BDX - Becton Dickinson Stock Is A Hold Here's Why

2023-10-04 18:25:13 ET

Summary

- Becton, Dickinson and Company is a global healthcare company specializing in medical supplies, devices, and diagnostic products.

- BDX saw solid growth in Q3 driven by strong demand for pharmacy automation systems and medical devices.

- The company raised its revenue guidance for FY23 and expects continued profitability improvement in the near future.

- However, the stock has a limited upside potential, based on my calculations. It's a "Hold" today, but may become a "Buy" in case it cools down a little.

The Company

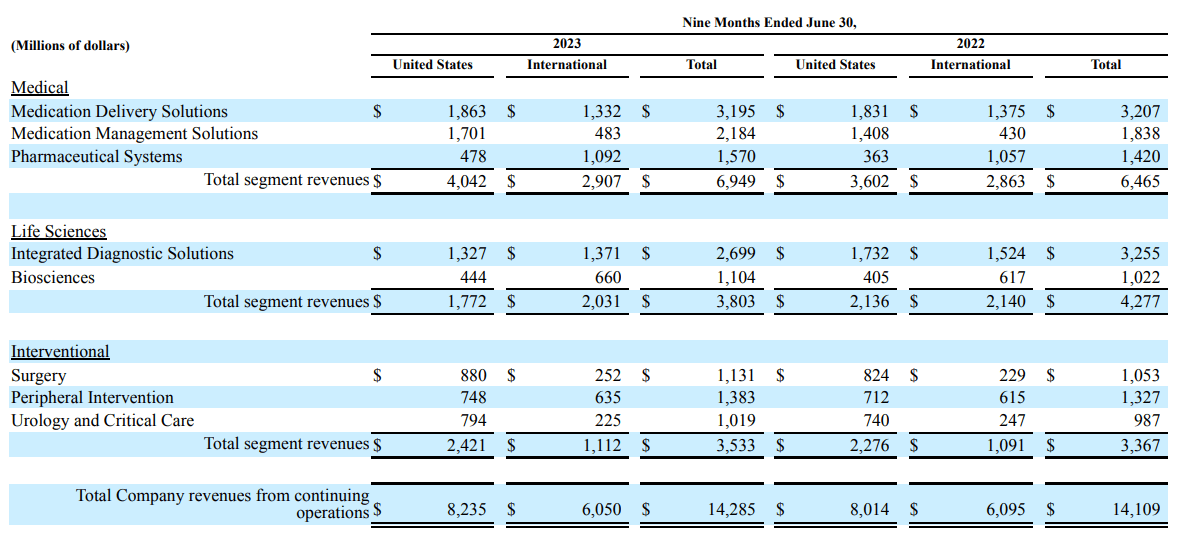

Becton, Dickinson and Company ( BDX ) is a $75-billion market cap global healthcare company that specializes in developing, manufacturing, and selling a wide range of medical supplies, devices, laboratory equipment, and diagnostic products. They serve healthcare institutions, physicians, researchers, clinical laboratories, the pharmaceutical industry, and the general public worldwide. According to the latest 10-Q report , BDX has 3 main operating segments:

-

BD Medica l [48.6% of total sales]: provides a variety of medical products, including intravenous catheters, syringes, medication delivery systems, and sharps disposal systems.

-

BD Life Sciences [26.6%]: focuses on specimen and blood collection products, diagnostic testing systems, microbiology products, and cell analysis tools.

-

BD Interventional [24.7%]: offers surgical products, including hernia repair, surgical infection prevention, and urology products.

{kind=link}

{kind=link}

BDX saw solid growth in fiscal Q3 FY2023 driven by strong demand for pharmacy automation systems and medical devices [BD Medical and BD International segments]. The firm obtained FDA clearance for the BD Alaris Infusion System, but the management anticipates modest initial sales growth as it focuses on replacing or upgrading systems for existing customers [ BDX's Q3 earnings call ].

The BD Alaris Infusion System is a modular and comprehensive infusion system that includes high-volume pumps, syringe and PCA pumps, breath monitoring, dose error reduction software, and a variety of other features. It is the only modular infusion system in the United States that can be customized to meet the specific needs of each patient.

