BDX - Becton Dickinson And Company: Strong Q4 But Clouded By 75bps Growth Headwind From China In FY24

2023-11-13 08:56:43 ET

Summary

- Becton, Dickinson and Company (referred hereon as BD) is a global medical device company with a diversified and high-quality portfolio.

- BD's three main segments, BD Medical, BD Life Sciences, and BD Interventional, contribute to its strong revenue growth.

- Weakness in China is expected to impact BD's drug delivery device business in FY24, leading to a "Hold" rating and a $200 fair value.

Becton, Dickinson and Company (BDX) is a global medical device company offering a broad range of medical supplies, devices, laboratory equipment, and diagnostic products used by the healthcare industry. The company has a highly diversified medical device and consumable portfolio with industry-leading quality. However, weakness in China is expected to predominantly impact its drug delivery device business in FY24. I am initiating coverage with a "Hold" rating and a $200 fair value.

Diversified and High-Quality Portfolio

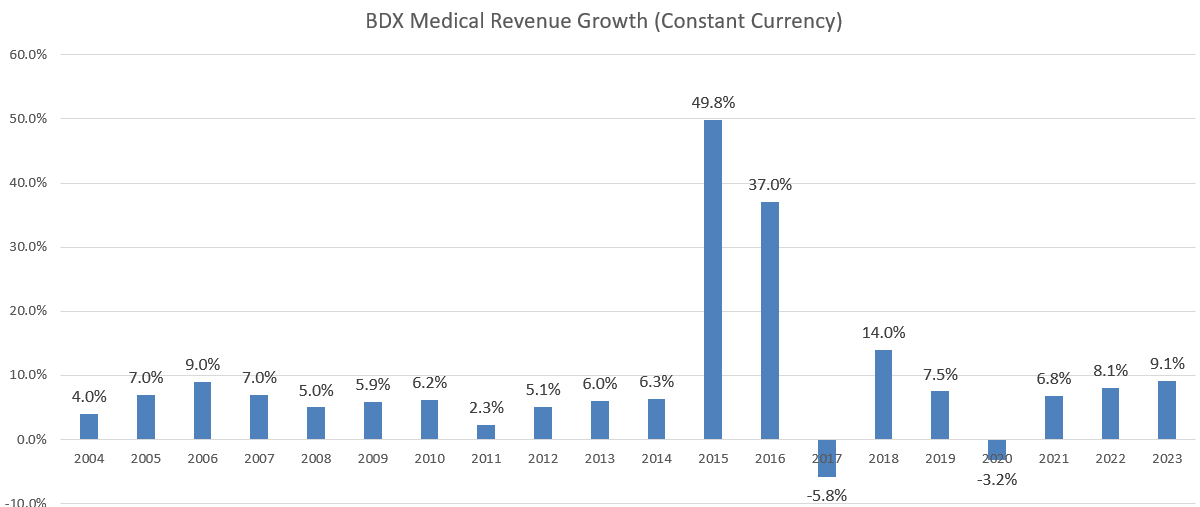

BD operates under three main segments: BD Medical, BD Life Sciences, and BD Interventional. BD Medical is the largest business segment, accounting for 49% of group revenue. It focuses on selling medication delivery solutions, medication management, and pharmaceutical systems. The product range includes peripheral intravenous catheters, syringes, infusion pumps, advanced peripheral catheters, and various other categories. These products play a crucial role in the day-to-day operations of hospitals, clinics, physicians' offices, and retail pharmacies, making them essential in the healthcare system. BD Medical is widely regarded as a high-quality manufacturer in the healthcare industry, experiencing robust growth at mid-to-high single digits on a constant currency basis over the past three years.

