GEO - Behind Bars But Ahead On Returns? Assessing GEO Group's Prospects Into 2023

Summary

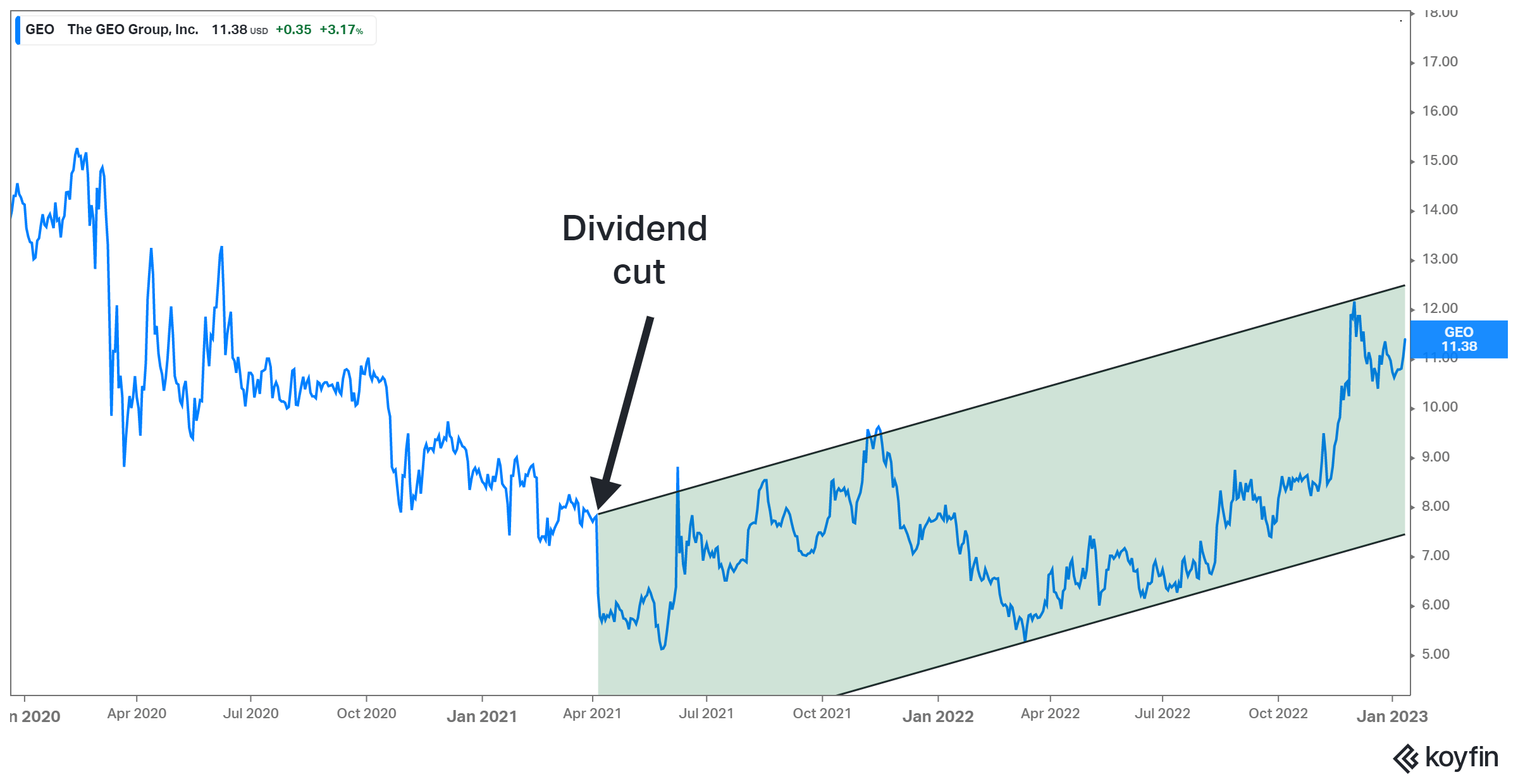

- Shares of The GEO Group have more than doubled since the dividend was cut.

- The leadership team appears to be taking appropriate actions despite the difficulties.

- That said, it might be an ideal time to lock some profits.

The days when The GEO Group ( GEO ) was a high-yield dividend investor's darling are long behind us. While income-oriented investors shed a tear at the time, management's decision to suspend the dividend to focus on paying down debt and return to self-funding CAPEX appears to have been quite fruitful.