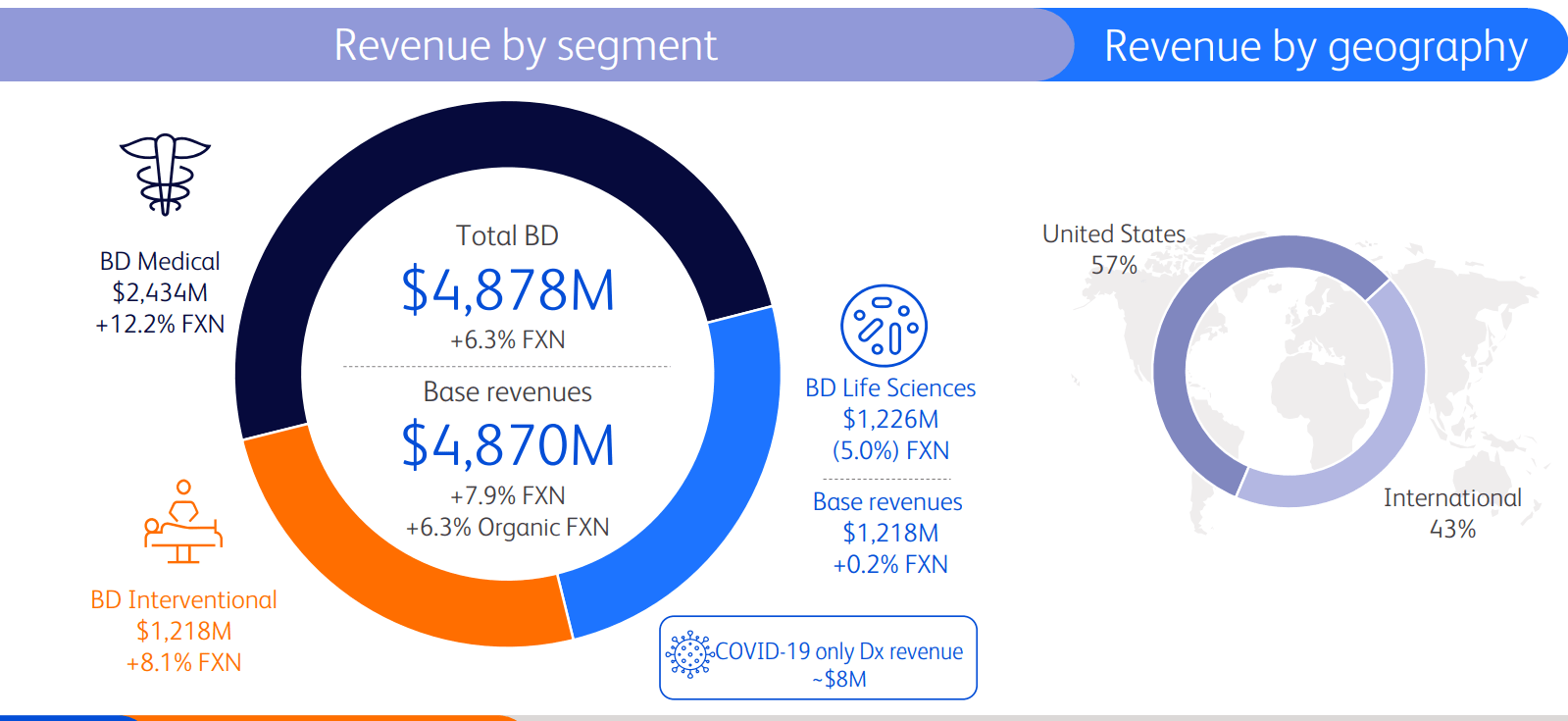

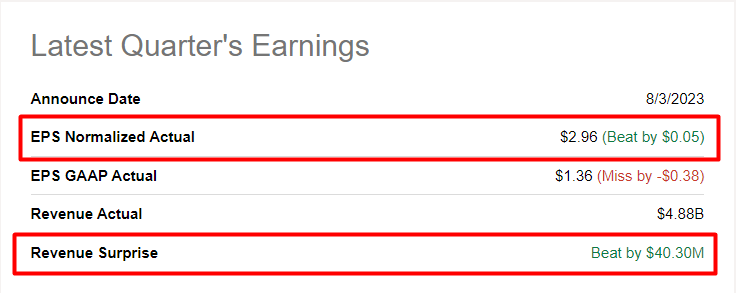

Back to the financial results. Third-quarter adjusted EPS increased by 11% to $2.96, surpassing expectations [Non-GAAP basis]. Revenue rose to $4.9 billion [also beat consensus], with a 5.1% increase as reported and 6.3% on a currency-neutral basis, excluding COVID-only diagnostic testing.

{kind=link}

BD Medical reported strong operational sales growth of 24.8%, benefiting from dispensing products and the Parata acquisition. The Pharmaceutical Systems segment posted 14.0% operational sales growth due to high demand for drug delivery devices. BD Life Sciences sales declined 5.1% due to lower testing volumes and distributor destocking in specimen management products.