{kind=link}

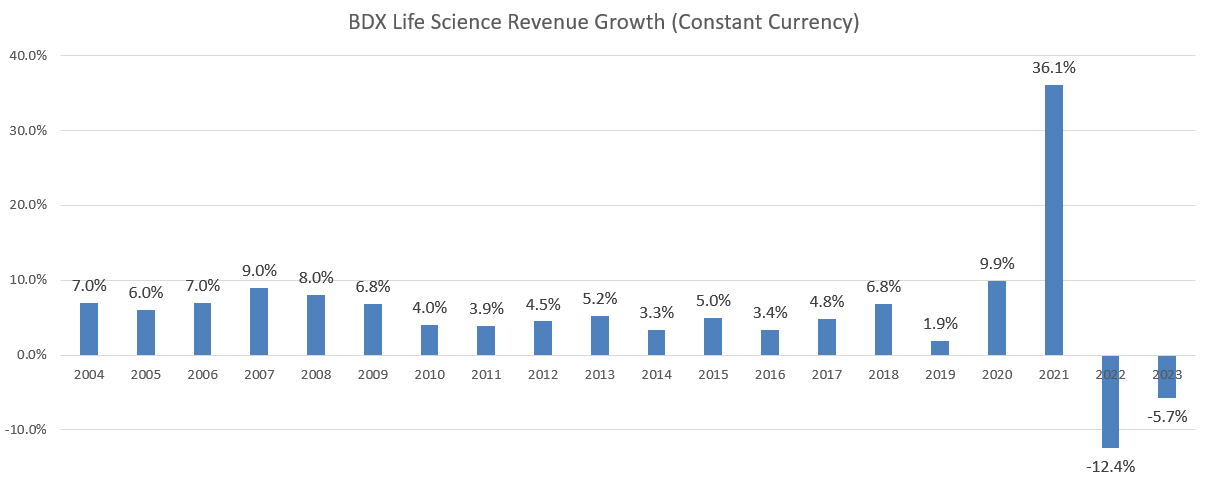

BD Life Sciences offers integrated diagnostic solutions and biosciences products, including cell sorters, analyzers, antibodies, and kits for performing cell analysis. The primary customers for BD Life Sciences are hospitals, laboratories, and clinics. During the pandemic, BD experienced explosive revenue growth due to manufacturing COVID-testing kits. However, in the post-pandemic period, the business is encountering growth challenges, with high year-over-year comparisons. BD Life Sciences revenue declined by 12.4% in FY22 and another 5.7% in FY23.

{kind=link}

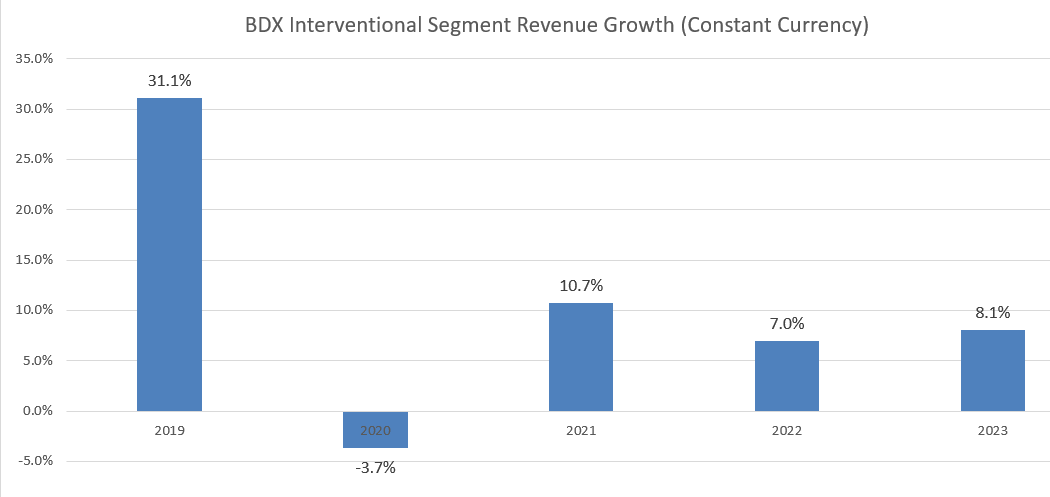

BD Interventional provides vascular, urology, oncology, and surgical specialty products primarily used in hospitals, with growth closely tied to surgical procedures. From my perspective, BD has executed an excellent strategy to enhance its penetration in hospitals, resulting in an impressive 8.1% revenue growth in FY23 on a constant currency basis.

