BELFB - Bel Fuse Stock: Growth Potential Is Still There

2023-06-16 09:27:47 ET

Summary

- Bel Fuse is a $730-million market cap firm that offers magnetic, power, and connectivity solutions for various applications.

- Q1 sales for Bel Fuse were $172 million, showing a substantial increase of 26% compared to the first quarter of 2022. Also, the gross margins improved dramatically YoY.

- The management expects an even higher consolidated margin profile due to the shift in product mix and profitability in the next quarters.

- Today's valuation of Bel Fuse allows the stock to continue its recent rally, albeit at a less vigorous pace than lately.

- I rate BELFB and BELFA a "Buy" this time and see an upside potential of at least another 17% by year-end.

The Company

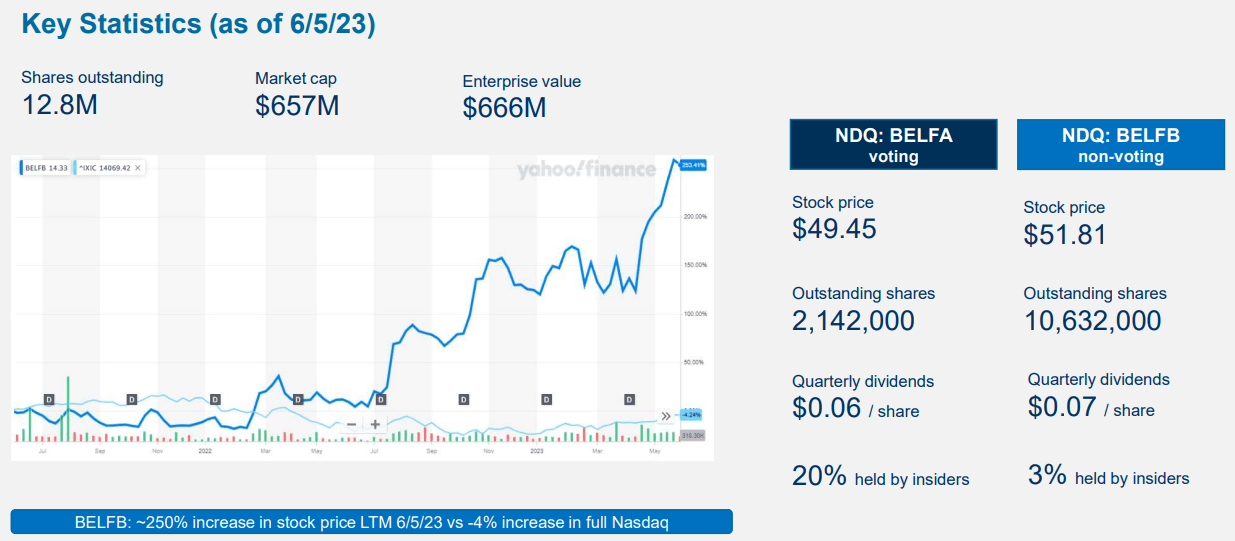

Bel Fuse Inc. ( BELFA ) ( BELFB ) is a $730-million market cap firm that designs, manufactures, and markets a wide range of products that are used in various industries, including networking, telecommunications, computing, industrial, data transmission, military, aerospace, transportation, eMobility, automotive, medical, broadcasting, and consumer electronics.