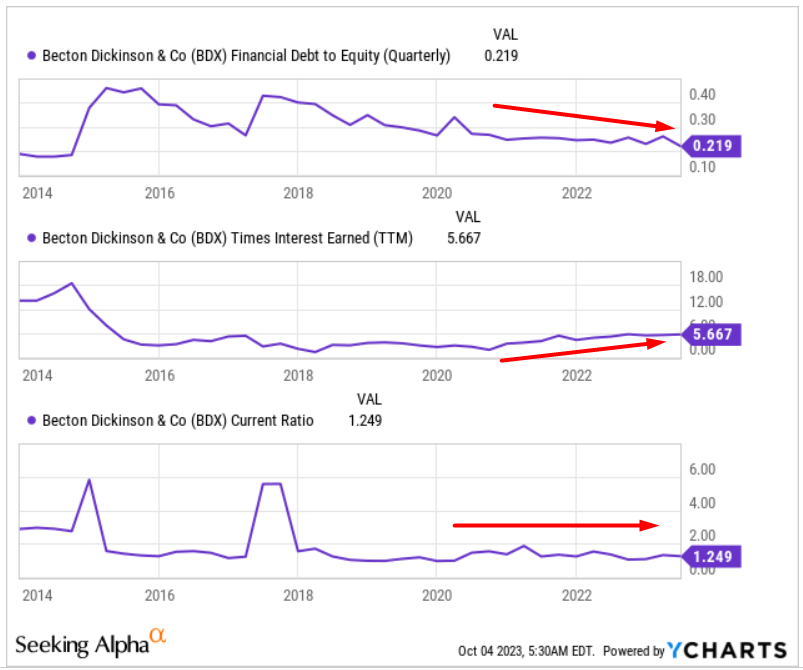

At the end of the third quarter, the amount of total cash on the balance sheet decreased by 11.57% year-on-year, while total debt (current and non-current) increased by 4.46% in the same period. However, in terms of key leverage and liquidity metrics, BDX looks good - both in absolute terms and in terms of momentum:

{kind=link}

Overall, BDX's Q3 profitability measures showed a slight YoY improvement, with a gross margin of 44.9% [+13 basis points] and an operating margin of 14.53% [+89 b.p.]. And it looks like the improvement should continue in the near future - at least that's what management says.

