BZH - Beazer's Investors Should Be Cautious

2023-07-25 07:55:11 ET

Summary

- Beazer Homes USA, a US-based homebuilder, faces potential risks due to its leveraged balance sheet.

- As the Fed raises interest rates, a possible cooldown in the real estate market could harm Beazer's ability to generate free cash flow.

- Despite a good rate of growth in revenues, Beazer's operating margin should fall further, posing a large risk for investors.

- The company has its Q3 earnings date around the corner, which could surprise the market in a negative way.

- Beazer's current valuation does not account for an expected earnings drop, and a discounted cash flow model suggests BZH stock is overvalued, reinforcing my sell-rating.

Beazer Homes USA ( BZH ) is a homebuilder based in the United States. While the company is valued very modestly compared to its current earnings, the company’s leveraged balance sheet and a likely earnings drop pose risks to investors. The company’s margins could fall further, posing a sizable risk for investors. At the current price of $27.76, I have a sell-rating for the stock.

The Company

Founded in 1985, Beazer is a company that builds detached houses across the United States. The company builds typical suburban homes, such as the following ones:

{kind=link}

Beazer tries to hit an affordable range in its homes. The company has a strategy to widen its geographical footprint, as it targets to grow the number of communities it builds homes into.

Financials

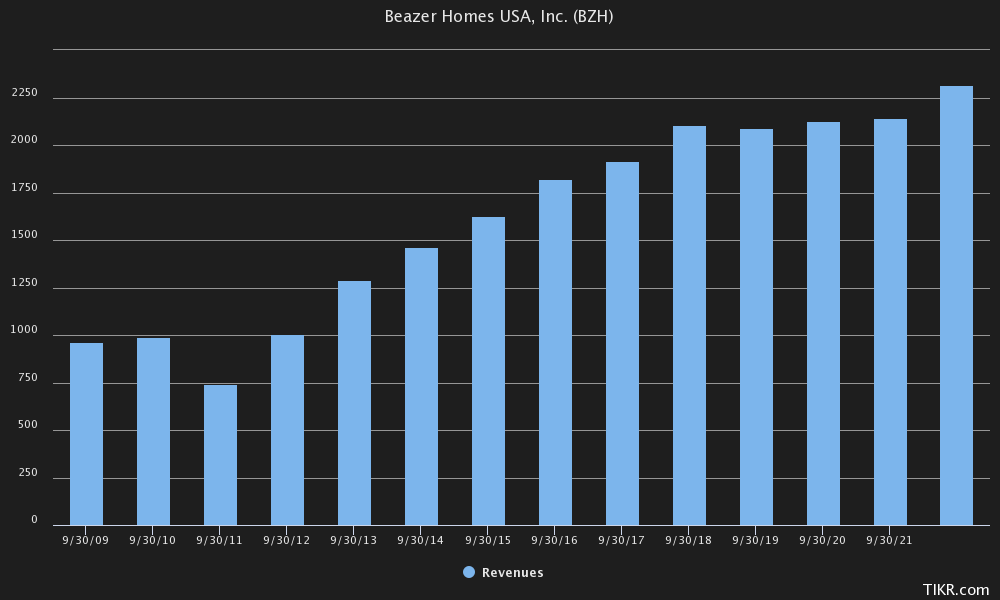

Beazer has been able to keep up a good rate of growth in its revenues, as the company’s compounded annual growth rate has been 8.7% for the last 10 years:

Beazer's Revenue Growth (Tikr)

{kind=link}

The revenue growth isn’t very profitable, as historically the company’s return on its capital has been around or below four percent. The current fiscal year is expected to be harder for Beazer too, as the company guides a revenue of >$2 billion – FY22’s revenues were $2317 million , so hitting the guidance could mean an almost 14% drop in revenues. Beazer should continue to grow in the coming years, as in the company’s Q2 earnings call the company’s CEO Allan Merrill told investors: “We're in great shape for '24 and well into '25. So the activity that we're engaged in right now is to sustain that growth rate into '26 and beyond.”

