LFUS - Belden Q4 2022 Earnings: Robust Results Justify A Further Upside

Summary

- Belden Inc. has done exceptionally recently, with earnings and revenue data from the most recent quarter showing that the company is doing better than expected.

- Over the past several months, the firm has already outperformed the broader market significantly, but BDC shares are still affordable.

- More likely than not, the company has additional upside from here.

Shares of Belden Inc (BDC), an enterprise focused on providing network infrastructure and broadband solutions, cabling and connectivity solutions, machine connectivity products, and more, roared higher on February 8th, closing up 7.4%. This move higher came in response to robust financial performance achieved by the company and overall favorable guidance when it comes to the 2023 fiscal year. Even though shares of the company have already been up significantly over the past several months, these developments suggest that some additional upside could be warranted. Clearly, the easy money has already been made by this point. But absent some deterioration of its fundamental condition, I do believe that it still warrants a 'buy' rating at this time.

Great results from Belden

In the past, I have written two articles discussing the investment worthiness of Belden. The most recent of these was published in November of last year. And in that article, I acknowledged that the company had done well over the prior few months in growing both its revenue and profits. That, combined with how shares were priced and with how optimistic management was about the near-term outlook for the company, led me to reiterate the 'buy' rating I had on the stock. Since then, shares have more than doubled the market return, posting upside for investors of 9.7% at a time when the S&P 500 was up only 4.1%. For context, since I initially wrote about the company in May of 2022, shares are up a whopping 60.6% compared to the 3.2% increase the S&P 500 saw.