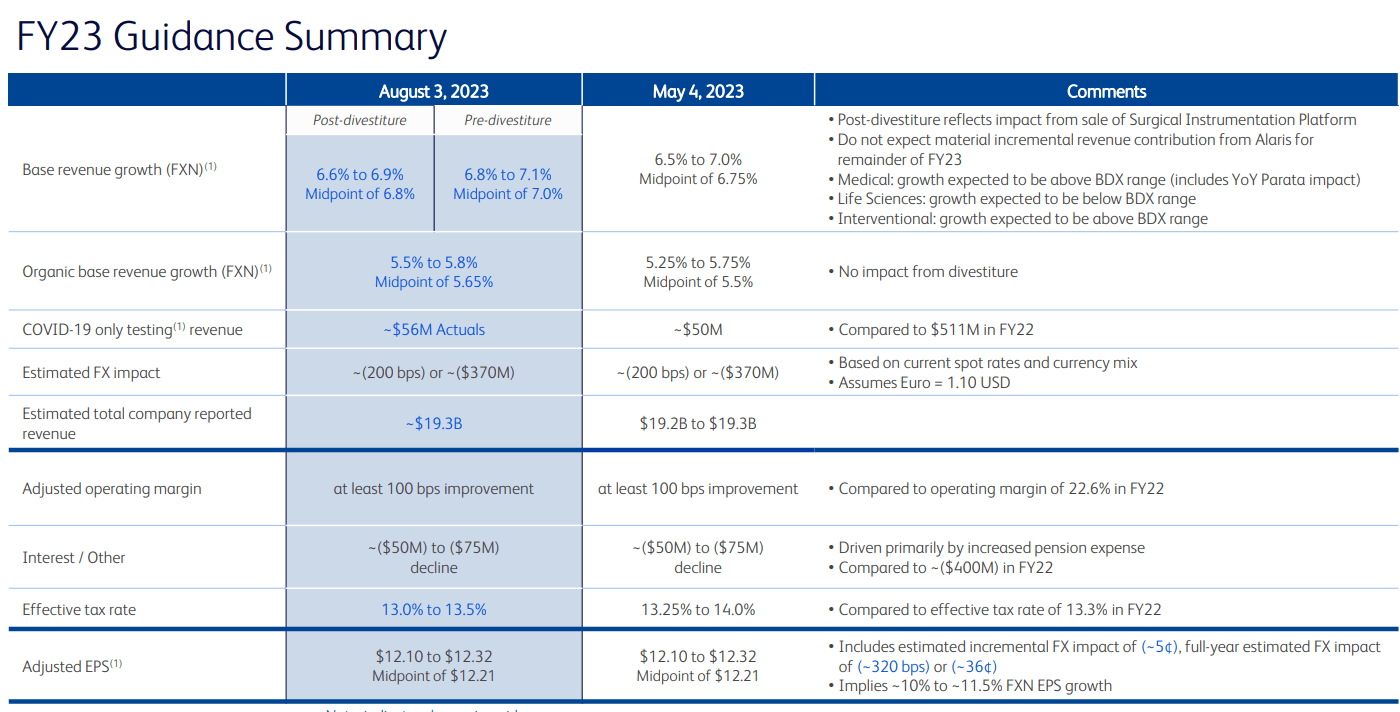

BDX raised its FY23 revenue guidance to $19.3 billion, which includes YTD COVID-only testing revenue. The firm expects FY2023 adjusted EPS of $12.10-12.32, factoring in impacts from divestitures and currency translation. On a currency-neutral basis, adjusted EPS is projected to grow by 10.0%-11.5%:

{kind=link}

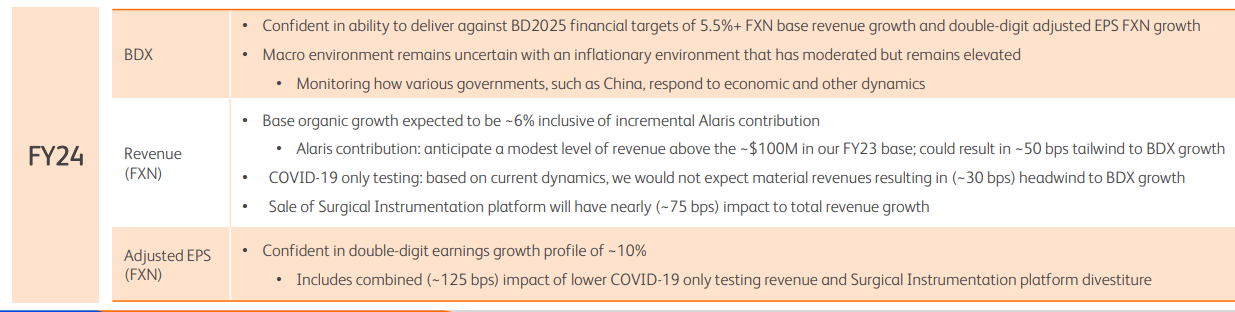

For FY2024 the company anticipates its core, excluding acquisitions and divestitures (organic growth), to be ~6%, including the additional contribution from the new Alaris Infusion System. And even accounting for lower COVID-testing revenue in FY2024, BDX expects to have a bottom line growth of ~10%, which is solid:

{kind=link}

In my opinion, BDX has quite favorable conditions for future growth. Analysts at KPMG forecast that the global medical device market is set to grow at a CAGR of 5% through 2030. I expect this figure to be underestimated, as the average age of medical devices, according to the Advancement of Medical Instrumentation ((AAMI)), was ~7.4 years in the middle of last year. A 2016 Becker's Hospital Review article cited a figure of 4.6 years, which was a long-standing record at the time. The minimum age of devices is about 7 years. That means, on average, medical devices have been slow to update in recent years, which has most likely created some sort of deferred demand that should give BDX a tailwind in the coming years.

But what about the company's valuation?