{kind=link}

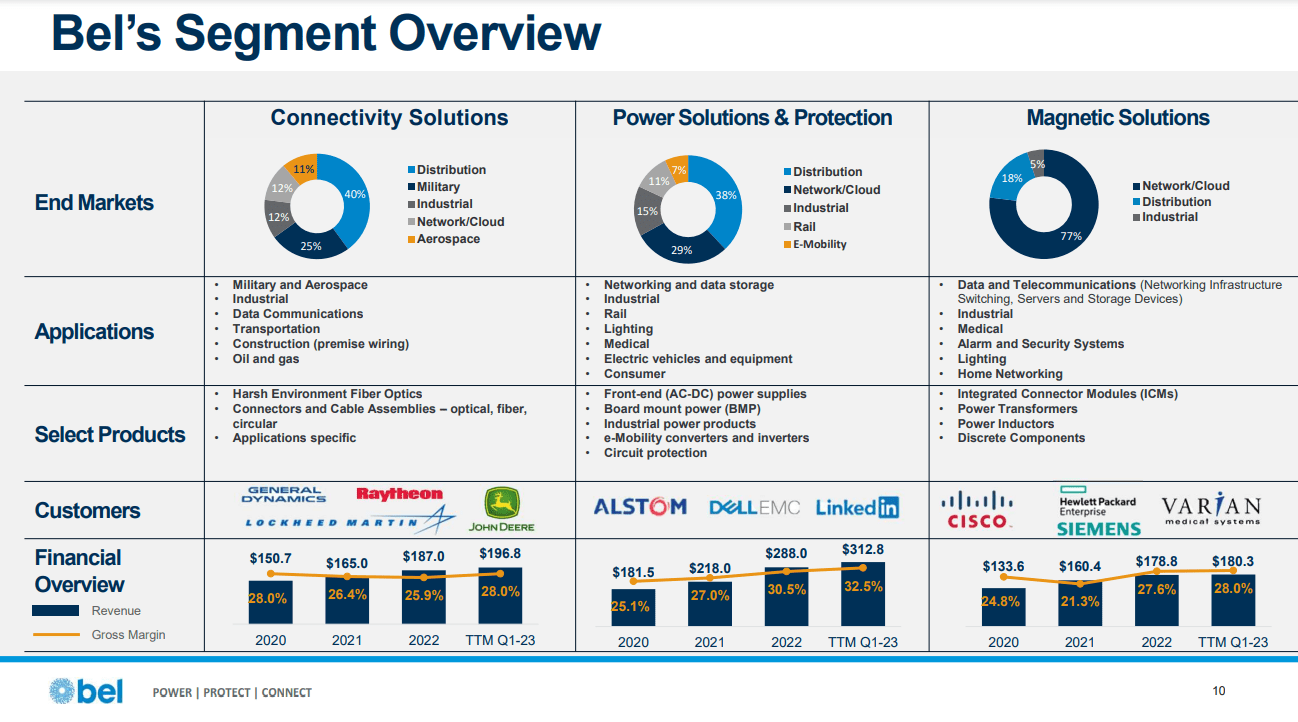

According to the most recent IR presentation , they operate through 3 product group segments: Power Solutions and Protection [45% of total sales], Connectivity Solutions [30%], and Magnetic Solutions [25%], with the majority of the whole sales volume coming from North America [67%]:

{kind=link}

Labor costs, materials, and overhead expenses drive the company's operating expenses. They manufacture their products in multiple facilities located in different countries.

Q1 sales for Bel Fuse were $172 million, showing a substantial increase of 26% compared to the first quarter of 2022 [source: the most recent 10-Q ]. The Power Solutions and Protection segment recorded sales of $83.2 million, marking a significant 41% increase from the previous year's first quarter. This growth was primarily driven by high demand for front-end, board-mounted power products, and e-mobility products, according to the management's words during the earnings call . The gross margin for this segment was 35.7%, a substantial improvement of 860 basis points compared to Q1 '22.

The Connectivity Solutions segment achieved sales of $53.4 million, indicating a 22% YoY increase that was attributed to the recovery of the commercial aerospace and military end markets. The gross margin for the Connectivity Solutions group improved to 34.1% in Q1 2023, up from 26.5% in Q1 2022.

The Magnetic Solutions segment reported Q1 sales of $35.8 million, reflecting a 4.5% YoY increase. The gross margin for this segment improved to 22.8% in Q1 2023, benefiting from higher sales volume and a favorable shift in the exchange rate of the Chinese renminbi.

{kind=link}

The backlog of orders for Power Solutions and Protection stood at $322 million, while the backlog for Connectivity Solutions was $116 million as of March 31. So the overall backlog decreased by 12% QoQ, but it was intentional as component availability improved and lead times began to normalize.