{kind=link}

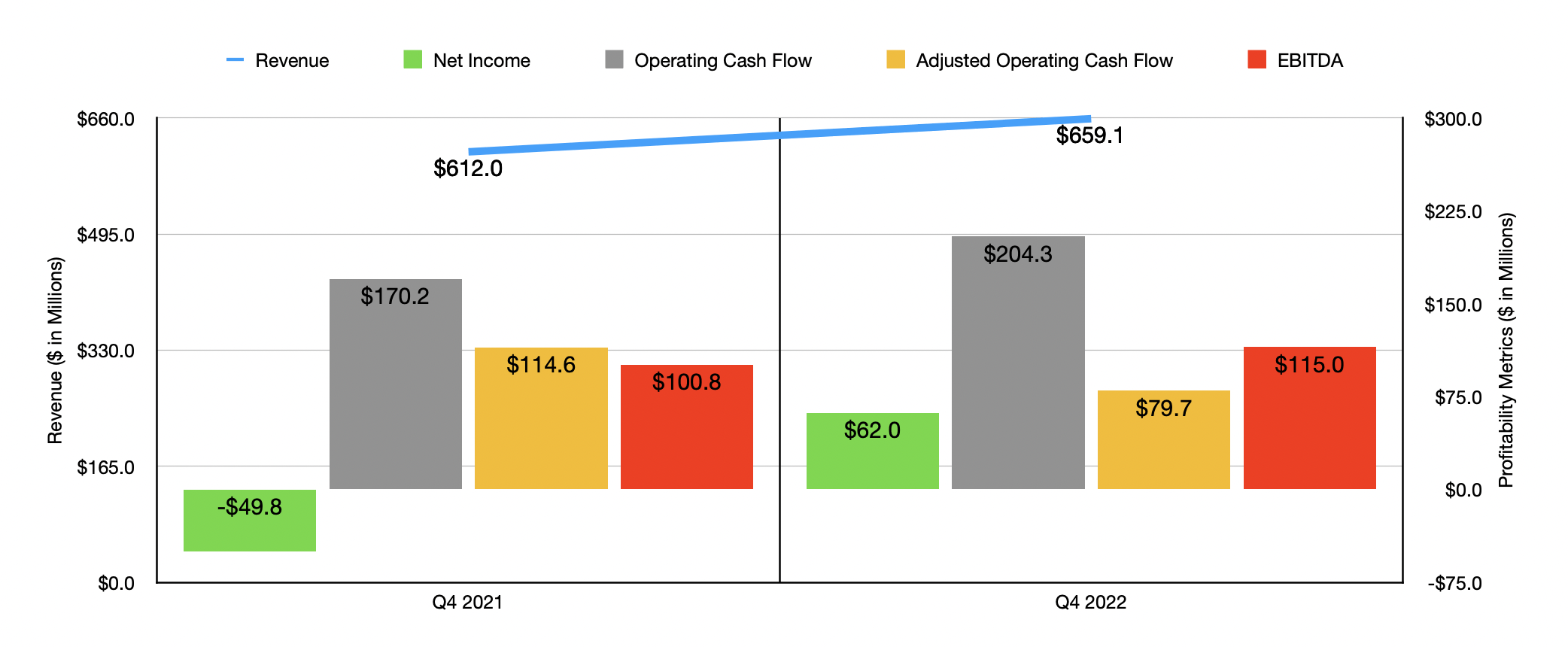

The most recent move higher for the company, a 7.4% rise on February 8th, was driven by robust financial performance reported by management covering the final quarter of the company's 2022 fiscal year . According to management, sales came in at $659.1 million. Not only did this represent a sizable improvement over the $612 million reported one year earlier, it also beat the expectations set by analysts to the tune of $14.8 million. The 8% increase year over year was driven by a 12% rise in organic growth. The Industrial Automation Solutions portion of the company reported an 18% rise in revenue, while Enterprise Solutions saw sales grow by 6%.

This rise in revenue brought with it improved profitability. Net income for the quarter came in at $62 million. That compares favorably to the $49.8 million loss experienced one year earlier. The actual non-GAAP earnings per share for the company came in at $1.75. That topped the expectations set by analysts to the tune of $0.09. Other profitability metrics followed the company hires well. Operating cash flow, for instance, expanded from $170.2 million to $204.3 million. On an adjusted basis, however, the metric would have fallen from $114.6 million to $79.7 million. Though disappointing, EBITDA worked to offset that, climbing from $100.8 million in the final quarter of 2021 to $115 million the same time this year.