The Valuation

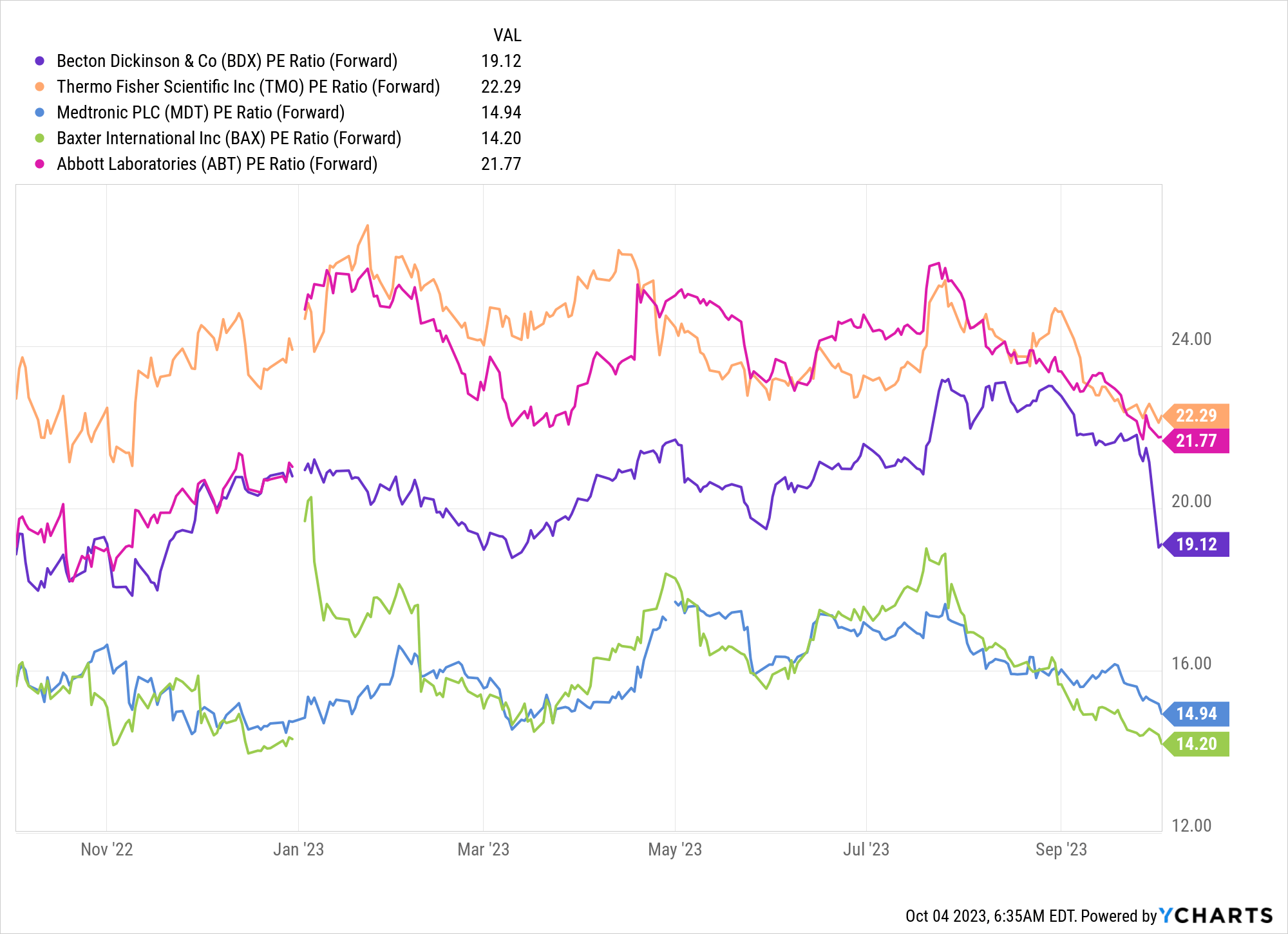

When I compare BDX to a number of other companies, the company seems fairly valued to me - perhaps even a little overvalued in terms of its next-year P/E ratio:

{kind=link}

However, in the context of the last 3 years, we see that BDX appears slightly undervalued, deviating from the relatively stable average P/E ratio [FWD, ~20.61x] for the discussed period:

The problem with the P/E ratio is that the net income of the company varies too much over different time periods. However, EBITDA-based ratios help to circumvent this problem as they tend to show a smoother picture. Based on EV/EBITDA [FWD], BDX is trading at a discount of 21.4% - one of the largest deviations in the last year:

Returning to the P/E ratio, we see the implied forward ratios continue to shrink - implying that the company will continue to actively grow earnings per share. If this is the case and BDX trades at its long-term average P/E of ~20.6x in 2024, the stock should be worth ~$279 over the next 12 months, which is 7.7% above its last closing price.

The Verdict

BDX has a pretty good presence in a strong and growing market where it definitely has a lot of prospects. However, the upside potential of only 7.7% that I calculated does not give me the right to rate the stock as a "Buy" - maybe it is a good investment in the long term (5-10 years), but obviously not in the medium term (1-2 years). So the existence of a slightly positive price potential makes the BDX stock a "Hold" in my opinion.

Thanks for reading!

For further details see:

Becton, Dickinson Stock Is A Hold, Here's Why