{kind=link}

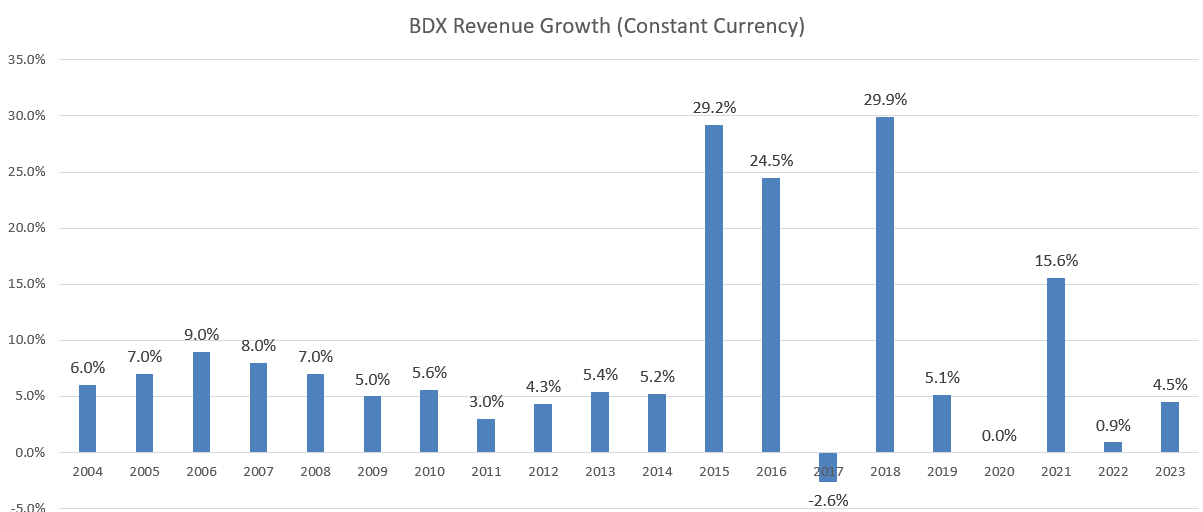

Overall, I believe BD's portfolios are well-diversified, and its products play a vital role in everyday patient care. Furthermore, BD is strategically positioned for growth with a robust pipeline of new products. During the Q4 FY23 earnings call , the management reported significant progress in their innovation pipeline, having launched 27 key new products that benefit researchers, providers, and patients. These products integrate AI, robotics, and other advanced technologies. BD remains committed to launching over 100 new products by FY25, as outlined in their Investor Day target. In the medical device industry, product innovation is crucial for growth, and BD stands out with a best-in-class product portfolio characterized by constant innovation. Over the past five years, they have consistently delivered more than 5% average revenue growth in constant currency.

{kind=link}

Large Acquisitions

Historically, BD has deployed its cash from operations into large acquisition deals that have been transformative for its core business. These acquisitions have enabled BD to enter new markets and broaden its product portfolios.

In 2015, BD acquired CareFusion for $12.2 billion, marking its entry into Medication Management and Patient Safety Solutions. In 2017, the acquisition of Bard for approximately $24 billion further expanded BD's reach in vascular, urology, oncology, and surgical specialty products. The Bard acquisition was particularly significant, contributing to BD's growth in emerging markets, including China. In 2022, BD acquired Parata Systems for $1.525 billion, entering the new Pharmacy Automation Solutions market.

While transformative acquisitions can bring strategic benefits, large deals are challenging to integrate, carry higher legal and operational risks, and may impact the quality of the acquiring company's balance sheet.