{kind=link}

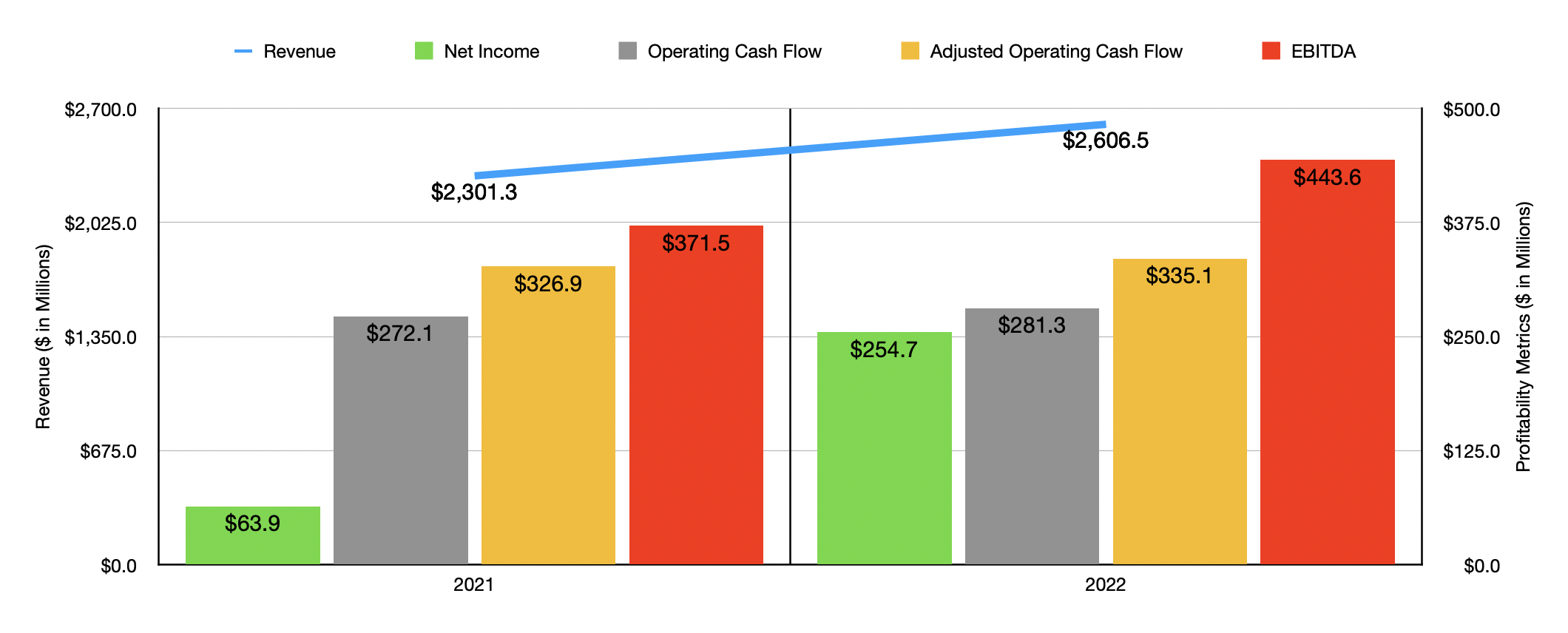

For 2022 in its entirety, sales for the company totaled $2.61 billion. That represents a year-over-year increase of 13.3%, driven by strong organic growth. Just as was the case with the final quarter of the year, profits followed sales higher. Net income of $254.7 million dwarfed the $63.6 million reported one year earlier. Operating cash flow managed to rise from $272.1 million to $281.3 million. And unlike in the third quarter on its own, operating cash flow increased, rising from $272.1 million to $281.3 million. Even on an adjusted basis, the metric rose from $326.9 million to $335.1 million. And finally, we have EBITDA, which jumped from $371.5 million in the 2021 fiscal year to $443.6 million the same time of the firm's 2022 fiscal year.

In addition to reporting robust financials, both for the final quarter of the year and the 2022 fiscal year as a whole, management also revealed guidance for 2023. Revenue, they said, should come in at between $2.67 billion and $2.72 billion. This compares against the $2.61 billion reported one year earlier and will be driven in large part by an increase in organic growth of between 3% and 5%. The company also said that earnings per share should be between $5.73 and $6.13, with the adjusted figure for this being between $6.60 and $7. Using the midpoint for the adjusted figure, this would translate to net income for the business of $297.2 million. If we assume that other profitability metrics will grow at the same rate that adjusted earnings should, then we should anticipate adjusted operating cash flow for 2023 of $349 million and EBITDA of roughly $461.9 million.