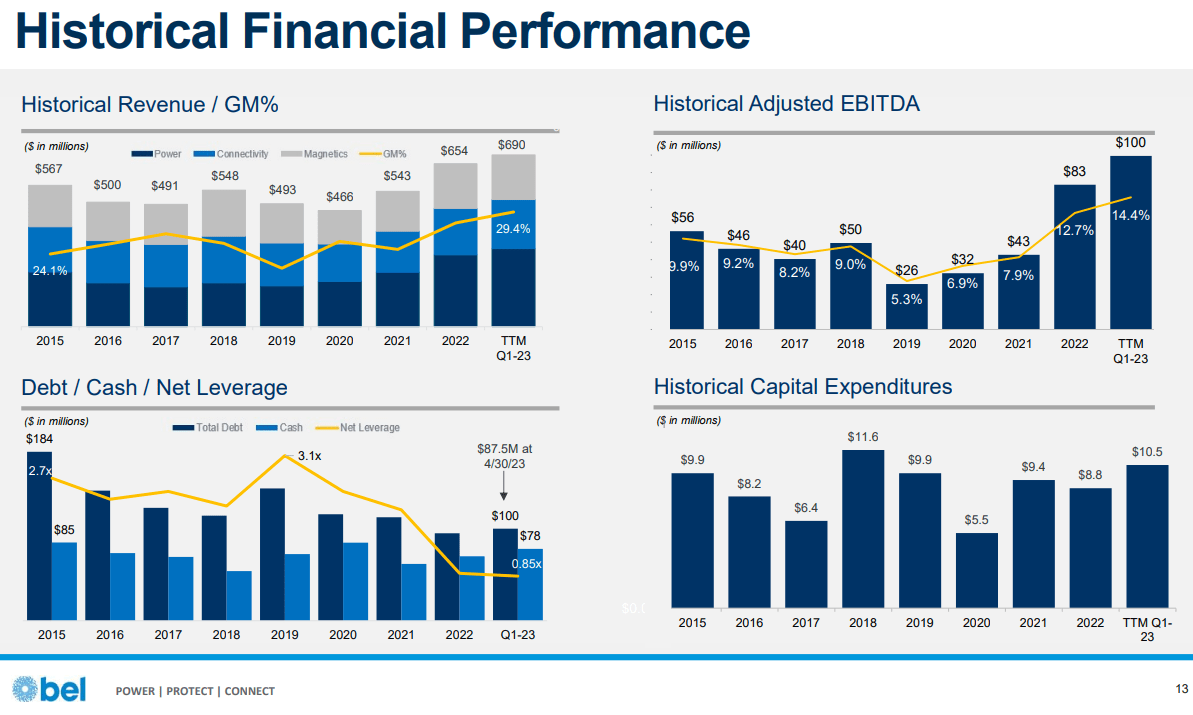

Despite the restructuring costs of $3.5 million that were incurred in Q1 2023 [primarily related to the factory consolidation initiative in China], Bel Fuse showed an increase in EBIT in Q1 FY2023 by ~143% YoY primarily because of a stronger gross margin. As a result, net income went up by ~189% YoY, but it impacted the EPS a bit differently since Bel Fuse has a dual-class stock structure.

{kind=link}

{kind=link}

Bel Fuse generated $16.8 million in cash flow from operating [CFO] activities during the first quarter, resulting in a free cash flow of $13.1 million. So the firm's cash balance increased to $77.8 million - that's over 10% of the total market cap. And it gives a net leverage of less than 1x - Bel Fuse looks quite stable where it stands, with record top-line growth and EBITDA generation capacity:

{kind=link}

Farouq Tuweiq, CFO of Bel Fuse, expressed optimism [during the earnings call] and mentioned that Q1 was an expectation-surpassing quarter for the company. Tuweiq also highlighted the strength and resiliency in certain end markets, including commercial air, military, and e-mobility. The management expects a higher consolidated margin profile due to the shift in product mix and profitability in these markets .

