BLTE - Belite Bio: The Pick Of The Post-IPO Biotechs - Is There Further Upside Ahead?

2023-08-22 15:51:40 ET

Summary

- Only a small percentage of recently listed biotech and healthcare companies have posted share price gains in the past year, highlighting the risk of investing in the sector.

- Belite Bio, however, a recently IPO'd company, has shown promising gains in its share price and has two Phase 3 studies underway for its lead candidate targeting eye diseases.

- Tinlarebant is an orally available therapy targeting Stargardt disease and Geographic Atrophy. The latter market could be worth over $10bn.

- Two injectable therapies have recently been approved in GA, but concerns around safety are already affecting sales of one.

- Belite's pivotal Stargardt data arrives this year - if positive, I'd expect the share price to do cartwheels, based on the approval shot and longer term approval shot in GA.

Investment Overview - Picking Post-IPO Biotech Gems Is Tricky (Without Due Diligence)

Across the pharmaceutical, biotech, and healthcare sectors, over the past 12 months only ~260 listed companies out of ~1,050 overall have posted share price gains. The average gain has been ~57%, however, a substantial figure, emphasising that the drug development industry probably offers more opportunity to buy a "double your money overnight" stock than any other.

The average 1-year loss of the ~800 other companies is ~-50% according to my research, however, emphasising the risk that biotech investing carries with it - felt especially keenly during a devastating bear market in 2022, following five years of exceptional gains for the sector.

The share prices of recently IPO'd biotech and healthcare companies have performed particularly badly - the average return of any company within these sectors that has been launched between six months and one year ago - ~20 companies - is approximately -28%. The average return of any company that listed less than three years ago is approximately -30%, my research suggests, with ~50 companies seeing their share prices move up since IPO, and ~220 moved down.

In this post I want to highlight one of the best-performing recently IPO'd companies - Belite Bio ( BLTE ) - whose shares currently trade at $31. When the company launched its IPO in April 2022, it raised ~$36m at $6 per share.

Belite stock had hit highs over $40 post-IPO, and traded above $30 in April 2022, before sinking to a low under $12 in June this year. The price has been gaining rapidly in recent weeks however and spiked - from $23 to $31 - after the company released some upbeat Q2 2023 earnings and updates from management.

Despite the gains, Belite's market cap valuation remains below $1bn. With two medium-term approval shots in play targeting the multi-billion dollar eye-disease markets, there may be a case to argue that the company is undervalued relative to the strength of its opportunity - particularly when compared to sector rivals.

On the other hand, with the market so quick to punish recently IPO'd biotechs following even the slightest misstep, the risk of share price losses if Belite's lead candidate does not succeed in its late-stage trials is high. In this post I'll attempt to break down the risk-reward profile in relation to Belite in more detail, and speculate about where the share price may track to in 12-18 months' time.

Belite's Two Phase 3 Studies Make A Medium-Term Case For A Commercial Product

Belite is currently conducting two Phase 3 studies of its lead candidate, LBS-008, or Tinlarebant, which it describes as follows in its Q2 2023 earnings press release :

Tinlarebant (LBS-008) is designed to be an oral, potent, once-daily retinol-binding protein 4 (RBP4) antagonist that decreases RBP4 levels in the blood and selectively lowers vitamin A (retinol) delivery to the eye without disrupting systemic retinol delivery to other tissues. Vitamin A is critical to normal vision but can accumulate as toxic byproducts leading to retinal cell death and vision loss diseases such as Stargardt disease ("STGD1") and Geographic Atrophy ("GA"), the advanced form of dry Age-Related Macular Degeneration ("dry AMD").

