BDX - Becton Dickinson: 4 Reasons To Buy This Growth At A Reasonable Price Play

2024-01-22 00:18:10 ET

Summary

- Becton, Dickinson and Company has underperformed the market and healthcare sector in recent years.

- The company's balance sheet has improved significantly which I believe will allow for increased returns of capital to shareholders going forward.

- BDX's recent guidance for FY 2024 has lowered earnings expectations, but the company has a history of beating consensus estimates.

- The stock is trading at an attractive valuation relative to the broader market.

- I am initiating BDX with a buy rating.

Becton, Dickinson and Company ( BDX ) has underperformed the broader market and healthcare sector more broadly over the past few years. The stock has delivered a total return of 4% over the past 5 years. Comparably, during the same time period the S&P 500 has delivered a total return of 94% and the Health Care Select Sector SPDR ETF ( XLV ) has delivered a total return of 69%.

Currently, the stock is rated a Hold by other Seeking Alpha analysts. There are four reasons why I disagree with this characterization and am bullish on the stock:

1. Balance sheet has improved significantly

2. Recently released FY 2024 guidance has lowered earnings expectations

3. Attractive valuation vs the broader stock market

4. Attractive valuation relative to historical norms and reasonable valuation vs peers

Seeking Alpha

1. Balance sheet has improved significantly

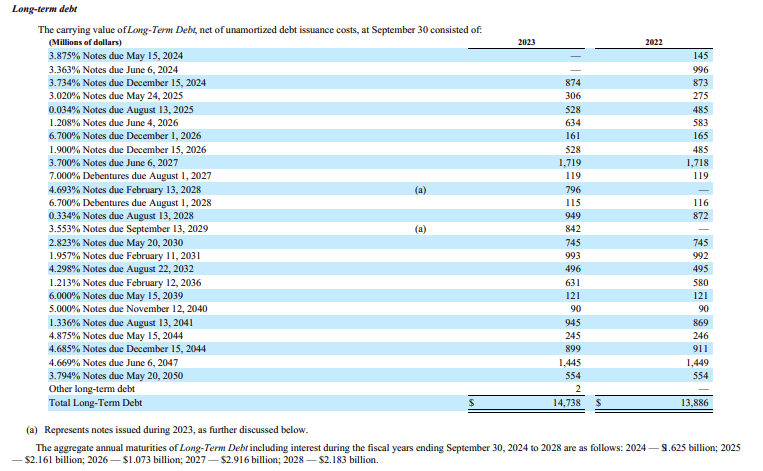

BDX took on a significant amount of debt to finance its $24 billion acquisition of C R Bard in 2017. As a result of this, BDX's net debt level and leverage level increased substantially. Since then, the company has gradually reduced debt levels and net leverage (based on adj. EBITDA) is now 2.6x which represents the lowest net leverage level since FY 2021. BDX currently has investment-grade credit ratings from Moody's, S&P, and Fitch.

Currently, BDX has $15.9 billion in total debt ($14.7 billion of which is long-term) with a weighted average cost of 3.0%. As shown by the table below, much of BDX's debt is longer-term in nature which is a positive as the company will not face significantly higher interest expense in the near-term due to refinancing needs.

Given the improved balance sheet, I believe BDX is well-position to focus more on returning capital to shareholders over the next few years. The company has stated that it is committed to increasing the dividend and returning cash to shareholders through share repurchases.

In November 2023, BDX announced a 4.4% increase in its dividend. This increase was the company's 52 consecutive years of dividend growth.

Prior to the company's decision to pursue larger-scale acquisitions resulting in stock issues, beginning with the 2015 acquisition of CareFusion for $12.2 billion, it had steadily reduced shares outstanding. Now that the company is focused on tuck-in M&A instead of transformational M&A, I expect it to use more cash to repurchase shares going forward.

As of September 30, 2023, the company had authorization to repurchase up to 8.8 million shares which represents ~3% of shares outstanding. In November 2023, the company executed accelerated share repurchase agreements to repurchase $500 million of its stock.