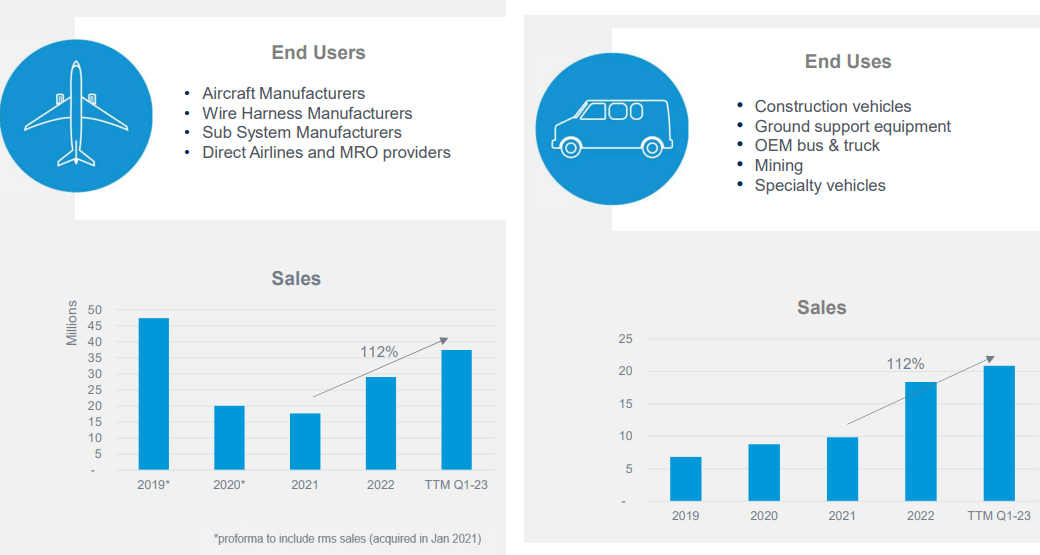

Management sees the main growth markets in the aerospace and EMobility end markets - after the coronavirus, sales in these markets are really recovering very quickly:

{kind=link}

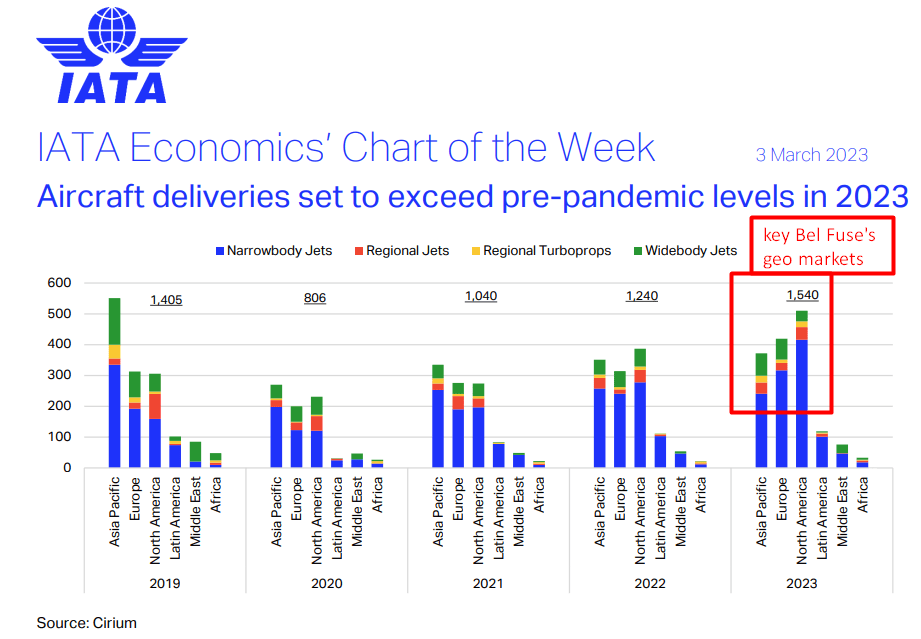

I looked at third-party research reports to review the future performance predictions of these end markets. Fortune Business Insights notes that the global market for electric mobility will grow from $279.45 billion in 2021 to $1,507.21 billion in 2028 at a CAGR of 27.2% [7 years]. In my opinion, that's quite a lot. Emergen Research, another independent research house, sees the same CAGR of 27.2%, but through 2032.