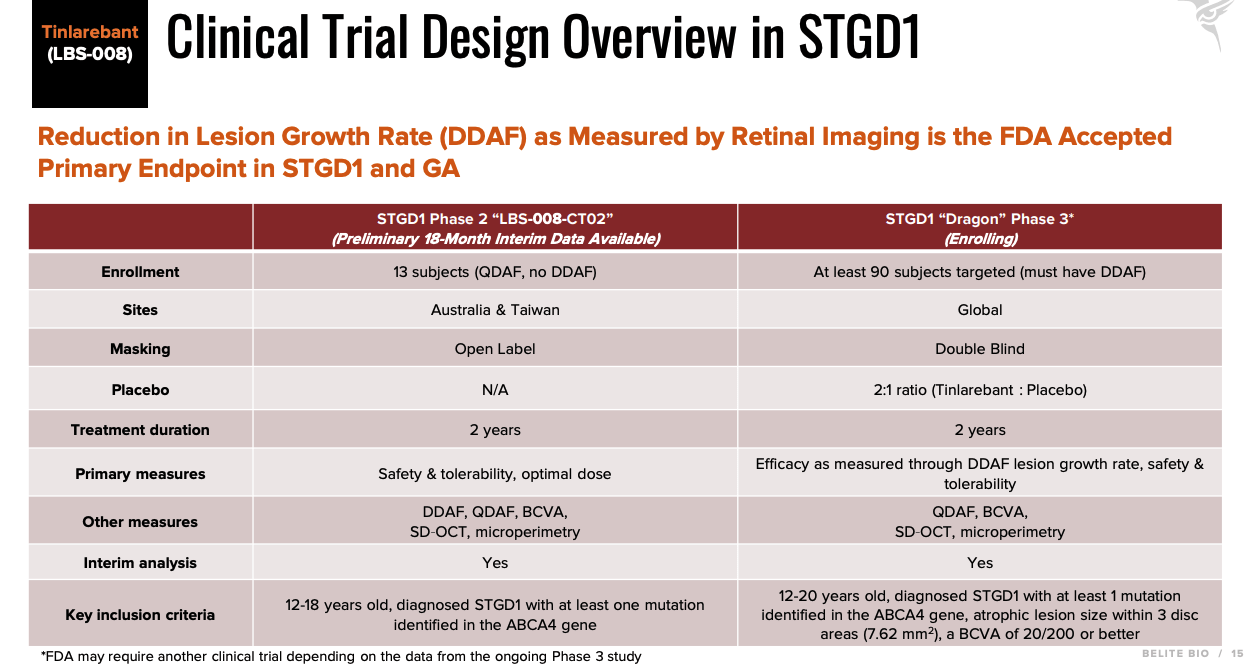

The two Phase 3 studies are DRAGON - a "2-year, randomized, double-masked, placebo-controlled, global, multi-center, pivotal Phase 3 trial in STGD1 subjects aged 12-20 years old", and PHOENIX - a "2-year prospective, randomized (2:1, active:placebo, n ~430), double-masked, placebo-controlled, global, multi-center, Phase 3 trial in subjects with GA".

The primary efficacy point in the fully-enrolled DRAGON study is slowing of lesion growth rate, and interim efficacy and safety data is expected by mid-2024. Interim analysis from the PHOENIX study, which has the same endpoint, and recently dosed its first patient, is expected at the midpoint of the study - likely in 2H24. Meanwhile, an ongoing Phase 2 study - LBS-008-CT02 - recently showed that:

- Nearly 60% of subjects (7 out of 12) had no incident atrophic retinal lesions as assessed by fundus autofluorescence ("FAF") imaging.

- Tinlarebant stabilized visual acuity with no significant loss and no clinically significant changes in retinal thickness.

And that:

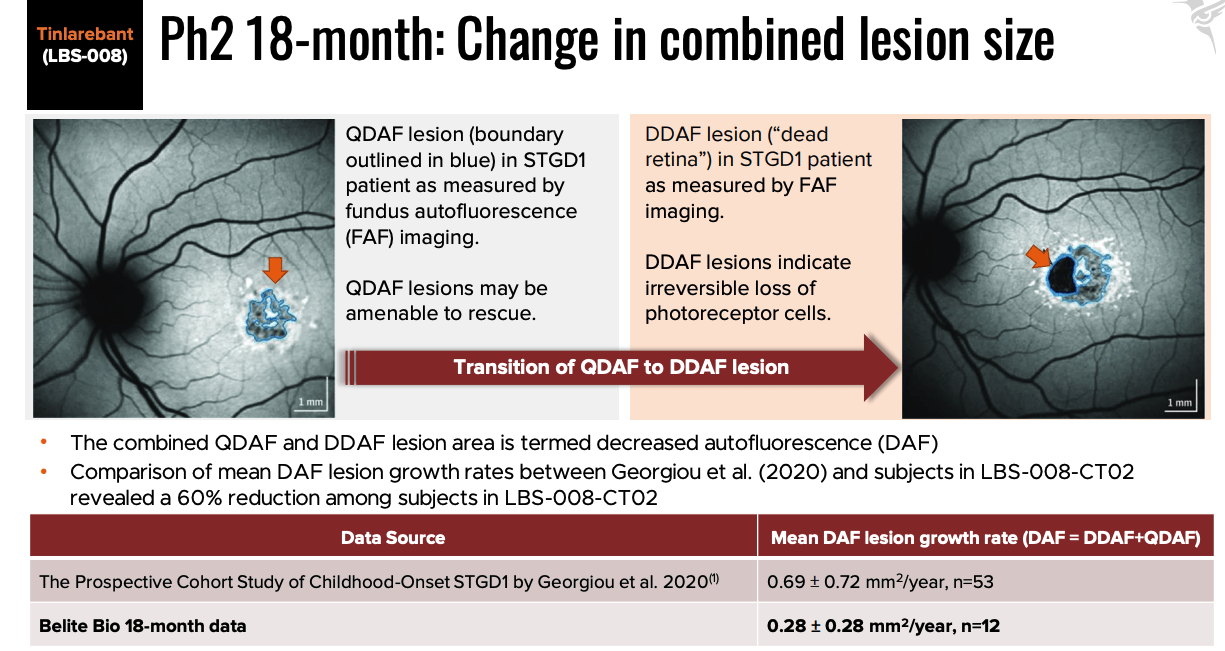

- When compared with ProgStar (historical) study participants ? 18 years old with only questionably decreased autofluorescence ("QDAF") lesions at baseline, subjects in LBS-008-CT02 treated for up to 18 months showed:

- Reduced expansion of DAF lesion size from baseline;

- Reduced expansion in definitely decreased autofluorescence ("DDAF") lesion size from baseline.

There are no currently FDA approved treatments for STGD1, and no orally available therapies available to treat GA.

Market Opportunity - Advantage Of A Non-Injectable Could Give Belite An Edge In Larger GA Market

STGD1 is an inherited juvenile form of macular degeneration - a disease which can cause loss of central vision - which affects ~30k people in the US, Belite estimates.

GA is a far larger market - according to Belite's 2022 20-F Submission (annual report), advanced macular degeneration - the intermediate and advanced stages of which often involve GA, symptoms of which include chronic progressive degeneration of the macula - affects:

... an estimated 20 million AMD patients in the United States and over 196 million patients worldwide with an estimated global direct healthcare cost of US$255 billion.

Interestingly, two other injectable drugs have recently been approved to treat GA. The first is Apellis Pharmaceuticals' ( APLS ) Syfovre, which was approved in February by the FDA. The drug was pegged by analysts for peak sales over $2.5bn, but shortly after launch the American Society of Retinal Specialists ("ASRS") flagged safety concerns relating to cases of occlusive retinal vasculitis detected in patients. Apellis' stock price was rocked by the news, dropping from ~$84, to a low of $24 last month, although the company still enjoys a market cap of $3.7bn. Syfovre generated $67.3m of revenues in Q2 2023.

Belite management believes the adverse safety events are a common side effect of injectable therapies, making the case for an orally available therapy like Tinlarebant even stronger. The company's Chief Scientific Officer ("CSO') Nathan Mata told analysts on the Q2 2023 earnings call :

So there's inflammation, there's all types of things that can happen when you puncture an eyeball with a needle, and you have to do it repeatedly, every other month or every third month, whatever it is, this is a very aggressive invasive treatment therapy. So like we believe once an oral therapeutic is approved, I think patients will flock to it and that will certainly detract from the uptake of either Apellis drug or the Astellas/Iveric drug that just recently got approved. So we're not too concerned about the injectable therapeutics.

The Astellas/Iveric Bio drug Mata refers to is newly approved - in GA - therapy Izervay. The drug was developed by Iveric Bio and met endpoints in two pivotal studies in GA, which pointed to a 59% reduction in rate of vision loss at 12 months, before Iveric was acquired by Astellas in a $5.9bn deal. Analysts have speculated peak sales of the drug could reach $3bn per annum.