{kind=link}

2. Recently released FY 2024 guidance has lowered earnings expectations

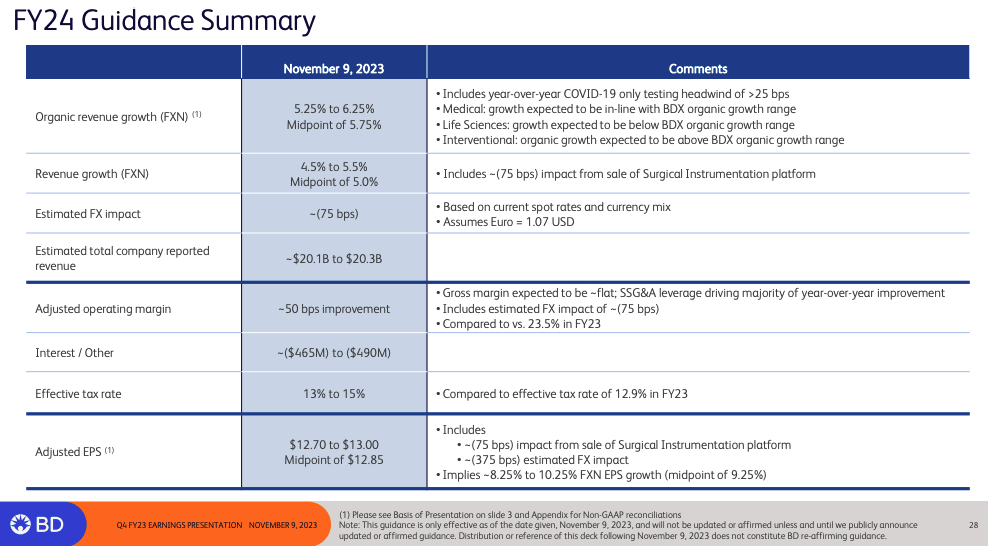

As part of its Q4 2023 earnings release, BDX issued FY 2023 guidance. The company expects revenue to come in at $20.1 billion to $20.3 billion and Adjusted EPS to come in at $12.70 to $13.00. Consensus estimates had called for revenue of $20.36 billion and Adjusted EPS of $13.51. Shares fell by ~10% due in part to the disappointing guidance.

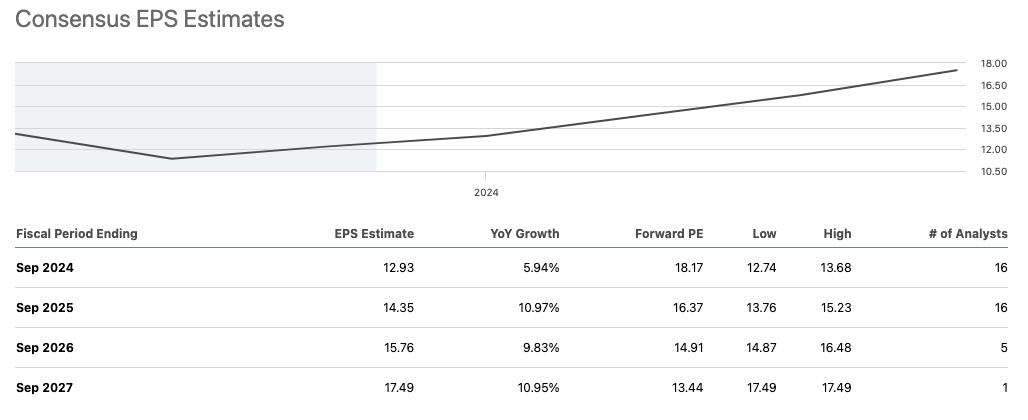

Wall Street analysts have updated their estimates following the release and consensus FY 2024 estimates now call for revenue of $20.24 billion and Adjusted EPS of $12.93.

I believe that BDX has lowered the bar to a level that it is confident that it can deliver on or beat for FY 2023. It is important to note that BDX FY 2023 results exceeded its initial projections. During Q4 2022, BDX projected that for FY 2023 it would deliver revenue of $18.7 billion and Adjusted EPS of $11.98. In the end, BDX delivered FY 2023 revenue of $19.4 billion and Adjusted EPS of $12.21.