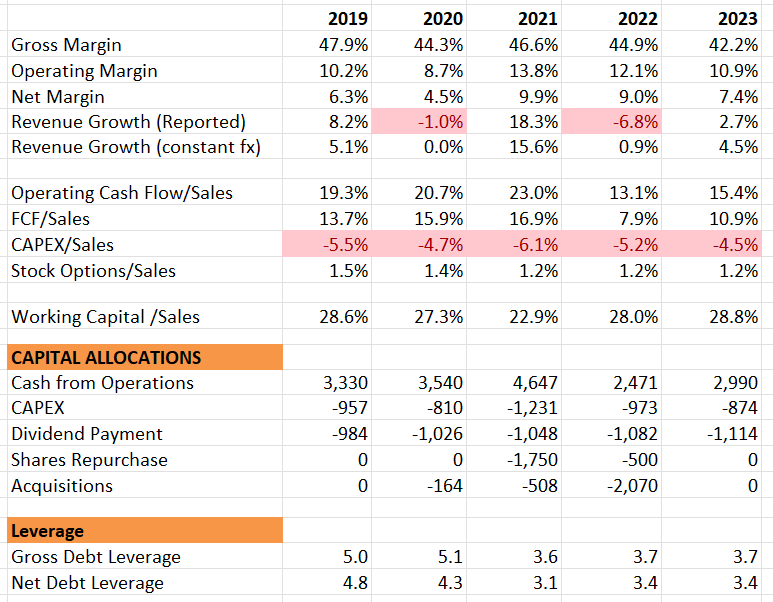

Over the past nine years, BD generated $26.6 billion in cash from operations, coincidentally spending the same amount on acquisitions. This approach contrasts with a preference for cash distribution through dividends or share buybacks. Due to these acquisitions, BD's gross debt leverage increased to 5x in FY19. Since then, the company has been actively working to deleverage its balance sheet, with gross leverage standing at 3.7x at the end of FY23, although it remains relatively high compared to other medical device companies.

{kind=link}

Weak China Growth Despite Strong Quarterly Result

BD reported a robust Q4 FY23 result , achieving a 5.9% revenue growth on a currency-neutral basis. Notably, the Life Science segment returned to positive growth after three consecutive quarters of negative growth, attributed to declining revenue from COVID testing-related business. For FY23, the company surpassed expectations by delivering a base organic revenue growth of 5.8%, exceeding the initial guidance by 100 basis points. Overall, it was a strong finish for FY23.