The list prices of Syfovre and Izervay are both ~$2,100 for a month's course of treatment, so if we assume an annual cost of ~$25k, and that Belite opts to use a similar price point to Astellas and Apellis, then the total addressable market in STGD1 could be ~$750m, while a 1% of a potential 20m patient market in GA would provide a peak sales opportunity of over $5bn.

Efficacy - Can Belite Match Injectable Efficacy?

Before Belite can even think about commercial sales, however, the company needs to prove its orally available drug can match up to its injectable rivals in a pivotal study. The drug has impressed the FDA so far, and has patent protection in place that ought to late into the middle of next decade, as Belite's Chairman and CEO told analysts on the company's last earnings call:

We have so far received fast track designation, rare pediatric disease designation, and orphan drug designation, which allows us to frequently discuss our progress with the FDA, and see how we can expedite the approval of this drug, if we show positive results from our Phase III study. I'd also like to mention that we still have a long patent life with the first composition of matter patent expiring in 2035 and patent extensions and new patents being filed, which will extend the patent portfolio into the 2050s

Most of the clinical proof of concept for Tinlarebant comes from the Phase 2 Open Label study, the design of which closely mirrors the design of the Phase 3 DRAGON study, as we can see below.

{kind=link}

Tinlarebant is derived from an anti-cancer drug, fenretinide, which went a long way to proving Belite's thesis that RBP4 suppression of over 70% leads to reduction in lesion growth rates, in studies conducted by CSO Mata in the past.

Tinlarebant was designed to address the twin weaknesses of fenretinide - bioavailability, and potency - while delivering the 70% RBP4 suppression the drug requires to have a positive effect on patient's vision. The open label data showed that the mean lesion growth rate in patients using Tinlarebant was 60% less than data collected from a previous study in 53 patients, as shown below.

{kind=link}

Tinlarebant was also shown to stabilise visual acuity, with no significant loss and no clinically significant changes in retinal thickness reported in the study, while the safety profile was also promising, although 75% of patients experienced mild and transient delayed Dark Adaptation and Xanthopsia/Chromatopsia.

Some questions remain unanswered however, such as how Tinlarebant will perform in a study with a placebo arm, as both DRAGON and PHOENIX will be, how the drug will perform in a much larger study - PHOENIX is a 400+ patient study - and whether the drug duration of response lasts a full two years. Tinlarebant is yet to meet a specific primary endpoint, and efficacy data in late-stage studies, if used to mount a New Drug Application ("NDA"), will be more thoroughly scrutinised for any potential flaws, as will the trial structure itself.

In terms of the injectable competition, according to an Apellis press release announcing the approval of Syfovre, in its two pivotal DERBY and OAKS studies:

SYFOVRE reduced the rate of GA lesion growth compared to sham and demonstrated increasing treatment effects over time, with the greatest benefit (up to 36% reduction in lesion growth with monthly treatment in DERBY) occurring between months 18-24

According to an Iveric Bio press release announcing the approval of Izervay:

The rate of GA growth was evaluated at baseline, 6 months, and 12 months. In each registrational trial, over a 12-month period, the primary analysis showed a statistically significant reduction in the rate of GA growth in patients treated with IZERVAY compared to sham. Slowing of disease progression was observed as early as 6 months with up to a 35% reduction in the first year of treatment.

The benchmark for approval then will likely be around the 35% lesion shrinkage mark, and Belite management suggested on the latest earnings call that Tinlarebant was achieving "about a 50% reduction in the combined lesion growth rate" at 18 months in the Open Label study.

If that suggests that both Phase 3 studies stand a good chance of success, then it should also be noted that trials are often different in character, and a larger patient set may deliver more varied results.

Management seems to believe Tinlarebant works better when treating patients with earlier forms of eye disease, although in the GA study especially, such patients may not be available. Even in a commercial setting, patients may not be diagnosed early enough for Tinlarebant to be fully efficacious. A further concern could be that the FDA concludes further studies are required before an approval can be granted - a risk Belite itself has acknowledged, that would significantly slow the company's progress, whilst eroding its first-mover advantage.