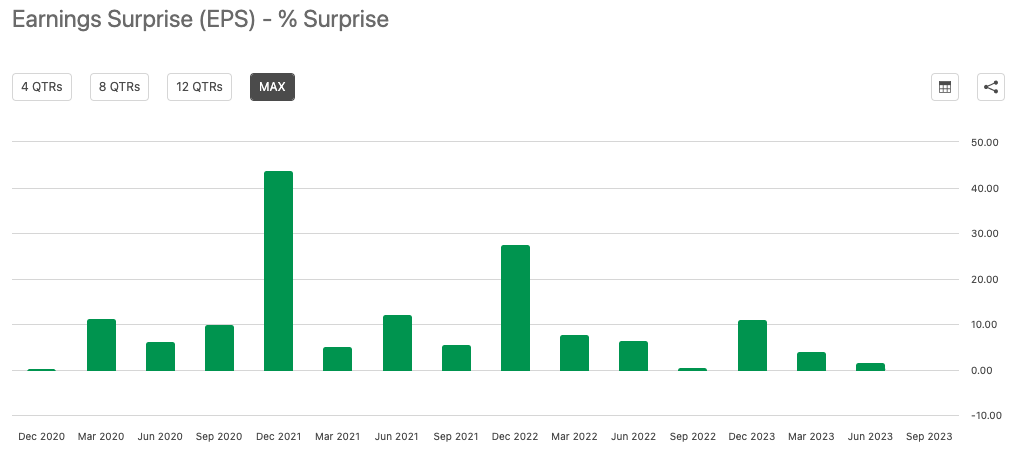

In addition to beating its own guidance last year, BDX also has a strong history of delivering results that have exceeded analyst expectations. As shown by the chart below, BDX has met or exceeded consensus EPS estimates for every quarter since December 2020.

For these reasons, I believe there is a good chance that BDX will deliver better FY 2024 results than current company guidance and consensus estimates indicate which would be bullish for the stock.

{kind=link}

{kind=link}

3. Attractive valuation vs. the broader stock market

BDX currently trades at 18x FY 2024 consensus EPS and 16.4x FY 2025 consensus EPS. Comparably, the S&P 500 trades at 21.5x consensus FY 2024 earnings. Thus, on a relative basis, BDX is somewhat cheaper.

Consensus estimates call for the S&P 500 to grow earnings by ~12% which compares to a consensus FY 2024 EPS growth rate of ~6% for BDX. However, over the following few years, BDX is expected to grow earnings by 10%-11% each year. Historically, the S&P 500 has grown earnings by high single-digit percentages each year. Thus, on the whole, I believe the long-term growth prospects for BDX are similar to the S&P 500.

Given the fact that I believe BDX and the S&P 500 have similar long-term growth potential, I view BDX as attractive given the current modest valuation discount. Moreover, I also believe that BDX could even trade at a premium due to the fact that its business is fairly defensive and less cyclical than the broader market. Evidence for the lack of cyclicality can be seen in the fact that BDX has historically exhibited an average 3-year trailing beta of 0.73x

{kind=link}

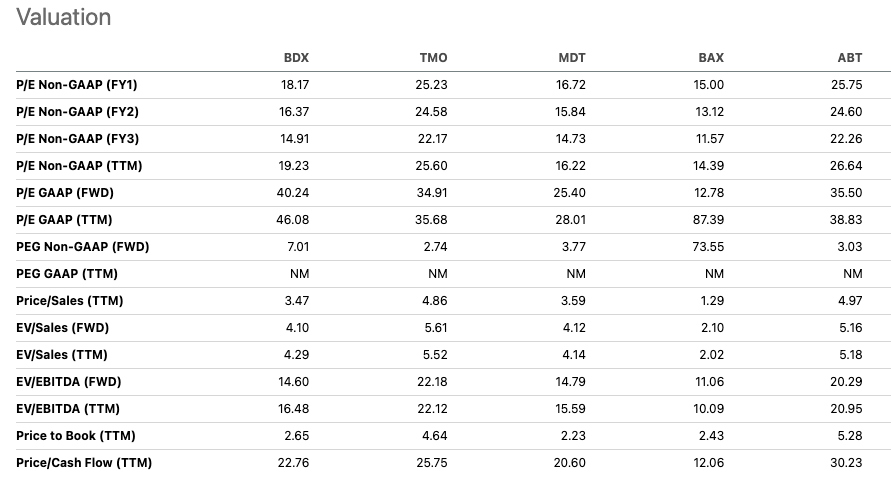

4. Attractive valuation relative to historical norms and reasonable valuation vs. peers

As shown by the charts below, BDX is trading at an attractive valuation relative to recent historical norms.

BDX's forward P/E ratio of 18.2x compares to a recent historical average of 21x. Additionally, BDX's trailing EV/EBITDA ratio of 18.7x compares to a recent historical average of 21.1x. Thus, based on these metrics I believe BDX is trading at a fairly attractive valuation relative to historical norms.

BDX trades towards the lower end of its peer group in terms of valuation. Medtronic ( MDT ) and Baxter International ( BAX ) trade essentially in line with BDX based on key metrics such as forward P/E ratio and forward EV/EBITDA while Abbott Laboratories ( ABT ), and Thermo Fisher Scientific ( TMO ) trade at a premium. Given the fact that BDX is expected to grow EPS at a similar rate to these companies, I believe BDX's current valuation is reasonable to peers.

