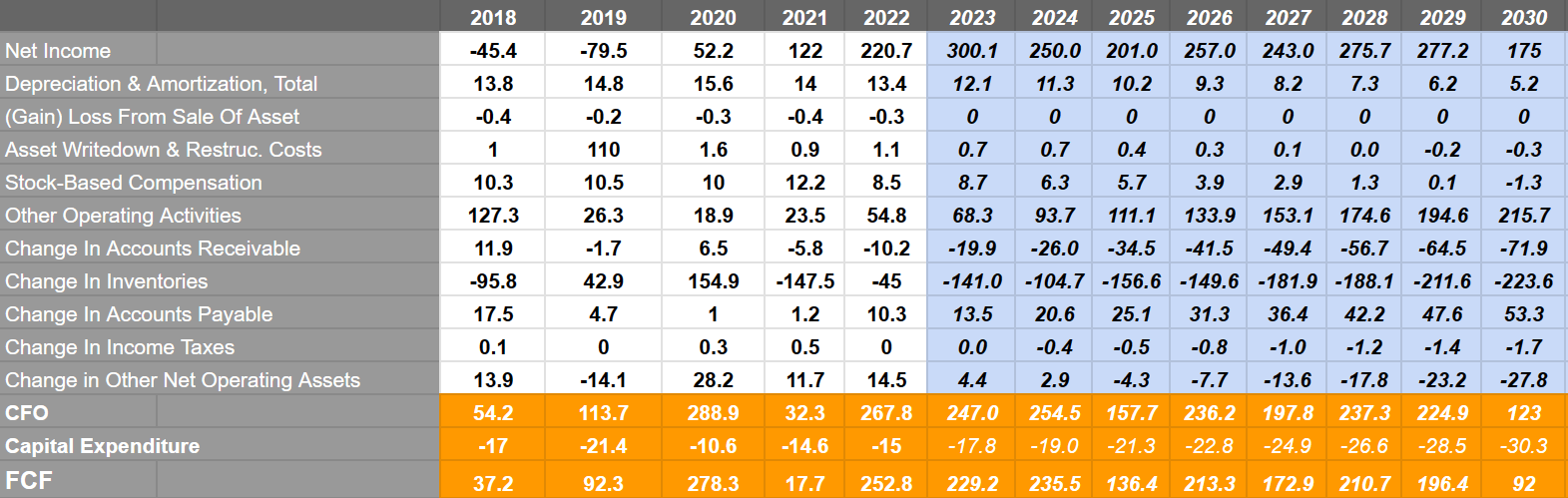

My DCF model included 2030 net income close to $175 million, depreciation and amortization of close to $5 million, and stock-based compensation of about -$2 million. Besides, with changes in accounts receivable of close to -$72 million, change in inventories close to -$224 million, and change in accounts payable worth $53 million, I obtained 2030 CFO of about $122 million. Finally, with 2030 capital expenditure of close to -$31 million, 2030 FCF would be about $92 million.

{kind=link}

Considering previous free cash flow which stood between -$300 million and $324 million, I believe that my FCF results of about $229-$92 million are likely.

