BELFB - Bel Fuse: Great Long-Term Potential Inexpensive Valuation But Beware Of The China Risk

2023-10-03 05:34:32 ET

Summary

- Bel Fuse is massively undervalued relative to its peers on an EV/EBIT basis, despite being a high-quality company.

- The company is focused on growth industries such as electrification, 5G, AI, and EV plus infrastructure.

- Bel Fuse has a strong balance sheet with low debt and high interest coverage, which protects the downside and leaves plenty of upside potential.

Thesis

Seeking Alpha

Since my last article on Bel Fuse (BELFB), which you can read here , the company has significantly outperformed the S&P 500. The stock is still undervalued on an EV/EBIT basis, but they have improved margins this year even though sales have suffered a bit. As they have deleveraged, they have also improved their risk/reward ratio tremendously. Therefore, the odds of beating the S&P 500 over the next 5 years are relatively high, and even a 15% annual return is not out of reach. Today, a potential multiple expansion is the strongest factor driving this potential outcome, combined with a moderate revenue growth rate.

Company Profile Of Bel Fuse

{kind=link}

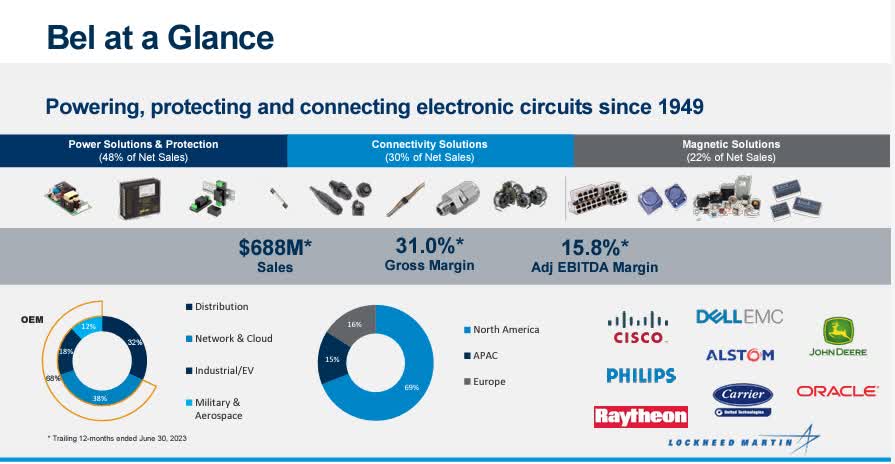

In this presentation from last month , the figures are slightly different than in the last earnings release as these are TTM figures. But it is clear that they have focused on the connectivity and power solutions segments, where the margins are currently better. Bel Fuse also sees the biggest growth opportunities in electrification, 5G, AI and EV plus infrastructure. So that's generally where they're going to shift their focus. These are all growth industries, so the TAM should be huge and growing.

Thanks to the improved margins, the Net Income is growing steadily. Should sales grow faster again in 2024, $100 million in Net Income is within the realm of possibility. The backlog is definitely there. But it will be important to serve it, but it looks like there are some problems for Bel Fuse to do that right now.

Investor Presentation Jefferies

In the disliked Magnetics category, they were able to reduce the backlog significantly, but Power and Connectivity are still relatively high. Therefore, it will be interesting to see if Q3 and Q4 will lead to a strong reduction in the backlog, as these are typically two strong quarters for Bel Fuse. External factors have certainly played a role, but within the next year they should try to get back to 2020 level. This is one of the biggest criticisms many investors have of Bel Fuse, but if it is only temporary, this would be a great opportunity for long term investors.

BELFB Balance Sheet

With only $60 million in debt and $65 million in cash and cash equivalents, liquidity is assured. Net income TTM is also $72 million and therefore higher than debt. For me personally, a Debt/Net Income < 4x is a sign of a healthy balance sheet and Bel Fuse's ratio is much better. $65m / $72m = 0.9x

The interest coverage of the S&P 500 is usually 10x, therefore Bel Fuse's 23x is very safe.