The stock has more than doubled from its lows following the dividend cut, with investors no longer pricing shares based on their underlying dividend yield but as a deep value opportunity.

GEO Group's stock price chart (Koyfin)

{kind=link}

Another catalyst that has likely contributed to the stock's gains over the past year is Michael Burry's vote of confidence in GEO. In Scion Asset Management's latest 13f filings , it was revealed that Michael Burry added five stocks to his fund and also heavily doubled down on his GEO position, which was more than tripled compared to the previous quarter.

In fact, up until the prior quarter, GEO was Scion Asset Management's sole publicly-traded equity holding. Considering how picky Mr. Burry is with his stock selection, his high conviction toward the stock was interpreted by many investors as a great vote of confidence in GEO's prospects.

Mr. Burry's faith in the stock likely stems from the fact that GEO's management has navigated the adversity that concerns its very own business model (ethical considerations over private prisons) rather skillfully. Overall, it appears that management has positioned the company well to self-fund its operations and potentially resume returning capital to shareholders.

That said, with shares now trading near their highest levels since the summer of 2022, the case of GEO being a deep-value stock may be fading. Therefore, it might be a good opportunity for investors to lock in some profits as we advance into 2023.

How Has The GEO Group Coped With Recent Challenges?

GEO's business model, which is focused on creating value for shareholders through providing government agencies with secure facilities, processing centers, and prison space, has, over the years, come under intense scrutiny and criticism from the public.

Despite corporate and government institutions giving the company a hard time, GEO's management has helmed the ship quite skillfully in rough waters.

The shortfall in bank financing

As public opposition to private prison companies swelled in recent years, major banks began to cut ties with the industry about four years ago. This presented a significant obstacle for GEO because, as is the case with any company whose operations revolve around real estate, debt is a critical means for the company to fund its future growth.