In aerospace, growth will be much more modest. The Precision Business Insight analyst sees this market growing at a CAGR of 8.6% over the forecast period 2022-28, while her colleague at Acumen Research and Consulting forecasts a CAGR of 8.8% for the aerospace composites market size [through 2030]. In any case, it's important to realize that the aerospace recovery is most likely not yet complete [post-COVID], so the leverage for Bel Fuse's addressable market growth may be much more positive than it may appear at first glance when looking only at CAGRs.

{kind=link}

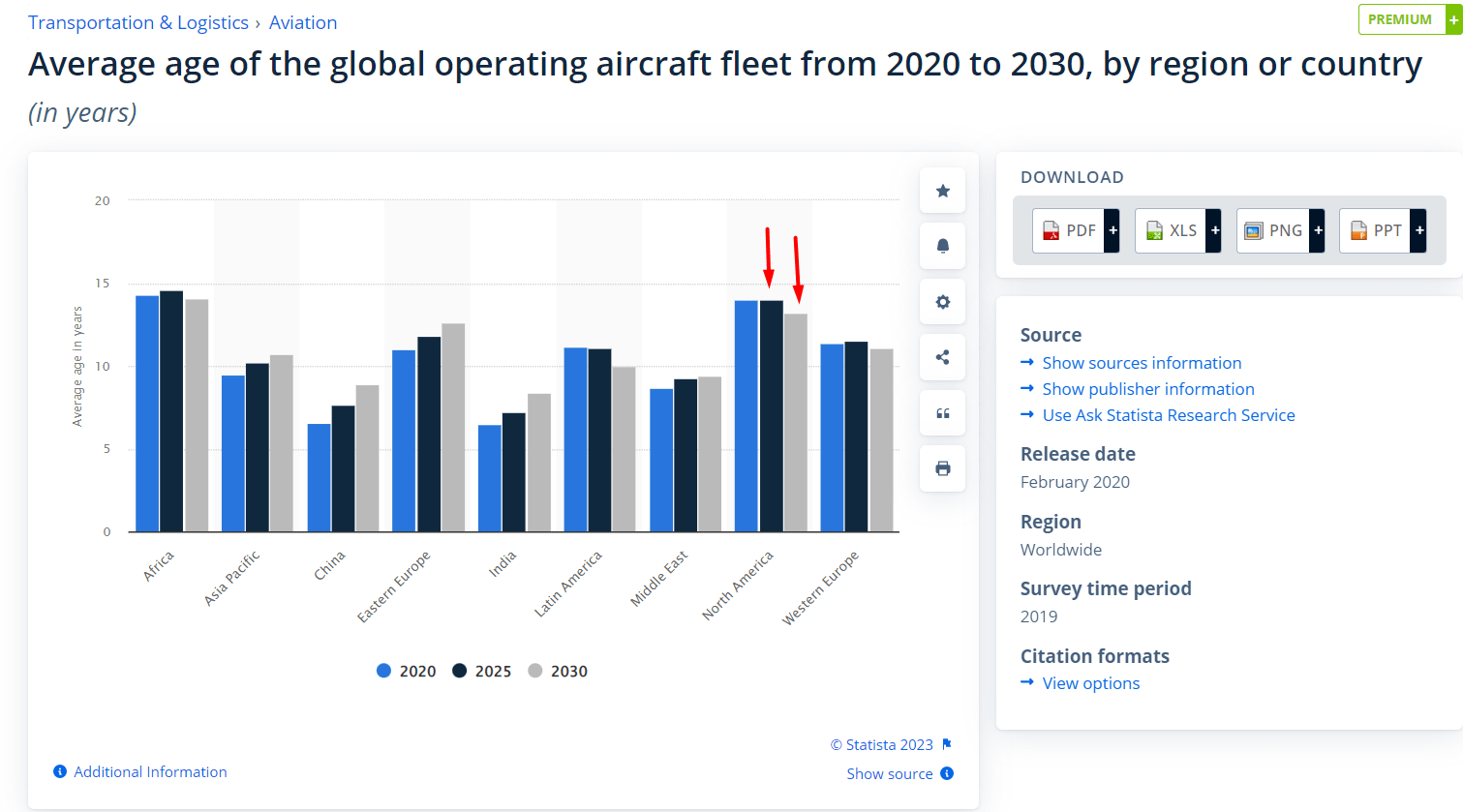

In addition, the average age of aircraft in Bel Fuse's most important market - the U.S. - is now about the same as in Africa. I think that opens up opportunities for additional growth - maintaining old planes requires a large number of new components that the company manufactures. And judging by the pricing power Bel Fuse demonstrated in Q1 FY2023, end customers may be willing to continue paying a good price for specifically Bel's components.

