BELFB - Bel Fuse Inc.: Possible Investment With A High Return And Some Risk

Summary

- It looks undervalued on an EV/EBIT and FCF yield basis.

- But it looks much more fairly valued if you look at what is priced into the share price.

- Only time will tell whether they can maintain their return on capital and grow sales.

Thesis

Bel Fuse Inc. (BELFB) is a small, undervalued stock that has performed really well over the past year. It has returned more than 100%, while the S&P 500 has lost double digits over the same period. The big question now is whether everything is priced in, or is this stock still undervalued? In my opinion, this stock is fairly valued at the moment, but it still has room to grow. This is because we have a positive outlook based on improvements in margins and returns on capital, but most of this is already priced into the share price.

Short Introduction

Bel Fuse designs, manufactures and markets products for powering, protecting and collecting electronic circuits. The company is headquartered in New Jersey, but most of its manufacturing capacity is located in the People's Republic of China. 62% of its employees, 73% of its manufacturing facilities and 26% of its property, plant and equipment are located in the PRC.

There are currently 2 different shares in circulation. BELFA with voting rights and BELFB which is non-voting. As a result, BELFB has a slightly higher dividend payment.

{kind=link}

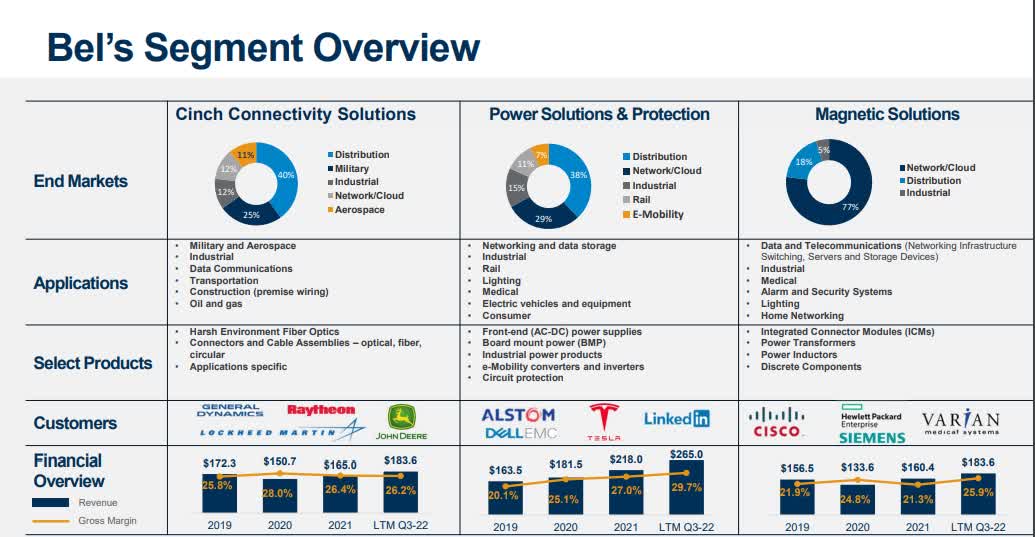

Bel Fuse has the following three business segments: Cinch Connectivity Solutions, Power Solutions & Protection and Magnetic Solutions. Power Solutions, which includes the high-demand e-mobility business, is the fastest-growing division with the best margins. The other two are almost flat or growing slowly.

Analysis

{kind=link}

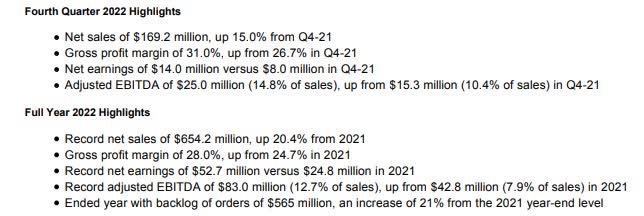

2022 was a record-breaking year. Net sales increased by 20% and gross profit margins improved by 330 points. Part of the margin improvement was due to favourable movements in the exchange rate of the Chinese Renminbi . Higher demand in commercial aerospace and e-mobility contributed in 2022 and will also have an impact in 2023. The $20 million in e-mobility sales has the potential to double again this year.