{kind=link}

*Price / Earnings Ratio Utilizes Adjusted Net Income

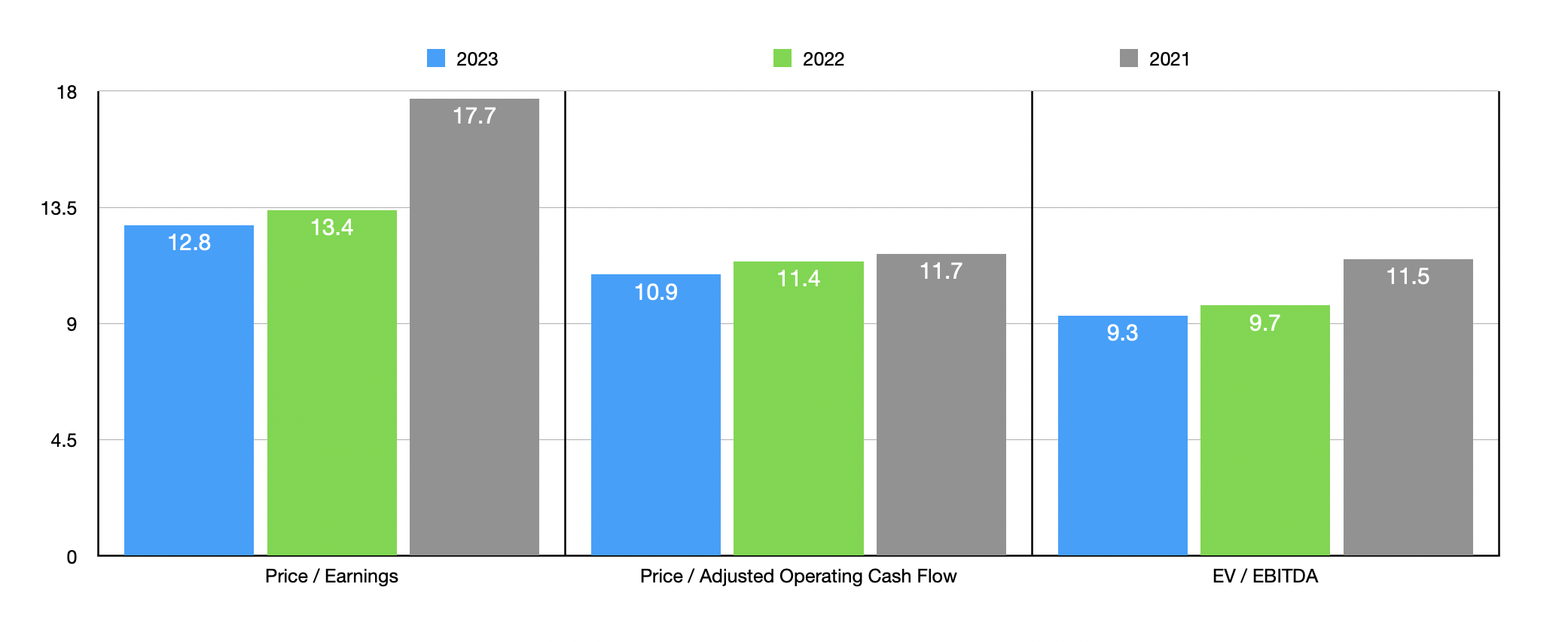

Based on these figures, shares of Belden are trading at a forward price-to-earnings multiple of 12.8. The forward price to adjusted operating cash flow multiple should be 10.9, while the EV to EBITDA multiple should total 9.3. By comparison, using the data from 2022, these multiples should be more expensive but still quite low, trading at 13.4, 11.4, and 9.7, respectively. And if we were to use the data from 2021, these multiples would be 17.7, 11.7, and 11.5, respectively. As part of my analysis, I also compared Belden to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 7.8 to a high of 26.6. Using the EV to EBITDA approach, the range was from 3.9 to 17.3. In both of these cases, three of the five firms were cheaper than our prospect. Meanwhile, using the price to operating cash flow approach, the range was from 6.6 to 23.2. In this case, only one of the five companies was cheaper than Belden.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Belden Inc. |

| 13.4 |

| 11.4 |

| 9.7 |

| Vishay Intertechnology ( VSH ) |

| 7.8 |

| 6.6 |

| 3.9 |

| Knowles Corporation ( KN ) |

| 10.6 |

| 16.7 |

| 8.8 |

| Bel Fuse ( BELFA ) |

| 11.4 |

| 17.3 |

| 7.9 |

| Littelfuse ( LFUS ) |

| 18.1 |

| 16.1 |

| 12.5 |

| Amphenol Corporation ( APH ) |

| 26.6 |

| 23.2 |

| 17.3 |

Takeaway

According to all the data at my disposal, it's clear that Belden is showing solid signs of a recovery. Revenue, profits, and cash flow metrics continue to show signs of strength. Management expects this kind of trend to continue through at least 2023. Add in how attractively braced shares are, both on an absolute basis and relative to similar firms, and I would make the case that some additional upside is likely warranted from here. As such, I've decided to keep the 'buy' rating I had on the stock previously.

For further details see:

Belden Q4 2022 Earnings: Robust Results Justify A Further Upside