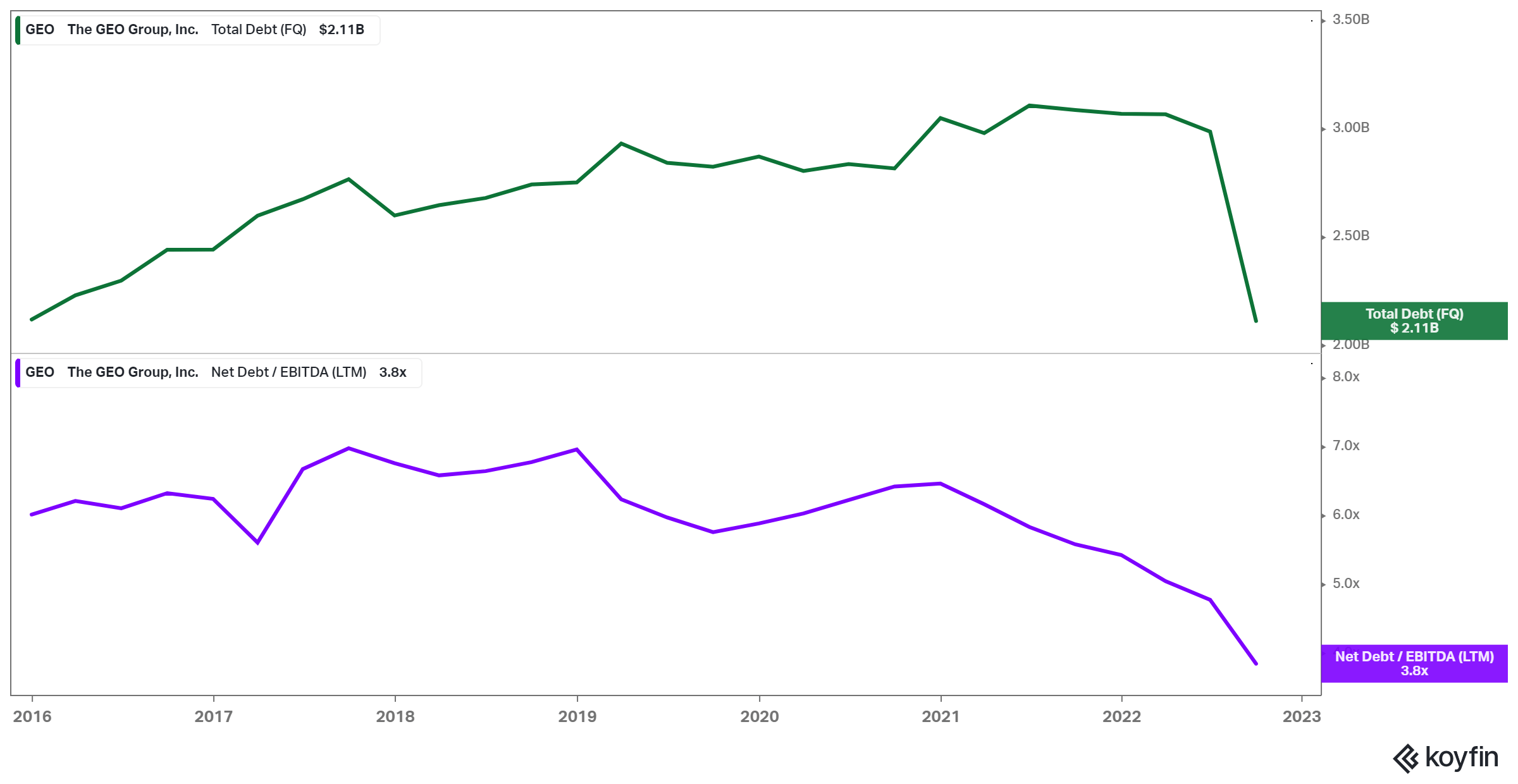

At the same time, with shares trading at a discount, issuing equity would have been disastrous to combat this development. Some months later, management saw that their best bet was to cut the dividend and commence aggressive deleveraging. If you can't issue/refinance debt, you might as well pay it down and self-fund everything in the future. Not the best scenario, but you do the best with what you have. Total debt has now been cut by around 1/3, while the company's net debt / EBITDA has fallen to 3.8X.

GEO Group's total debt and leverage ratio (Koyfin)

{kind=link}

Thus, the company has already made great progress toward its goal of lowering its net leverage to below 3.5X adjusted EBITDA by the end of 2023 and to below 3X adjusted EBITDA by the end of 2024.

Going forward, management has made clear they remain focused on allocating most of the free cash flow towards further downsizing net recourse debt by about $200 million annually. Once they reach their stated debt and leverage reduction goals, management intends to start considering resuming returning capital to shareholders.

President Biden's directive to terminate agreements with private prison companies

Another misfortune that GEO had to contend with was the Executive Order issued by President Biden about two years ago, directing the Department of Justice to discontinue renewing contracts with privately-operated, for-profit prisons. This development sent shivers down the spines of GEO's investors.

Nevertheless, GEO found ways to somewhat circumvent the order. Not only does the order not apply to facilities that GEO manages on behalf of U.S. Immigration and Customs Enforcement, but GEO also started to engage in intergovernmental service agreements with counties. Through this way, counties then contract directly with the federal government for detention services, allowing GEO to renew contracts with these facilities and to some extent, bypass this order.

Thus far, renewals persist with no notable disruption. For example, in Q3, GEO successfully renewed two managed-only contracts in its Secure Services segment, including a two-year term for the 1,948-bed South Bay Correctional and Rehabilitation Facility in Florida and a five-year term for the 500-bed Phoenix West correctional and rehabilitation facility in Arizona.

It Could Be An Ideal Time To Lock In some Gains - Here's Why

Following GEO's updated approach toward deleveraging and its overall operations remaining rather robust despite the difficulties that arose over the past two years, the stock has performed quite nicely.