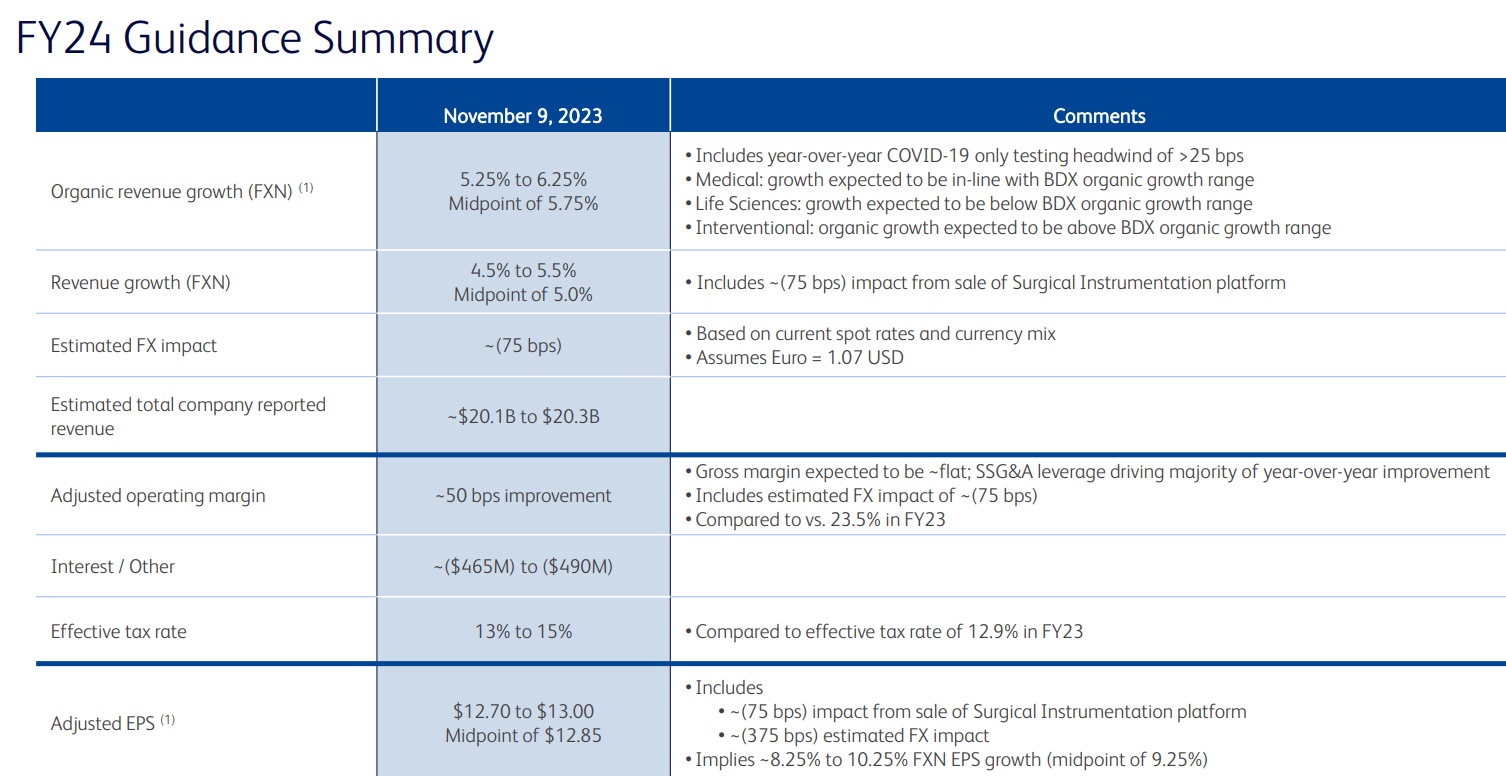

In addition to the positive results, the company issued guidance for FY24, projecting a 5.75% organic revenue growth at the midpoint of the 5.25% to 6.25% range.

{kind=link}

Despite the strong overall performance, BD's Medical business experienced a decline in medication delivery systems in China. During the earning call , their management explained this weakness, attributing it to several factors. The entire demand for healthcare in China is quite weak, given the recent pandemic and the implementation of a zero-covid policy. Additionally, the government's ongoing anti-corruption efforts in healthcare have led to a pause in many procurements within the healthcare systems. BD specifically highlighted the impact of weak volume-based procurement in China. They project their China business to show flat to modest growth in FY24, creating a 75 basis points growth headwind for the company.

In my view, their guidance for China may be somewhat optimistic. Their assumption appears similar to that of most major multinational companies: a decline in H1 in China, followed by growth in the second half of FY24. However, I believe the weak growth in China could extend for more than one year, considering that the current anti-corruption campaign is still ongoing, and Chinese domestic consumption remains very weak.

As such, I still anticipate some risk of guidance cuts for the company in the coming quarters.

{kind=link}

Key Risks

BD Alaris infusion system : The FDA requested BD to recall their Alaris Pump Module due to the risk of the keypad lifting up, potentially leading to unresponsive or stuck keys as a result of fluid entry. This prompted a Class I recall, the most serious type defined by the FDA. The recall of the Alaris infusion pump created significant growth headwinds for the company, requiring them to halt product distribution and undertake a lengthy process of re-submitting FDA clearance. In July 2023, BD received FDA 510 clearance for the updated Alaris Infusion System and resumed product distribution. During the call , they mentioned initiating the shipping of Alaris products, anticipating a gradual recovery in growth from the Alaris Infusion System in the next year, albeit with an expected ramp-up period.