{kind=link}

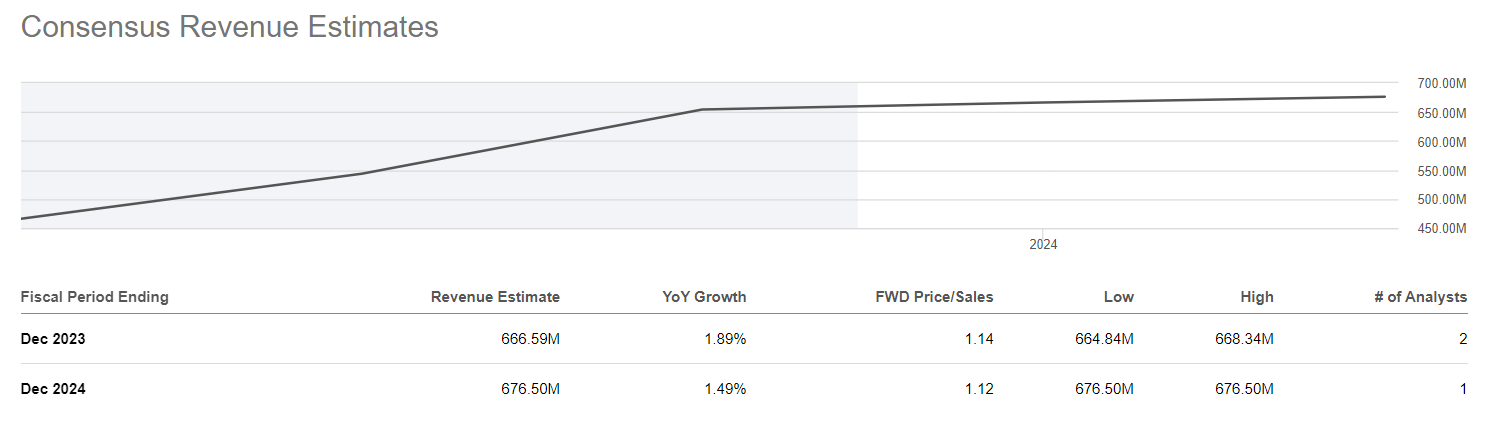

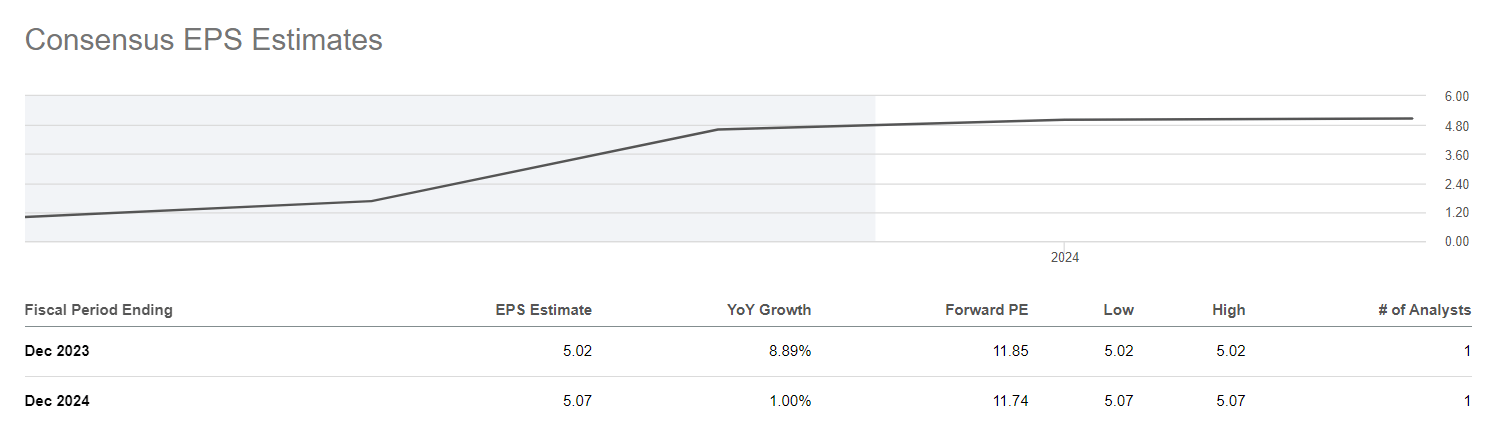

Anyway, Bel Fuse has a positive outlook for Q2 2023, with sales projected to be in the range of $162 million to $170 million. The consensus revenue estimate aligns with the analysis. However, for FY2024, one analyst, whose estimate is included in the consensus, projects a modest YoY revenue growth of +1.49% and an even lower growth rate of +1% for EPS.

{kind=link}

{kind=link}

I doubt very much that Bel Fuse will have as weak growth next year as it's now expected to have. Last quarter, the company beat the EPS consensus by 63.2%, while it has never shown a negative earnings surprise in the last 2 years . As the stock's visibility increases, I think Bel Fuse will either continue to beat consensus data as low as it's now, or attract more outside opinions and start pricing in more plausible and numerous expectations. Either option, I believe, should be accompanied by an increase in the company's capitalization.

Valuation Allows Bel's Rally to Keep Going

As I wrote above, the company still has more than 10% of its capitalization in cash on the balance sheet - that's still a lot, in my opinion, and provides some margin of safety.

Bel Fuse is among the electronic components industry within the IT sector , which currently has a median EV/EBITDA [FWD] multiple of 14.7x , according to Seeking Alpha Premium. Bel's EV/EBITDA for the next year is 8.5x, 42% below the median and about the company's historical average value:

Given the margin improvement in Q1 FY23, I estimate that Bel Fuse's EV/EBITDA multiple should be ~10x by year-end, which I think is pretty conservative. Then we should get a fair estimate of about $850 or an upside of ~17% on the latest close price. And that's even though I'm comparing today to forward EV / EBITDA based on consensus data that is too low, in my opinion. Given this, I conclude that today's valuation of Bel Fuse allows the stock to continue its recent rally, albeit at a less vigorous pace than lately.

The Bottom Line

Of course, some risks with Bel Fuse cannot be ignored. First, the company is low capitalized [< $1 billion market cap], which affects its volatility. Second, the company has two classes of stock, which complicates its capital structure. Incidentally, given the choice between BELFA and BELFB, I'd go for the non-voting shares [the latter] as they're more liquid. The third risk is the reduction in order backlog in Q1. Management said this was pre-planned, but who knows - if the backlog continues to decline, the 1-2% FY24 revenue growth and earnings per share forecasts may turn out to be true. In that case, the growth potential will be minimal.

However, despite the risks and doubts, I rate BELFB and BELFA a "Buy" this time and see an upside potential of at least another 17% by year-end .

Thanks for reading!

For further details see:

Bel Fuse Stock: Growth Potential Is Still There