Financials

{kind=link}

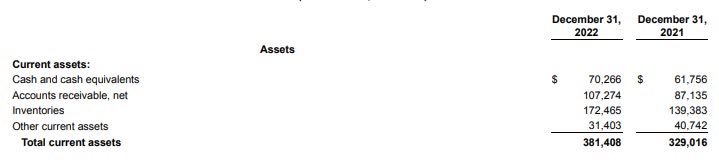

The increase in cash compared to the end of 2021 was a positive improvement. But you have to look at the increase in inventories and see if they can be reduced or if they will increase further in 2023.

Q4 Investor Presentation

A very good improvement is the net leverage, which has fallen dramatically. Although acquisitions are an important part of their growth strategy, they have managed to fund them with cash and still increase their cash holdings. In addition, they paid $3.4 million in dividends. They really strengthened their financial position in 2022.

EBIT in 2022 is $59.059m, which compares to an EV of $472.67m, implying an EBIT multiple of ~8. This is an attractive price in the current market. If we take a look at the FCF Yield, we get a result of 6.66%. CF Op: $40.3m - CapEx $8.8m = $31.5m FCF / $472.67m EV. This is also very attractive relative to the FCF yield of the S&P 500, which is 2.80%.

{kind=link}

The number of shares outstanding is also growing slowly, but I do not think it is a big dilution for shareholders at the moment. But as always, we have to look at future developments. Buying back shares at the right price is always a nice way of rewarding shareholders. If they could do that in the future, it would really help shareholders. Stock cannibals are among the best investments in the long term.

With a P/E of 8.62, there is also some room for multiple expansion, as some of the peers have slightly higher P/E ratios.

Management

{kind=link}

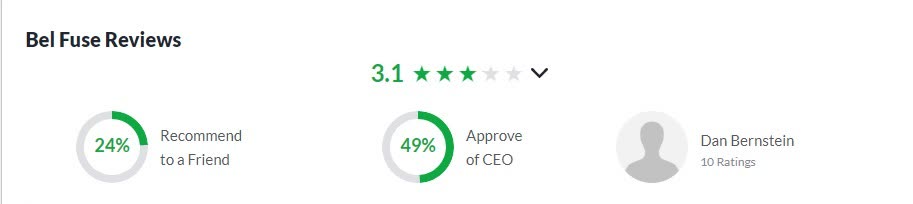

Management ratings on Glassdoor are not very good. But there are only 19 reviews so far and the CEO has only 10 ratings. So the sample size is quite small. Also, they have hired new people for some important roles in the company in recent years, and I think you should give them time to show how they can manage their positions.

Reverse DCF

{kind=link}

I like to do a reverse DCF to see what is priced into the share price. Assuming a 9x P/E and a 10% discount rate, I get the result that EPS has to grow 10% per year to justify this share price. Looking at the historical EPS growth rate, it has risen from $1.39 in 2013 to $4.24 in 2022. This is a CAGR of ~12%. Slightly higher than projected growth. However, if we apply a discount to the future growth rate because the future is uncertain, and we don't know if they can achieve a 12% CAGR again, the stock looks fairly valued.

Return on Capital

Author

The return on capital over the last 5 years does not look very good. It is only in the low double digits. For me, a threshold for investments is a ROC above 20% over 5 years, so you know they can invest effectively to create value. Last year looks promising, but I want to wait and see if they can maintain that return.

Risks

As stated in the Short Introduction section. Bel Fuel is really dependent on its Chinese operations. What reinforces this is the fact that they have to pay salaries, labour + overheads in Renminbi. And when almost 70% of your business is in China, this is a risk you need to address. Furthermore, 1 customer alone accounted for ~10% of 2021 revenue.

Conclusion

As usual with these small, undervalued stocks, you get a good price for what you get. But as always in life, nothing comes for free, so there is usually some risk involved with these small stocks. A customer that accounts for 10% of net sales and almost 70% of the company in China is a risk that many people are not prepared to take. These things lead me to conclude that Bel Fuel is fairly valued when you take them into account. Nevertheless, small-cap stocks with the opportunity to improve ROC and the chance for multiple expansions are still a good candidate for impressive returns. Bel Fuel has all the conditions to achieve this.

For further details see:

Bel Fuse Inc.: Possible Investment With A High Return And Some Risk