Debt Leverage : As mentioned earlier, BD's gross debt leverage is above 3x, which is relatively high compared to other medical device companies. In FY23, they generated approximately $3 billion in cash flow from operations, primarily attributed to their effective inventory management in the second half of the year. The company anticipates double-digit growth in cash flow from operations in FY24. This enhanced cash generation is expected to provide them with the capability to reduce their high levels of debt.

In FY23, BD demonstrated a commitment to debt reduction by paying down over $700 million when they temporarily halted their share repurchase program. This strategic move suggests an active effort to manage their debt levels. In my opinion, it is likely that their debt leverage will decrease over time, barring any substantial new debt incurred due to another large acquisition.

Valuation

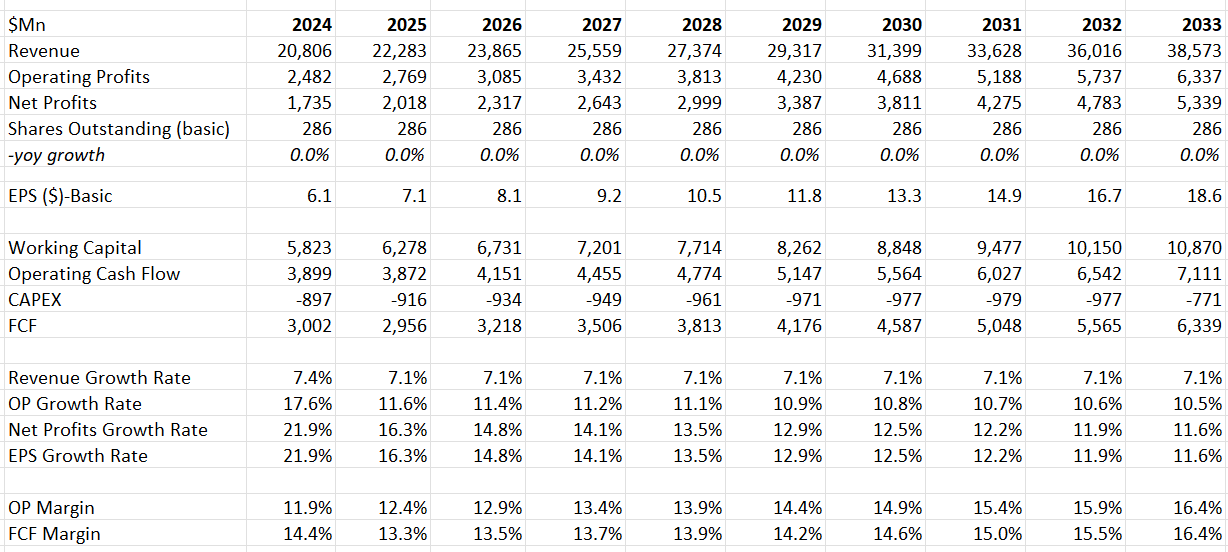

The model's assumptions for FY24 align with the company’s guidance at the midpoint. In my view, the company may have underestimated the challenges in their China business, thus limiting their ability to achieve the higher end of the guidance range. For normalized revenue growth, I assume a 5.5% organic revenue growth, consistent with their historical revenue growth pattern. Additionally, I anticipate that tuck-in acquisitions could contribute another 1.6% to revenue growth. Due to their robust new product pipeline and operating leverage, their operating margin is expected to expand over time. According to my calculations, the DCF model forecasts a 50 basis points annual margin expansion.

{kind=link}

The model employs a 10% discount rate, a 4% terminal growth rate, and a 14% tax rate. Based on my estimate, the fair value of their stock price is calculated to be $200 per share.

Conclusion

I appreciate BD's extensive range of product portfolios, widely utilized throughout the healthcare system. Their dedication to new product research and launches is expected to contribute significantly to topline growth and margin expansion. However, the challenges in their China business could potentially impact near-term growth. In my evaluation, the current stock price appears overvalued, leading me to initiate a "Hold" rating with a fair value per share estimated at $200.

For further details see:

Becton, Dickinson And Company: Strong Q4 But Clouded By 75bps Growth Headwind From China In FY24