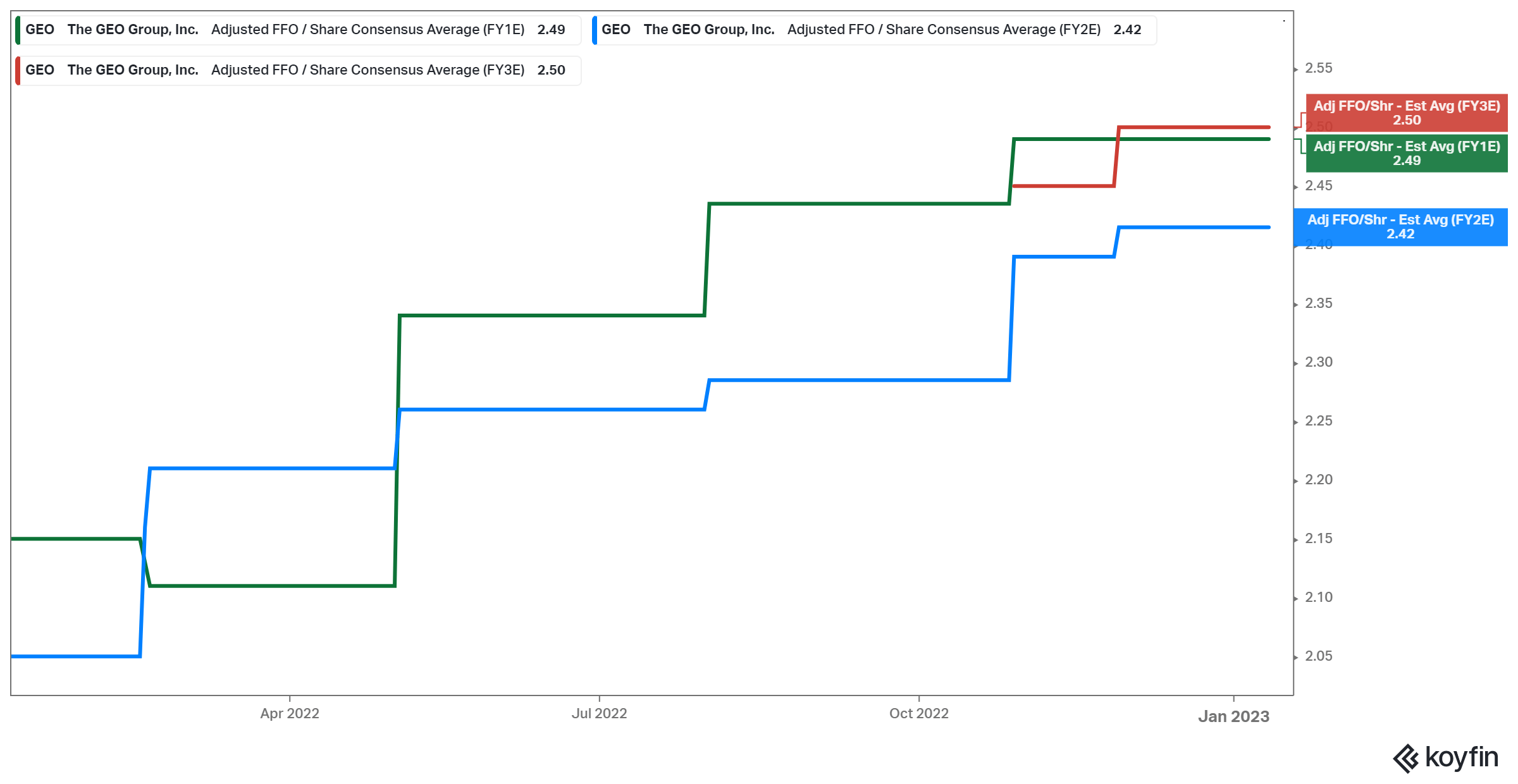

Analysts have been increasingly positive about the company's future profitability as well, expecting AFFO/share to hover close to $2.50 in the coming years.

{kind=link}

These estimates should translate to a free cash flow of about $280 million. While this could improve with interest expenses on the decline, let's assume free cash flow remains rather constant in the years following 2024, which is when management is supposed to start assessing resuming capital returns toward shareholders. This is to be prudent against further challenges and the lack of growth prospects.

If they start distributing about 50% of free cash flow (close to $140 million), that would imply a dividend yield of close to 10% at the stock's current price levels. This sounds like an attractive investment proposition. However, considering that uncertainty remains over what percentage of the free cash flow will be returned, combined with the fact that no capital returns are likely to occur over the next couple of years, locking in some profits after the stock has already more than doubled since the dividend cut sounds like a reasonable decision.

At the end of the day, even a 10% yield may not be that attractive, given that GEO's overall growth opportunities will remain quite limited and further challenges may arise in the future. In that respect, GEO's risk/reward ratio is no longer as attractive as it was when the shares were trading below $10, and shares don't offer the same deep-value opportunity in 2023 as they once did.

For further details see:

Behind Bars, But Ahead On Returns? Assessing GEO Group's Prospects Into 2023