With trailing 12m sales of $688m and an FCF yield of 9% to 10%, annual FCF could be $61m to $68m, which is more than the outstanding debt, making the balance sheet even safer and hedging the downside. With a 5-year average FCF yield of only 2.93% , Bel Fuse has grown rapidly and may consider returning cash to shareholders in the future if it does not find attractive opportunities to deploy capital elsewhere. I think the risk/reward is attractive because the upside for Bel Fuse is quite high and the downside is protected by the strong balance sheet.

BELFA Capital Allocation

According to Michael Mauboussin's ROIC studies, companies that start with a low ROIC and achieve strong growth are among the best investments. And Bel Fuse has made such a development, which has also been reflected in the share price, as shareholders have received an incredible return over the last 2 years. Because they have little debt and little interest to pay, they have a low WACC, which makes for a wide ROIC-WACC spread. If they can maintain that, it would be very attractive for shareholders. The wider the spread, the better the stock tends to perform over the long term.

They are currently using much of their cash flow to invest in growth and R&D and are also looking for M&A targets. The magnetics facility in China is expected to be completed before the end of the year and should provide a boost to this segment and its earnings. This is likely to be felt in Q1 or Q2 2024.

The end of the shortage of ICs and power supplies should also have a positive impact on the next quarter or the fourth quarter .

Valuation Of Bel Fuse

Due to its broad portfolio, Bel Fuse has a large number of competitors and most of them are much larger or more suitable competitors are private. Therefore, a comparison with other companies is not so easy, but with an EV / EBIT of about 6.8x, it should be clear that the company is not expensive. Even for an unknown small cap, an EV / EBIT of around 10x to 12x should be more than reasonable, especially considering their ability to generate FCF and their rock-solid balance sheet.

They always look undervalued relative to their peers, and in some cases have the potential to double or triple their multiple to get to the same level.

Multiple expansions combined with earnings growth could therefore lead to strong returns for shareholders. A powerful combination. And when rising dividends are added to the mix, shareholders could see their total return improve dramatically. With enough FCF available, the question now is whether management will show that it wants to return cash to shareholders.

{kind=link}

- Diluted EPS TTM: $5.76

- Discount Rate: 10%

- Exit Multiple: 10x

To justify the current share price and achieve a 10% CAGR over the next 10 years, diluted EPS must grow 9% annually. Over the last 10 years, BELFB has achieved a CAGR of about 12%, so the reverse DCF also shows that the shares are undervalued. Potential future share repurchases would also significantly increase EPS growth when Bel Fuse considers them in a few years when they are a more mature company. The potential to exceed the required 9% CAGR is certainly there, given the strong FCF.

Risks

One risk I highlighted in my last article is that while the company is headquartered in the U.S., more than 60% of the employees are in China, and the combination of the magnetics division in China makes the exposure to China even greater. It will be interesting to read the next 10k and see how many employees and manufacturing capabilities are in China. I think that is something that a lot of people are not aware of because it adds a political risk.

In addition, I am not sure that Bel Fuse has enough pricing power and competitive advantage. Larger companies in their industry should have the same level of expertise and better distribution channels, but Bel Fuse could be a good fit for some larger companies.

Conclusion

Bel Fuse has had a strong year so far, deleveraging the balance sheet, improving margins and showing strong growth in return on capital. In addition, the shares are trading at a level that is too cheap in my opinion. But the China risks and the continuing sales declines are a bit worrying. Q3 sales guidance is below Q2 and Q1, but management is confident that there are enough growth drivers to get them back on track in 2024. If they are able to turn the sales growth engine back on in 2024, the current share price would be a bargain.

Even with moderate sales growth, Bel Fuse has the opportunity to be an investment that rewards shareholders with an annual return of 15%+ over the next 5 years due to its low starting valuation. Eventually, the market will realize that the multiple is too low. Using the reverse DCF as a guide, the stock is undervalued if you are looking for a 10% annual return, so a little multiple expansion would put it in the 15% annual return range.

Without the China risks, the company would most likely trade at a much higher multiple, so this is the thing that I do not like at the moment because it introduces a risk that is very unpredictable. I think revenues should start growing again in 2024, so I think this risk is only temporary.

For further details see:

Bel Fuse: Great Long-Term Potential, Inexpensive Valuation, But Beware Of The China Risk