Source: Ycharts

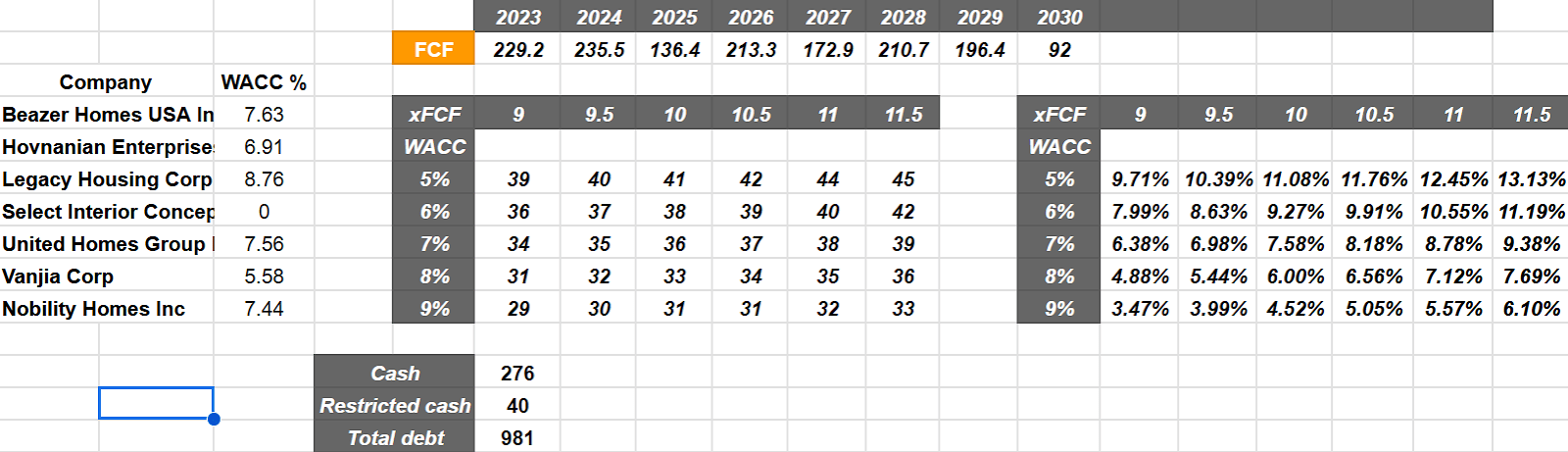

I also checked some of the peers , which reported a WACC of close to 5% and 9%. Additionally, the company’s senior notes include interest rates close to 5.8% and 7.2%. With these figures, I believe that assuming a WACC between 5% and 9% makes sense.

Source: 10-Q

I also included an EV/FCF of close to 9x and 11.5x, which I think is a proper valuation given the previous trading multiples.

Source: Ycharts

With the previous assumptions, I obtained a target price between $29 per share and $45 per share with a median of $36-$37. Additionally, I obtained an IRR close to 3% and 13% and a median IRR close to 7%-9%. With these results, I believe that the company appears significantly undervalued.

{kind=link}

Competitors

Competition in the construction market is not only high, but also highly fragmented, in the hands of large companies with national scope and an expanded geographic footprint, independent contractors from regional markets, and other companies with a position similar to Blazer Homes, with a geographical scope limited to a number of determining states. The competition that represents a risk in this sense comes mostly from companies with national reach, which have greater financial capabilities and lower costs than this company.

Risks

Firstly, based on the federal government's economic adjustments to current inflation, the increase in interest rates represents a risk factor since the majority of Beazer Homes clients access loans or mortgages for the purchase of homes, and these increases may affect the ability to pay the loans or mortgages and the subsequent completion of projects. Likewise, current inflation and market conditions generate risks for the company, mainly in relation to the price of the land that it already owns and the ability to interpret market conditions in the acquisition of future land.

Along with this, it is important to note that the share prices of this company have demonstrated high levels of volatility in recent months, and there is no certainty of stabilization in the short term. As a result, many analysts out there may use large WACCs, which may make Beazer Homes look a bit expensive. If many people think that the company is expensive, we may see a decline in the stock price.

Additionally, operating margins also depend on a number of factors related to home sales and land development cycles, and the significant quarter-over-quarter decline may also add volatility and uncertainty to the stock price of Beazer Homes USA.

Conclusion

Beazer Homes USA delivered an impressive quarterly report, and expects double digit sales pace with backlog conversion of about 60% in Q4. With these figures, I would expect a lot of new investors having a look at the business model soon. In the long-term, I believe that the energy efficient tax credits from now to about 2030, further successful acquisition of land, and recent cost reduction initiatives announced will most likely push FCF up. Yes, there are also some risks out there from the total amount of debt, changes in the interest rates, and price volatility, however I think that Beazer Homes USA appears undervalued.

For further details see:

Beazer Homes USA: Cost Reduction Initiatives, Beneficial Expectations, And Undervalued