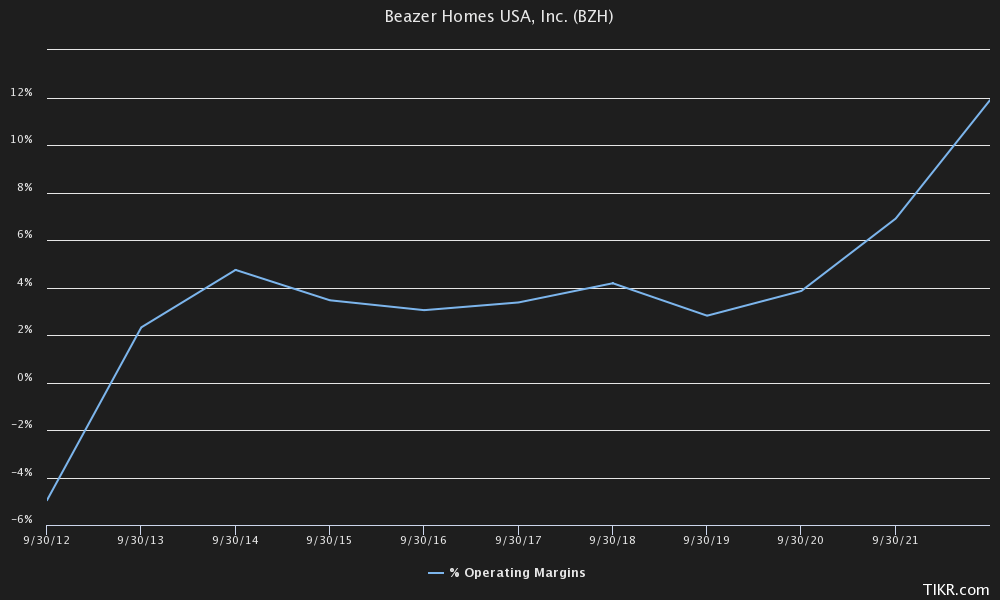

Beazer’s revenues aren’t the only financial metric that’s expected to drop in FY23 – the company guides an earnings per share of around $4 , when it was $7.22 in FY22. This should be expected, though, as Beazer’s margins have been at unsustainable levels for the past couple of years – the company’s operating margin has reached a high of 11.9% in FY22, compared to average margins of about four percent before Covid-related light monetary policy leading to a heated real estate market:

Beazer's Historical EBIT Margin (Tikr)

{kind=link}

Analysts expect the company’s operating margin to stay at around 6.8% for FY23, which would correspond to the guidance of $4 EPS. This figure still would have downside to the company’s historical margins; a risk that investors take when investing in the stock.

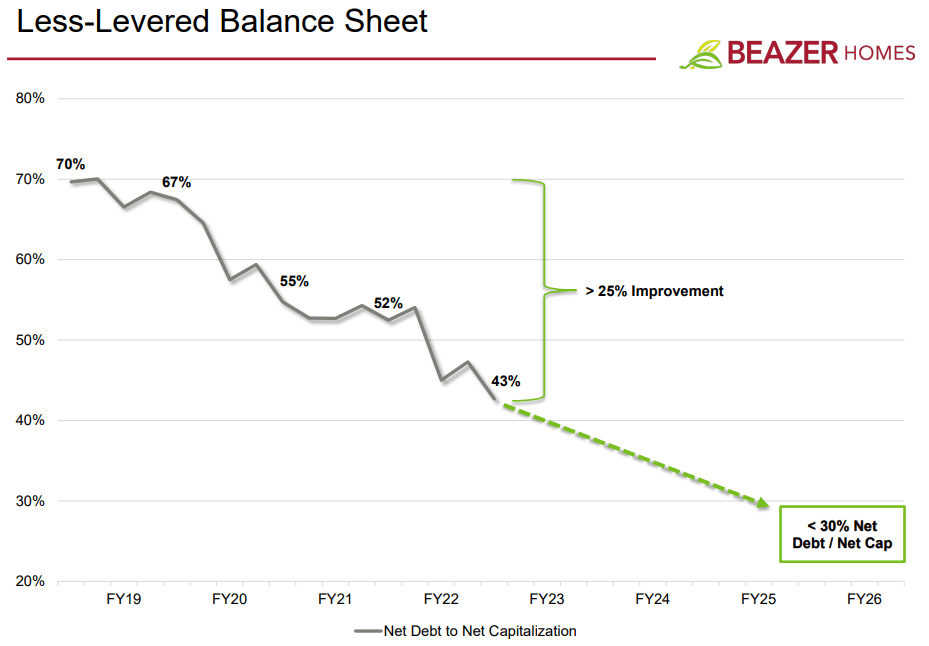

Beazer’s risks don’t end with margins, as the company holds a staggering $985 million in long-term debt . The company is in the process of deleveraging their financing, but as their debt amounts to multiple years of free cash flow, this should take time. The leveraged balance sheet is addressed in the company’s Q2/FY23 presentation:

Beazer Q2 Earnings Presentation

{kind=link}

The company does hold $241 million in cash, too – I don’t believe the company should necessarily run into liquidity problems any time soon even with all of its debt.

Upcoming Earnings

Beazer will report its Q3/FY23 earnings on July 27th in the after-market hours. Analysts expect the company's earnings to drop by 2.7% and EBIT to drop by 54% compared to previous year's earnings for the same period. The following quarter's expectations have a revenue drop of over 30%, which would put the company's FY23 earnings in line with its guidance with expected margins. I believe the shown revenues could likely drop more than expected in the soon-released Q3 earnings - I don't see a reason as to why Q4 should be so much weaker in revenues than Q3, considering the guidance was given a while ago; how could the company's management foresee a huge drop in Q4 without a sizable one in Q3?