Concluding Thoughts - There Is Obvious Promise Here - A Speculative Buy & Hold Ahead of Key Data Readouts

Belite is not a large company, but its IPO has been a notable success to date and its lead drug candidate Tinlarebant has a differentiated mechanism of action ("MoA") and oral availability that could present an intriguing counterpoint to injectable therapies in a commercial setting.

Provided the drug can succeed in its two pivotal studies, it may not be unreasonable to consider Tinlarebant as a blockbuster-selling drug in waiting, in which case, Belite stock has to be substantially undervalued with a market cap under $1bn, even after the latest share price run-up.

A commercial stage Pharma typically trades at a value of 3-5 times revenues - if analysts are right and blockbuster sales are a strong likelihood within the GA market, then Belite's valuation could be 3-5x times what it is today in a few years' time so long as the company can show it is fulfilling that prediction.

Belite is not a cash rich company - cash position as of Q2 2023 was reported as just $43m. Net loss across the first half of 2023 was only $3.4m, however the costs of running pivotal late-stage studies may result in much higher costs going forward - I would not be surprised to see Belite raise a triple-digit million sum if its initial STGD1 data impresses, although in that event share price gains from the positive data ought to easily outweigh any losses due to subsequent dilution.

In summary, if Belite is able to successfully commercialise Tinlarebant - perhaps sometime in early 2025 - then the company surely deserves a valuation on par with e.g. Apellis - currently $3.7bn, or could become an M&A target for a larger Pharma with a price tag of anything up to $6bn - as Astellas paid for Iveric Bio.

With that said, of course, it's important to factor in the risks in play. The proof of concept for Tinlarebant seems to have been broadly established, but there are still many unanswered questions around safety and efficacy that will only be resolved once we have the pivotal study data.

If Tinlarebant is only effective in STGD1, for example, its target market would shrink and blockbuster sales would likely be out of reach. If the drug proved to be ineffective in both indications, investors would lose out heavily as the company is only developing one other asset, LBS-009 - an anti-RBP4 oral therapy targeting non-alcoholic fatty liver disease ("NAFLD"), nonalcoholic steatohepatitis ("NASH"), type 2 diabetes ("T2D" and gout. These are large target markets, but the drug has not yet entered the clinic and as such, carries very little value - Belite's fortunes are almost exclusively tied up in Tinlarebant.

Ultimately, after running the rule over Belite I'd be prepared to give the company a "Buy" recommendation, and believe the company can continue to buck the post-IPO bear trend for biotech companies, based on several factors.

Firstly, the successful approval of two therapies recently for GA suggests to me that this indication is becoming easier to address, thanks to a better understanding of what is required to treat the disease. As such, I think Belite, based on early Tinlarebant data, and the benchmarks for approval has a good shot at securing an approval for a clearly differentiated product to current standards of care.

Secondly, issues around injectables and adverse safety events make an obvious case for an orally available therapy in this market, and the recent issues highlighted by the ASRS around Syfovre plays straight into Belite's hands.

Thirdly, I am not aware of any close competition for Belite in the oral eye-disease therapy market - the company appears to be the leading horse in this race, with strong patent protection - and fourthly, based on the valuations of its rival GA drug developers, Apellis and Iveric, even discounting for the risks associated with waiting for pivotal study data, Belite stock should arguably be valued higher today - the closer we get to a key data readout - and the first one is due this year - the higher the price may rise.

A final positive for Belite is its potential access to the Chinese market - Tinlarebant has entered a Phase 3 study in China, being conducted by a Contract Research Organisation ("CRO"). It is hard to quantify the chances of successfully marketing and selling the drug in the region, but it adds to the overall value proposition - as do approval shots in Europe, the United Kingdom and Japan also - my understanding is Belite holds all global rights to the drug.

In conclusion, I think Belite is an interesting stock to watch - and potential buy - for the next several months as we await DRAGON data. Positive results open up the STGD1 market, and a peak ~$500m revenue opportunity, I'd expect, but also raises the prospect of a corresponding approval in GA, which would make Belite a far more valuable company than it is today, a momentum stock, and a potential acquisition target.

For further details see:

Belite Bio: The Pick Of The Post-IPO Biotechs - Is There Further Upside Ahead?