Based on these metrics, I believe a reasonable valuation for BDX is a forward P/E ratio of 21x which implies a fair value of $272. This would mean BDX is trading in line with its recent historical norm and in line with the S&P 500 (which I view as having similar growth potential but more cyclicality.)

Author (Seeking Alpha data)

{kind=link}

Key Risks To Consider

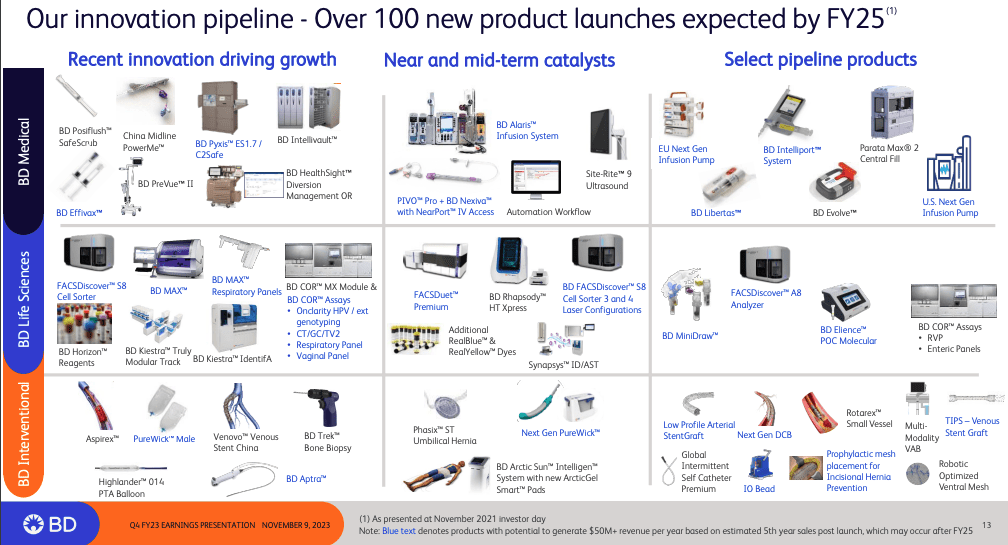

One key risk to consider is that BDX's pipeline fails to deliver. The medical technology business requires almost constant innovation as competition is intense to provide the best patient experience possible. BDX targets annual R&D spending of 6% of sales. During FY 2024, BDX spent $1.2 billion on R&D.

Over the past 2 years, BDX has launched 52 new products. By FY 2025, the company plans to launch over 100 new products including major launches across all of its divisions. If the company fails to deliver on new product launches, it will be very difficult for the company to grow earnings going forward. While the success or failure of any one product currently in the pipeline is difficult to predict, the diverse nature of the pipeline is positive as the company is fairly diversified in terms of its product pipeline. However, investors should closely monitor the product pipeline for any signs of systemic challenges across multiple products.

Another key risk to consider is that BDX could face reimbursement challenges in the future due to potential changes in the way that insurance companies pay for medical services as governments continue to consider and move toward value-based reforms. While significant changes in reimbursement structure are unlikely in the near term, it is a risk that investors must continue to monitor as changes to reimbursement rates could have negative consequences for BDX.

{kind=link}

Conclusion

BDX has delivered weak results for shareholders over the past few years and is currently out of favor with investors. However, I believe that shares offer an attractive investment opportunity at current levels.

BDX has significantly improved its balance sheet over the past few years. The result of this is that I expect BDX to focus more on returning capital to shareholders via increased share repurchases over the next few years which should serve as a positive for the stock.

BDX shares recently fell after the company released FY 2024 guidance which was below consensus levels. The company has a long history of delivering better than consensus results and thus I believe there is a good chance that it will end up beating FY 2024 results.

The stock trades at a modest valuation discount to the S&P 500 but has similar growth prospects. Moreover, as a healthcare company, BDX's earnings are generally less subject to cyclical risks. For this reason, I believe BDX should trade in line with the broader market as opposed to the current discount. Additionally, I find BDX attractive based on its current valuation relative to its own historical norms.

I am initiating the stock with a buy rating and would consider downgrading the stock if it fails to meet earnings expectations in FY 2024. I would also consider downgrading the stock if the valuation pictures become less attractive.

For further details see:

Becton, Dickinson: 4 Reasons To Buy This Growth At A Reasonable Price Play