Valuation

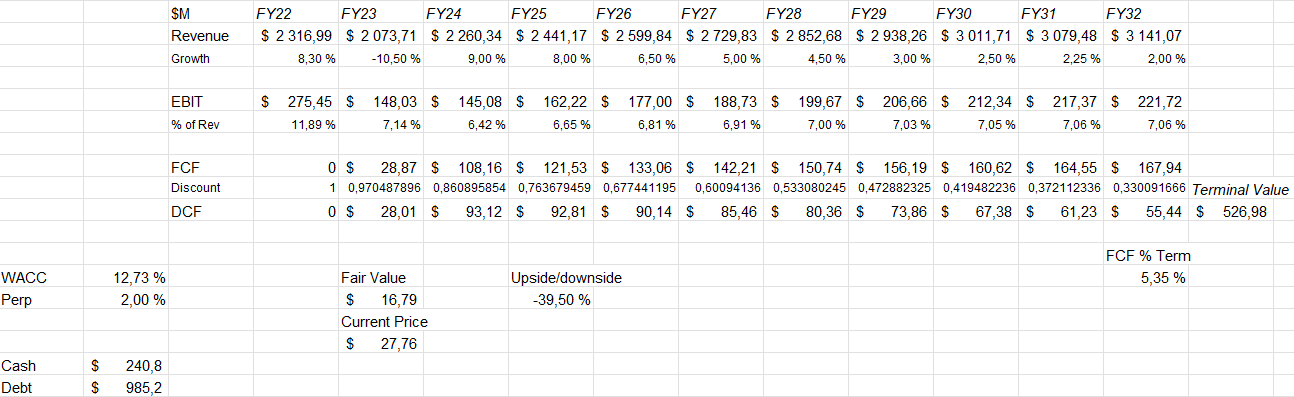

For FY23 the company is currently valued at a price-to-earnings ratio of around 7. This could be considered as cheap, but a further demonstration of the company’s value proves otherwise in my opinion. To visualize this I constructed a discounted cash flow model, that has a large 40% downside from the stock’s current price with reasonable assumptions:

DCF Model of Beazer (Author's Calculation)

{kind=link}

I expect the company to continue its growth after FY23, with a 9% growth that slowly fades into a perpetual growth rate of two percent. On the margin side, I expect Beazer’s margin to be around 7.1% for FY23 and getting a further drop in FY24 to 6.4%. This margin grows back into around a 7.0% margin, showing some pricing power from the company. These assumptions are reasonable in my opinion, although the assumed margins are still well above the company’s historical averages. The company should convert its earnings into free cash flow quite well as their needs for investments aren’t too large – a faster growth rate could increase capital expenditure needs, but I wouldn’t have a higher growth as a base case.

I used a weighted average cost of capital of 12.73%, a figure that I derived from a capital asset pricing model:

CAPM of Beazer (Author's Calculation)

I expect the company’s debt to have an interest rate of six percent in the future. As the company is quite leveraged, but deleveraging, I think their long-term debt-to-equity ratio should be around 35%.

On the cost of equity side, I use the United States’ 10-year bond yield as the risk-free rate. Currently the yield stands at 3.84%. The used equity risk premium is Professor Aswath Damodaran’s latest estimate updated on July 14 th . Tikr estimates the company’s historical beta to be 2.17, a very high figure. Finally, I add a liquidity premium of half a percent as the company’s stock is reasonably liquid. These expectations craft a 17.16% cost of equity and a cost of capital of 12.73% which I used in the DCF model.

Risks

The company is highly exposed to higher interest rates that the Federal Reserve has been pushing – higher interest rates generally cool down the real estate market, as mortgage payments become bigger and investors’ required yield increases. A slowdown in home sales could create a short-term hiccup in the company’s cash flows. This risk is well known by investors, as the stock has a beta of 2.17 – a very risky pick in terms of macroeconomic risks.

Also, as the company holds an unhealthy amount of debt, debt payments could pose a risk for investors. All the company’s debt is in long-term debt for the moment being, so they shouldn’t concern investors too much in the short term, but a prolonged hard period with home sales could tamper Beazer’s cash flows in a way that dangers their ability to pay back debts.

Closing Remarks

I believe the stock’s current valuation doesn’t account for an earnings drop that should be due. The company has had a couple years of boosted operating margins, but as the real estate market should cool down, these margins are at a risk. A DCF model reveals that the stock is currently overvalued if my assumptions of the company’s cash flows are near accurate. Before the company shows it can keep up margins that are stronger than historically, I have a sell-rating at the current stock price.

For further details see:

Beazer's Investors Should Be Cautious